Cellulose Fiber Market

Cellulose Fiber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705948 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

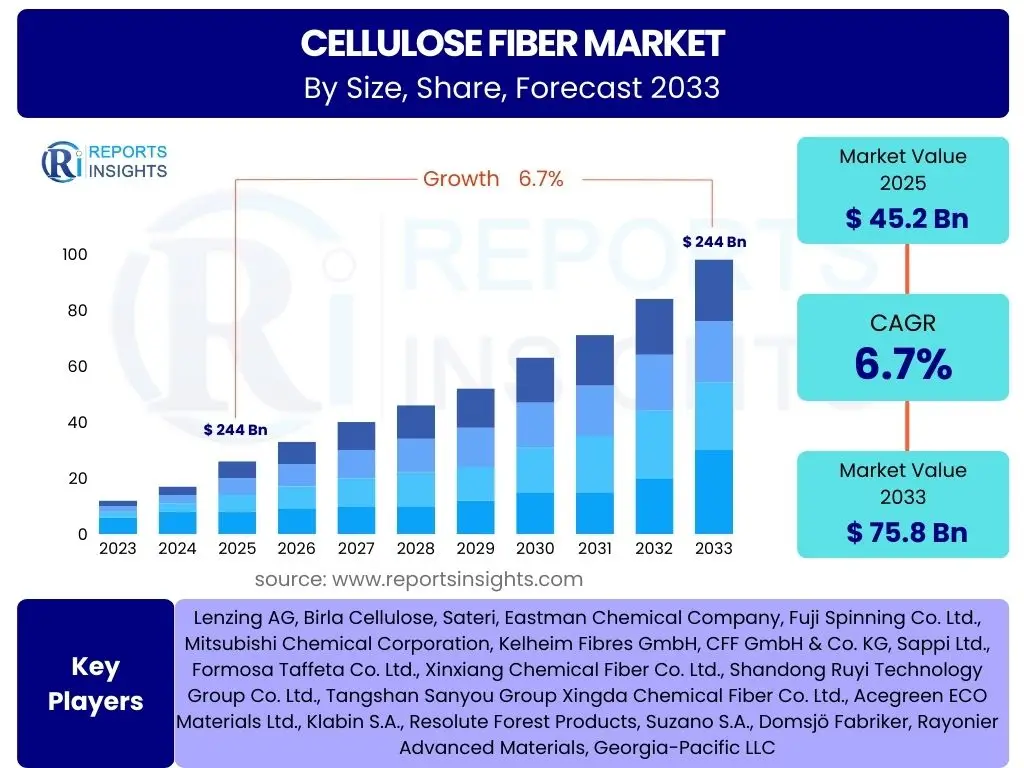

Cellulose Fiber Market Size

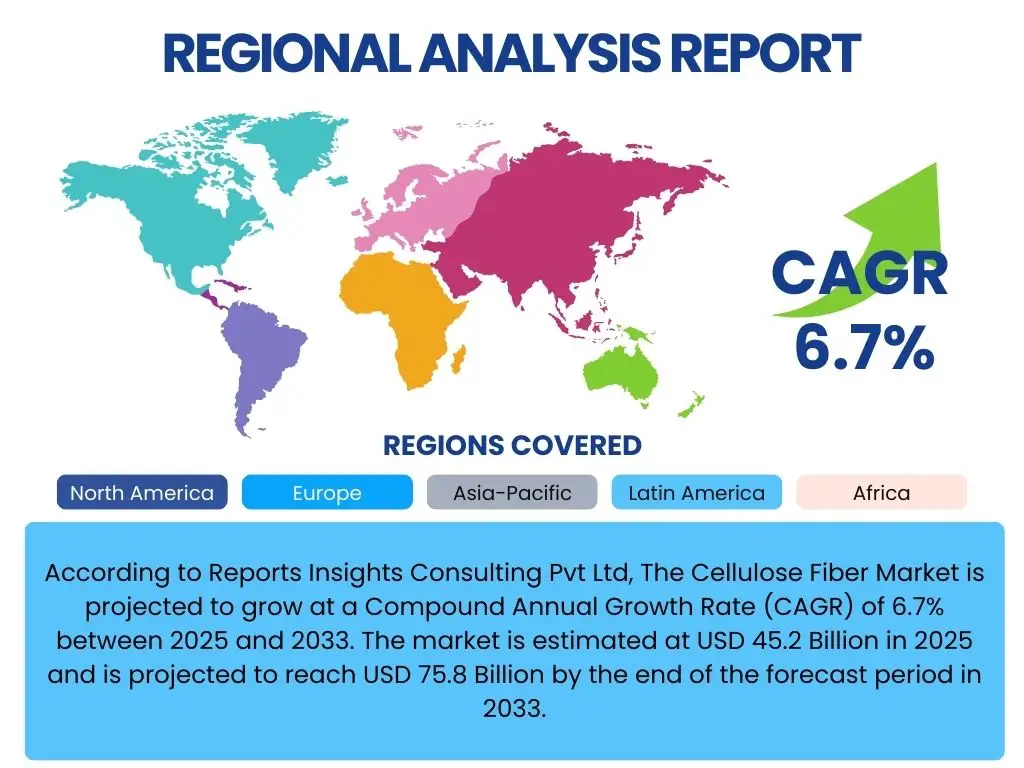

According to Reports Insights Consulting Pvt Ltd, The Cellulose Fiber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 45.2 Billion in 2025 and is projected to reach USD 75.8 Billion by the end of the forecast period in 2033.

Key Cellulose Fiber Market Trends & Insights

The Cellulose Fiber market is significantly influenced by a growing global emphasis on sustainability and circular economy principles. Consumers and industries alike are increasingly seeking eco-friendly alternatives to traditional synthetic materials, driving innovation in cellulose-based products. This shift is particularly evident in the textile and packaging sectors, where the demand for biodegradable and renewable resources is accelerating.

Technological advancements in manufacturing processes, such as closed-loop systems for lyocell production, are enhancing the environmental profile and cost-effectiveness of cellulose fibers. Furthermore, the diversification of applications beyond traditional textiles into areas like composites, filtration, and hygiene products is creating new market avenues. Regulatory support for bio-based materials and increasing investments in sustainable product development are reinforcing these trends, positioning cellulose fibers as a critical component of the future bioeconomy.

- Growing demand for sustainable and biodegradable materials across industries.

- Advancements in production technologies improving efficiency and environmental footprint.

- Expansion of applications beyond textiles into industrial and technical sectors.

- Increasing consumer awareness and preference for eco-friendly products.

- Supportive governmental regulations and initiatives promoting bio-based economies.

AI Impact Analysis on Cellulose Fiber

The integration of Artificial intelligence (AI) is poised to revolutionize various aspects of the Cellulose Fiber market, from raw material sourcing to final product manufacturing and quality control. Users frequently inquire about how AI can optimize complex production processes, which are often resource-intensive and require precise parameter management. AI-driven predictive analytics can forecast demand, optimize supply chains, and reduce waste, leading to significant operational efficiencies and cost reductions.

Moreover, AI can play a crucial role in accelerating research and development for new cellulose fiber variants with enhanced properties. Through machine learning algorithms, researchers can analyze vast datasets to identify optimal chemical compositions, processing conditions, and material structures, thereby shortening development cycles for novel applications. AI's capacity for real-time monitoring and anomaly detection will also improve product consistency and quality assurance, addressing concerns about scalability and performance variability in advanced cellulose materials.

- Optimization of production processes for increased efficiency and reduced waste.

- Enhanced quality control and consistency through real-time monitoring and predictive analytics.

- Accelerated research and development of novel cellulose fiber types and applications.

- Improved supply chain management and demand forecasting for raw materials and finished products.

Key Takeaways Cellulose Fiber Market Size & Forecast

The Cellulose Fiber market is on a robust growth trajectory, primarily fueled by the global imperative for sustainable materials. The significant projected increase in market size from USD 45.2 Billion in 2025 to USD 75.8 Billion by 2033 underscores a profound shift in industrial priorities towards eco-friendly and renewable resources. This growth is not merely incremental but reflective of a fundamental change in consumer preferences and regulatory landscapes, which are increasingly favoring biodegradable and circular economy solutions.

A key insight is the diversified application potential of cellulose fibers, extending beyond their traditional stronghold in textiles to encompass innovative uses in non-wovens, composites, and specialized industrial products. This versatility, coupled with ongoing advancements in production technologies like lyocell and modal, ensures a strong competitive edge against synthetic alternatives. The market's resilience and expansion are intrinsically linked to its ability to offer high-performance, environmentally responsible materials that meet evolving industry demands and contribute to a more sustainable future.

- Significant market expansion driven by global sustainability trends.

- Diversification of applications beyond traditional textile uses.

- Strong competitive position against synthetic fibers due to environmental benefits.

- Positive long-term outlook supported by technological innovation and regulatory support.

Cellulose Fiber Market Drivers Analysis

The Cellulose Fiber market is propelled by a convergence of factors that emphasize environmental responsibility and material innovation. A primary driver is the escalating global demand for sustainable products, driven by heightened consumer awareness and corporate commitments to eco-friendly practices. This demand particularly impacts industries seeking alternatives to fossil-fuel-derived materials, pushing cellulose fibers to the forefront due to their natural origin, biodegradability, and renewable nature. Furthermore, stringent environmental regulations and government initiatives aimed at reducing plastic waste and promoting bio-based economies are creating a favorable policy environment, incentivizing the adoption and development of cellulose fiber technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Sustainable Products | +1.8% | Global, particularly Europe & North America | Long-term |

| Growing Textile Industry Adoption of Eco-fibers | +1.5% | Asia Pacific, Europe | Mid-to-long term |

| Rising Environmental Regulations and Awareness | +1.2% | Global, especially Europe | Long-term |

| Technological Advancements in Production Processes | +0.9% | Global | Mid-term |

| Expansion into New Application Areas (e.g., Composites, Non-wovens) | +0.8% | North America, Europe, Asia Pacific | Mid-to-long term |

Cellulose Fiber Market Restraints Analysis

Despite significant growth drivers, the Cellulose Fiber market faces several restraints that could impede its expansion. One key challenge is the relatively higher production cost of certain advanced cellulose fibers, such as lyocell, compared to conventional synthetic fibers or even some natural fibers like cotton. This cost disparity can limit adoption, particularly in price-sensitive markets. Additionally, the reliance on specific wood pulp or agricultural waste as raw materials introduces concerns about sustainable sourcing, deforestation, or competition with food crops, requiring careful management to ensure a truly eco-friendly supply chain. Market penetration can also be hindered by the lack of widespread consumer awareness or education regarding the benefits and distinctions of various cellulose fiber types, leading to slower adoption rates in certain end-use segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs Compared to Synthetics | -0.8% | Global | Mid-term |

| Raw Material Sourcing and Price Volatility | -0.6% | Global | Short-to-mid term |

| Competition from Established Synthetic Fibers | -0.5% | Asia Pacific, Emerging Markets | Long-term |

| Complex Manufacturing Processes Requiring High Investment | -0.4% | Global | Long-term |

Cellulose Fiber Market Opportunities Analysis

The Cellulose Fiber market presents numerous opportunities for growth, driven by innovation and evolving market needs. A significant opportunity lies in the development of novel applications for nanocellulose and microfibrillated cellulose, which offer superior strength, lightweight properties, and biodegradability for advanced materials in sectors like electronics, biomedical, and automotive. Furthermore, the increasing focus on circular economy models is creating demand for recycled cellulose fibers and processes that utilize textile waste, presenting a substantial opportunity for sustainable product innovation and resource efficiency. Untapped potential also exists in emerging economies where industrialization and consumer disposable income are rising, leading to increased demand for both textiles and non-woven products, offering new markets for cellulose fiber manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Nanocellulose and Microfibrillated Cellulose | +1.3% | North America, Europe, Asia Pacific | Long-term |

| Expansion into Circular Economy Models and Recycling | +1.0% | Europe, North America | Mid-to-long term |

| Growth in Emerging Economies for Textiles and Non-wovens | +0.9% | Asia Pacific, Latin America, MEA | Mid-to-long term |

| Innovation in Blended Fabrics and Performance Materials | +0.7% | Global | Mid-term |

| Partnerships for Sustainable Sourcing and Production | +0.6% | Global | Short-to-mid term |

Cellulose Fiber Market Challenges Impact Analysis

The Cellulose Fiber market is confronted by several challenges that demand strategic responses from industry players. One significant challenge pertains to the scalability of new, more sustainable production technologies, such as those for lyocell and modal fibers. While these methods offer environmental benefits, scaling them up to meet burgeoning global demand efficiently and cost-effectively remains an engineering and financial hurdle. Additionally, ensuring a consistently sustainable and ethically sourced supply of raw materials, particularly wood pulp, without contributing to deforestation or biodiversity loss, poses an ongoing challenge for the industry. Moreover, market fragmentation and the need for standardized quality metrics across diverse applications can hinder broader adoption and consumer trust, requiring collaborative efforts for industry-wide harmonization.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability of Advanced Production Technologies | -0.7% | Global | Mid-to-long term |

| Ensuring Sustainable and Ethical Raw Material Sourcing | -0.5% | Global, especially regions with forests | Long-term |

| Managing Production Waste and Effluents | -0.4% | Global | Mid-term |

| Competition from Cost-Effective Synthetic Alternatives | -0.3% | Asia Pacific, Emerging Markets | Long-term |

Cellulose Fiber Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Cellulose Fiber market, covering its historical performance, current dynamics, and future growth projections. It meticulously examines market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages extensive data analysis and expert insights to offer strategic intelligence for stakeholders, enabling informed decision-making in a rapidly evolving global market. Special emphasis is placed on the impact of technological advancements and the escalating demand for sustainable materials shaping the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.2 Billion |

| Market Forecast in 2033 | USD 75.8 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lenzing AG, Birla Cellulose, Sateri, Eastman Chemical Company, Fuji Spinning Co. Ltd., Mitsubishi Chemical Corporation, Kelheim Fibres GmbH, CFF GmbH & Co. KG, Sappi Ltd., Formosa Taffeta Co. Ltd., Xinxiang Chemical Fiber Co. Ltd., Shandong Ruyi Technology Group Co. Ltd., Tangshan Sanyou Group Xingda Chemical Fiber Co. Ltd., Acegreen ECO Materials Ltd., Klabin S.A., Resolute Forest Products, Suzano S.A., Domsjö Fabriker, Rayonier Advanced Materials, Georgia-Pacific LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cellulose Fiber market is extensively segmented by various characteristics, reflecting the diverse nature of its products and applications. This segmentation allows for a granular understanding of market dynamics within specific categories, providing insights into growth drivers and demand patterns. The primary segmentation includes analysis by type of fiber, encompassing both regenerated and acetate fibers, each with unique properties and manufacturing processes. Further segmentation by application highlights the broad utility of these fibers across various industries, from textiles to advanced industrial uses. Finally, an end-use industry analysis provides a holistic view of the market's penetration into major sectors like apparel, medical, and automotive, revealing key consumption patterns and future growth areas.

- By Type:

- Viscose

- Lyocell

- Modal

- Cupro

- Acetate

- Cellulose Esters

- Others (e.g., Regenerated Cellulose, Microfibrillated Cellulose)

- By Application:

- Textiles

- Apparel

- Home Furnishings

- Non-wovens

- Hygiene Products (diapers, feminine care)

- Medical Textiles (bandages, surgical drapes)

- Wipes (personal care, industrial)

- Industrial

- Composites (automotive, construction)

- Filtration

- Automotive (interiors, structural components)

- Packaging

- Others (e.g., Electronics, Food additives)

- Textiles

- By End-Use Industry:

- Apparel

- Home Textiles (bedding, towels, upholstery)

- Medical & Healthcare

- Building & Construction

- Automotive

- Filtration

- Packaging

- Personal Care

- Others (e.g., Sportswear, Agriculture)

Regional Highlights

The Cellulose Fiber market demonstrates distinct regional dynamics influenced by varying levels of industrial development, regulatory frameworks, and consumer preferences. Asia Pacific (APAC) stands as the largest and fastest-growing market, driven by its extensive textile and apparel manufacturing base, coupled with increasing awareness and demand for sustainable materials from a burgeoning middle class. Countries like China, India, and Southeast Asian nations are significant producers and consumers, benefiting from robust economic growth and supportive government initiatives for green manufacturing.

Europe represents a mature yet highly innovative market, characterized by stringent environmental regulations and a strong emphasis on circular economy principles. The region is a hub for research and development in advanced cellulose fibers, particularly lyocell and modal, and boasts high consumer demand for eco-friendly fashion and home textiles. Countries such as Germany, Austria, and Sweden lead in sustainable production practices and technological advancements, often setting global benchmarks for the industry.

North America is also a prominent market, marked by increasing consumer demand for sustainable products and the adoption of bio-based materials in diverse applications, including non-wovens and industrial composites. The region benefits from significant investments in research and innovation aimed at developing next-generation cellulose fibers and exploring new end-use possibilities. Latin America, the Middle East, and Africa (MEA) are emerging markets, showing gradual but steady growth, primarily driven by expanding textile industries and increasing awareness of sustainability, albeit with challenges related to infrastructure and technological adoption compared to more developed regions.

- Asia Pacific (APAC): Dominates the market due to large-scale textile production, rising disposable incomes, and increasing environmental awareness in countries like China, India, and Bangladesh.

- Europe: A leader in sustainable innovation and consumption, driven by strong regulatory support for bio-based materials and high consumer demand for eco-friendly products, with Germany, Austria, and Sweden at the forefront.

- North America: Exhibits steady growth fueled by a growing preference for sustainable alternatives in apparel, non-wovens, and industrial sectors, alongside significant R&D investments.

- Latin America: Emerging market with growing textile industries and increasing interest in sustainable practices, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Gradually expanding market, primarily influenced by textile manufacturing growth and a nascent but rising demand for sustainable products.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cellulose Fiber Market.- Lenzing AG

- Birla Cellulose

- Sateri

- Eastman Chemical Company

- Fuji Spinning Co. Ltd.

- Mitsubishi Chemical Corporation

- Kelheim Fibres GmbH

- CFF GmbH & Co. KG

- Sappi Ltd.

- Formosa Taffeta Co. Ltd.

- Xinxiang Chemical Fiber Co. Ltd.

- Shandong Ruyi Technology Group Co. Ltd.

- Tangshan Sanyou Group Xingda Chemical Fiber Co. Ltd.

- Acegreen ECO Materials Ltd.

- Klabin S.A.

- Resolute Forest Products

- Suzano S.A.

- Domsjö Fabriker

- Rayonier Advanced Materials

- Georgia-Pacific LLC

Frequently Asked Questions

What are the primary applications of cellulose fibers?

Cellulose fibers are primarily used in textiles for apparel and home furnishings, non-wovens for hygiene products and medical textiles, and industrial applications such as composites, filtration, and automotive components due to their versatile properties.

Why are cellulose fibers considered sustainable?

Cellulose fibers are considered sustainable because they are derived from renewable natural resources like wood pulp, are biodegradable, and can be produced using environmentally friendly closed-loop processes that minimize chemical waste and water consumption.

How do cellulose fibers compare to synthetic fibers?

Cellulose fibers offer natural breathability, absorbency, and biodegradability, distinguishing them from synthetic fibers (e.g., polyester, nylon) which are petroleum-based, non-biodegradable, and often contribute to microplastic pollution. While synthetics may offer superior durability for specific uses, cellulose fibers excel in comfort and environmental footprint.

What is the market outlook for cellulose fibers?

The market outlook for cellulose fibers is highly positive, projected to grow significantly due to increasing global demand for sustainable materials, stringent environmental regulations, technological advancements in production, and diversification into new high-value applications.

What are the main types of regenerated cellulose fibers?

The main types of regenerated cellulose fibers include Viscose (Rayon), Lyocell (e.g., Tencel), and Modal. Each type offers distinct properties and is produced using different manufacturing processes, with Lyocell being particularly noted for its environmentally responsible production method.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted