SAW and BAW Filter Market

SAW and BAW Filter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703655 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

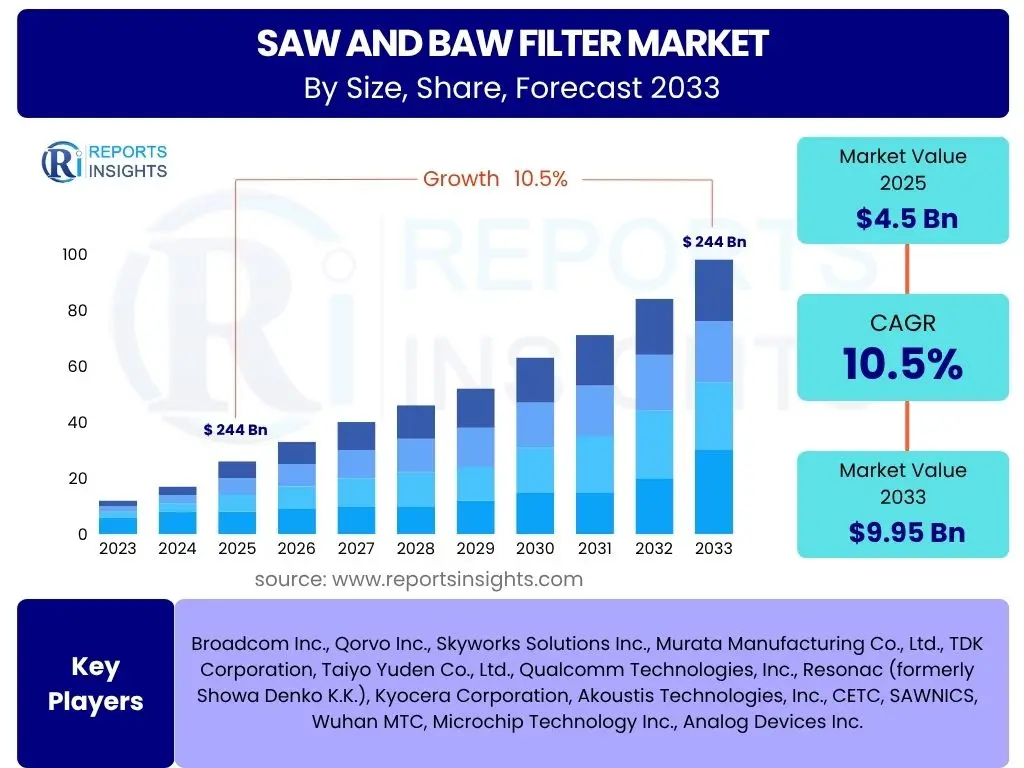

SAW and BAW Filter Market Size

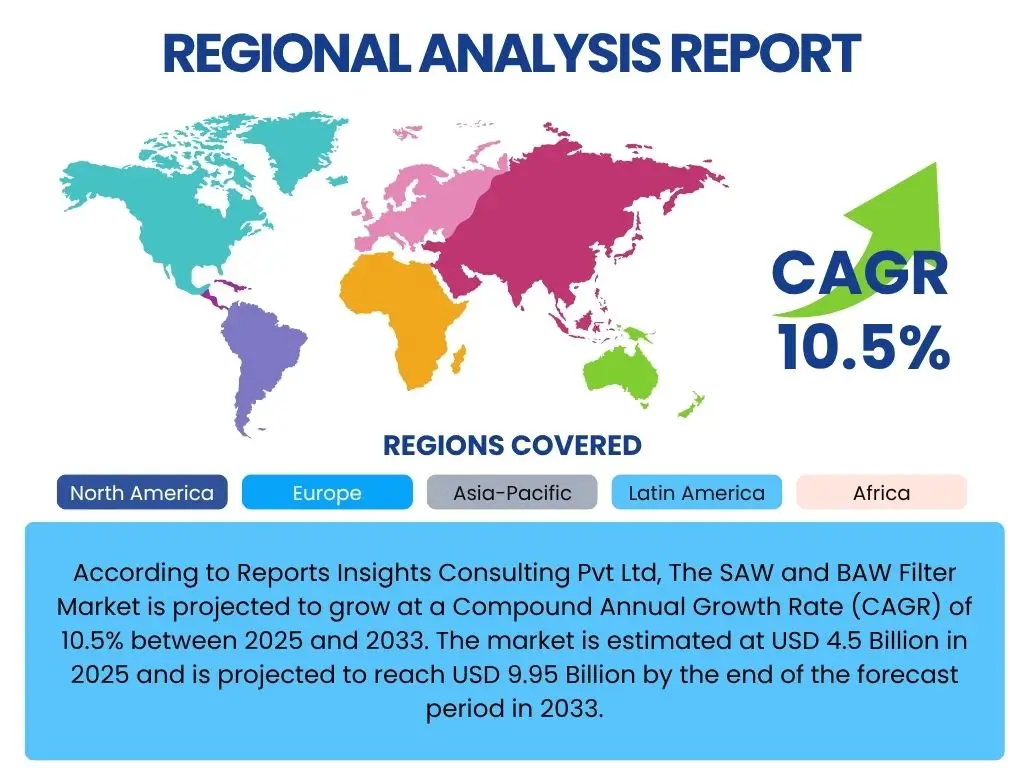

According to Reports Insights Consulting Pvt Ltd, The SAW and BAW Filter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 9.95 Billion by the end of the forecast period in 2033.

Key SAW and BAW Filter Market Trends & Insights

The SAW (Surface Acoustic Wave) and BAW (Bulk Acoustic Wave) filter market is experiencing robust expansion, primarily driven by the global proliferation of 5G networks and the increasing demand for high-performance RF components in connected devices. Industry stakeholders are observing a significant shift towards more compact, efficient, and higher-frequency filters, essential for enabling advanced wireless communication standards and miniaturization across various electronic applications. This trend is further fueled by the rising complexity of smartphone architectures, the rapid growth of the Internet of Things (IoT) ecosystem, and the escalating integration of sophisticated electronics in automotive systems, all of which necessitate superior signal processing and interference management capabilities.

Technological advancements in filter design and manufacturing processes are also playing a crucial role in shaping market dynamics. Innovations such as the development of ultra-wideband filters, reconfigurable filters, and advanced packaging techniques are addressing the challenges of higher frequency bands and multi-band communication. Furthermore, the push for enhanced power efficiency and reduced latency in next-generation devices is compelling manufacturers to invest in research and development, leading to filters with improved insertion loss and steeper rejection characteristics. These ongoing innovations are critical for maintaining signal integrity in increasingly crowded RF spectrums, thereby securing the market's long-term growth trajectory.

- Accelerated global deployment of 5G infrastructure and devices.

- Increasing demand for miniaturized and high-performance RF filters.

- Growing adoption of IoT devices across diverse sectors.

- Expansion of advanced driver-assistance systems (ADAS) and connected car technologies.

- Development of filters supporting new and higher frequency bands (e.g., mmWave).

- Focus on energy-efficient and low-latency filter solutions.

AI Impact Analysis on SAW and BAW Filter

The integration of Artificial Intelligence (AI) is transforming various facets of the SAW and BAW filter industry, primarily influencing design, manufacturing, and the applications that drive filter demand. Users frequently inquire about how AI can optimize filter performance and reduce development cycles. AI algorithms, particularly machine learning and deep learning, are being increasingly employed in the early stages of filter design to simulate, predict, and optimize acoustic wave propagation characteristics, material selections, and physical layouts. This allows for faster iteration, identification of optimal designs, and a significant reduction in time-to-market for new filter products, addressing the urgent need for custom solutions in a rapidly evolving technological landscape.

Furthermore, AI plays a pivotal role in enhancing the manufacturing efficiency and quality control of SAW and BAW filters. Predictive analytics and machine vision systems, powered by AI, are utilized to monitor production lines, detect anomalies, and forecast equipment failures, thereby minimizing downtime and improving yield rates. The demand for these filters is also indirectly impacted by AI, as the proliferation of AI-powered devices, such as autonomous vehicles, smart home devices, and advanced robotics, creates a cascading effect of increased demand for high-precision, reliable RF front-end modules that incorporate these filters. As AI continues to become more pervasive in end-user applications, the demand for sophisticated SAW and BAW filters capable of supporting complex data transmission and communication will continue to grow.

- AI-driven optimization of SAW and BAW filter design parameters, accelerating development.

- Enhanced manufacturing processes through AI-powered predictive maintenance and quality control.

- Increased demand for filters stemming from the proliferation of AI-enabled devices (e.g., autonomous vehicles, smart cities, advanced robotics).

- AI algorithms aiding in rapid prototyping and material selection for improved filter performance.

- Potential for AI to enable adaptive and reconfigurable filters for dynamic RF environments.

Key Takeaways SAW and BAW Filter Market Size & Forecast

The SAW and BAW filter market is poised for substantial growth over the next decade, with a projected CAGR highlighting its critical role in the advancement of modern communication technologies. A primary takeaway is the undeniable influence of 5G deployment, which acts as the strongest catalyst for market expansion, driving the need for filters capable of operating at higher frequencies and managing complex signal environments. Beyond 5G, the widespread adoption of IoT devices and the rapid evolution of automotive electronics are significant contributors, ensuring a broad and diversified demand base for these essential components across various sectors.

Another crucial insight is the continuous innovation within filter technology, which is paramount to sustaining market momentum. Manufacturers are actively pursuing advancements in material science, design methodologies, and packaging techniques to meet the ever-increasing performance demands. This commitment to research and development is crucial for overcoming technical challenges associated with miniaturization and high-frequency operation, ensuring that SAW and BAW filters remain indispensable in the evolving wireless ecosystem. The market's resilience and growth are thus intrinsically linked to ongoing technological breakthroughs and the ability to adapt to new application requirements.

- Significant market growth forecast, driven predominantly by 5G expansion.

- Increasing integration of SAW/BAW filters in diverse applications like IoT and automotive.

- Continuous technological advancements crucial for meeting performance demands and market evolution.

- Market resilience despite economic fluctuations due to fundamental role in connectivity.

- Shift towards higher frequency and compact filter solutions.

SAW and BAW Filter Market Drivers Analysis

The global rollout of 5G technology stands as the paramount driver for the SAW and BAW filter market. 5G networks demand significantly higher frequencies, greater bandwidths, and lower latencies, which necessitates advanced RF front-end modules incorporating high-performance filters. Both SAW and BAW filters are uniquely positioned to meet these stringent requirements, with BAW filters particularly suited for higher frequency bands (above 2 GHz) critical for 5G mmWave applications. The widespread adoption of 5G-enabled smartphones, IoT devices, and infrastructure equipment directly translates into increased demand for these sophisticated filters, impacting various regional markets globally as 5G penetration deepens.

Beyond 5G, the burgeoning ecosystem of the Internet of Things (IoT) and the rapid advancements in automotive electronics are significant market accelerators. IoT devices, ranging from smart home appliances to industrial sensors, require compact and energy-efficient filters for reliable wireless communication. Similarly, the automotive industry's shift towards connected cars, autonomous driving systems, and advanced infotainment systems mandates robust and high-temperature tolerant filters for cellular connectivity, GPS, and other communication modules. These sectors, characterized by continuous innovation and expanding application areas, provide a sustained growth impetus for the SAW and BAW filter market across all major geographical regions, influencing short to long-term market forecasts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Deployment | +2.5% | Global (North America, APAC, Europe) | Short to Medium Term (2025-2029) |

| Increasing IoT Device Proliferation | +1.8% | Global (APAC, North America, Europe) | Medium to Long Term (2027-2033) |

| Growth in Automotive Electronics | +1.5% | Europe, North America, APAC (China, Japan) | Medium to Long Term (2026-2033) |

| Miniaturization Trends in Consumer Electronics | +1.2% | Global (APAC, North America) | Short to Medium Term (2025-2030) |

| Demand for High-Performance RF Modules | +1.0% | Global | Ongoing (2025-2033) |

SAW and BAW Filter Market Restraints Analysis

The high manufacturing cost associated with advanced SAW and BAW filters, particularly those designed for high frequencies and stringent performance requirements, poses a significant restraint on market expansion. The fabrication processes for these filters involve intricate lithography, precise material deposition, and specialized packaging, all of which contribute to elevated production expenses. This cost factor can limit widespread adoption in price-sensitive applications or emerging markets, potentially favoring alternative, less expensive filter technologies in certain segments. While demand for premium filters remains strong in flagship devices, cost pressures can impact profit margins and slow down penetration into lower-tier device categories, particularly in developing regions.

Another notable restraint is the inherent complexity in designing and manufacturing filters for increasingly crowded and higher frequency spectrums. As communication technologies evolve, the specifications for rejection, bandwidth, and insertion loss become more demanding, pushing the limits of current design methodologies and material properties. This technical complexity requires significant investment in research and development, highly skilled labor, and specialized equipment, making it challenging for new entrants and potentially slowing down innovation cycles. Furthermore, geopolitical uncertainties and supply chain vulnerabilities, exacerbated by recent global events, introduce risks related to raw material availability and manufacturing capacity, potentially causing production delays and price volatility for critical components.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs | -0.9% | Global (Emerging Economies) | Ongoing (2025-2033) |

| Technical Complexity in High-Frequency Design | -0.7% | Global | Ongoing (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Tensions | -0.6% | Global (Specific manufacturing hubs in APAC) | Short to Medium Term (2025-2028) |

| Competition from Alternative Filter Technologies (e.g., Ceramic, LC) | -0.5% | Global (Low-end/Cost-sensitive applications) | Ongoing (2025-2033) |

SAW and BAW Filter Market Opportunities Analysis

The emergence of new frequency bands and the ongoing evolution of wireless communication standards present significant growth opportunities for the SAW and BAW filter market. Beyond the current focus on 5G sub-6 GHz and mmWave, future communication technologies, including 6G research and satellite communication systems, will require even more advanced and specialized filters capable of handling extremely high frequencies and complex signal environments. This necessitates continuous innovation in filter design, material science, and packaging, creating avenues for manufacturers to develop next-generation solutions. Furthermore, the increasing complexity of multi-band, multi-mode devices across consumer electronics and industrial applications drives demand for highly integrated and reconfigurable filter modules, opening new product development pathways.

Untapped and emerging markets also represent considerable opportunities for market expansion. While established markets in North America, Europe, and developed APAC countries show strong growth, regions in Latin America, Middle East, and Africa are experiencing increasing smartphone penetration and infrastructure development. These regions, as they progressively adopt 4G and 5G technologies, will generate substantial demand for cost-effective yet reliable SAW and BAW filters. Moreover, the diversification of filter applications into new sectors such as industrial automation, smart agriculture, and advanced medical devices, coupled with the potential for strategic partnerships and mergers and acquisitions, offers avenues for market players to expand their global footprint and diversify revenue streams, contributing positively to the overall market CAGR over the forecast period.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Frequency Bands (e.g., 6G, Satellite Communication) | +1.5% | Global | Medium to Long Term (2028-2033) |

| Untapped Markets (Emerging Economies) for 4G/5G Rollout | +1.2% | Latin America, MEA, Southeast Asia | Medium Term (2026-2031) |

| Integration with AI and Machine Learning for Smart/Adaptive Filters | +1.0% | Global | Medium to Long Term (2027-2033) |

| Diversification into Industrial and Medical IoT Applications | +0.8% | North America, Europe, Developed APAC | Medium to Long Term (2027-2033) |

| Strategic Partnerships and Collaborations for R&D | +0.7% | Global | Ongoing (2025-2033) |

SAW and BAW Filter Market Challenges Impact Analysis

The SAW and BAW filter market faces significant challenges due to intense competition and the rapid pace of technological obsolescence. The market is dominated by a few major players who continuously invest heavily in R&D to maintain their competitive edge. This creates a challenging environment for smaller companies and new entrants, as they struggle to keep up with the rapid innovation cycles and significant capital investments required for advanced filter manufacturing. Furthermore, the rapid evolution of wireless communication standards and device architectures means that filter designs can become obsolete quickly, necessitating constant adaptation and redevelopment, which puts pressure on product lifecycles and profitability, particularly for mass-produced consumer electronics.

Another critical challenge is the inherent technical complexity and stringent performance requirements for filters operating in increasingly crowded and higher frequency spectrums. Designing filters that offer optimal performance (e.g., low insertion loss, high rejection, wide bandwidth) while also meeting miniaturization demands is a continuous engineering hurdle. Achieving this requires highly specialized expertise, advanced simulation tools, and sophisticated fabrication techniques. Additionally, geopolitical factors, including trade disputes and export controls on critical technologies or raw materials, can disrupt supply chains and increase the cost of production, directly impacting market stability and the ability of manufacturers to deliver products efficiently and on time, thereby influencing the overall market CAGR.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition Among Key Players | -0.8% | Global | Ongoing (2025-2033) |

| Rapid Technological Obsolescence | -0.7% | Global | Short to Medium Term (2025-2029) |

| Complexities in High-Frequency Design and Manufacturing | -0.6% | Global | Ongoing (2025-2033) |

| Strict Regulatory Standards and Certification Processes | -0.4% | North America, Europe, APAC (China, Japan) | Ongoing (2025-2033) |

| Skilled Labor Shortage in Advanced RF Engineering | -0.3% | Global | Medium to Long Term (2027-2033) |

SAW and BAW Filter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global SAW and BAW filter market, covering historical market performance from 2019 to 2023, with detailed projections extending to 2033. The scope encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. It also includes extensive segmentation analysis across various dimensions, detailed regional insights, and profiles of key industry players, offering strategic intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 9.95 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Broadcom Inc., Qorvo Inc., Skyworks Solutions Inc., Murata Manufacturing Co., Ltd., TDK Corporation, Taiyo Yuden Co., Ltd., Qualcomm Technologies, Inc., Resonac (formerly Showa Denko K.K.), Kyocera Corporation, Akoustis Technologies, Inc., CETC, SAWNICS, Wuhan MTC, Microchip Technology Inc., Analog Devices Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The SAW and BAW filter market is comprehensively segmented to provide a nuanced understanding of its diverse components and applications. Segmentation by filter type distinguishes between SAW (Surface Acoustic Wave) filters, typically used for frequencies below 2.5 GHz, and BAW (Bulk Acoustic Wave) filters, which are more suitable for higher frequencies (above 2 GHz), particularly for 5G and Wi-Fi applications. This distinction is critical as it highlights the technological capabilities and market positioning of different filter solutions based on their fundamental operating principles and material properties. The growing demand for higher frequency capabilities is increasingly favoring BAW filter solutions, especially in advanced communication systems.

Further segmentation by application provides insights into the primary end-use industries driving market demand. Smartphones continue to represent the largest application segment, demanding an increasing number of filters per device due to growing band complexity. However, significant growth is also observed in emerging areas such as automotive electronics, including ADAS and connected car systems, as well as the rapidly expanding Internet of Things (IoT) ecosystem, which encompasses a wide array of consumer and industrial devices. Additional segments, including telecommunications infrastructure, industrial applications, and healthcare, also contribute to the market's overall dynamism, illustrating the pervasive need for precise and reliable frequency filtering across various sectors.

- By Filter Type: SAW Filters, BAW Filters

- By Application: Smartphones, Tablets, Wearables, Automotive (ADAS, Infotainment, Telematics), IoT Devices (Consumer, Industrial), Telecommunications Infrastructure (Base Stations, Small Cells), Industrial, Healthcare, Aerospace & Defense

- By Frequency Range: Below 1 GHz, 1 GHz - 6 GHz, Above 6 GHz (mmWave)

- By Material: Quartz, Lithium Niobate (LiNbO3), Lithium Tantalate (LiTaO3), Sapphire, Silicon

Regional Highlights

- Asia Pacific (APAC): APAC is anticipated to remain the dominant market for SAW and BAW filters, driven by its robust manufacturing base for consumer electronics, particularly smartphones, and the accelerated deployment of 5G networks in countries like China, South Korea, and Japan. The region also benefits from a large and rapidly expanding IoT ecosystem and increasing investments in telecommunications infrastructure.

- North America: This region is characterized by significant investments in advanced telecommunications infrastructure, including extensive 5G rollout, and a strong presence of key technology innovators. The demand for high-performance filters is also propelled by the growing adoption of connected devices, advanced automotive electronics, and increasing R&D activities in aerospace and defense applications.

- Europe: Europe represents a mature market with a strong emphasis on automotive electronics, industrial IoT, and the development of next-generation communication standards. Countries like Germany and France are leading in automotive technological advancements, contributing significantly to the demand for high-reliability filters in connected vehicles.

- Latin America: This region is expected to demonstrate steady growth, primarily fueled by increasing smartphone penetration, ongoing expansion of 4G and nascent 5G networks, and a growing adoption of IoT devices in various sectors, though from a smaller base compared to developed regions.

- Middle East and Africa (MEA): The MEA region is emerging as a growth market, driven by increasing government initiatives for digital transformation, rising smartphone usage, and investments in telecommunications infrastructure development, particularly in GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the SAW and BAW Filter Market.- Broadcom Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- Qualcomm Technologies, Inc.

- Resonac (formerly Showa Denko K.K.)

- Kyocera Corporation

- Akoustis Technologies, Inc.

- CETC

- SAWNICS

- Wuhan MTC

- Microchip Technology Inc.

- Analog Devices Inc.

Frequently Asked Questions

What are SAW and BAW filters and how do they work?

SAW (Surface Acoustic Wave) and BAW (Bulk Acoustic Wave) filters are critical radio frequency (RF) components used to filter specific frequency signals. SAW filters operate by converting electrical signals into acoustic waves on the surface of a piezoelectric substrate, which are then converted back into electrical signals. BAW filters, conversely, use bulk acoustic waves traveling perpendicular to the substrate surface. Both types excel at precise frequency selection and interference rejection in wireless communication systems.

Why are SAW and BAW filters essential for 5G technology?

SAW and BAW filters are essential for 5G because they enable the precise frequency selection and rejection required for the high-frequency bands and massive bandwidths characteristic of 5G networks. BAW filters are particularly crucial for 5G's higher frequency (above 2 GHz) and mmWave applications due to their superior performance, smaller size, and temperature stability, ensuring clear and reliable signal transmission in complex RF environments.

What is the primary difference between SAW and BAW filters?

The primary difference lies in their operating mechanism and frequency capabilities. SAW filters utilize acoustic waves propagating on the surface of a substrate and are typically used for frequencies up to approximately 2.5 GHz. BAW filters use acoustic waves that propagate through the bulk of the substrate and are generally preferred for higher frequencies (above 2 GHz) due to their better performance at higher frequencies, higher power handling, and smaller form factor, making them ideal for demanding applications like 5G.

Which industries are the primary consumers of SAW and BAW filters?

The primary consumers of SAW and BAW filters are the telecommunications industry, particularly smartphone manufacturers and network infrastructure providers. Other significant industries include automotive electronics (for connected cars and ADAS), the Internet of Things (IoT) across consumer and industrial applications, and to a lesser extent, aerospace and defense, and industrial automation, all requiring reliable wireless communication.

What is the market outlook for SAW and BAW filters over the next decade?

The market outlook for SAW and BAW filters is highly positive, driven by the ongoing global rollout of 5G networks, the continuous proliferation of IoT devices, and the increasing integration of advanced electronics in the automotive sector. The market is projected to experience substantial growth, with a strong CAGR, as demand for high-performance, miniaturized, and efficient RF filters continues to escalate across various burgeoning technological ecosystems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted