Composite Insulator Market

Composite Insulator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705234 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

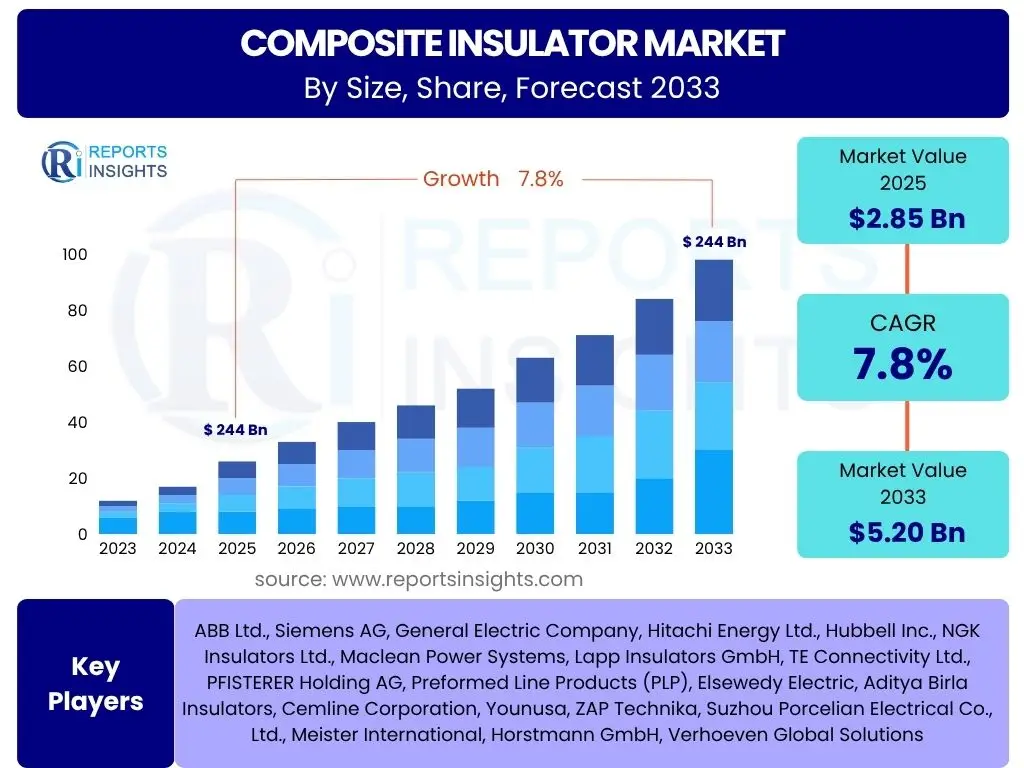

Composite Insulator Market Size

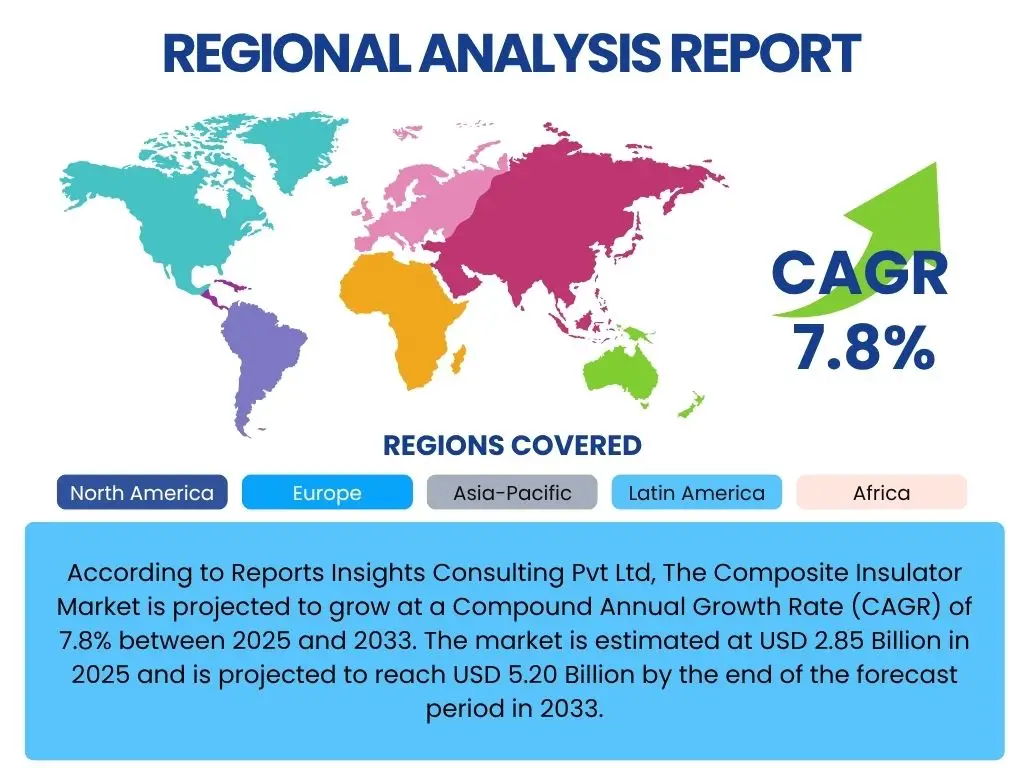

According to Reports Insights Consulting Pvt Ltd, The Composite Insulator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 5.20 Billion by the end of the forecast period in 2033.

Key Composite Insulator Market Trends & Insights

The Composite Insulator Market is undergoing significant transformation driven by a confluence of technological advancements, environmental imperatives, and expanding infrastructure needs. A primary trend involves the increasing global adoption of smart grid technologies, which necessitate high-performance, durable, and low-maintenance insulation solutions. Composite insulators, with their inherent advantages in terms of weight, hydrophobicity, and resistance to environmental degradation, are ideally suited for these modern grid applications, particularly in mitigating power outages and enhancing grid reliability. Furthermore, the rapid expansion of renewable energy sources, such as wind and solar farms, often located in remote or challenging environments, fuels the demand for composite insulators capable of withstanding extreme weather conditions and reducing maintenance cycles.

Another prominent insight is the growing emphasis on sustainable and resilient infrastructure. Governments and utilities worldwide are investing heavily in upgrading aging transmission and distribution networks to improve efficiency and reduce carbon footprint. This push aligns perfectly with the benefits offered by composite insulators, which are lighter, easier to install, and boast a longer operational life compared to traditional ceramic or glass insulators. Innovations in material science, leading to enhanced performance and reduced costs, further accelerate their market penetration. The trend towards ultra-high voltage (UHV) transmission lines also mandates the use of advanced insulation materials, where composite insulators demonstrate superior flashover performance and reduced leakage currents, cementing their role in the future of power transmission.

- Global shift towards smart grid infrastructure and automation.

- Rapid integration of renewable energy sources into existing grids.

- Increased investment in grid modernization and expansion projects.

- Technological advancements in polymer materials and manufacturing processes.

- Growing demand for lightweight, durable, and environmentally friendly insulation solutions.

- Emergence of ultra-high voltage (UHV) transmission lines necessitating advanced insulation.

AI Impact Analysis on Composite Insulator

Artificial intelligence (AI) is poised to significantly transform the Composite Insulator Market by optimizing various stages of the product lifecycle and operational deployment. Users frequently inquire about AI's role in predictive maintenance, quality control, and design optimization. AI algorithms can analyze vast datasets from grid sensors, weather patterns, and historical performance to predict potential insulator failures before they occur, enabling proactive maintenance and minimizing costly downtime. This shift from reactive to predictive maintenance enhances grid reliability and extends the operational lifespan of composite insulators. Additionally, AI-powered visual inspection systems, utilizing drones and computer vision, can identify defects or damage on insulators more efficiently and accurately than manual methods, particularly in remote or hazardous locations.

Beyond operational efficiencies, AI also holds immense promise in the design and manufacturing phases of composite insulators. Generative design AI can explore a multitude of material combinations and structural configurations to optimize insulator performance, weight, and cost, accelerating the development of next-generation products. Machine learning models can be employed to monitor and control manufacturing processes in real-time, ensuring consistent product quality, reducing waste, and improving production efficiency. Furthermore, AI can assist in supply chain optimization by forecasting demand, managing inventory, and streamlining logistics for raw materials and finished products, leading to more resilient and cost-effective operations within the composite insulator industry. The integration of AI therefore represents a paradigm shift towards smarter, more efficient, and more reliable power infrastructure.

- Predictive maintenance for insulator health monitoring and failure prevention.

- AI-powered visual inspection and damage detection using drones and computer vision.

- Optimization of manufacturing processes for improved quality and reduced waste.

- Enhanced material design and innovation through generative AI and simulation.

- Supply chain optimization and demand forecasting for efficient resource management.

- Development of smart insulators with integrated sensors and AI for real-time performance monitoring.

Key Takeaways Composite Insulator Market Size & Forecast

The Composite Insulator Market is on a robust growth trajectory, primarily driven by global energy demand, grid modernization efforts, and the inherent superior performance attributes of composite materials over traditional insulators. A critical takeaway is the escalating investment in renewable energy infrastructure, which inherently favors composite insulators due to their lightweight nature, resistance to environmental degradation, and ease of installation in diverse and often challenging geographical locations. This sustained push for green energy and the accompanying grid reinforcement projects will remain a pivotal growth catalyst throughout the forecast period. Furthermore, the market's expansion is significantly bolstered by the replacement of aging infrastructure in developed economies and the rapid electrification initiatives in developing regions, both of which require reliable, long-lasting, and efficient insulation solutions.

Another significant takeaway is the increasing technological sophistication within the industry, leading to higher performance standards and broader application potential for composite insulators. Innovations in polymer science, such as enhanced silicone rubber formulations, are improving the hydrophobicity, UV resistance, and overall longevity of these insulators, making them suitable for even the most extreme environmental conditions. The market's future is also shaped by a rising awareness among utilities regarding the long-term cost benefits of composite insulators, including reduced maintenance expenses and fewer unscheduled outages. This comprehensive understanding of their total cost of ownership, combined with regulatory support for more resilient and sustainable grid components, solidifies the market's positive outlook, projecting substantial expansion across various voltage levels and end-use applications through 2033.

- Significant growth expected due to global energy demand and grid modernization.

- Renewable energy integration is a primary driver for composite insulator adoption.

- Aging infrastructure replacement and new electrification projects fuel market expansion.

- Technological advancements in material science enhance product performance and lifespan.

- Cost-benefit analysis favors composite insulators due to lower maintenance and higher reliability.

- Emerging economies in APAC and Latin America present substantial growth opportunities.

Composite Insulator Market Drivers Analysis

The Composite Insulator Market is propelled by several key drivers that reflect the evolving needs of global power infrastructure. The paramount driver is the worldwide push for grid modernization and expansion, aimed at improving the reliability, efficiency, and capacity of electricity networks. As utilities invest in smart grids and upgrade legacy systems, the demand for high-performance, low-maintenance components like composite insulators escalates due to their superior dielectric properties, lighter weight, and resistance to pollution and vandalism. This modernization is critical for accommodating the growing demand for electricity, especially in rapidly urbanizing areas and industrial zones.

Another significant driver is the rapid integration of renewable energy sources, such as wind and solar, into the main power grid. These installations often require transmission lines in remote or environmentally challenging locations where the lightweight and robust nature of composite insulators offers distinct advantages in terms of installation ease, reduced structural costs, and resilience to harsh weather. Furthermore, environmental concerns and stricter regulatory frameworks worldwide are prompting a shift away from traditional ceramic and glass insulators, which can be heavier and more prone to breakage, towards more environmentally friendly and resilient composite alternatives. The superior performance of composite insulators in polluted or humid environments also makes them a preferred choice for enhancing grid resilience in climate-vulnerable regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Modernization and Expansion | +2.1% | North America, Europe, APAC | 2025-2033 |

| Integration of Renewable Energy Sources | +1.8% | Europe, Asia Pacific, North America | 2025-2033 |

| Superior Performance Over Traditional Insulators | +1.5% | Global | 2025-2033 |

| Urbanization and Industrialization | +1.2% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Investment in Ultra-High Voltage (UHV) Lines | +0.9% | China, India, Brazil | 2028-2033 |

Composite Insulator Market Restraints Analysis

Despite the strong growth drivers, the Composite Insulator Market faces certain restraints that could impact its expansion. A significant limiting factor is the higher initial cost of composite insulators compared to conventional ceramic or glass alternatives. While composite insulators offer long-term cost benefits through reduced maintenance and extended lifespan, the upfront investment can be a deterrent for some utilities or projects, particularly in budget-constrained regions. This cost disparity can slow down adoption rates, especially for bulk replacement projects where the sheer volume can magnify initial expenditure concerns.

Another restraint involves the challenges associated with the lack of standardization and testing protocols across various regions. While progress has been made, differences in material specifications, design parameters, and quality control measures can create complexities for manufacturers and end-users alike. This can lead to issues related to interoperability, perceived reliability, and increased scrutiny during procurement. Furthermore, the relatively nascent stage of composite insulator technology compared to traditional options means that long-term performance data in certain extreme conditions or over extended decades of service is still accumulating, leading to a degree of hesitation among some conservative utility operators who prioritize proven longevity and familiarity. The issues related to potential brittle fracture in certain older designs or specific environmental conditions, though largely addressed in modern composites, can also contribute to this hesitancy, requiring continuous research and robust product development to overcome.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Initial Cost Compared to Traditional Insulators | -1.5% | Global, particularly Emerging Economies | 2025-2030 |

| Lack of Standardized Testing and Certification | -0.8% | Global | 2025-2029 |

| Perceived Longevity and Reliability Concerns for Some Utilities | -0.6% | North America, Europe | 2025-2028 |

| Challenges in Recycling and Disposal of Composite Materials | -0.4% | Europe, North America | 2028-2033 |

Composite Insulator Market Opportunities Analysis

The Composite Insulator Market is poised to capitalize on several significant opportunities driven by evolving global energy landscapes and technological advancements. One primary opportunity lies in the burgeoning smart grid initiatives worldwide. As electricity networks become increasingly digitized and automated, there is a growing demand for components that can integrate seamlessly with advanced monitoring and control systems. Composite insulators, with their potential for embedded sensors and smart functionalities, offer a distinct advantage in enabling real-time performance monitoring and predictive maintenance, thereby enhancing grid resilience and efficiency. This shift towards intelligent infrastructure creates a fertile ground for market growth, especially in developed economies investing heavily in modernizing their grid networks.

Another substantial opportunity resides in the expansion of high-voltage direct current (HVDC) transmission lines and ultra-high voltage (UHV) alternating current (AC) lines. These critical components of modern long-distance power transmission require insulators with exceptional dielectric strength, reduced leakage currents, and superior pollution performance, characteristics where composite insulators demonstrably outperform traditional alternatives. The increasing investment in HVDC/UHV projects, particularly in countries with large geographical expanses or those pursuing long-distance power evacuation from renewable energy hubs, presents a niche yet high-value market segment. Furthermore, the continuous research and development in advanced polymer composites offer opportunities for creating even more durable, lightweight, and cost-effective insulators, pushing the boundaries of their application and expanding their competitive edge against conventional materials. Lastly, the significant potential for replacing millions of aging ceramic and glass insulators globally, particularly in areas prone to environmental stress or vandalism, provides a sustained aftermarket growth opportunity for composite insulator manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart Grid Technologies | +1.7% | North America, Europe, China | 2025-2033 |

| Growth of High Voltage Direct Current (HVDC) and UHV AC Lines | +1.4% | China, India, Brazil, Europe | 2026-2033 |

| Replacement of Aging Traditional Insulator Infrastructure | +1.1% | Global | 2025-2033 |

| Technological Advancements in Material Science | +0.9% | Global | 2025-2033 |

| Expansion in Remote and Harsh Environment Applications | +0.7% | Global | 2025-2033 |

Composite Insulator Market Challenges Impact Analysis

The Composite Insulator Market faces distinct challenges that can impede its otherwise promising growth trajectory. One significant challenge is the intense competition from established traditional insulator manufacturers and the availability of lower-cost alternatives, especially in price-sensitive markets. While composite insulators offer long-term value, the upfront cost can be a barrier, leading some utilities to opt for conventional ceramic or glass insulators for initial installations or basic replacements, particularly in regions where budget constraints are severe. This price competition necessitates continuous innovation and cost optimization from composite insulator manufacturers to maintain their competitive edge.

Another critical challenge revolves around the raw material supply chain. The primary raw materials for composite insulators, such as silicone rubber, fiberglass rods, and metal fittings, can be subject to price volatility and supply disruptions due to global market dynamics, geopolitical events, or natural disasters. Such instability can impact manufacturing costs, lead times, and ultimately, the profitability of composite insulator producers. Furthermore, while composite insulators generally boast superior performance, concerns regarding their long-term degradation mechanisms, particularly in specific environmental conditions (e.g., prolonged UV exposure, severe pollution, or extreme temperature cycling), require ongoing research and rigorous field validation to fully assuage. Addressing these long-term performance perceptions and ensuring robust, reliable supply chains are crucial for sustained market confidence and widespread adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Sensitivity | -1.2% | Global, particularly Emerging Economies | 2025-2033 |

| Raw Material Price Volatility and Supply Chain Disruptions | -0.9% | Global | 2025-2030 |

| Perception of Limited Long-Term Field Performance Data | -0.7% | North America, Europe | 2025-2028 |

| Stringent Regulatory and Certification Requirements | -0.5% | Global | 2025-2033 |

Composite Insulator Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Composite Insulator Market, covering market size estimations, historical data, and future growth projections up to 2033. It examines key market trends, drivers, restraints, opportunities, and challenges influencing the industry's trajectory. The report also includes a detailed segmentation analysis, regional insights, and profiles of leading market players, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 5.20 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, General Electric Company, Hitachi Energy Ltd., Hubbell Inc., NGK Insulators Ltd., Maclean Power Systems, Lapp Insulators GmbH, TE Connectivity Ltd., PFISTERER Holding AG, Preformed Line Products (PLP), Elsewedy Electric, Aditya Birla Insulators, Cemline Corporation, Younusa, ZAP Technika, Suzhou Porcelian Electrical Co., Ltd., Meister International, Horstmann GmbH, Verhoeven Global Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Composite Insulator Market is comprehensively segmented based on material, voltage level, application, and end-use industry, reflecting the diverse requirements and technological advancements within the power transmission and distribution sector. Each segment plays a crucial role in shaping market dynamics, with specific material types offering distinct performance characteristics, and varying voltage levels dictating design and manufacturing complexities. The broad range of applications, from critical transmission infrastructure to localized industrial use, further highlights the versatility and growing adoption of composite insulators across the global energy landscape.

Understanding these segmentations is vital for stakeholders to identify niche markets, assess competitive landscapes, and formulate targeted strategies. For instance, the demand for silicone-based composite insulators is driven by their superior hydrophobicity and pollution resistance, while ultra-high voltage applications require highly specialized designs. The utilities sector remains the largest end-user, but industrial and railway applications are showing increasing adoption, indicating diversification of market opportunities. This detailed breakdown allows for a granular analysis of market trends and growth prospects within each specific category.

- By Material:

- Silicone

- EPDM (Ethylene Propylene Diene Monomer)

- Others (e.g., Hybrid Polymers)

- By Voltage Level:

- Low Voltage (Up to 1 kV)

- Medium Voltage (1 kV to 69 kV)

- High Voltage (70 kV to 220 kV)

- Extra High Voltage (221 kV to 800 kV)

- Ultra High Voltage (Above 800 kV)

- By Application:

- Transmission Lines

- Distribution Lines

- Substations

- Railways

- Industrial Applications (e.g., factories, specialized plants)

- By End-Use Industry:

- Utilities (Power Generation, Transmission, Distribution Companies)

- Industrial (Oil & Gas, Mining, Manufacturing, Construction)

- Railways (Metro, High-Speed Rail, Conventional Rail)

- Residential (Indirectly through grid connections)

Regional Highlights

- North America: This region is characterized by significant investments in grid modernization and the replacement of aging infrastructure. The United States and Canada are driving demand for composite insulators due to increasing renewable energy integration, smart grid initiatives, and the need for resilient power systems against extreme weather events. Regulatory support for advanced grid technologies further propels market growth, particularly in EHV and UHV applications aimed at long-distance power transmission.

- Europe: Europe is a mature market focusing heavily on renewable energy deployment, including offshore wind farms, and strengthening cross-border interconnections. Stringent environmental regulations and a strong emphasis on reducing carbon emissions favor the adoption of lightweight, eco-friendly composite insulators. Countries like Germany, France, and the UK are at the forefront of investing in advanced grid components and smart grid technologies, driving demand for high-performance insulators.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market due to rapid industrialization, urbanization, and vast infrastructure development projects, particularly in countries like China, India, Japan, and Southeast Asian nations. Significant investments in power generation capacity expansion, rural electrification programs, and the establishment of new transmission and distribution networks are fueling immense demand. The region's diverse geographical conditions also benefit from the superior pollution performance and lightweight characteristics of composite insulators.

- Latin America: This region is experiencing considerable growth driven by increasing electricity demand, grid expansion projects, and the modernization of existing power infrastructure. Countries like Brazil, Mexico, and Argentina are investing in renewable energy sources and improving grid reliability. The challenging terrains and diverse climates in some parts of Latin America make composite insulators a preferred choice due to their robust performance and ease of installation.

- Middle East and Africa (MEA): The MEA region is witnessing substantial growth driven by large-scale power infrastructure development projects, driven by economic diversification efforts and growing energy consumption. Gulf Cooperation Council (GCC) countries are investing heavily in new power plants and transmission networks. Africa's vast potential for renewable energy and ongoing electrification initiatives across the continent are creating significant opportunities for composite insulators, especially for extending grid access to remote areas and improving grid stability in challenging environments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Composite Insulator Market.- ABB Ltd.

- Siemens AG

- General Electric Company

- Hitachi Energy Ltd.

- Hubbell Inc.

- NGK Insulators Ltd.

- Maclean Power Systems

- Lapp Insulators GmbH

- TE Connectivity Ltd.

- PFISTERER Holding AG

- Preformed Line Products (PLP)

- Elsewedy Electric

- Aditya Birla Insulators

- Cemline Corporation

- Younusa

- ZAP Technika

- Suzhou Porcelian Electrical Co., Ltd.

- Meister International

- Horstmann GmbH

- Verhoeven Global Solutions

Frequently Asked Questions

What are composite insulators and how do they differ from traditional insulators?

Composite insulators are advanced electrical insulators made from a fiberglass core, polymer housing (e.g., silicone rubber), and metal end fittings. They differ from traditional ceramic or glass insulators by being lighter, more resistant to pollution flashover, hydrophobic, and less prone to breakage, offering enhanced performance and reduced maintenance needs.

What is the projected growth rate of the Composite Insulator Market?

The Composite Insulator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, driven by increasing grid modernization, renewable energy integration, and superior material performance.

What are the key drivers for the Composite Insulator Market?

Key drivers include global grid modernization and expansion, the rapid integration of renewable energy sources, the superior performance attributes of composite materials over traditional insulators, and increased investment in ultra-high voltage (UHV) transmission lines.

Which regions are expected to show significant growth in the Composite Insulator Market?

The Asia Pacific (APAC) region is expected to be the fastest-growing market due to extensive infrastructure development and electrification projects, followed by strong growth in North America and Europe driven by grid modernization and renewable energy initiatives.

How is AI impacting the Composite Insulator Market?

AI is impacting the market by enabling predictive maintenance for insulators, optimizing manufacturing processes, assisting in material design, and enhancing supply chain efficiency, leading to more reliable and cost-effective grid operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted