Reverse Osmosi System Market

Reverse Osmosi System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709313 | Last Updated : December 05, 2025 |

Format : ![]()

![]()

![]()

![]()

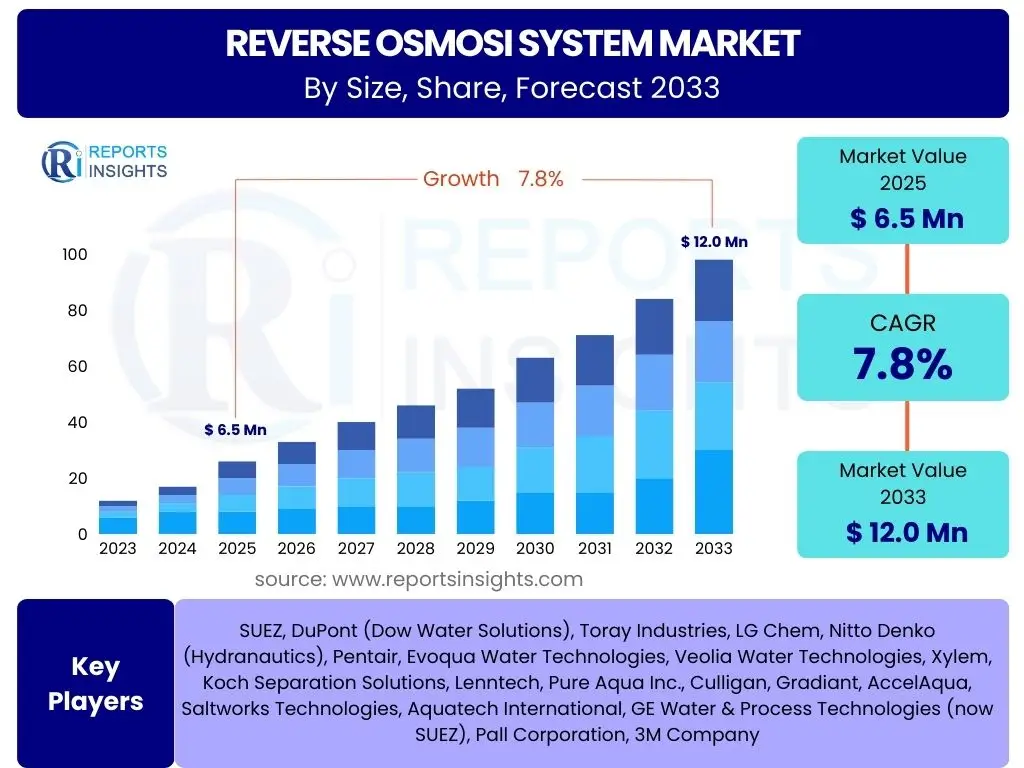

Reverse Osmosi System Market Size

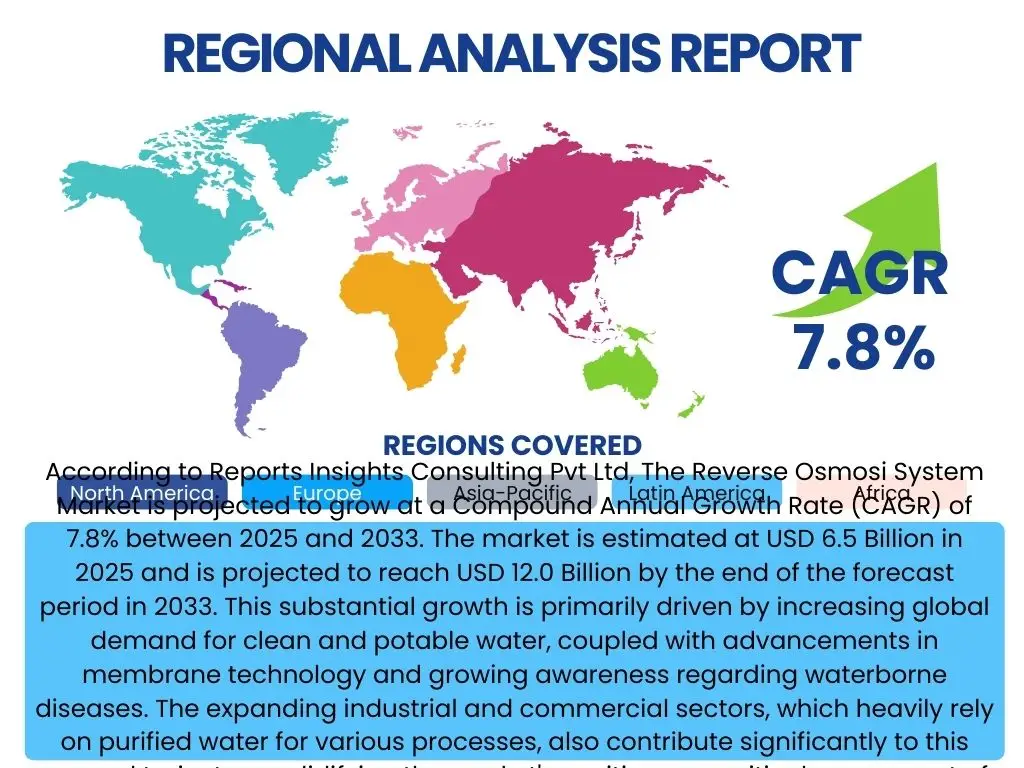

According to Reports Insights Consulting Pvt Ltd, The Reverse Osmosi System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 6.5 Billion in 2025 and is projected to reach USD 12.0 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by increasing global demand for clean and potable water, coupled with advancements in membrane technology and growing awareness regarding waterborne diseases. The expanding industrial and commercial sectors, which heavily rely on purified water for various processes, also contribute significantly to this upward trajectory, solidifying the market's position as a critical component of global water infrastructure.

Key Reverse Osmosi System Market Trends & Insights

User inquiries frequently highlight the evolving landscape of Reverse Osmosis (RO) technology, with a strong focus on sustainability, efficiency, and smart integration. Key themes emerging include the drive for energy-efficient systems, the development of advanced membranes that reduce waste, and the incorporation of digital technologies for enhanced monitoring and control. Consumers and industrial users alike are seeking solutions that not only provide high-quality purified water but also minimize environmental impact and operational costs, leading to innovations across the entire RO system value chain.

- Integration of Smart Monitoring and IoT for real-time performance tracking and predictive maintenance.

- Development of Low-Pressure and Energy-Efficient Membranes to reduce operational costs and carbon footprint.

- Increasing adoption of Point-of-Use (POU) and Point-of-Entry (POE) compact RO systems for residential and small commercial applications.

- Focus on Hybrid Purification Systems combining RO with UV, UF, or activated carbon for comprehensive water treatment.

- Emergence of Circular Economy principles in RO, emphasizing waste reduction, brine recovery, and modular designs.

- Customization and scalability of RO solutions to meet diverse industrial and municipal water treatment demands.

AI Impact Analysis on Reverse Osmosi System

Common questions concerning AI's impact on Reverse Osmosis (RO) systems revolve around its potential to revolutionize operational efficiency, reduce downtime, and enhance water quality. Users are keen to understand how artificial intelligence can optimize complex filtration processes, predict maintenance needs before failures occur, and adapt to varying water conditions in real-time. There is significant interest in AI's role in making RO systems more autonomous, intelligent, and sustainable, particularly in managing energy consumption and minimizing water wastage.

- Predictive maintenance algorithms reduce system downtime by forecasting component failures.

- Real-time optimization of operating parameters, such as pressure and flow rates, for improved energy efficiency.

- Enhanced water quality monitoring and analysis through AI-powered sensors and data analytics.

- Automated fault detection and diagnosis, enabling quicker troubleshooting and reduced manual intervention.

- Adaptive filtration processes that adjust membrane performance based on varying feed water characteristics.

- Improved brine management and recovery strategies through AI-driven process control.

Key Takeaways Reverse Osmosi System Market Size & Forecast

Analysis of user inquiries about the Reverse Osmosis (RO) system market forecast reveals a strong interest in understanding the core drivers behind the projected growth and identifying lucrative investment areas. Users frequently seek clarity on the long-term viability of the market, the influence of technological advancements, and the regional disparities in adoption rates. The overarching takeaway points to a resilient market, propelled by increasing global water scarcity and heightened health consciousness, offering substantial opportunities for innovation and expansion across diverse applications.

- Robust and consistent market growth anticipated over the forecast period, driven by fundamental global needs.

- Technological innovation, particularly in membrane efficiency and system automation, is a critical growth catalyst.

- Significant investment opportunities exist across residential, commercial, industrial, and municipal segments.

- Asia Pacific and North America are expected to remain key growth regions due to rapid industrialization and stringent regulations.

- Sustainability and energy efficiency are becoming paramount, influencing product development and consumer choice.

Reverse Osmosi System Market Drivers Analysis

The global Reverse Osmosis (RO) system market is primarily propelled by several key factors that underscore the critical need for advanced water purification solutions. A fundamental driver is the escalating issue of global water scarcity and the increasing contamination of existing freshwater sources. As populations grow and industrial activities intensify, the demand for potable and process water continues to outstrip supply, making RO systems indispensable for transforming various water sources into usable forms. This environmental imperative, combined with growing public awareness regarding waterborne diseases and the health benefits of purified water, further fuels market expansion.

Beyond the immediate concerns of water availability and safety, regulatory frameworks are playing an increasingly significant role. Governments and international bodies are implementing stricter standards for water quality and wastewater discharge, compelling industries and municipalities to adopt more effective treatment technologies like RO. Furthermore, rapid industrialization, particularly in emerging economies, drives the need for high-purity water for manufacturing processes, ranging from pharmaceuticals and semiconductors to food and beverages, where water quality directly impacts product integrity and operational efficiency. The continuous advancements in membrane technology, leading to more efficient, durable, and cost-effective RO systems, also act as a crucial enabler, making these solutions more accessible and appealing across diverse applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Water Scarcity | +2.1% | Globally, particularly Asia Pacific, MEA | Long-term (2025-2033) |

| Stringent Water Quality Regulations | +1.8% | North America, Europe, China, India | Medium to Long-term (2025-2030) |

| Growing Industrial Demand for High Purity Water | +1.5% | Asia Pacific (China, India), North America | Medium-term (2025-2029) |

| Rising Health Awareness & Waterborne Diseases | +1.2% | Emerging Economies, Latin America | Long-term (2025-2033) |

| Technological Advancements in Membrane Technology | +1.0% | Globally | Short to Medium-term (2025-2028) |

Reverse Osmosi System Market Restraints Analysis

Despite the robust growth trajectory of the Reverse Osmosis (RO) system market, several significant restraints pose challenges to its unbridled expansion. One of the primary concerns is the relatively high initial capital expenditure associated with implementing RO systems, particularly for large-scale industrial and municipal applications. This cost includes not only the RO units themselves but also pre-treatment and post-treatment stages, which are crucial for optimal performance and longevity. For budget-constrained entities or regions with limited financial resources, this upfront investment can be a substantial deterrent, delaying or preventing adoption.

Another considerable restraint is the issue of energy consumption inherent in the RO process. The high pressure required to force water through semi-permeable membranes demands significant energy input, leading to higher operational costs and an increased carbon footprint. While technological advancements are continuously working to reduce energy requirements, this remains a critical factor for industries seeking to minimize their environmental impact and operational expenses. Furthermore, the generation of concentrate or brine, which contains high levels of dissolved solids, presents an environmental challenge. The disposal of this wastewater requires careful management to prevent pollution, adding to operational complexities and costs, especially in regions with strict environmental regulations or limited disposal options. These factors collectively necessitate ongoing innovation to make RO systems more economically viable and environmentally sustainable.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -1.5% | Emerging Economies, SMEs Globally | Long-term (2025-2033) |

| Significant Energy Consumption | -1.2% | Globally, particularly energy-sensitive industries | Medium to Long-term (2025-2033) |

| Brine/Concentrate Disposal Challenges | -1.0% | Coastal Regions, Arid Areas, Europe, North America | Long-term (2025-2033) |

| Membrane Fouling and Scaling Issues | -0.8% | Globally, particularly industries with complex feed water | Continuous |

| Competition from Alternative Purification Methods | -0.5% | Globally | Short-term (2025-2027) |

Reverse Osmosi System Market Opportunities Analysis

The Reverse Osmosis (RO) system market is ripe with numerous opportunities for growth and innovation, driven by evolving global needs and technological advancements. One significant area of opportunity lies in the development and adoption of advanced membrane technologies. Innovations such as forward osmosis, nanofiltration, and hybrid membrane systems offer improved efficiency, reduced energy consumption, and enhanced selectivity for specific contaminants. These advancements can broaden the applicability of RO to more challenging water sources and specialized industrial processes, opening new market segments and increasing the overall appeal of RO solutions.

Furthermore, the expanding focus on wastewater treatment and reuse presents a substantial opportunity. As water resources become scarcer, treating and recycling industrial and municipal wastewater becomes crucial. RO systems are highly effective in tertiary treatment, producing high-quality effluent suitable for various non-potable and even potable applications, thereby creating a circular water economy. The growing demand for point-of-use (POU) and point-of-entry (POE) water purification systems in the residential sector, especially in developing regions and areas with unreliable municipal water supplies, also offers a fertile ground for market expansion. Lastly, strategic partnerships, mergers, and acquisitions can consolidate market positions and enable companies to leverage complementary technologies and expand their geographical reach, capitalizing on the fragmented nature of the water treatment industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Membrane Technology (e.g., FO, NF) | +1.9% | Globally | Medium to Long-term (2026-2033) |

| Increasing Demand for Wastewater Treatment & Reuse | +1.7% | Globally, particularly industrial hubs, arid regions | Long-term (2025-2033) |

| Expansion of Point-of-Use (POU) Systems Market | +1.4% | Emerging Economies, Rural Areas, Households | Short to Medium-term (2025-2029) |

| Integration with Renewable Energy Sources | +1.1% | Remote Areas, Off-grid locations, Sustainability-focused regions | Medium-term (2026-2030) |

| Strategic Partnerships and M&A Activities | +0.9% | Globally | Continuous |

Reverse Osmosi System Market Challenges Impact Analysis

The Reverse Osmosis (RO) system market, while promising, faces several operational and environmental challenges that demand innovative solutions. A significant challenge is the complex pre-treatment requirements for feed water, particularly when dealing with highly contaminated or varying water sources. Inadequate pre-treatment can lead to rapid membrane fouling, scaling, and degradation, which severely reduces system efficiency, increases maintenance costs, and shortens the lifespan of expensive RO membranes. This necessitates sophisticated and often costly pre-filtration stages, adding to the overall system complexity and capital investment, especially for industrial and municipal applications.

Another pressing challenge revolves around the environmental and economic disposal of brine or concentrate, which is a byproduct of the RO process. This highly saline wastewater contains concentrated contaminants and cannot be simply discharged without proper treatment, especially in inland areas or regions with strict environmental regulations. Managing and disposing of this brine responsibly, or even finding methods for its beneficial reuse or zero liquid discharge (ZLD), presents significant technical and financial hurdles. Furthermore, the operational complexity of large-scale RO plants, requiring skilled personnel for monitoring, maintenance, and troubleshooting, can be a challenge in regions with a shortage of specialized expertise. Addressing these challenges through advanced technologies, sustainable practices, and comprehensive training is crucial for the continued growth and acceptance of RO systems globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Pre-treatment Requirements | -1.3% | Globally, particularly industrial applications | Continuous |

| Environmentally Sound Brine Management & Disposal | -1.1% | Inland Areas, Coastal Regions, Europe, North America | Long-term (2025-2033) |

| High Operational and Maintenance Costs | -0.9% | SMEs, Developing Nations | Continuous |

| Membrane Lifespan and Replacement Costs | -0.7% | Globally | Short to Medium-term (2025-2029) |

| Skilled Workforce Requirement for Operation | -0.6% | Developing Nations, Remote Areas | Long-term (2025-2033) |

Reverse Osmosi System Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Reverse Osmosis (RO) System market, providing an in-depth analysis of its current size, historical performance, and future growth projections. The scope encompasses detailed segmentation across various types, applications, and end-use sectors, offering a granular view of market opportunities and challenges. It also identifies key market drivers, restraints, and the potential impact of emerging trends like AI integration and sustainable practices, aiming to equip stakeholders with actionable insights for strategic decision-making and investment planning across different geographical regions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 12.0 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SUEZ, DuPont (Dow Water Solutions), Toray Industries, LG Chem, Nitto Denko (Hydranautics), Pentair, Evoqua Water Technologies, Veolia Water Technologies, Xylem, Koch Separation Solutions, Lenntech, Pure Aqua Inc., Culligan, Gradiant, AccelAqua, Saltworks Technologies, Aquatech International, GE Water & Process Technologies (now SUEZ), Pall Corporation, 3M Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Reverse Osmosis (RO) system market is comprehensively segmented to provide a detailed understanding of its diverse applications and technological nuances. This segmentation allows for a granular analysis of market drivers, opportunities, and challenges across various product types, components, and end-user industries. By breaking down the market into these specific categories, stakeholders can identify niche markets, assess competitive landscapes, and formulate targeted strategies for growth and market penetration, ensuring that solutions are tailored to specific needs and operational requirements.

- By Type:

- Cellulose Acetate Membranes: Traditional and cost-effective for specific applications.

- Thin-Film Composite Membranes: Widely used for high performance and broad applicability.

- Polyamide Membranes: Known for chemical resistance and high salt rejection.

- Others: Emerging and specialized membrane materials.

- By Component:

- RO Membranes: The core filtration element.

- Pre-filters: Sediment Filters, Carbon Filters for initial impurity removal.

- Pumps: High-pressure pumps for osmotic pressure overcoming.

- Storage Tanks: For purified water storage.

- UV Sterilizers: For final disinfection.

- Others: Housings, valves, fittings, pressure gauges, etc.

- By Application:

- Desalination: Converting seawater or brackish water into fresh water.

- Wastewater Treatment: Treating industrial and municipal effluent for reuse or safe discharge.

- Industrial Process Water: Providing high-purity water for manufacturing processes.

- Potable Water Treatment: Ensuring safe drinking water for communities and households.

- By End-Use:

- Residential: Point-of-use and whole-house systems for homes.

- Commercial: Systems for offices, restaurants, hotels, and small businesses.

- Industrial:

- Food & Beverage: For product purity and process water.

- Pharmaceutical: Ultrapure water for drug manufacturing.

- Chemical & Petrochemical: For process water and wastewater treatment.

- Power Generation: Boiler feed water and cooling tower makeup.

- Semiconductor & Electronics: Ultrapure water for chip manufacturing.

- Others: Agriculture, textiles, mining.

- Municipal: Large-scale water treatment plants for public supply.

- By Configuration:

- Wall-Mounted: Space-saving residential and commercial units.

- Under-Sink: Discreet residential filtration.

- Countertop: Portable and easy-to-install units.

- Floor-Standing: Larger commercial and industrial systems.

- Portable: For outdoor use or temporary needs.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to rapid industrialization, burgeoning population, increasing urbanization, and acute water scarcity issues, particularly in countries like China and India, driving demand for both industrial and residential RO systems.

- North America: Characterized by high adoption of advanced RO technologies, stringent environmental regulations, and significant investment in wastewater treatment and reuse, alongside a robust residential market driven by health consciousness.

- Europe: Exhibits steady growth, propelled by strict EU water quality directives, a strong focus on sustainable water management, and the increasing application of RO in industrial processes and desalination projects in southern European countries.

- Middle East and Africa (MEA): A crucial region for desalination due to severe water scarcity, with substantial investments in large-scale RO plants for potable water supply, particularly in Saudi Arabia, UAE, and other Gulf nations.

- Latin America: Expected to show considerable growth, driven by improving economic conditions, increasing access to clean water initiatives, and rising industrial development demanding purified process water across various sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Reverse Osmosi System Market.- SUEZ

- DuPont (Dow Water Solutions)

- Toray Industries

- LG Chem

- Nitto Denko (Hydranautics)

- Pentair

- Evoqua Water Technologies

- Veolia Water Technologies

- Xylem

- Koch Separation Solutions

- Lenntech

- Pure Aqua Inc.

- Culligan

- Gradiant

- AccelAqua

- Saltworks Technologies

- Aquatech International

- Pall Corporation

- 3M Company

Frequently Asked Questions

Analyze common user questions about the Reverse Osmosi System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Reverse Osmosis (RO) system and how does it work?

A Reverse Osmosis system is a water purification technology that uses a semi-permeable membrane to remove ions, unwanted molecules, and larger particles from drinking water. It works by applying pressure to overcome osmotic pressure, forcing water molecules through the membrane while leaving contaminants behind, resulting in highly purified water.

What are the primary benefits of using a Reverse Osmosis system?

The main benefits include highly effective removal of a wide range of contaminants such as dissolved salts, heavy metals, chlorine, fluoride, bacteria, and viruses, leading to safer, better-tasting water. RO systems also improve water clarity and can reduce reliance on bottled water, offering cost savings and environmental advantages.

Are there any drawbacks to Reverse Osmosis water purification?

Potential drawbacks include the generation of concentrate (wastewater), which needs proper disposal, and the removal of beneficial minerals alongside contaminants. Some systems can be slow, and the initial installation cost can be higher than other filtration methods. Energy consumption is also a consideration for larger systems.

How often should RO membranes and filters be replaced?

The replacement frequency depends on water quality and usage. Pre-filters (sediment and carbon) typically require replacement every 6-12 months. The RO membrane, which is the heart of the system, usually lasts 2-5 years under normal conditions, though some high-quality membranes can last longer.

What is the typical cost of installing and maintaining a residential Reverse Osmosis system?

The initial installation cost for a residential RO system can range from USD 200 to USD 1,500, depending on the system's capacity, features, and complexity. Annual maintenance, primarily filter and membrane replacement, typically costs between USD 50 and USD 200, varying with component prices and water quality.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted