Fine Ceramic Market

Fine Ceramic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704250 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Fine Ceramic Market Size

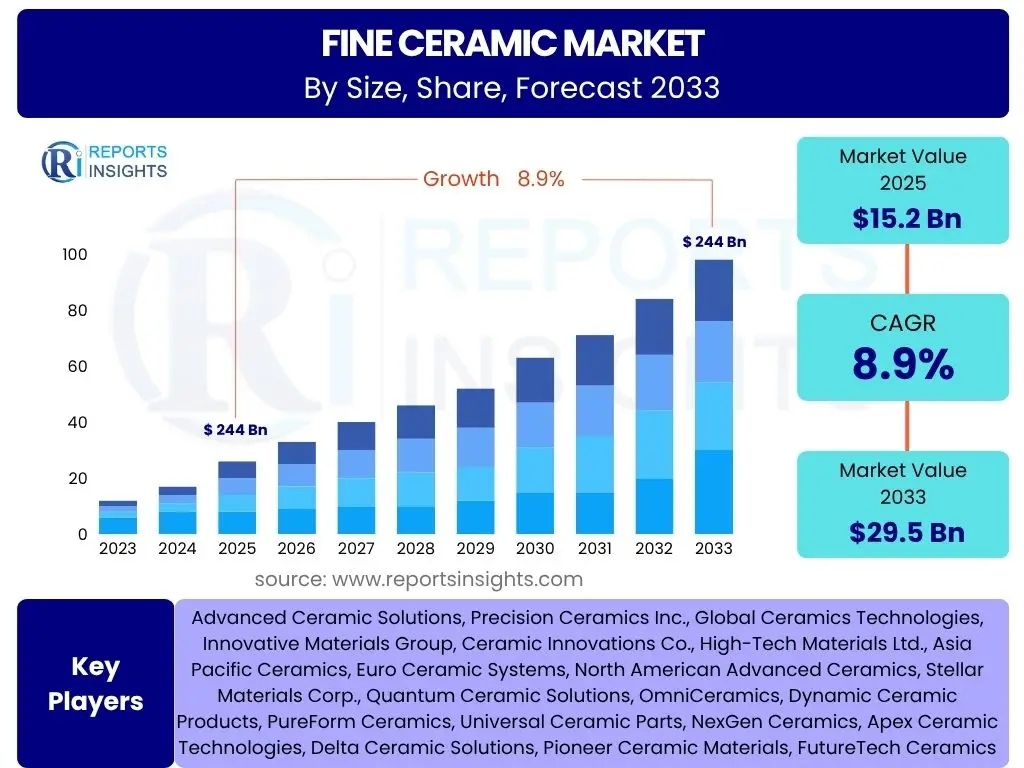

According to Reports Insights Consulting Pvt Ltd, The Fine Ceramic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 29.5 Billion by the end of the forecast period in 2033.

Key Fine Ceramic Market Trends & Insights

The Fine Ceramic market is currently experiencing a transformative phase, driven by advancements in material science and evolving industrial demands. A significant trend observed is the increasing adoption of fine ceramics in high-performance applications, where their superior properties such as wear resistance, high temperature stability, and electrical insulation are indispensable. This includes sectors like advanced electronics, electric vehicles, and medical devices, where traditional materials often fall short of stringent performance requirements. The ongoing miniaturization of electronic components, for instance, necessitates ceramic substrates and encapsulations that offer exceptional thermal management and dielectric properties in compact forms.

Furthermore, a growing emphasis on sustainability and energy efficiency is shaping the market landscape. Manufacturers are increasingly exploring eco-friendly production processes and recyclable ceramic materials, aligning with global environmental regulations and consumer preferences. Another notable insight pertains to the diversification of ceramic types and processing techniques. Beyond conventional oxides, non-oxide ceramics like silicon nitride and silicon carbide are gaining prominence for their enhanced mechanical strength and thermal shock resistance. The integration of additive manufacturing (3D printing) for complex ceramic geometries is also emerging as a key trend, enabling rapid prototyping and customized production, which could significantly reduce manufacturing lead times and costs in the long term.

- Growing demand for advanced electronic components, including those used in 5G and IoT devices.

- Increasing adoption of fine ceramics in electric vehicles (EVs) for battery components, sensors, and structural parts due to lightweight and heat resistance.

- Expansion of medical and dental applications, particularly in biocompatible implants and high-precision instruments.

- Advancements in manufacturing technologies, including additive manufacturing and precision machining, facilitating complex designs and improved performance.

- Heightened focus on energy efficiency and sustainability in production processes and material development.

- Development of smart ceramics with integrated sensing and actuating capabilities for next-generation devices.

AI Impact Analysis on Fine Ceramic

Artificial Intelligence (AI) is poised to significantly transform the Fine Ceramic industry, primarily by enhancing research and development, optimizing manufacturing processes, and improving quality control. Industry stakeholders are particularly interested in how AI can accelerate material discovery and design, allowing for the rapid identification of novel ceramic compositions with desired properties. This involves leveraging machine learning algorithms to analyze vast datasets of material properties, synthesis parameters, and performance characteristics, thereby reducing the time and cost associated with traditional trial-and-error experimentation. The predictive capabilities of AI are anticipated to streamline the development cycle for new ceramic products, enabling faster market entry for innovative solutions across various applications.

In the realm of manufacturing, AI offers substantial potential for process optimization and automation. This includes using AI-driven systems for real-time monitoring and adjustment of sintering temperatures, pressure, and atmospheric conditions, which are critical for achieving precise material microstructure and performance. Predictive maintenance, another key application, utilizes AI to analyze sensor data from manufacturing equipment, identifying potential failures before they occur and minimizing costly downtime. Concerns revolve around the initial investment required for AI infrastructure, the need for specialized data scientists and engineers, and the ethical implications of autonomous decision-making in production. Nevertheless, the industry widely expects AI to lead to higher production yields, reduced waste, and more consistent product quality, ultimately enhancing the competitive edge of ceramic manufacturers.

- Accelerated materials discovery and development through AI-driven computational modeling and data analysis.

- Optimization of ceramic manufacturing processes, including sintering, pressing, and machining, for improved efficiency and yield.

- Enhanced quality control and defect detection systems using computer vision and machine learning algorithms.

- Predictive maintenance for ceramic production equipment, minimizing downtime and operational costs.

- Automation of design and simulation tasks for complex ceramic geometries and composite structures.

- Supply chain optimization and demand forecasting for raw materials and finished fine ceramic products.

Key Takeaways Fine Ceramic Market Size & Forecast

The Fine Ceramic market is poised for robust growth, driven primarily by the escalating demand from high-technology sectors that leverage the material's unparalleled properties. A central takeaway is the critical role of innovation in material science and processing techniques. The continuous development of new ceramic compositions and advanced manufacturing methods, such as additive manufacturing and precision machining, is not only expanding the range of applications but also enhancing the performance capabilities of existing products. This innovation cycle is essential for meeting the increasingly stringent requirements of industries like electronics, automotive, and medical, where material performance directly impacts product functionality and reliability. The market's resilience is further supported by its indispensable nature in these critical applications, making it less susceptible to short-term economic fluctuations compared to other material markets.

Geographically, the Asia Pacific region is expected to maintain its dominance in both production and consumption, fueled by rapid industrialization, particularly in electronics manufacturing and electric vehicle production. This highlights the importance of strategic investments in this region for market participants. Another key insight is the growing emphasis on customization and specialized solutions. As industries evolve, the demand for fine ceramics tailored to specific application requirements is increasing, fostering a trend towards closer collaboration between ceramic manufacturers and end-use industries. Furthermore, the market's future growth is intricately linked to ongoing research and development efforts, especially in areas such as smart ceramics, biocompatible materials, and energy-efficient production, indicating a long-term trajectory of technological advancement and market expansion.

- Significant growth projected, indicating strong underlying demand across various high-tech industries.

- Asia Pacific region is anticipated to remain the leading market, driven by electronics, automotive, and industrial manufacturing growth.

- Innovation in material development and advanced processing techniques is a primary growth catalyst.

- Electronics, automotive (especially EVs), and medical sectors are the key application areas driving market expansion.

- The market's resilience is underpinned by the essential and often irreplaceable nature of fine ceramics in critical applications.

- Increasing trend towards customized and application-specific fine ceramic solutions.

Fine Ceramic Market Drivers Analysis

The expansion of the Fine Ceramic market is significantly propelled by the increasing demand from the electronics industry. Fine ceramics are indispensable in the production of electronic components such as substrates, insulators, capacitors, and packaging due to their superior dielectric properties, thermal conductivity, and high-temperature stability. The proliferation of 5G technology, Internet of Things (IoT) devices, and advanced consumer electronics necessitates materials that can withstand rigorous operating conditions while enabling miniaturization and enhanced performance. This consistent technological evolution in electronics creates a sustained and growing need for high-quality fine ceramics, directly influencing market growth rates.

Another pivotal driver is the accelerating shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs). Fine ceramics are crucial for various EV components, including battery separators, power electronics (e.g., inverters, converters), sensors, and structural parts. Their lightweight properties contribute to extended battery range, while their excellent thermal management capabilities are vital for the efficient and safe operation of high-power electrical systems. As global automotive regulations push for lower emissions and consumer adoption of EVs continues to surge, the demand for these specialized ceramic materials within the automotive sector is expected to rise sharply, providing a substantial impetus to the market's trajectory. Furthermore, the burgeoning medical and dental sectors contribute significantly, requiring biocompatible and wear-resistant ceramics for implants, prosthetics, and surgical instruments, thereby diversifying the market's application base.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Electronics Industry | +1.8% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Growing Adoption in Electric Vehicles (EVs) | +1.5% | Europe, Asia Pacific (China, Japan), North America | Mid to Long-term (2025-2033) |

| Expansion of Medical and Dental Applications | +0.9% | North America, Europe, Japan | Long-term (2025-2033) |

| Advancements in Industrial Machinery and Equipment | +0.7% | Germany, Japan, China, USA | Mid-term (2025-2030) |

Fine Ceramic Market Restraints Analysis

Despite the robust growth potential, the Fine Ceramic market faces several inherent restraints that could temper its expansion. One significant challenge is the high production cost associated with fine ceramics. The manufacturing process often involves complex and energy-intensive steps, including precise raw material purification, intricate shaping, and high-temperature sintering, which require specialized equipment and skilled labor. These factors contribute to a higher unit cost compared to conventional materials like metals or plastics, making fine ceramics less competitive in cost-sensitive applications where their superior properties are not absolutely essential. This cost barrier can limit their widespread adoption in certain volume-driven industries, particularly in developing regions.

Another major restraint is the volatility in the prices and availability of key raw materials. Many fine ceramics rely on specialized oxides and non-oxides such as high-purity alumina, zirconia, silicon nitride, and rare earth elements. The sourcing of these materials can be subject to geopolitical factors, supply chain disruptions, and fluctuating commodity prices. Any significant increase in raw material costs or supply shortages can directly impact manufacturing expenses and production timelines, leading to higher product prices and potentially reduced market demand. Furthermore, the inherent brittleness of certain fine ceramic materials, despite their exceptional hardness and wear resistance, can pose design and application challenges, requiring careful engineering and design considerations to prevent catastrophic failure, which adds to design complexity and manufacturing risk.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs and Manufacturing Complexity | -1.2% | Global, particularly developing markets | Long-term (2025-2033) |

| Volatility of Raw Material Prices and Supply | -0.8% | Global, especially regions reliant on imports | Mid-term (2025-2030) |

| Brittleness and Limited Ductility | -0.5% | Specific application areas requiring impact resistance | Long-term (2025-2033) |

| Competition from Alternative Materials | -0.3% | Global, particularly in less demanding applications | Mid-term (2025-2030) |

Fine Ceramic Market Opportunities Analysis

The Fine Ceramic market is presented with significant growth opportunities stemming from the continuous evolution of advanced technological applications. One prominent area of opportunity lies in the expanding demand for next-generation telecommunications infrastructure, specifically 5G networks and satellite communication systems. These systems require materials with exceptionally low dielectric loss, high thermal stability, and precise dimensional control for components such as antennas, filters, and high-frequency circuit boards. Fine ceramics are uniquely positioned to meet these stringent requirements, offering manufacturers a substantial avenue for market expansion as these technologies are deployed globally.

Another compelling opportunity emerges from the growing trend towards miniaturization and higher performance in various electronic and medical devices. As devices become smaller yet more powerful, the need for materials that can dissipate heat efficiently, provide superior electrical insulation, and maintain structural integrity under extreme conditions becomes paramount. Fine ceramics, with their intrinsic properties, are ideally suited for these evolving design paradigms. Furthermore, the advent of additive manufacturing (3D printing) technologies for ceramics opens up new possibilities for creating complex geometries and custom parts that were previously unachievable with traditional manufacturing methods. This innovation allows for rapid prototyping, reduced material waste, and the production of highly specialized components for niche applications in aerospace, defense, and custom medical implants, thereby creating new market segments and driving revenue growth. The push for sustainable and energy-efficient solutions also presents opportunities for developing new ceramic compositions with reduced environmental impact during production or improved performance in energy-saving applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in 5G and Advanced Communication | +1.0% | Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Integration with Additive Manufacturing (3D Printing) | +0.8% | Global, especially research-intensive regions | Long-term (2027-2033) |

| Increasing Demand for Lightweight and High-Performance Materials | +0.7% | Automotive, Aerospace, Sports industries globally | Mid to Long-term (2025-2033) |

| Development of Smart Ceramics and Composites | +0.6% | North America, Europe, Japan, South Korea | Long-term (2028-2033) |

Fine Ceramic Market Challenges Impact Analysis

The Fine Ceramic market faces several critical challenges that demand strategic responses from manufacturers and stakeholders. One significant hurdle is the requirement for substantial research and development (R&D) investments. Developing new ceramic materials with enhanced properties, improving existing manufacturing processes, and adapting to emerging application demands necessitate continuous R&D efforts. This often involves significant financial outlay, specialized laboratories, and highly skilled personnel, making it challenging for smaller players to compete effectively and for the industry as a whole to rapidly innovate without considerable capital infusion. The high cost and long lead times associated with R&D can slow down the introduction of advanced ceramic solutions to the market.

Another pervasive challenge is the shortage of skilled labor and technical expertise. The fine ceramic manufacturing process is highly specialized, requiring operators and engineers with a deep understanding of material science, powder metallurgy, and precision engineering. There is a notable gap between the demand for such skilled professionals and their availability, particularly in regions experiencing rapid industrial growth. This talent deficit can constrain production capacity, hinder technological adoption, and potentially compromise product quality. Furthermore, navigating complex regulatory frameworks, especially for medical and aerospace applications, presents a significant challenge. Adhering to stringent certifications, quality standards, and safety regulations adds to development costs and market entry barriers, requiring extensive compliance efforts and ongoing audits, which can delay market access for new products and innovations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research and Development (R&D) Costs | -0.9% | Global | Long-term (2025-2033) |

| Shortage of Skilled Labor and Technical Expertise | -0.7% | Global, particularly developed economies | Mid to Long-term (2025-2033) |

| Stringent Regulatory Compliance and Certification | -0.6% | North America, Europe, Japan | Long-term (2025-2033) |

| Intellectual Property Protection and Competitive Landscape | -0.4% | Global | Mid-term (2025-2030) |

Fine Ceramic Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Fine Ceramic market, offering a detailed overview of its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market trends, key drivers, restraints, opportunities, and challenges influencing industry dynamics. It segments the market by material type, application, end-use industry, and region, providing granular insights into each segment's contribution and growth potential. The report also highlights the competitive landscape by profiling major market players, their strategies, and recent developments, delivering valuable intelligence for stakeholders seeking to understand market positioning and strategic implications. The integration of AI impact analysis further enriches the report, addressing the transformative role of artificial intelligence in ceramic manufacturing and innovation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 29.5 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Ceramic Solutions, Precision Ceramics Inc., Global Ceramics Technologies, Innovative Materials Group, Ceramic Innovations Co., High-Tech Materials Ltd., Asia Pacific Ceramics, Euro Ceramic Systems, North American Advanced Ceramics, Stellar Materials Corp., Quantum Ceramic Solutions, OmniCeramics, Dynamic Ceramic Products, PureForm Ceramics, Universal Ceramic Parts, NexGen Ceramics, Apex Ceramic Technologies, Delta Ceramic Solutions, Pioneer Ceramic Materials, FutureTech Ceramics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fine Ceramic market is meticulously segmented to provide a granular view of its diverse components and their respective growth trajectories. This segmentation allows for a detailed understanding of market dynamics across various material compositions, end-use applications, and industry verticals, highlighting specific areas of demand and innovation. The primary segmentation dimensions include material type, application area, and the specific end-use industry, each revealing unique market characteristics and growth drivers. Analyzing these segments provides strategic insights into which ceramic types are gaining traction, where new applications are emerging, and which industries are exhibiting the highest rates of adoption for fine ceramic solutions, enabling targeted market strategies and product development.

- By Material Type: Alumina Ceramics, Zirconia Ceramics, Silicon Carbide Ceramics, Silicon Nitride Ceramics, Others (e.g., Boron Carbide, Aluminum Nitride). This segment highlights the chemical composition driving specific properties and applications.

- By Application: Electronic Components, Automotive Components, Medical and Healthcare, Industrial Machinery, Aerospace and Defense, Environmental and Energy, Others. This segment focuses on the functional use of fine ceramics across various sectors.

- By End-Use Industry: Electronics & Semiconductor, Automotive & Transportation, Medical & Healthcare, Industrial & Manufacturing, Aerospace & Defense, Energy & Environmental, Chemical & Petrochemical. This segment identifies the specific industries consuming fine ceramic products.

Regional Highlights

- Asia Pacific (APAC): Dominates the Fine Ceramic market due to robust manufacturing bases in electronics, automotive (especially EV production), and industrial machinery in countries like China, Japan, South Korea, and India. Rapid urbanization and industrialization further drive demand.

- North America: A significant market driven by technological advancements in aerospace and defense, medical devices, and high-end electronics. Strong R&D capabilities and a focus on specialized applications contribute to its growth.

- Europe: Characterized by strong automotive (premium vehicles, EVs), industrial, and medical sectors, particularly in Germany, France, and the UK. Emphasis on advanced manufacturing techniques and stringent quality standards supports market expansion.

- Latin America: Expected to show steady growth, albeit from a smaller base, driven by expanding industrial sectors and increasing foreign investments in manufacturing.

- Middle East and Africa (MEA): Emerging market with potential growth fueled by infrastructure development, diversification of economies, and increasing adoption of advanced technologies in oil and gas, and energy sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fine Ceramic Market.- Advanced Ceramic Solutions

- Precision Ceramics Inc.

- Global Ceramics Technologies

- Innovative Materials Group

- Ceramic Innovations Co.

- High-Tech Materials Ltd.

- Asia Pacific Ceramics

- Euro Ceramic Systems

- North American Advanced Ceramics

- Stellar Materials Corp.

- Quantum Ceramic Solutions

- OmniCeramics

- Dynamic Ceramic Products

- PureForm Ceramics

- Universal Ceramic Parts

- NexGen Ceramics

- Apex Ceramic Technologies

- Delta Ceramic Solutions

- Pioneer Ceramic Materials

- FutureTech Ceramics

Frequently Asked Questions

What are Fine Ceramics?

Fine ceramics, also known as advanced or engineering ceramics, are non-metallic, inorganic materials processed to achieve superior mechanical, thermal, electrical, and chemical properties. They are engineered for high-performance applications where conventional materials cannot meet the demanding requirements, often exhibiting high hardness, wear resistance, corrosion resistance, and thermal stability.

What are the primary applications of Fine Ceramics?

Fine ceramics are primarily used in high-technology applications across various industries, including electronics (substrates, insulators), automotive (sensors, battery components for EVs), medical and dental (implants, surgical instruments), industrial machinery (bearings, seals), aerospace and defense (thermal protection, structural components), and environmental/energy (catalyst supports, fuel cells).

Which region dominates the Fine Ceramic market?

The Asia Pacific (APAC) region currently dominates the Fine Ceramic market in terms of both production and consumption. This is primarily attributed to the presence of major electronics manufacturing hubs, a burgeoning automotive industry, particularly in electric vehicles, and robust industrial growth in countries such as China, Japan, and South Korea.

What are the key drivers for the Fine Ceramic market growth?

Key drivers for the Fine Ceramic market include increasing demand from the electronics industry for miniaturized and high-performance components, the rapid adoption of fine ceramics in electric vehicles due to their lightweight and thermal management properties, and the expanding use in medical and dental applications for biocompatible and wear-resistant implants. Advancements in industrial machinery also contribute significantly.

What challenges does the Fine Ceramic market face?

The Fine Ceramic market faces several challenges, including the high production costs associated with complex manufacturing processes, volatility in raw material prices and supply chains, and the inherent brittleness of some ceramic materials. Additionally, the industry is challenged by the need for substantial research and development investments and a shortage of skilled labor and technical expertise.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted