Robotic Position Sensor Market

Robotic Position Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705724 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Robotic Position Sensor Market Size

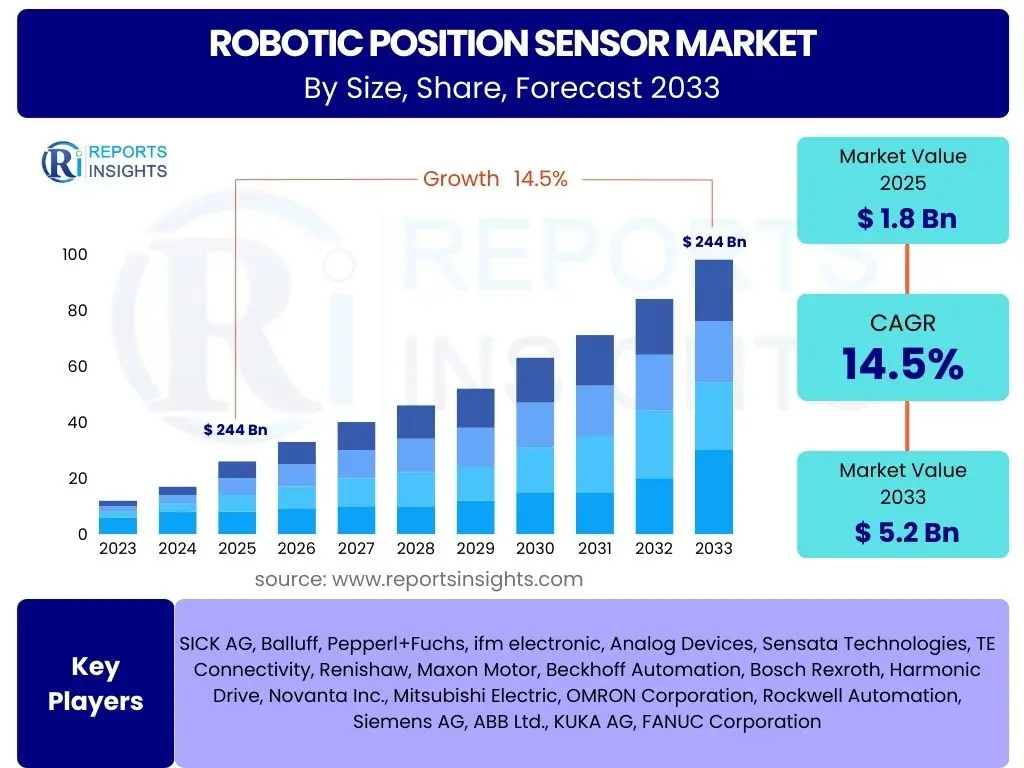

According to Reports Insights Consulting Pvt Ltd, The Robotic Position Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 5.2 Billion by the end of the forecast period in 2033.

Key Robotic Position Sensor Market Trends & Insights

User inquiries into the Robotic Position Sensor market frequently highlight the transformative impact of technological advancements and evolving industrial requirements. There is significant interest in understanding how these sensors are becoming more sophisticated, integrated, and application-specific. Common questions revolve around the adoption of smart sensor technologies, the drive towards miniaturization, and the increasing demand for high-precision, real-time feedback mechanisms in diverse robotic systems.

Furthermore, users seek insights into the market's response to the Industry 4.0 paradigm, particularly concerning enhanced connectivity, data analytics, and the role of sensors in enabling predictive maintenance and autonomous operations. The shift towards collaborative robots (cobots) and autonomous mobile robots (AMRs) also garners considerable attention, with a focus on how position sensors are evolving to meet the stringent safety and performance standards required by these applications. The market is witnessing a continuous push for sensors that can operate reliably in harsh industrial environments while offering improved cost-efficiency and ease of integration, thereby driving innovation in materials, design, and communication protocols.

- Miniaturization and compact design for integration into smaller, more complex robotic systems.

- Enhanced precision, accuracy, and resolution for critical robotic operations.

- Increased integration of sensor fusion technologies for comprehensive environmental understanding.

- Growing adoption of wireless sensor solutions to reduce cabling complexity and improve flexibility.

- Development of robust and durable sensors capable of operating in harsh industrial environments.

- Emphasis on smart sensors with embedded processing capabilities for edge computing and real-time data analysis.

- Transition towards standardized communication protocols for seamless integration within industrial automation ecosystems.

AI Impact Analysis on Robotic Position Sensor

Common user questions regarding AI's impact on robotic position sensors primarily focus on how artificial intelligence capabilities can enhance sensor performance, data interpretation, and overall robotic system autonomy. Users are keen to understand if AI can make sensors more adaptive, improve their accuracy in dynamic environments, and contribute to predictive maintenance strategies by analyzing sensor data. There is also interest in how AI facilitates sensor fusion, allowing data from multiple sensor types to be combined for a more comprehensive and reliable understanding of the robot's position and environment.

The integration of AI algorithms directly influences the demand for more advanced and intelligent position sensors capable of generating richer datasets. AI-driven systems require high-fidelity, real-time positional data to execute complex tasks, navigate autonomously, and interact safely with their surroundings. This creates a synergistic relationship where AI relies on sophisticated position sensing for its effectiveness, and in turn, drives the innovation and development of next-generation sensors with integrated processing and learning capabilities. Users anticipate that AI will not only optimize sensor performance but also enable new functionalities, such as advanced human-robot collaboration and highly adaptive industrial automation processes.

- Enhanced precision and accuracy through AI-driven calibration and error correction algorithms.

- Predictive maintenance capabilities enabled by AI analysis of sensor data patterns, anticipating component failure.

- Improved autonomous navigation and path planning in dynamic environments via AI-powered sensor data fusion.

- Adaptive control systems where AI adjusts robot movements based on real-time positional feedback.

- Facilitation of advanced human-robot collaboration by ensuring precise and safe interaction using AI-interpreted sensor data.

- Optimized resource utilization and energy efficiency in robotic operations through AI-driven sensor management.

Key Takeaways Robotic Position Sensor Market Size & Forecast

User questions about the key takeaways from the Robotic Position Sensor market size and forecast often center on understanding the most significant growth drivers, the dominant regional markets, and the emerging application areas that will shape future demand. There is a strong desire to identify the primary technological advancements propelling market expansion and to assess the impact of evolving industry standards and automation trends on sensor adoption. Users also seek clarity on the long-term investment opportunities and the potential for disruption by novel sensor technologies or manufacturing techniques.

A crucial insight is the sustained robust growth across the forecast period, primarily fueled by the accelerating adoption of industrial automation and collaborative robotics across various sectors. The automotive, electronics, and manufacturing industries remain pivotal, yet significant expansion is observed in healthcare, logistics, and emerging fields such as agriculture robotics. The market's trajectory is also heavily influenced by continuous innovation in sensor precision, miniaturization, and the integration of smart functionalities, which collectively enhance the versatility and performance of robotic systems. This indicates a highly dynamic market driven by both technological push and application-specific demand pull.

- Robust market growth driven by escalating demand for automation and advanced robotics across diverse industries.

- Industrial automation, particularly in automotive and electronics manufacturing, remains a primary growth engine.

- Significant opportunities are emerging in new application areas such as healthcare, logistics, and service robotics.

- Technological advancements in sensor precision, miniaturization, and smart features are critical for market expansion.

- Asia Pacific is projected to be the fastest-growing region, fueled by rapid industrialization and manufacturing expansion.

- Increased focus on collaborative robots (cobots) and autonomous mobile robots (AMRs) is boosting demand for specialized position sensors.

Robotic Position Sensor Market Drivers Analysis

The Robotic Position Sensor market is significantly propelled by the global surge in industrial automation and the widespread adoption of robotics across diverse sectors. Industries are increasingly investing in automation to enhance efficiency, reduce labor costs, and improve manufacturing quality. This trend directly translates into a higher demand for sophisticated position sensors, which are fundamental components for precise robot movement, control, and navigation. The proliferation of Industry 4.0 initiatives, emphasizing smart factories and interconnected systems, further necessitates advanced sensing capabilities to enable real-time data exchange and intelligent decision-making within automated environments.

Beyond traditional industrial applications, the rapid expansion of collaborative robots (cobots) and autonomous mobile robots (AMRs) is creating new avenues for market growth. Cobots, designed to work alongside humans, require highly accurate and reliable position sensors to ensure safety and precise interaction, driving innovation in sensor design. Similarly, AMRs in logistics and warehousing rely heavily on precise positioning for navigation, obstacle avoidance, and task execution. Furthermore, continuous technological advancements in sensor design, including miniaturization, improved accuracy, and enhanced durability, are making these components more versatile and cost-effective, thereby accelerating their integration into a broader range of robotic systems and applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Industrial Automation & Robotics | +4.2% | Global (Asia Pacific, Europe, North America) | 2025-2033 |

| Growth in Collaborative Robots (Cobots) and AMRs | +3.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in Sensor Miniaturization & Precision | +3.0% | Global (Developed Economies) | 2025-2033 |

| Rise of Industry 4.0 & Smart Manufacturing Initiatives | +2.8% | Europe, Asia Pacific, North America | 2025-2033 |

| Growing Demand for Automation in Healthcare & Logistics | +1.0% | North America, Europe, Asia Pacific | 2027-2033 |

Robotic Position Sensor Market Restraints Analysis

Despite the robust growth trajectory, the Robotic Position Sensor market faces certain restraints that could impede its full potential. A primary concern is the relatively high initial cost associated with advanced, high-precision position sensors, especially for specialized applications or smaller enterprises. The investment required for integrating these sophisticated sensors, along with the associated control systems and calibration procedures, can be a significant barrier for some potential adopters, particularly in cost-sensitive industries or developing economies. This cost factor can lead to slower adoption rates or the preference for less advanced, albeit less accurate, alternatives.

Another significant restraint involves the technical complexities related to sensor integration and calibration. Robotic systems often require multiple types of sensors to work in conjunction, necessitating complex integration processes and precise calibration to ensure optimal performance and accuracy. The lack of standardized interfaces or plug-and-play solutions across different manufacturers can further complicate this process, increasing deployment time and requiring specialized expertise. Additionally, the susceptibility of some sensor technologies to harsh environmental conditions such as extreme temperatures, electromagnetic interference, or vibrations can limit their application in certain demanding industrial settings, thereby restraining market expansion in those specific niches.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Sensors | -1.5% | Global (Developing Economies, SMEs) | 2025-2030 |

| Technical Complexities in Integration & Calibration | -1.0% | Global | 2025-2033 |

| Susceptibility to Harsh Environmental Conditions | -0.8% | Specific Industrial Sectors | 2025-2033 |

| Lack of Standardization Across Sensor Technologies | -0.5% | Global | 2025-2028 |

Robotic Position Sensor Market Opportunities Analysis

The Robotic Position Sensor market is poised for significant opportunities driven by the emergence of new robotic applications and the increasing demand for automation in previously untapped sectors. Beyond traditional manufacturing, sectors such as healthcare, agriculture, and construction are increasingly adopting robotics, creating a substantial need for specialized position sensors tailored to unique environmental and operational requirements. In healthcare, for instance, surgical robots and rehabilitation exoskeletons demand ultra-precise and reliable sensors for patient safety and intricate procedures. This diversification of robotic applications opens vast new markets for sensor manufacturers.

Furthermore, the ongoing development of sensor fusion technologies presents a considerable opportunity. By combining data from multiple sensor types—such as position, force, vision, and tactile sensors—robots can gain a more comprehensive and accurate understanding of their environment and interactions. This fusion allows for enhanced performance in complex tasks, improved safety in human-robot collaboration, and more robust navigation in dynamic surroundings. Manufacturers who can develop integrated, multi-modal sensor solutions will gain a competitive edge. Additionally, the continuous push towards smart factories and the Internet of Things (IoT) provides opportunities for sensors with integrated connectivity and edge processing capabilities, enabling real-time data analysis and predictive maintenance within interconnected industrial ecosystems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Robotic Applications (e.g., Healthcare, Agriculture) | +2.0% | Global | 2026-2033 |

| Advancements in Sensor Fusion Technology | +1.8% | Global (Developed Economies) | 2025-2033 |

| Growth of Smart Factory & IoT Ecosystems | +1.5% | Europe, North America, Asia Pacific | 2025-2033 |

| Expansion in Developing Economies and Emerging Markets | +1.0% | Asia Pacific, Latin America, MEA | 2027-2033 |

Robotic Position Sensor Market Challenges Impact Analysis

The Robotic Position Sensor market faces several challenges that require continuous innovation and strategic responses from manufacturers and integrators. One significant challenge is maintaining high accuracy and precision across diverse operating conditions, which can be affected by factors such as temperature fluctuations, electromagnetic interference, and mechanical vibrations. Ensuring sensor reliability and consistency in harsh industrial environments or sensitive medical applications demands robust design and rigorous testing, often increasing manufacturing complexity and cost. Furthermore, the miniaturization trend, while a driver, also presents a challenge in maintaining sensor performance within increasingly compact form factors, as physical constraints can limit the size of sensing elements and signal processing components.

Another critical challenge lies in the calibration and maintenance of position sensors throughout their operational lifespan. Accurate calibration is crucial for ensuring the precision of robotic movements, but this process can be time-consuming and require specialized tools and expertise. Moreover, the long-term drift or degradation of sensor performance necessitates regular maintenance and recalibration, adding to the total cost of ownership for end-users. Addressing these maintenance complexities through self-calibration features or predictive maintenance diagnostics will be vital for broader market acceptance. Additionally, intense competition within the sensor market, coupled with evolving technological standards and the rapid pace of innovation, compels manufacturers to continuously invest in research and development to stay competitive, adding pressure on profit margins.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining High Accuracy in Diverse Operating Conditions | -1.2% | Global | 2025-2033 |

| Complexities of Calibration & Long-term Maintenance | -1.0% | Global | 2025-2033 |

| High Competition & Rapid Technological Obsolescence | -0.7% | Global | 2025-2033 |

| Data Security & Integrity Concerns for Smart Sensors | -0.5% | North America, Europe | 2026-2033 |

Robotic Position Sensor Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Robotic Position Sensor Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers the historical performance from 2019 to 2023, establishes 2024 as the base year, and projects market growth through 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 5.2 Billion |

| Growth Rate | 14.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SICK AG, Balluff, Pepperl+Fuchs, ifm electronic, Analog Devices, Sensata Technologies, TE Connectivity, Renishaw, Maxon Motor, Beckhoff Automation, Bosch Rexroth, Harmonic Drive, Novanta Inc., Mitsubishi Electric, OMRON Corporation, Rockwell Automation, Siemens AG, ABB Ltd., KUKA AG, FANUC Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Robotic Position Sensor market is broadly segmented to provide a granular understanding of its diverse components and application areas. This segmentation helps in identifying specific growth pockets, technological preferences, and industry-specific demands. The primary segmentations include sensor type, underlying technology, specific robotic application, and the end-use industry, each contributing uniquely to the market's overall dynamics and growth trajectory.

Understanding these segments is crucial for stakeholders to tailor their product development, marketing strategies, and investment decisions. For instance, the demand for absolute position sensors might be higher in applications requiring power-off memory, while optical encoders are preferred for high-precision, high-resolution tasks. Similarly, the automotive industry's need for robust and reliable sensors differs significantly from the healthcare sector's requirement for sterile and highly accurate solutions for surgical robots. This multi-dimensional segmentation highlights the intricate nature of the market and the diverse needs it addresses across the global industrial landscape.

- By Type: Absolute Position Sensors, Incremental Position Sensors, Rotary Position Sensors, Linear Position Sensors, Force/Torque Sensors, Proximity Sensors, Vision Sensors, Tactile Sensors, Pressure Sensors, Temperature Sensors, Flow Sensors.

- By Technology: Optical Encoders, Magnetic Encoders, Capacitive Encoders, Inductive Encoders, Resolvers, Potentiometers, Hall Effect Sensors, LVDT (Linear Variable Differential Transformer), Ultrasonic Sensors.

- By Application: Industrial Robots (Articulated Robots, SCARA Robots, Delta Robots, Cartesian Robots), Collaborative Robots (Cobots), Service Robots (Logistics Robots, Medical & Healthcare Robots, Cleaning Robots, Field Robots), Autonomous Mobile Robots (AMRs), Drones, Robotic Surgical Systems, Exoskeletons.

- By End-Use Industry: Automotive & Transportation, Electronics & Semiconductor, Manufacturing & Industrial Automation, Healthcare & Pharmaceuticals, Logistics & Warehousing, Defense & Aerospace, Food & Beverage, Agriculture, Construction.

Regional Highlights

- North America: This region is a significant market for robotic position sensors, driven by strong investments in automation, a robust manufacturing sector, and pioneering advancements in robotics and AI. The presence of key automotive and aerospace industries, coupled with increasing adoption of collaborative robots, fuels demand. Extensive research and development activities also contribute to its leadership in sensor technology innovation.

- Europe: Europe represents a mature but continuously growing market, largely due to its advanced industrial automation infrastructure, particularly in Germany and the Nordic countries. The region's focus on Industry 4.0 initiatives and the widespread use of robots in precision manufacturing, automotive, and logistics sectors contribute substantially to market expansion. Emphasis on workplace safety also drives the demand for high-precision sensors in human-robot collaboration.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily fueled by rapid industrialization, burgeoning manufacturing sectors (especially in China, Japan, South Korea, and India), and increasing government support for automation. The region is a global manufacturing hub, leading to high adoption rates of industrial robots and subsequently, position sensors. Emerging economies within APAC are also witnessing significant investments in robotics for efficiency and productivity gains.

- Latin America: This region is experiencing steady growth in the robotic position sensor market, driven by increasing industrialization and modernization efforts in countries like Brazil and Mexico. The automotive and manufacturing sectors are key contributors, adopting automation to enhance competitiveness. While smaller than other regions, it offers developing opportunities as industries mature and invest in advanced technologies.

- Middle East and Africa (MEA): The MEA market for robotic position sensors is in its nascent stage but shows promising growth, primarily influenced by infrastructure development projects, diversification of economies away from oil, and increasing investments in manufacturing and logistics automation. Countries in the GCC region are leading the adoption of robotics in energy, construction, and healthcare sectors, indicating future potential for sensor demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Robotic Position Sensor Market.- SICK AG

- Balluff

- Pepperl+Fuchs

- ifm electronic

- Analog Devices

- Sensata Technologies

- TE Connectivity

- Renishaw

- Maxon Motor

- Beckhoff Automation

- Bosch Rexroth

- Harmonic Drive

- Novanta Inc.

- Mitsubishi Electric

- OMRON Corporation

- Rockwell Automation

- Siemens AG

- ABB Ltd.

- KUKA AG

- FANUC Corporation

Frequently Asked Questions

What are robotic position sensors?

Robotic position sensors are critical components used in robotic systems to determine the exact location, orientation, and movement of a robot's joints, end-effectors, or the entire robot within its operating environment. They provide precise feedback data essential for accurate control, navigation, and safe operation, enabling robots to perform tasks with high precision and repeatability.

How do robotic position sensors work?

Robotic position sensors typically work by converting a physical position or displacement into an electrical signal. This can be achieved through various technologies such as optical (using light beams), magnetic (detecting magnetic fields), inductive (sensing changes in electromagnetic fields), or capacitive (measuring changes in electrical charge). These signals are then processed by the robot's control system to calculate and adjust its position in real-time.

What are the key applications of robotic position sensors?

Robotic position sensors are vital across numerous applications including industrial automation (e.g., assembly lines, welding, painting in automotive and electronics), collaborative robotics (cobots for human-robot interaction), service robots (e.g., logistics, healthcare, cleaning), autonomous mobile robots (AMRs for navigation), and specialized fields like robotic surgery and exoskeletons, where extreme precision is paramount.

What are the latest trends in robotic position sensor technology?

Current trends in robotic position sensor technology include miniaturization for compact robot designs, enhanced precision and resolution for advanced tasks, integration of AI and machine learning for predictive capabilities and adaptive control, development of robust sensors for harsh environments, and the adoption of wireless communication for increased flexibility and reduced cabling complexity.

What challenges does the robotic position sensor market face?

The market faces challenges such as the high initial cost of advanced sensors, complexities in integration and precise calibration, the need for consistent performance in harsh operating conditions (e.g., extreme temperatures, EMI), and the continuous pressure from rapid technological advancements requiring constant innovation to avoid obsolescence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted