Refractory Ceramic Fiber Market

Refractory Ceramic Fiber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704017 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

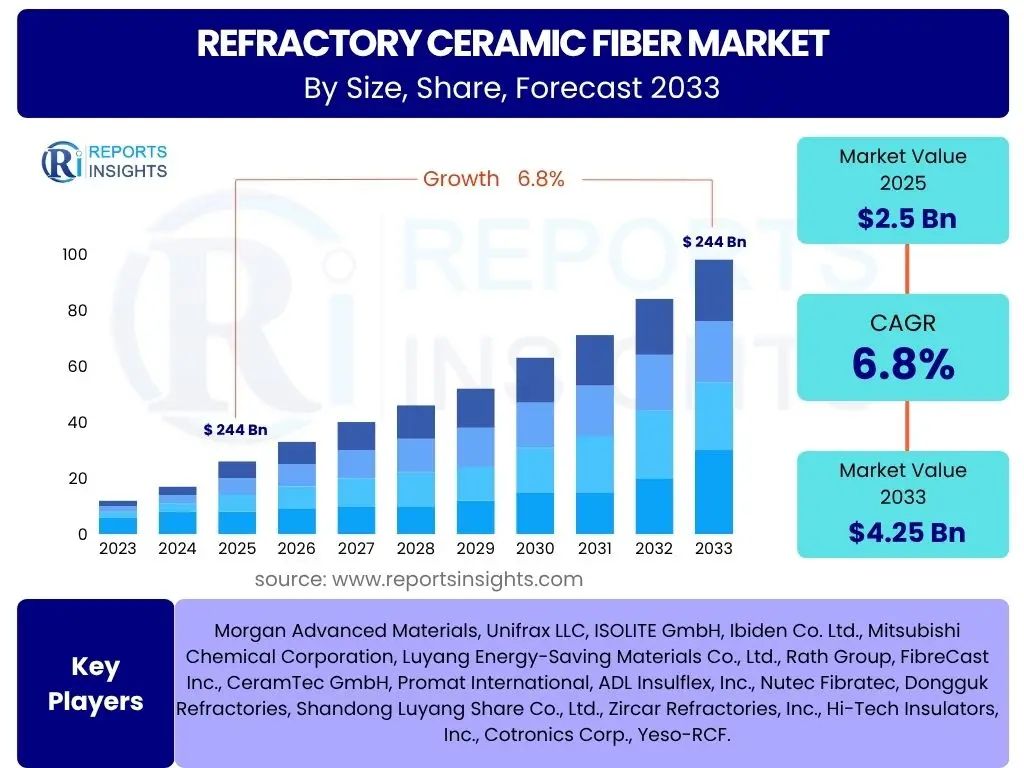

Refractory Ceramic Fiber Market Size

According to Reports Insights Consulting Pvt Ltd, The Refractory Ceramic Fiber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.25 Billion by the end of the forecast period in 2033.

Key Refractory Ceramic Fiber Market Trends & Insights

The Refractory Ceramic Fiber (RCF) market is currently experiencing significant shifts driven by evolving industrial demands, increasing environmental consciousness, and continuous technological advancements. Users frequently inquire about the latest innovations and the market's trajectory towards more sustainable solutions. The primary trends indicate a move towards enhanced performance characteristics, greater energy efficiency in industrial applications, and the development of bio-soluble alternatives to address health and safety concerns associated with traditional RCFs.

Furthermore, the growth of high-temperature industrial processes across various sectors, including steel, ceramics, glass, and petrochemicals, is a strong underlying current boosting RCF demand. There is a notable emphasis on extending the lifespan of refractory linings and reducing overall energy consumption in industrial furnaces and kilns. This focus is leading to demand for RCF products that offer superior insulation properties and durability, supporting cost-efficiency and operational improvements for end-users. The market is also observing regional shifts in manufacturing capabilities and consumption patterns, with Asia Pacific maintaining its dominance due to rapid industrialization.

- Increasing demand for energy-efficient insulation solutions in high-temperature industrial applications.

- Growing adoption of bio-soluble and low bio-persistent (LBP) RCF alternatives due to stringent environmental and health regulations.

- Technological advancements in RCF manufacturing processes leading to improved product performance and reduced costs.

- Expansion of end-use industries such as iron and steel, ceramics, glass, and petrochemicals, particularly in emerging economies.

- Focus on lightweighting and thermal management in the automotive and aerospace sectors.

AI Impact Analysis on Refractory Ceramic Fiber

User inquiries concerning Artificial Intelligence (AI) in the Refractory Ceramic Fiber (RCF) sector often revolve around its potential to revolutionize manufacturing processes, enhance product quality, and optimize material development. There is a general expectation that AI can bring unprecedented levels of precision and efficiency to a traditionally materials-intensive industry. Specifically, users are keen to understand how AI can assist in predictive analytics for equipment maintenance, real-time quality control during production, and the accelerated discovery of novel RCF formulations with improved properties.

The deployment of AI and machine learning algorithms is anticipated to significantly influence various stages of the RCF lifecycle, from raw material selection and processing to final product application and performance monitoring. By analyzing vast datasets related to material composition, processing parameters, and operational conditions, AI can identify optimal manufacturing pathways, predict material degradation, and customize RCF solutions for specific industrial requirements. This integration promises not only enhanced operational efficiency and cost reduction but also a faster pace of innovation in developing next-generation refractory materials.

- Optimization of RCF manufacturing processes through predictive analytics and machine learning for improved yield and reduced waste.

- Enhanced quality control and defect detection in RCF products using AI-powered vision systems and data analysis.

- Accelerated research and development of new RCF formulations and materials with desired thermal and mechanical properties.

- Predictive maintenance for industrial furnaces and kilns utilizing RCF linings, extending equipment lifespan and reducing downtime.

- Supply chain optimization and demand forecasting for RCF raw materials and finished products, leading to better inventory management.

Key Takeaways Refractory Ceramic Fiber Market Size & Forecast

Analysis of common user questions regarding the Refractory Ceramic Fiber (RCF) market size and forecast reveals a strong interest in understanding the underlying growth drivers, the resilience of the market against potential restraints, and the overall trajectory of demand over the coming decade. Users often seek clarity on which sectors are propelling growth and how sustainability efforts might impact future market dynamics. The insights suggest a market poised for steady expansion, underpinned by essential industrial applications and a growing emphasis on energy efficiency.

The primary takeaway is that the RCF market's robust growth is intrinsically linked to the continuous operation and expansion of high-temperature industries worldwide. While traditional applications remain foundational, increasing regulatory pressure for reduced environmental impact and improved worker safety is fostering innovation in bio-soluble RCFs, presenting both opportunities and challenges. The forecast indicates that despite potential headwinds from material alternatives or production costs, the indispensable role of RCF in thermal insulation and high-temperature resistance will ensure sustained demand, with significant regional contributions from industrializing economies.

- The RCF market is set for consistent growth, driven by indispensable applications in high-temperature industrial processes.

- Innovation in bio-soluble RCFs is a crucial factor for future growth, addressing environmental and health concerns.

- Asia Pacific is expected to remain the dominant region due to ongoing industrial development and infrastructure projects.

- Energy efficiency mandates across industries are boosting demand for high-performance RCF insulation solutions.

- Strategic partnerships and mergers are shaping the competitive landscape, aiming for expanded product portfolios and market reach.

Refractory Ceramic Fiber Market Drivers Analysis

The Refractory Ceramic Fiber (RCF) market is propelled by several key drivers stemming from the intrinsic needs of various industrial sectors. A predominant factor is the continuous global demand for energy efficiency in high-temperature processes across manufacturing, power generation, and petrochemical industries. RCF's superior insulation properties directly contribute to energy savings by reducing heat loss, making it a preferred material for furnace and kiln linings, which aligns with corporate sustainability goals and cost-reduction strategies.

Furthermore, the expansion of core industrial sectors, particularly in emerging economies, significantly boosts the consumption of RCF. Industries such as iron and steel, glass, and ceramics require high-performance refractory materials for their demanding operational environments. The increasing production capacities and the establishment of new industrial facilities globally translate into a sustained demand for RCF, as it provides durable and effective thermal management solutions crucial for operational integrity and efficiency. This ongoing industrialization, coupled with stricter regulatory standards for thermal performance and emissions, reinforces RCF's market position.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for energy-efficient industrial insulation | +1.5% | Global, Europe, North America, Asia Pacific | Mid-term to Long-term (2025-2033) |

| Expansion of high-temperature industrial sectors (e.g., steel, glass, ceramics) | +1.2% | Asia Pacific (China, India), Latin America, Middle East | Short-term to Mid-term (2025-2029) |

| Increasing adoption in new applications like automotive and aerospace for lightweighting | +0.8% | North America, Europe, Asia Pacific | Mid-term to Long-term (2027-2033) |

| Replacement demand for worn-out refractory linings in aging infrastructure | +0.5% | North America, Europe, Mature Economies | Ongoing (2025-2033) |

Refractory Ceramic Fiber Market Restraints Analysis

The Refractory Ceramic Fiber (RCF) market faces notable restraints that could temper its growth trajectory. A primary concern is the health and safety implications associated with traditional RCF products, specifically the potential for respirable fibers to cause health issues. This concern has led to stringent occupational safety regulations in many regions, necessitating expensive handling procedures, specialized protective equipment, and increased disposal costs for end-users. These regulatory hurdles and associated compliance expenses can deter adoption or favor alternative materials in certain applications, especially in highly regulated markets.

Another significant restraint is the growing competition from alternative high-temperature insulation materials, including mineral wool, micro-porous insulation, and advanced ceramic foams. These alternatives are often marketed as safer, more cost-effective, or possessing specific performance advantages in niche applications. While RCF maintains its dominance in very high-temperature environments, the continuous development of these substitute materials presents a competitive pressure. Additionally, the relatively high production cost of RCF compared to some alternatives, coupled with potential fluctuations in raw material prices, can impact its overall market competitiveness and profitability, particularly in price-sensitive sectors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent health and safety regulations regarding respirable fibers | -0.9% | Europe, North America, Japan | Ongoing (2025-2033) |

| Competition from alternative high-temperature insulation materials (e.g., mineral wool, bio-soluble fibers) | -0.7% | Global | Mid-term (2025-2030) |

| High production costs and potential raw material price volatility | -0.5% | Global | Short-term to Mid-term (2025-2028) |

| Challenges in RCF waste disposal and recycling | -0.3% | Global, Developed Economies | Long-term (2029-2033) |

Refractory Ceramic Fiber Market Opportunities Analysis

Despite existing restraints, the Refractory Ceramic Fiber (RCF) market is presented with significant opportunities for growth and innovation. A key opportunity lies in the burgeoning industrialization and infrastructure development across emerging economies, particularly in Asia Pacific and Latin America. These regions are witnessing a rapid increase in manufacturing capabilities, including expansion in iron and steel, glass, and petrochemical sectors, which inherently drives demand for high-performance thermal insulation materials like RCF. The establishment of new industrial plants and the modernization of existing facilities create a substantial market for RCF products.

Another considerable opportunity stems from the increasing demand for eco-friendly and bio-soluble RCF variants. With rising environmental awareness and stricter health regulations, manufacturers are investing in research and development to produce fibers that offer comparable performance to traditional RCFs but with significantly reduced health risks. This shift caters to a growing segment of environmentally conscious industries and positions RCF as a more sustainable high-temperature insulation solution. Furthermore, the automotive sector's continuous drive for lightweighting and enhanced thermal management, particularly in electric vehicles and advanced internal combustion engines, presents new application avenues for RCF in exhaust systems, battery insulation, and heat shields, driving specialized product innovation and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising industrialization and infrastructure development in emerging economies | +1.0% | Asia Pacific (China, India), Latin America | Mid-term to Long-term (2026-2033) |

| Growing demand for bio-soluble RCF due to health and environmental considerations | +0.8% | Global, Europe, North America | Short-term to Mid-term (2025-2030) |

| Expansion of RCF applications in automotive, aerospace, and renewable energy sectors | +0.7% | Global | Mid-term to Long-term (2027-2033) |

| Technological advancements leading to new RCF product formulations and properties | +0.5% | Global | Ongoing (2025-2033) |

Refractory Ceramic Fiber Market Challenges Impact Analysis

The Refractory Ceramic Fiber (RCF) market encounters several significant challenges that could impede its growth and operational efficiency. One prominent challenge is managing the regulatory landscape concerning RCF's health and safety. The classification of traditional RCF as a potential carcinogen in some jurisdictions, despite industry efforts to demonstrate safe usage with proper controls, continues to pose a challenge for manufacturers and end-users regarding handling, installation, and disposal. Compliance with varying global and regional regulations, and the ongoing need for extensive worker training and personal protective equipment, adds considerable operational complexity and cost.

Another critical challenge is the volatility of raw material prices, particularly for alumina and silica, which are key components in RCF production. Fluctuations in the supply and cost of these raw materials directly impact the manufacturing expenses and profit margins of RCF producers. Furthermore, maintaining supply chain stability and resilience, especially in the face of geopolitical tensions or unexpected global events (such as pandemics or trade disputes), remains a persistent concern. These disruptions can lead to material shortages, increased logistics costs, and delays in product delivery, undermining market confidence and operational predictability for RCF manufacturers and their customers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating complex and varying health and safety regulations globally | -0.8% | Global, Europe, North America | Ongoing (2025-2033) |

| Price volatility of key raw materials (alumina, silica) | -0.6% | Global | Short-term to Mid-term (2025-2028) |

| Maintaining competitiveness against alternative insulation materials with perceived safer profiles | -0.5% | Global | Mid-term (2025-2030) |

| Ensuring sustainable disposal and recycling practices for RCF waste | -0.4% | Developed Economies | Long-term (2029-2033) |

Refractory Ceramic Fiber Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Refractory Ceramic Fiber (RCF) market, offering a detailed segmentation by various parameters including product type, application, and end-use industry. It encompasses historical data, current market trends, and a robust forecast for the period up to 2033. The report meticulously examines market dynamics, identifying key drivers, restraints, opportunities, and challenges that shape the industry landscape. Furthermore, it includes a thorough competitive analysis, profiling major market players and their strategies, alongside an assessment of regional market performance and future growth prospects across key geographical areas.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.25 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Morgan Advanced Materials, Unifrax LLC, ISOLITE GmbH, Ibiden Co. Ltd., Mitsubishi Chemical Corporation, Luyang Energy-Saving Materials Co., Ltd., Rath Group, FibreCast Inc., CeramTec GmbH, Promat International, ADL Insulflex, Inc., Nutec Fibratec, Dongguk Refractories, Shandong Luyang Share Co., Ltd., Zircar Refractories, Inc., Hi-Tech Insulators, Inc., Cotronics Corp., Yeso-RCF. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Refractory Ceramic Fiber (RCF) market is comprehensively segmented to provide a granular understanding of its diverse applications and product forms, allowing for targeted market strategies and detailed trend analysis. The segmentation by product type reveals the prevalence and specific uses of RCF in various forms such as blankets, boards, and modules, each designed for distinct thermal insulation requirements in high-temperature environments. This categorization highlights the versatility of RCF in accommodating different industrial designs and operational demands, from flexible insulation blankets to rigid structural components.

Further segmentation by application areas, including furnace and kiln linings, automotive components, and fire protection systems, underscores the broad utility of RCF across a multitude of end-use industries. This detailed breakdown helps in identifying specific growth pockets and understanding the varying performance expectations in each application. The end-use industry segmentation, encompassing sectors like petrochemical, iron & steel, and ceramics, offers insights into the primary consumers of RCF, reflecting the market's dependence on the health and growth of these foundational industries. This multi-faceted segmentation ensures a holistic view of the market's structure and its inherent dynamics.

- By Product Type: Blanket, Board, Paper, Module, Vacuum Formed Shapes, Bulk, Others

- By Application: Furnace & Kiln Linings, Boilers, Ovens, Heat Treatment, Fire Protection, Automotive, Aerospace, Power Generation, Petrochemical, Iron & Steel, Ceramics, Glass, Others

- By End-Use Industry: Petrochemical, Ceramics, Iron & Steel, Aluminum, Power Generation, Others

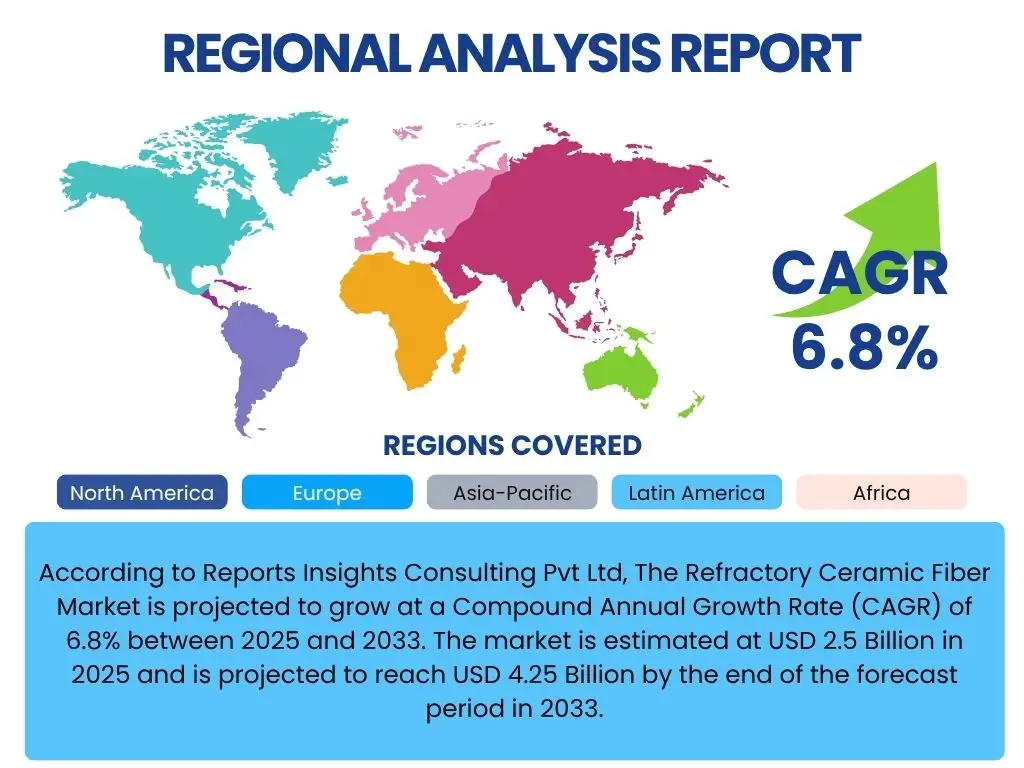

Regional Highlights

The global Refractory Ceramic Fiber (RCF) market exhibits distinct regional dynamics, influenced by industrialization levels, regulatory environments, and technological adoption rates. Asia Pacific stands as the dominant region, driven by extensive manufacturing activities and rapid industrial expansion in countries like China and India. The robust growth in the iron & steel, glass, and ceramics industries across these nations fuels a significant demand for RCF in furnace and kiln lining applications. Moreover, ongoing infrastructure development and increasing energy efficiency mandates in the region further contribute to market expansion, making it a pivotal area for RCF manufacturers and suppliers.

North America and Europe represent mature markets characterized by stringent environmental and safety regulations, which have led to a higher adoption of bio-soluble RCF alternatives and a focus on advanced performance materials. These regions are also significant for R&D in new RCF technologies and applications, particularly in automotive and aerospace sectors aiming for lightweighting and enhanced thermal management. While the growth rate may be slower compared to Asia Pacific, the established industrial base and emphasis on high-value applications ensure a steady demand. Latin America and the Middle East & Africa are emerging markets, showing promising growth due to increasing investments in industrial infrastructure and processing capabilities, particularly in the petrochemical and power generation sectors, offering new avenues for RCF market penetration.

- Asia Pacific: Largest and fastest-growing market, driven by industrialization in China and India, strong demand from iron & steel, ceramics, and glass industries, and increasing energy efficiency focus.

- North America: Mature market with steady demand, emphasis on advanced RCF products and bio-soluble alternatives, significant adoption in automotive, aerospace, and petrochemical industries.

- Europe: Characterized by stringent environmental regulations, driving innovation towards safer RCF alternatives; strong demand from established industrial sectors and growing focus on energy conservation.

- Latin America: Emerging market with increasing industrial investments, particularly in Brazil and Mexico, contributing to growing demand for RCF in various manufacturing sectors.

- Middle East & Africa: Growing market spurred by investments in oil & gas, petrochemical, and power generation industries, leading to increased adoption of RCF for high-temperature insulation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Refractory Ceramic Fiber Market.- Morgan Advanced Materials

- Unifrax LLC

- ISOLITE GmbH

- Ibiden Co. Ltd.

- Mitsubishi Chemical Corporation

- Luyang Energy-Saving Materials Co., Ltd.

- Rath Group

- FibreCast Inc.

- CeramTec GmbH

- Promat International

- ADL Insulflex, Inc.

- Nutec Fibratec

- Dongguk Refractories

- Shandong Luyang Share Co., Ltd.

- Zircar Refractories, Inc.

- Hi-Tech Insulators, Inc.

- Cotronics Corp.

- Yeso-RCF

Frequently Asked Questions

What is Refractory Ceramic Fiber (RCF)?

Refractory Ceramic Fiber (RCF) is a synthetic mineral fiber primarily composed of alumina and silica, designed for high-temperature insulation applications. It is renowned for its excellent thermal insulation properties, high-temperature stability, low thermal conductivity, and lightweight nature, making it ideal for use in industrial furnaces, kilns, and other demanding heat processing environments.

What are the primary applications of Refractory Ceramic Fiber?

RCF is extensively used across various high-temperature industrial applications, including the lining of furnaces, kilns, and ovens in the iron and steel, ceramics, glass, and petrochemical industries. Other key applications include fire protection, insulation in power generation plants, and thermal management components in the automotive and aerospace sectors due to its superior heat resistance and lightweight characteristics.

What are the key drivers for the Refractory Ceramic Fiber market growth?

The RCF market is primarily driven by the increasing global demand for energy-efficient industrial insulation, the continuous expansion of high-temperature industries like steel and glass, and the need for durable thermal management solutions in various manufacturing processes. The ongoing industrialization in emerging economies and the development of new applications in automotive and aerospace also contribute significantly to market growth.

Are there health concerns associated with RCF, and what are the alternatives?

Traditional RCF can pose health concerns due to the potential for respirable fibers, leading to stringent safety regulations in many regions. As a response, the market is seeing a growing shift towards bio-soluble or low bio-persistent (LBP) fibers, which offer similar performance with reduced health risks. Other alternatives include mineral wool, advanced ceramic foams, and microporous insulation, each with specific advantages for different temperature ranges and applications.

What is the future outlook for the Refractory Ceramic Fiber market?

The future outlook for the RCF market is positive, with projected steady growth driven by ongoing industrial demand and a strong emphasis on energy efficiency and sustainability. Innovation in bio-soluble RCFs will be a key growth propeller, addressing health and environmental considerations. While challenges like regulatory compliance and raw material price volatility persist, the indispensable role of RCF in high-temperature insulation ensures its continued relevance and expansion, particularly in industrializing regions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted