Power Converter and Inverter Market

Power Converter and Inverter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701557 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

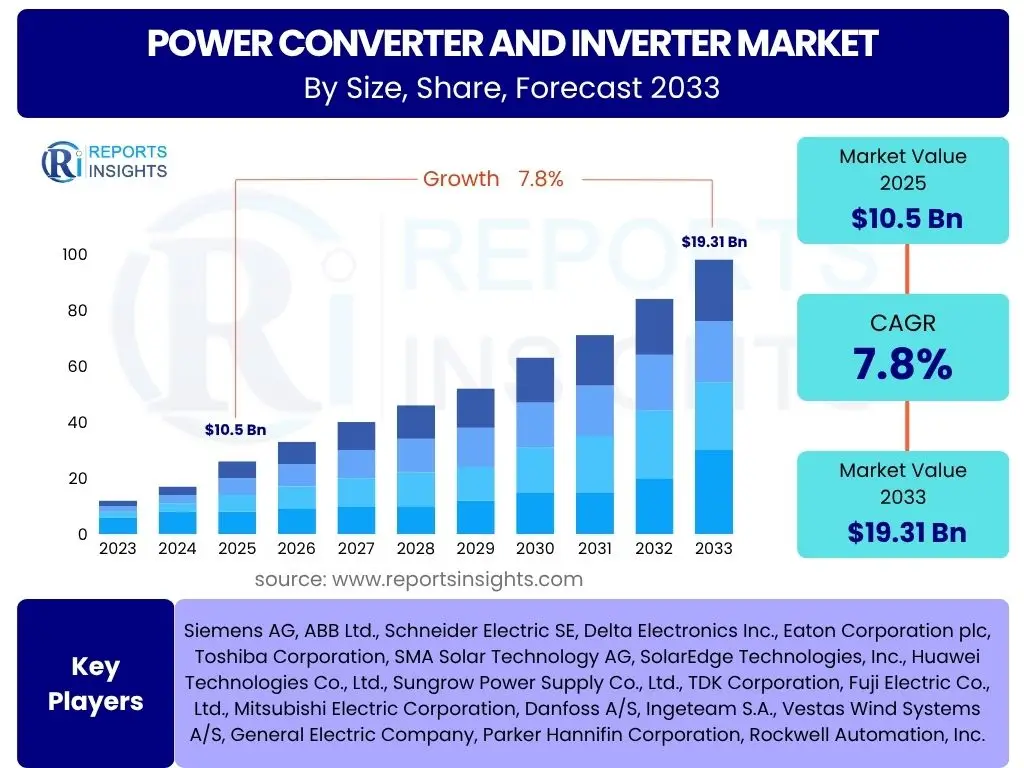

Power Converter and Inverter Market Size

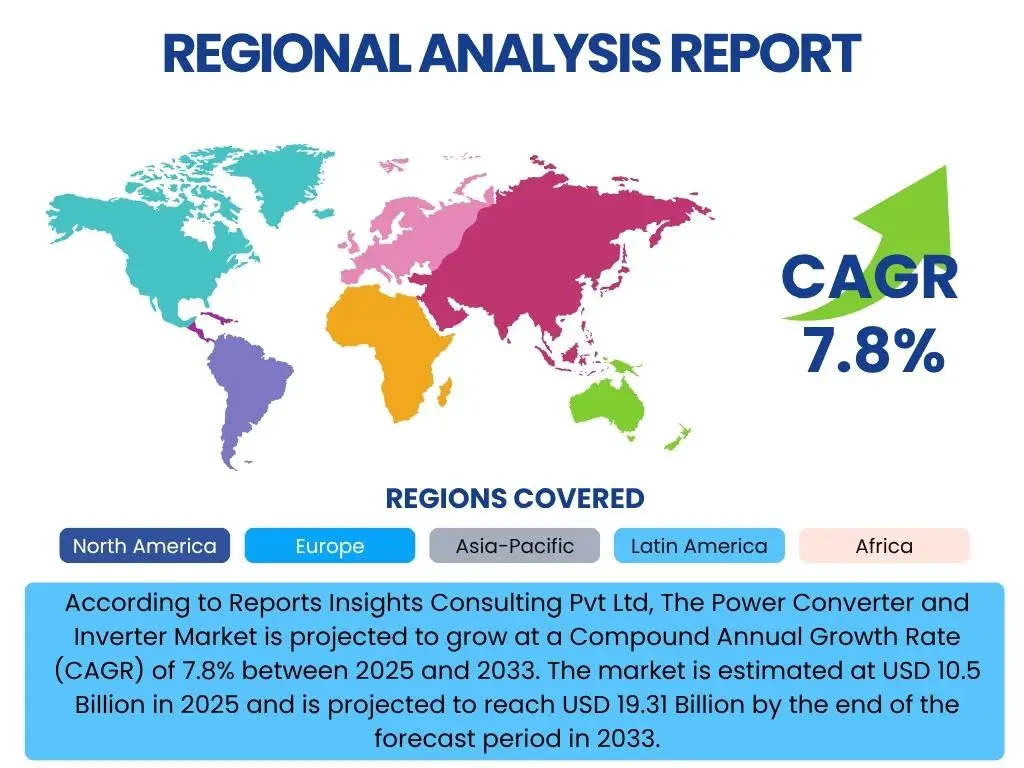

According to Reports Insights Consulting Pvt Ltd, The Power Converter and Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 10.5 Billion in 2025 and is projected to reach USD 19.31 Billion by the end of the forecast period in 2033.

Key Power Converter and Inverter Market Trends & Insights

The power converter and inverter market is undergoing significant transformation, primarily driven by the global energy transition and technological advancements. A key trend involves the increasing demand for high-efficiency and high-power-density solutions, fueled by the widespread adoption of renewable energy sources such as solar and wind power, as well as the rapid expansion of electric vehicle (EV) infrastructure. These systems are becoming more compact, robust, and capable of handling complex power management requirements, shifting away from traditional, bulky designs to more integrated and intelligent modules. The emphasis is on maximizing energy yield and minimizing losses across diverse applications, from large-scale utility grids to residential installations and portable devices.

Another prominent trend is the integration of wide bandgap (WBG) semiconductors, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN), into converter and inverter designs. These materials offer superior performance characteristics compared to traditional silicon, including higher switching frequencies, lower power losses, and improved thermal management. This enables the development of smaller, lighter, and more efficient power electronics. Furthermore, there is a growing focus on smart grid compatibility and digitalization, allowing converters and inverters to communicate seamlessly within energy networks, optimize power flow, and contribute to grid stability and resilience. The convergence of power electronics with advanced control systems and connectivity solutions is shaping the next generation of energy management.

- Increased adoption of renewable energy sources, particularly solar and wind, driving demand for efficient grid-tied and off-grid inverters.

- Rapid growth of electric vehicle (EV) charging infrastructure and on-board chargers necessitating advanced power conversion solutions.

- Transition towards wide bandgap (WBG) semiconductors like SiC and GaN for higher efficiency, power density, and thermal performance.

- Development of smart inverters with enhanced communication capabilities for grid stabilization, demand response, and distributed energy resource management.

- Miniaturization and modularization of power converters and inverters for space-constrained applications and easier scalability.

- Emphasis on energy efficiency and reduction of power losses across industrial, commercial, and residential sectors.

- Integration of artificial intelligence and machine learning for predictive maintenance and optimized energy flow.

AI Impact Analysis on Power Converter and Inverter

Artificial intelligence (AI) is set to significantly revolutionize the power converter and inverter market by enhancing operational efficiency, predictive capabilities, and overall system intelligence. Users are keenly interested in how AI can optimize energy management, reduce downtime through predictive maintenance, and enable more autonomous and adaptive control of power systems. AI algorithms can analyze vast amounts of data from converter and inverter operations, including voltage, current, temperature, and environmental conditions, to identify patterns indicative of potential failures or inefficiencies. This proactive approach minimizes unexpected outages, extends equipment lifespan, and lowers maintenance costs, addressing critical concerns related to reliability and operational expenditure.

Furthermore, AI facilitates intelligent energy management by optimizing power conversion processes in real-time. This involves dynamically adjusting inverter parameters to maximize energy harvest from renewable sources, improve grid integration, and efficiently manage bidirectional power flow for applications like vehicle-to-grid (V2G) systems. AI-driven control systems can predict energy demand and supply fluctuations, enabling converters and inverters to respond optimally, thereby improving grid stability and efficiency. Users anticipate that AI will lead to more resilient, responsive, and self-optimizing power electronics, paving the way for advanced smart grids and more sustainable energy ecosystems, moving beyond traditional rule-based control to adaptive, learning systems.

- Predictive maintenance and fault detection through AI-driven analytics, minimizing downtime and extending equipment lifespan.

- Real-time optimization of power conversion efficiency by dynamically adjusting parameters based on AI analysis of operating conditions.

- Enhanced energy management and grid integration capabilities, enabling smarter load balancing and demand response.

- Autonomous control and adaptive learning for intelligent energy routing and fault recovery in complex power networks.

- Improved design and simulation processes for new converter and inverter architectures through AI-assisted tools.

- Advanced cybersecurity measures for interconnected smart inverters and power systems.

Key Takeaways Power Converter and Inverter Market Size & Forecast

The power converter and inverter market is poised for robust growth, driven primarily by the global transition towards sustainable energy and the burgeoning electric vehicle sector. Stakeholders seeking market insights consistently inquire about the primary growth drivers, the longevity of current demand trends, and the core technological shifts underpinning this expansion. The forecast indicates sustained momentum, with significant investment flowing into renewable energy infrastructure, smart grid development, and advanced charging solutions for EVs. This market trajectory is not merely a short-term trend but a long-term shift towards decentralized and more efficient power management systems, suggesting enduring opportunities for innovation and market expansion.

A crucial takeaway is the increasing importance of efficiency, reliability, and intelligence in power conversion technologies. As energy systems become more complex and interconnected, the demand for converters and inverters capable of seamless integration, bidirectional power flow, and intelligent control will intensify. The adoption of wide bandgap semiconductors, coupled with advancements in AI and IoT, will be pivotal in shaping the next generation of these devices. This signifies that market participants must focus on continuous technological innovation, strategic partnerships, and tailored solutions to meet diverse application requirements across various geographical regions, ensuring competitiveness and fostering sustainable growth in a dynamic energy landscape.

- Significant market growth projected, reaching USD 19.31 Billion by 2033, driven by a strong CAGR of 7.8%.

- The market's expansion is fundamentally linked to the global push for renewable energy adoption and the rapid electrification of transportation.

- Technological advancements, particularly in wide bandgap semiconductors and AI integration, are critical enablers of market growth and innovation.

- Increasing demand for energy-efficient, reliable, and smart power conversion solutions across industrial, commercial, and residential sectors.

- Opportunities for market players lie in developing high-power-density, grid-friendly, and intelligent converter and inverter systems.

Power Converter and Inverter Market Drivers Analysis

The accelerating global transition to renewable energy sources stands as a primary driver for the power converter and inverter market. As countries worldwide commit to reducing carbon emissions and increasing reliance on clean energy, the deployment of solar photovoltaic and wind power installations continues to surge. Power converters and inverters are indispensable components in these systems, converting the variable direct current (DC) output from solar panels or the alternating current (AC) from wind turbines into usable AC power for grids or localized consumption. This fundamental requirement ensures a consistent and growing demand for advanced, efficient, and reliable power conversion technologies capable of integrating seamlessly with diverse grid infrastructures.

Beyond renewable energy, the explosive growth of the electric vehicle (EV) market and its supporting charging infrastructure is another significant impetus. EVs rely heavily on power converters for battery charging (AC-DC and DC-DC) and inverters for converting DC battery power into AC for motor drives. As EV adoption rapidly expands globally, the demand for efficient, high-power, and compact charging solutions, both public and private, directly translates into increased demand for sophisticated power converters and inverters. Furthermore, the ongoing modernization of industrial processes, the expansion of smart grid initiatives, and the increasing global emphasis on energy efficiency across all sectors continue to fuel the need for advanced power electronics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Renewable Energy Adoption | +2.5% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Electric Vehicle (EV) Proliferation & Charging Infrastructure | +2.0% | China, Europe, North America | Medium to Long-term (2025-2033) |

| Increasing Demand for Energy Efficiency | +1.2% | Global | Long-term (2025-2033) |

| Smart Grid Development & Modernization | +1.0% | North America, Europe, Developed Asia Pacific | Medium to Long-term (2025-2033) |

| Industrial Automation & Robotics Growth | +0.8% | Global | Medium-term (2025-2030) |

| Advancements in Battery Energy Storage Systems (BESS) | +0.7% | Global | Long-term (2025-2033) |

Power Converter and Inverter Market Restraints Analysis

Despite robust growth prospects, the power converter and inverter market faces significant restraints, primarily stemming from the high initial capital investment required for advanced systems. Modern, high-efficiency converters and inverters, particularly those utilizing wide bandgap semiconductors or designed for complex grid integration, often come with substantial upfront costs. This can be a deterrent for smaller businesses, residential consumers, or developing regions where budget constraints might favor less advanced, cheaper alternatives. While the long-term operational savings and efficiency gains might offset these costs, the immediate financial outlay can hinder broader adoption, especially in price-sensitive markets.

Another critical restraint is the volatility and potential for disruption within the global supply chain, particularly for crucial electronic components and raw materials. The power electronics industry relies on a complex network of suppliers for semiconductors, passive components, and rare earth elements. Geopolitical tensions, trade disputes, natural disasters, or pandemics can significantly disrupt these supply chains, leading to material shortages, increased component costs, and extended lead times for manufacturing. Such disruptions not only inflate production costs but also delay product delivery, impacting market growth and hampering the ability of manufacturers to meet burgeoning demand, creating uncertainty for both producers and end-users.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.5% | Global, particularly emerging economies | Long-term (2025-2033) |

| Supply Chain Disruptions & Raw Material Price Volatility | -1.0% | Global | Short to Medium-term (2025-2028) |

| Technical Complexities & Integration Challenges | -0.8% | Global | Medium-term (2025-2030) |

| Grid Instability Concerns with Decentralized Generation | -0.5% | Regions with nascent smart grids | Medium-term (2025-2030) |

| Lack of Standardized Regulations Across Regions | -0.4% | Global, especially cross-border projects | Long-term (2025-2033) |

Power Converter and Inverter Market Opportunities Analysis

The power converter and inverter market presents significant opportunities stemming from the vast untapped potential in emerging economies, particularly for renewable energy deployment. Countries in regions like Southeast Asia, Africa, and Latin America are rapidly developing their energy infrastructure and increasingly turning to solar, wind, and hydro power to meet escalating electricity demands. These regions often lack extensive traditional grid infrastructure, making decentralized and off-grid solutions, powered by advanced converters and inverters, highly attractive. As these economies grow, so too will the investment in and adoption of modern power conversion technologies, creating substantial new market segments and avenues for growth for manufacturers and service providers alike.

Further opportunities arise from the continuous evolution of grid modernization initiatives and the expansion of battery energy storage systems (BESS). As grids become smarter and more resilient, there is an increasing need for sophisticated converters that can manage bidirectional power flow, provide grid support services, and seamlessly integrate diverse energy sources and loads. The rapid advancements in battery technology, coupled with the decreasing cost of storage, are driving the proliferation of BESS for grid stability, peak shaving, and renewable energy firming. Converters and inverters are central to BESS operation, presenting a burgeoning market for high-power, intelligent, and efficient conversion solutions. Additionally, niche applications such as vehicle-to-grid (V2G) technology, hydrogen electrolyzers, and advanced industrial power supplies offer specialized growth pathways.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Economies' Renewable Energy Deployment | +1.8% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Growth of Battery Energy Storage Systems (BESS) | +1.5% | Global | Long-term (2025-2033) |

| Advancements in Wide Bandgap Semiconductors (SiC, GaN) | +1.2% | Global | Medium to Long-term (2025-2033) |

| Development of Vehicle-to-Grid (V2G) Technology | +0.9% | North America, Europe, Japan | Medium to Long-term (2027-2033) |

| Demand for Off-Grid and Microgrid Solutions | +0.7% | Remote & Rural Areas (Africa, Asia Pacific) | Long-term (2025-2033) |

| Smart Home Energy Management Systems | +0.6% | Developed Countries | Medium-term (2025-2030) |

Power Converter and Inverter Market Challenges Impact Analysis

The power converter and inverter market faces significant challenges, particularly the rapid pace of technological obsolescence, which demands continuous and substantial investment in research and development. With new semiconductor materials like SiC and GaN constantly evolving, alongside innovations in control algorithms and energy management systems, devices can become outdated relatively quickly. Manufacturers must allocate substantial resources to R&D to remain competitive, pushing the boundaries of efficiency, power density, and intelligence. This constant need for innovation can strain financial resources, especially for smaller companies, and necessitates a proactive approach to product lifecycle management to mitigate the risk of inventory devaluation.

Another pressing challenge is ensuring the reliability and durability of power converters and inverters, especially when deployed in harsh operating environments such as extreme temperatures, high humidity, or remote locations. These conditions can accelerate component degradation, leading to premature failures and reduced system lifespan. Manufacturers must implement rigorous testing protocols, employ robust materials, and design for resilience to meet demanding environmental specifications. Furthermore, the increasing connectivity and intelligence of modern power electronics introduce cybersecurity risks, making them potential targets for malicious attacks that could disrupt energy flow or compromise grid stability. Addressing these vulnerabilities requires ongoing investment in secure hardware and software architectures, adding complexity and cost to product development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & High R&D Costs | -1.3% | Global | Long-term (2025-2033) |

| Ensuring Reliability & Durability in Harsh Environments | -1.0% | Global, particularly industrial/outdoor applications | Long-term (2025-2033) |

| Cybersecurity Threats to Smart Grid Components | -0.8% | Global, particularly developed regions | Medium to Long-term (2025-2033) |

| Shortage of Skilled Workforce for Installation & Maintenance | -0.6% | Global | Long-term (2025-2033) |

| Managing Electromagnetic Interference (EMI) Issues | -0.5% | Global | Medium-term (2025-2030) |

Power Converter and Inverter Market - Updated Report Scope

This report offers an extensive analysis of the global Power Converter and Inverter Market, detailing its size, growth trajectory, and key influencing factors. It provides an in-depth segmentation breakdown, regional insights, competitive landscape analysis, and strategic recommendations for market participants, covering a comprehensive historical period and a forward-looking forecast.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 Billion |

| Market Forecast in 2033 | USD 19.31 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., Schneider Electric SE, Delta Electronics Inc., Eaton Corporation plc, Toshiba Corporation, SMA Solar Technology AG, SolarEdge Technologies, Inc., Huawei Technologies Co., Ltd., Sungrow Power Supply Co., Ltd., TDK Corporation, Fuji Electric Co., Ltd., Mitsubishi Electric Corporation, Danfoss A/S, Ingeteam S.A., Vestas Wind Systems A/S, General Electric Company, Parker Hannifin Corporation, Rockwell Automation, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The power converter and inverter market is comprehensively segmented to provide granular insights into its diverse components and applications. Understanding these segments is crucial for identifying specific growth pockets, tailoring product development strategies, and optimizing market entry approaches. The segmentation by type differentiates between various converter functionalities and inverter architectures, reflecting the distinct technological requirements for different power conversion needs within the electrical ecosystem. This breakdown highlights the dominance and growth trends of specific inverter types, such as micro-inverters for residential solar or central inverters for utility-scale projects, and the diverse applications of power converters in general power management.

Further segmentation by power rating allows for an analysis of demand across low, medium, and high-power applications, which often correspond to different end-use sectors and technological complexities. The application segment provides a detailed view of where power converters and inverters are predominantly utilized, from renewable energy generation and electric vehicles to industrial motor drives and consumer electronics. Lastly, the end-use industry segmentation provides a vertical-specific perspective, illustrating the adoption patterns and unique demands from sectors like automotive, energy & utilities, and manufacturing. This multi-faceted segmentation ensures a thorough understanding of market dynamics and opportunities across the entire value chain.

- By Type:

- Power Converter:

- AC-DC Converters

- DC-DC Converters

- DC-AC Converters

- Inverter:

- String Inverters

- Central Inverters

- Micro Inverters

- Hybrid Inverters

- Power Converter:

- By Power Rating:

- Low Power (Up to 10 kW)

- Medium Power (10 kW - 100 kW)

- High Power (Above 100 kW)

- By Application:

- Renewable Energy:

- Solar Power

- Wind Power

- Hydro Power

- Electric Vehicles:

- EV Charging Stations

- On-board Chargers

- Industrial:

- Motor Drives

- Uninterruptible Power Supplies (UPS)

- Welding Equipment

- Industrial Power Supplies

- Consumer Electronics

- Grid Infrastructure:

- Smart Grids

- Microgrids

- Commercial:

- HVAC Systems

- Lighting

- Data Centers

- Aerospace and Defense

- Renewable Energy:

- By End-Use Industry:

- Automotive

- Energy & Utilities

- Manufacturing

- Commercial & Residential

- Telecommunications

- Healthcare

Regional Highlights

- North America: North America represents a mature yet dynamically growing market for power converters and inverters, driven by significant investments in grid modernization, renewable energy integration, and the expanding electric vehicle sector. The United States and Canada are leading the charge, with substantial solar and wind power installations requiring advanced grid-tied inverters and battery energy storage solutions. Additionally, the rapid deployment of EV charging infrastructure across the region is fueling demand for high-power DC-DC converters and AC-DC rectifiers. Regulatory support for clean energy and smart grid initiatives further propels market growth, emphasizing efficiency and grid stability.

- Europe: Europe is a pioneering region in renewable energy adoption and smart grid technologies, making it a robust market for power converters and inverters. Countries like Germany, the UK, France, and Spain are at the forefront of solar and wind energy expansion, driving demand for advanced inverter technologies that can efficiently integrate distributed energy resources into complex grid networks. The stringent energy efficiency standards and ambitious decarbonization targets across the European Union further stimulate the market for high-performance and intelligent power conversion solutions. Furthermore, the strong emphasis on EV manufacturing and adoption contributes significantly to the regional market for charging infrastructure components.

- Asia Pacific (APAC): The Asia Pacific region is the largest and fastest-growing market for power converters and inverters, primarily due to rapid industrialization, urbanization, and a massive surge in renewable energy installations, particularly in China and India. These countries are investing heavily in large-scale solar farms, wind power projects, and expanding their national grids, necessitating a vast array of power conversion equipment. The burgeoning electric vehicle market in China, Japan, and South Korea also contributes significantly to demand for EV charging components and on-board power electronics. Government initiatives promoting clean energy, coupled with increasing disposable incomes and technological advancements, are key drivers across the diverse economies of APAC.

- Latin America: The Latin American market for power converters and inverters is experiencing steady growth, driven by increasing renewable energy investments, particularly in solar and wind power in countries like Brazil, Mexico, and Chile. These nations are leveraging their abundant natural resources to meet growing electricity demand and diversify their energy mix. While the market is still developing compared to more mature regions, the increasing focus on energy independence and sustainability is creating significant opportunities for power conversion technologies, especially for utility-scale projects and emerging off-grid solutions in remote areas.

- Middle East and Africa (MEA): The MEA region is emerging as a significant market, primarily propelled by large-scale solar power projects and diversification efforts away from fossil fuels, particularly in the Middle East. Countries like Saudi Arabia and UAE are investing heavily in gigawatt-scale solar installations and smart city initiatives, driving demand for high-power utility-scale inverters. In Africa, the focus is on expanding energy access through decentralized renewable energy solutions, including mini-grids and off-grid solar systems, which heavily rely on smaller-scale converters and inverters. Economic development and increasing industrial activity across the region also contribute to the demand for power electronics.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Converter and Inverter Market.- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- Delta Electronics Inc.

- Eaton Corporation plc

- Toshiba Corporation

- SMA Solar Technology AG

- SolarEdge Technologies, Inc.

- Huawei Technologies Co., Ltd.

- Sungrow Power Supply Co., Ltd.

- TDK Corporation

- Fuji Electric Co., Ltd.

- Mitsubishi Electric Corporation

- Danfoss A/S

- Ingeteam S.A.

- Vestas Wind Systems A/S

- General Electric Company

- Parker Hannifin Corporation

- Rockwell Automation, Inc.

Frequently Asked Questions

Analyze common user questions about the Power Converter and Inverter market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Power Converter and Inverter Market?

The Power Converter and Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, driven by increasing demand for renewable energy and electric vehicles.

Which key trends are shaping the Power Converter and Inverter Market?

Key trends include the widespread adoption of wide bandgap semiconductors (SiC and GaN), the integration of AI for predictive maintenance and optimized energy management, and the increasing demand for high-efficiency solutions in renewable energy and EV charging infrastructure.

What are the primary drivers for market growth?

The market is primarily driven by the global push for renewable energy integration (solar and wind), the rapid expansion of the electric vehicle (EV) market and its charging infrastructure, and the growing emphasis on energy efficiency across various industrial and commercial sectors.

How is the market segmented?

The market is segmented by type (Power Converter, Inverter), power rating (low, medium, high), application (renewable energy, EVs, industrial, consumer electronics, grid infrastructure, commercial, aerospace and defense), and end-use industry (automotive, energy & utilities, manufacturing, commercial & residential, telecommunications, healthcare).

Which region is expected to dominate the Power Converter and Inverter Market?

The Asia Pacific (APAC) region is expected to dominate the market due to substantial investments in renewable energy infrastructure, rapid industrialization, and the booming electric vehicle market, particularly in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted