Robotic Simulator Market

Robotic Simulator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710402 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

Robotic Simulator Market Size

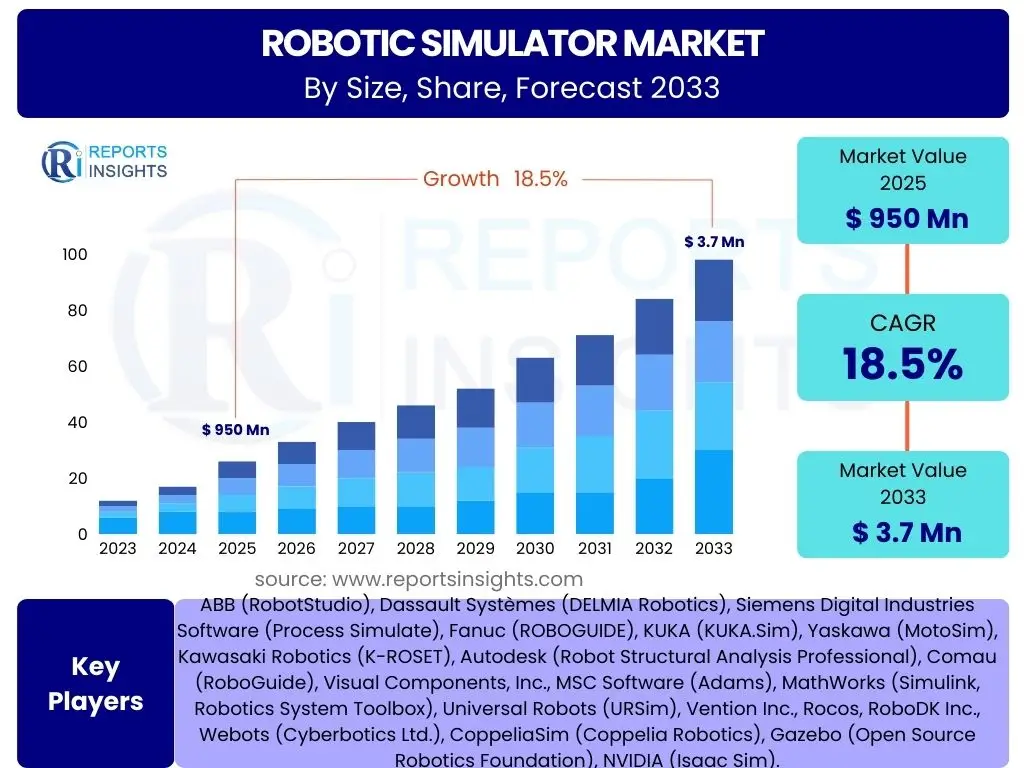

According to Reports Insights Consulting Pvt Ltd, The Robotic Simulator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 950 million in 2025 and is projected to reach USD 3.7 billion by the end of the forecast period in 2033.

Key Robotic Simulator Market Trends & Insights

The robotic simulator market is undergoing significant transformation, driven by advancements in digital twin technology, the increasing adoption of collaborative robots, and the growing complexity of robotic applications across diverse industries. Users frequently inquire about the integration of virtual commissioning, the role of cloud-based simulation platforms, and the demand for more realistic and accurate simulation environments that mirror real-world operational challenges. There is a strong emphasis on reducing development cycles and enhancing the safety and efficiency of robotic systems before physical deployment.

Another prominent trend involves the convergence of simulation with other emerging technologies such as augmented reality (AR) and virtual reality (VR), offering immersive training and design review experiences. The demand for user-friendly interfaces and robust simulation tools capable of handling multi-robot systems and dynamic environments is also a key area of interest. These developments collectively indicate a market moving towards more integrated, intelligent, and accessible simulation solutions.

- Integration of Digital Twin Technology for comprehensive lifecycle management.

- Rising adoption of cloud-based simulation platforms for scalability and accessibility.

- Increased demand for virtual commissioning to accelerate deployment.

- Focus on collaborative robot (cobot) simulation for human-robot interaction safety.

- Growing use of AR/VR for immersive training and design validation.

- Development of advanced physics engines for highly realistic simulations.

- Emphasis on AI-driven simulation for predictive analytics and autonomous system training.

AI Impact Analysis on Robotic Simulator

Artificial intelligence is profoundly reshaping the robotic simulator market, with users keenly interested in how AI enhances simulation capabilities, particularly for complex and autonomous robotic systems. Common inquiries revolve around AI's role in optimizing robot behaviors, enabling predictive maintenance, and facilitating more intelligent decision-making within simulated environments. AI-driven simulation is seen as critical for training machine learning models for robotics, allowing for massive data generation in safe, virtual settings without the need for expensive physical prototypes.

Furthermore, AI is instrumental in accelerating the design and development phases by automating parameter optimization, identifying potential failure points, and suggesting design improvements based on simulated performance data. Concerns often include the computational resources required for AI-enhanced simulations and the need for robust validation methods to ensure simulated AI performance translates effectively to real-world applications. The future trajectory suggests AI will make robotic simulators more adaptive, intelligent, and capable of generating highly realistic and challenging scenarios for advanced robot testing and learning.

- Enables training of AI/ML models for autonomous robots in virtual environments.

- Automates scenario generation and optimization for robust robot testing.

- Facilitates predictive analytics for robot performance and maintenance.

- Enhances realism and complexity of simulated environments through intelligent agents.

- Accelerates robot design and development cycles by optimizing parameters.

- Supports adaptive learning for robots, allowing them to improve behavior over time.

Key Takeaways Robotic Simulator Market Size & Forecast

Analysis of user questions regarding the market size and forecast for robotic simulators reveals a strong interest in understanding the underlying drivers of growth, particularly the role of Industry 4.0 initiatives and the increasing complexity of robotic deployments. Stakeholders are keen to identify the most promising segments and regions for investment, as well as the long-term sustainability of the projected growth rates. There is a clear recognition that the market is expanding rapidly due to the imperative for efficiency, safety, and cost reduction in robotics development.

The projected substantial growth from USD 950 million in 2025 to USD 3.7 billion by 2033, at an 18.5% CAGR, underscores the critical role simulation plays in the modern robotics ecosystem. Key insights indicate that companies are increasingly relying on simulation not just for initial design but for continuous optimization, virtual commissioning, and training throughout the robot's lifecycle. This holistic adoption of simulation tools is a primary factor contributing to the robust market expansion, driven by both technological advancements and practical industrial demands.

- The market exhibits robust growth, driven by rapid advancements in robotics and automation.

- Significant opportunities are emerging from the integration of simulation with AI and digital twin technologies.

- Industrial sectors, particularly manufacturing and logistics, are key adopters of robotic simulation.

- Cloud-based solutions are gaining traction due to their scalability and reduced infrastructure costs.

- Investment in advanced simulation tools is critical for competitive advantage in robotics development.

- The market forecast highlights a strong upward trajectory, signaling sustained demand for innovative simulation solutions.

Robotic Simulator Market Drivers Analysis

The expansion of the robotic simulator market is primarily fueled by the escalating adoption of automation across diverse industries. As industries increasingly integrate robots to enhance productivity, improve precision, and mitigate human error, the necessity for robust simulation tools to design, test, and optimize these systems becomes paramount. This shift towards automation is not limited to traditional manufacturing but extends into logistics, healthcare, and even service sectors, creating a broad demand for sophisticated simulation environments.

Furthermore, the growing complexity of modern robotic systems, which often involve intricate kinematics, multi-robot coordination, and human-robot interaction, necessitates advanced simulation capabilities. Simulators provide a safe, cost-effective, and efficient platform for developers to experiment with complex algorithms, validate safety protocols, and train operational staff without risking damage to expensive hardware or disrupting production schedules. The imperative to reduce time-to-market for new robotic solutions also significantly drives the adoption of simulation, enabling parallel development and early error detection.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Industrial & Service Robots | +3.2% | Global, particularly APAC (China, Japan), North America, Europe | Long-term |

| Demand for Cost-Effective & Risk-Free Robot Development | +2.8% | Global | Mid-term |

| Advancements in AI, Machine Learning, and Digital Twin Technologies | +2.5% | North America, Europe, Asia Pacific | Mid to Long-term |

| Growing Focus on Industry 4.0 & Smart Manufacturing Initiatives | +2.0% | Europe (Germany), APAC (Japan, South Korea), North America | Mid-term |

| Shortening Product Development Cycles & Time-to-Market Pressure | +1.8% | Global | Short to Mid-term |

Robotic Simulator Market Restraints Analysis

Despite the strong growth drivers, the robotic simulator market faces several restraints that could potentially temper its expansion. One significant challenge is the high initial cost associated with acquiring advanced simulation software and the necessary computational infrastructure. Small and medium-sized enterprises (SMEs), in particular, may find these upfront investments prohibitive, limiting their ability to leverage sophisticated simulation tools.

Another major restraint involves the complexity of accurately simulating real-world physics, sensor data, and environmental interactions. Achieving a high degree of fidelity in simulations, especially for highly dynamic and unstructured environments, can be technically challenging and may require specialized expertise. Furthermore, the steep learning curve associated with advanced simulation platforms and the scarcity of skilled personnel capable of operating and interpreting complex simulation results can hinder broader adoption, particularly in regions with nascent robotics ecosystems. The need for continuous updates and maintenance to keep simulation models current with evolving robot hardware and software also adds to the operational burden.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Operational Costs | -1.5% | Emerging Markets, SMEs Globally | Mid-term |

| Complexity in Achieving High Simulation Fidelity | -1.2% | Global | Long-term |

| Lack of Skilled Professionals for Advanced Simulation | -1.0% | Developing Regions | Mid to Long-term |

| Interoperability Challenges with Diverse Robot Platforms | -0.8% | Global | Short to Mid-term |

Robotic Simulator Market Opportunities Analysis

The robotic simulator market is ripe with opportunities, driven by technological advancements and unmet needs across various industries. A significant opportunity lies in the burgeoning field of collaborative robotics (cobots), where simulation is crucial for ensuring safe human-robot interaction and optimizing shared workspaces. The demand for simulating these nuanced interactions, including collision detection, force sensing, and adaptive path planning, presents a substantial growth avenue for specialized simulation solutions.

Another prominent opportunity emerges from the expanding application of robotics in non-traditional sectors such as healthcare (e.g., surgical robots, rehabilitation robots), agriculture (e.g., harvesting robots, autonomous sprayers), and logistics for warehouse automation. Each of these sectors presents unique simulation requirements, fostering innovation in specialized modules and features. Furthermore, the increasing trend towards remote operation and virtual commissioning, especially accelerated by global events, creates a robust demand for highly accurate and reliable cloud-based simulation platforms that can support geographically dispersed teams and enable off-site validation of robotic systems before physical deployment.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Applications (Healthcare, Agriculture, Logistics) | +2.5% | Global | Mid to Long-term |

| Growing Demand for Collaborative Robot (Cobot) Simulation | +2.2% | North America, Europe, Asia Pacific | Short to Mid-term |

| Rise of Cloud-based Simulation & Software-as-a-Service (SaaS) Models | +2.0% | Global | Mid-term |

| Integration with Virtual Reality (VR) & Augmented Reality (AR) for Immersive Experiences | +1.8% | North America, Europe | Long-term |

Robotic Simulator Market Challenges Impact Analysis

The robotic simulator market, while promising, contends with inherent challenges that can impede its full potential. A primary challenge is the continuous struggle to bridge the "reality gap" – the discrepancy between simulated behavior and actual robot performance. This gap arises from limitations in modeling complex physics, sensor noise, unpredictable environmental factors, and the inherent variability of real-world materials and interactions. Overcoming this requires highly sophisticated modeling techniques and extensive validation, which can be resource-intensive.

Another significant hurdle is the lack of standardized interoperability across different robot platforms and simulation software. Companies often utilize a diverse ecosystem of robotic hardware and software, making it challenging to integrate various simulation tools seamlessly. This fragmentation can lead to inefficiencies, increased development costs, and vendor lock-in. Furthermore, ensuring data security and intellectual property protection, particularly in cloud-based simulation environments, remains a critical concern, especially for organizations dealing with proprietary designs and sensitive operational data. Addressing these challenges requires collaborative efforts from industry players, research institutions, and standards bodies to foster a more integrated and secure simulation ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Bridging the "Reality Gap" in Simulation Accuracy | -1.8% | Global | Long-term |

| Lack of Standardization & Interoperability Across Platforms | -1.5% | Global | Mid-term |

| Data Security & Intellectual Property Concerns in Cloud Simulation | -1.3% | North America, Europe | Short to Mid-term |

| High Computational Requirements for Complex Simulations | -1.0% | Global | Mid-term |

Robotic Simulator Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Robotic Simulator Market, covering historical data, current market dynamics, and future projections. It delves into various market segments, regional landscapes, competitive environments, and the impact of emerging technologies like AI and digital twins. The report aims to offer strategic insights for stakeholders to navigate market opportunities and challenges, making informed business decisions based on robust data and expert analysis.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950 million |

| Market Forecast in 2033 | USD 3.7 billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB (RobotStudio), Dassault Systèmes (DELMIA Robotics), Siemens Digital Industries Software (Process Simulate), Fanuc (ROBOGUIDE), KUKA (KUKA.Sim), Yaskawa (MotoSim), Kawasaki Robotics (K-ROSET), Autodesk (Robot Structural Analysis Professional), Comau (RoboGuide), Visual Components, Inc., MSC Software (Adams), MathWorks (Simulink, Robotics System Toolbox), Universal Robots (URSim), Vention Inc., Rocos, RoboDK Inc., Webots (Cyberbotics Ltd.), CoppeliaSim (Coppelia Robotics), Gazebo (Open Source Robotics Foundation), NVIDIA (Isaac Sim). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The robotic simulator market is segmented across various dimensions to provide a granular understanding of its structure and growth dynamics. This comprehensive segmentation helps identify specific areas of demand, technological adoption patterns, and key application niches. Each segment reflects different user needs and operational contexts, from the type of robot being simulated to the industry in which it is deployed, and the specific phase of the robot lifecycle being addressed by simulation.

Understanding these segments is crucial for market players to tailor their offerings and for end-users to identify the most suitable simulation solutions for their unique requirements. The differentiation between software and services components, deployment models (on-premises versus cloud), and the diverse range of robot types and applications underscores the versatility and evolving nature of the robotic simulator market.

- By Component: This segment distinguishes between the core simulation software platforms and the associated services. Software includes the simulation engines, modeling tools, and user interfaces. Services encompass consulting, implementation, integration, training, and ongoing technical support, which are vital for maximizing the value of simulation investments.

- By Deployment: This covers how the simulation software is accessed and managed. On-premises solutions are installed and run on local servers and infrastructure, offering greater control and data security. Cloud-based solutions (SaaS) are hosted by vendors and accessed via the internet, providing scalability, flexibility, and reduced upfront IT costs.

- By Robot Type: Categorizes simulation based on the specific type of robot being modeled. This includes industrial robots (e.g., articulated, SCARA, Cartesian, collaborative robots for manufacturing), mobile robots (e.g., AGVs, AMRs, drones for logistics and inspection), humanoid robots, and specialized service robots. Each type has distinct kinematic, dynamic, and control requirements.

- By Application: Focuses on the primary use cases of robotic simulation. This encompasses design and development (for conceptualization and prototyping), testing and validation (for performance, safety, and reliability), training (for operators and programmers), optimization and control (for process improvement), and digital twin applications (for real-time monitoring and predictive maintenance).

- By Industry Vertical: Examines the adoption of robotic simulators across different industries. Key verticals include manufacturing (automotive, electronics, heavy industry, aerospace & defense), healthcare (surgical assistance, patient care), logistics & warehousing, agriculture, education & research, and energy & utilities. Each sector presents unique challenges and benefits from tailored simulation.

- By End-User: Differentiates between the types of organizations utilizing robotic simulation. Small and Medium-sized Enterprises (SMEs) typically seek more affordable and easier-to-implement solutions, while Large Enterprises often require highly customized, scalable, and integrated simulation platforms for complex operations.

Regional Highlights

The global robotic simulator market exhibits varied growth patterns and adoption rates across different geographical regions, influenced by industrialization levels, technological infrastructure, and investment in automation. Each region presents a unique set of drivers and opportunities, shaping the demand for robotic simulation solutions.

North America is a leading market, characterized by significant investment in advanced manufacturing, robotics research, and a strong presence of key technology developers. The region's emphasis on high-tech industries, coupled with government initiatives supporting automation and AI, drives the demand for sophisticated simulation tools. Europe also represents a mature market, with countries like Germany, France, and the UK at the forefront of Industry 4.0 adoption. The region's focus on precision engineering, robust safety standards, and a skilled workforce contributes to the consistent demand for high-fidelity robotic simulation, particularly in automotive and aerospace sectors. Asia Pacific stands out as the fastest-growing market, primarily fueled by the massive manufacturing base in countries like China, Japan, and South Korea. Rapid industrialization, government support for smart factories, and increasing labor costs are accelerating robot adoption and, consequently, the demand for simulation to optimize these deployments. Latin America and the Middle East and Africa (MEA) are emerging markets, with growing awareness and nascent adoption of robotics in sectors like oil and gas, mining, and basic manufacturing. While these regions currently hold smaller market shares, they are expected to witness significant growth as their industrial bases mature and embrace automation technologies.

- North America: Dominates the market due to high R&D investments, advanced manufacturing, and early adoption of industrial automation and AI in robotics. The US is a major contributor, driven by aerospace, automotive, and logistics sectors.

- Europe: A strong market propelled by Industry 4.0 initiatives, stringent quality standards, and a focus on collaborative robotics. Germany, with its robust manufacturing sector, leads in the region.

- Asia Pacific (APAC): The fastest-growing region, driven by rapid industrialization, large manufacturing bases (China, Japan, South Korea), increasing government support for robotics, and rising labor costs.

- Latin America: An emerging market with increasing adoption of robotics in automotive and mining industries, particularly in countries like Brazil and Mexico, leading to growing demand for simulation.

- Middle East and Africa (MEA): A nascent market with significant potential, especially in the oil and gas, construction, and logistics sectors, as governments invest in diversifying economies and enhancing automation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Robotic Simulator Market.- ABB (RobotStudio)

- Dassault Systèmes (DELMIA Robotics)

- Siemens Digital Industries Software (Process Simulate)

- Fanuc (ROBOGUIDE)

- KUKA (KUKA.Sim)

- Yaskawa (MotoSim)

- Kawasaki Robotics (K-ROSET)

- Autodesk (Robot Structural Analysis Professional)

- Comau (RoboGuide)

- Visual Components, Inc.

- MSC Software (Adams)

- MathWorks (Simulink, Robotics System Toolbox)

- Universal Robots (URSim)

- Vention Inc.

- Rocos

- RoboDK Inc.

- Webots (Cyberbotics Ltd.)

- CoppeliaSim (Coppelia Robotics)

- Gazebo (Open Source Robotics Foundation)

- NVIDIA (Isaac Sim)

Frequently Asked Questions

What is a robotic simulator?

A robotic simulator is a software application designed to create, test, and optimize robot programs and behaviors in a virtual environment. It allows engineers and developers to model robot kinematics, dynamics, sensor inputs, and environmental interactions without needing physical hardware, saving time and resources.

Why is robotic simulation important for robotics development?

Robotic simulation is crucial for reducing development costs, accelerating time-to-market, enhancing safety, and improving the efficiency of robotic systems. It enables risk-free testing of complex algorithms, validation of system performance, and virtual commissioning before physical deployment, minimizing potential errors and downtime.

How does AI impact the future of robotic simulators?

AI significantly enhances robotic simulators by enabling the training of autonomous robot behaviors, automating test scenario generation, and providing predictive analytics for robot performance. It contributes to more realistic and intelligent simulated environments, allowing for the development of highly adaptive and self-learning robotic systems.

What industries are the primary adopters of robotic simulators?

The manufacturing sector, particularly automotive, electronics, and heavy industry, is the largest adopter. Other significant industries include logistics & warehousing, aerospace & defense, healthcare, and education & research, all leveraging simulation for various applications from design to training.

What are the key benefits of using cloud-based robotic simulators?

Cloud-based robotic simulators offer benefits such as enhanced scalability, reduced upfront hardware costs, flexible accessibility from any location, and simplified collaboration among distributed teams. They eliminate the need for significant local computing infrastructure and provide access to powerful processing capabilities on demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted