Recycled PET Market

Recycled PET Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701546 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

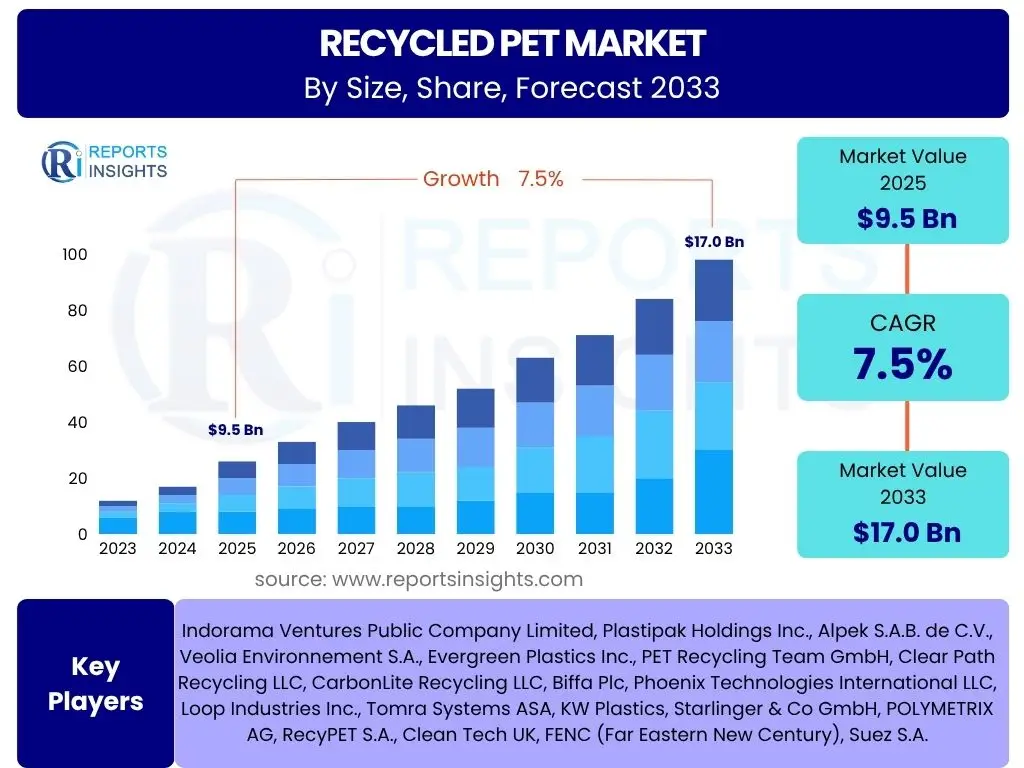

Recycled PET Market Size

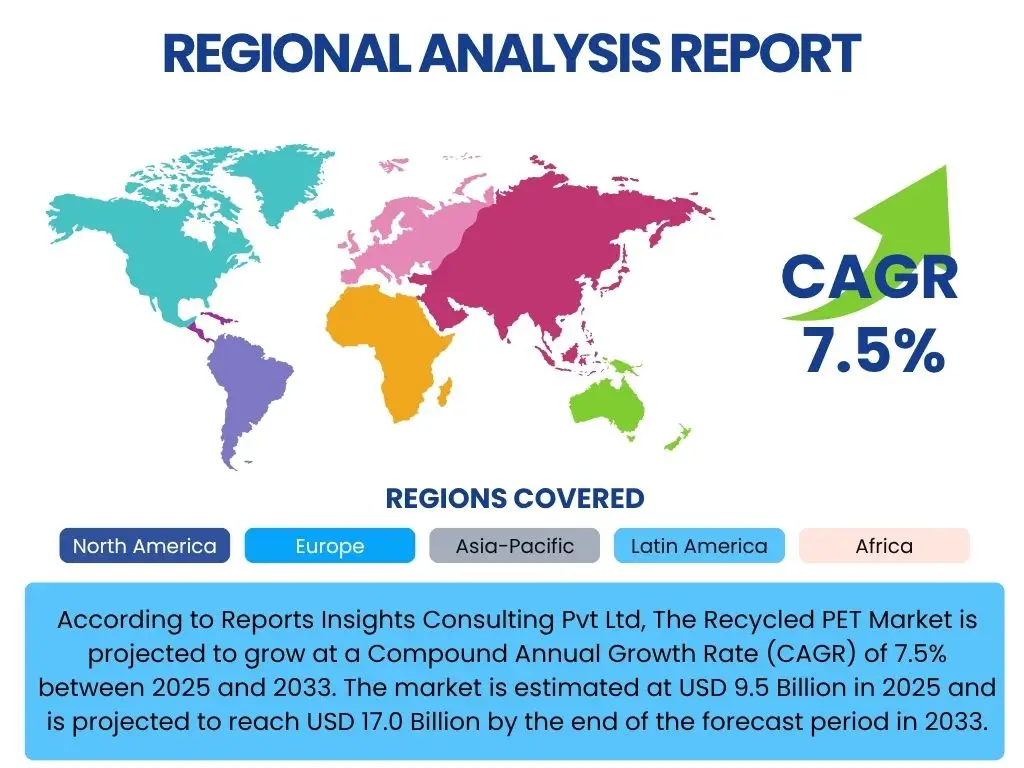

According to Reports Insights Consulting Pvt Ltd, The Recycled PET Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 9.5 Billion in 2025 and is projected to reach USD 17.0 Billion by the end of the forecast period in 2033.

Key Recycled PET Market Trends & Insights

Users frequently inquire about the driving forces behind the expansion of the Recycled PET market, particularly focusing on how sustainability objectives, circular economy principles, and technological innovations are shaping its trajectory. Common questions revolve around the increasing adoption of rPET by major brands, the impact of evolving consumer preferences towards eco-friendly products, and the role of enhanced collection and sorting infrastructures. There is also significant interest in the transition from linear to circular economic models, which positions rPET as a cornerstone material for achieving environmental stewardship.

The market is profoundly influenced by a global shift towards sustainable practices and a circular economy, driven by both regulatory pressures and corporate sustainability commitments. Brands are increasingly setting ambitious targets for incorporating recycled content into their products, particularly in packaging, which is a major catalyst for rPET demand. Furthermore, consumer awareness regarding plastic pollution has spurred a significant demand for products made from recycled materials, compelling manufacturers to adapt their supply chains and product offerings. These interconnected trends are collectively fostering an environment conducive to robust growth in the Recycled PET sector, highlighting its indispensable role in environmental sustainability.

- Increasing corporate sustainability targets and brand commitments to use recycled content.

- Growing consumer awareness and demand for eco-friendly and recycled products.

- Advancements in sorting, washing, and decontamination technologies for rPET.

- Expanding regulatory frameworks and bans on single-use plastics globally, promoting rPET adoption.

- Development of innovative applications for rPET beyond traditional packaging, including textiles and automotive.

- Rise of chemical recycling alongside mechanical recycling, offering high-quality, virgin-like rPET.

AI Impact Analysis on Recycled PET

User queries regarding the influence of Artificial Intelligence (AI) on the Recycled PET market frequently center on its potential to revolutionize efficiency, quality, and scalability within the recycling value chain. Stakeholders are keen to understand how AI can optimize the segregation of waste streams, reduce contamination rates, and improve the overall yield of high-quality rPET. Questions often arise concerning AI's application in logistics for waste collection, predictive maintenance for recycling machinery, and data analytics for market forecasting and supply chain management. The underlying expectation is that AI will introduce unprecedented levels of precision and automation, addressing some of the long-standing challenges in plastics recycling.

AI’s impact on the Recycled PET market is poised to be transformative, primarily by enhancing the intelligence and efficiency of recycling processes. AI-powered optical sorting technologies are significantly improving the accuracy and speed of identifying and separating PET from mixed waste streams, thereby reducing contamination and increasing the purity of collected material. Beyond sorting, AI algorithms can optimize logistical routes for waste collection, minimizing transportation costs and carbon footprint. Furthermore, AI contributes to predictive maintenance of recycling machinery, preventing breakdowns and ensuring continuous operation, while also providing valuable data analytics to forecast market trends and optimize supply chain operations. These applications collectively contribute to a more robust, efficient, and economically viable rPET industry.

- Enhanced sorting accuracy and speed through AI-powered optical sorters, reducing contamination.

- Optimized logistics for waste collection and transportation, leading to cost efficiencies.

- Improved quality control through automated inspection systems, ensuring consistent rPET properties.

- Predictive maintenance for recycling machinery, minimizing downtime and operational costs.

- Data-driven insights for feedstock quality assessment and market demand forecasting.

- Development of advanced material identification techniques for diverse PET waste types.

Key Takeaways Recycled PET Market Size & Forecast

Common user inquiries regarding the Recycled PET market size and forecast frequently highlight the desire to understand the core factors driving its projected growth and the strategic implications for businesses. Users are particularly interested in how environmental regulations, consumer demand for sustainable products, and corporate commitments to circularity are collectively contributing to the market's expansion. There's also a strong focus on identifying the most promising regions and applications for rPET, alongside the technological advancements that are enabling its broader adoption and quality improvement. The overarching theme is the market's transition from a niche segment to a mainstream component of the plastics industry, driven by global sustainability agendas.

The Recycled PET market is set for substantial growth, primarily propelled by increasingly stringent environmental regulations aimed at reducing plastic waste and promoting a circular economy. A significant driver is the growing commitment from major consumer brands to incorporate recycled content into their packaging, responding to heightened consumer awareness and demand for sustainable products. Technological advancements in mechanical and chemical recycling are enhancing the quality and broadening the applications of rPET, making it a viable alternative to virgin PET. This combination of regulatory push, corporate responsibility, consumer preference, and technological innovation positions the Recycled PET market as a key enabler of global sustainability initiatives, with significant investment opportunities across the value chain.

- Robust market growth driven by escalating environmental concerns and regulatory mandates.

- Increasing integration of rPET across diverse industries, particularly packaging and textiles.

- Strong corporate sustainability commitments pushing for higher recycled content targets.

- Technological advancements in recycling processes improving rPET quality and expanding its applicability.

- Significant investment opportunities in collection infrastructure and processing capabilities.

- Regional disparities in growth influenced by varying regulatory landscapes and consumer adoption rates.

Recycled PET Market Drivers Analysis

The Recycled PET market is significantly propelled by a confluence of environmental imperatives, regulatory pressures, and evolving market dynamics. Global efforts to combat plastic pollution have galvanized governments to implement policies that mandate recycled content and restrict the use of virgin plastics. Concurrently, major corporations are setting ambitious sustainability goals, committing to incorporating a higher percentage of recycled materials into their products, which directly fuels the demand for rPET. This corporate commitment is further reinforced by a growing consumer preference for eco-friendly products, creating a robust market pull for sustainable alternatives like rPET. These drivers collectively establish a strong foundation for the sustained growth of the Recycled PET market, positioning it as a cornerstone of the circular economy.

Technological innovations within the recycling sector also play a crucial role, enhancing the efficiency and effectiveness of rPET production. Advancements in sorting, washing, and decontamination processes enable the conversion of a wider range of PET waste into high-quality rPET suitable for various applications, including food-grade packaging. This improvement in quality and versatility broadens the addressable market for rPET, making it more competitive with virgin PET. The increasing investment in these advanced recycling technologies underscores the industry's commitment to overcoming technical barriers and scaling up production, thereby solidifying these drivers as fundamental to the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Policies | +2.0% | Global, particularly Europe, North America | Short to Mid-term (2025-2029) |

| Increasing Corporate Sustainability Initiatives | +1.8% | North America, Europe, Asia Pacific | Mid-term (2027-2033) |

| Rising Consumer Demand for Sustainable Products | +1.5% | Europe, North America, Asia Pacific | Short to Mid-term (2025-2029) |

| Technological Advancements in Recycling Processes | +1.2% | Global | Mid to Long-term (2027-2033) |

| Growth in Food-Grade rPET Applications | +1.0% | Global | Short to Mid-term (2025-2030) |

Recycled PET Market Restraints Analysis

Despite robust growth prospects, the Recycled PET market faces significant restraints that can impede its full potential. A primary challenge is the inconsistent supply and quality of post-consumer PET waste, which forms the crucial feedstock for rPET production. Collection systems vary widely across regions, leading to supply bottlenecks and fluctuations in raw material availability. Furthermore, the presence of contaminants in collected PET waste necessitates extensive sorting and cleaning processes, which add to operational complexities and increase production costs. These issues directly impact the efficiency and economic viability of recycling operations, making it difficult to scale up production consistently to meet growing demand.

Another notable restraint is the volatility in virgin PET prices. When virgin PET prices are low, the economic incentive to use rPET diminishes, as it becomes less cost-competitive. This fluctuating price dynamic can create uncertainty for rPET producers and discourage long-term investments in recycling infrastructure. Moreover, the capital intensity of establishing and operating advanced recycling facilities, coupled with the ongoing operational costs for energy and labor, presents a financial barrier. Addressing these restraints will require coordinated efforts across the value chain, including policy support, investment in collection infrastructure, and technological innovation to reduce processing costs and improve material quality.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inconsistent Supply and Quality of PET Waste Feedstock | -1.5% | Global, particularly developing regions | Short to Mid-term (2025-2029) |

| Contamination and Challenges in Sorting and Processing | -1.2% | Global | Short-term (2025-2027) |

| Volatility in Virgin PET Prices | -1.0% | Global | Short-term (2025-2027) |

| High Capital Investment and Processing Costs | -0.8% | Asia Pacific, Latin America | Mid-term (2027-2033) |

| Lack of Standardized Recycling Infrastructure | -0.7% | Global, especially emerging markets | Mid-term (2027-2033) |

Recycled PET Market Opportunities Analysis

The Recycled PET market presents significant opportunities for growth and innovation, driven by an expanding range of applications and technological advancements. One key area of opportunity lies in diversifying beyond traditional bottle-to-bottle recycling into new high-value end-use sectors such as automotive, construction, and specialized consumer goods. As industries increasingly prioritize sustainable materials, rPET offers a versatile and environmentally friendly alternative to virgin plastics. This expansion into novel applications not only broadens the market for rPET but also enhances its perceived value and reduces reliance on a single market segment.

Furthermore, the rapid development of chemical recycling technologies represents a transformative opportunity. While mechanical recycling remains dominant, chemical recycling processes can convert challenging PET waste streams into monomers, which can then be repolymerized into virgin-like PET. This breakthrough addresses issues of contamination and quality degradation associated with traditional methods, opening doors for an unlimited recycling loop and enabling the production of food-grade rPET from a broader feedstock base. Coupled with the rising implementation of Extended Producer Responsibility (EPR) schemes globally, which shift the financial burden of waste management to producers, these factors create a fertile ground for investment and innovation, fostering a more robust and sustainable rPET market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New High-Value Applications | +1.5% | Global (e.g., automotive, construction, textile) | Mid to Long-term (2027-2033) |

| Development of Advanced Chemical Recycling Technologies | +1.3% | Europe, North America | Long-term (2030-2033) |

| Growth in Emerging Economies with Increasing Environmental Awareness | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Implementation of Extended Producer Responsibility (EPR) Schemes | +0.9% | Europe, North America, parts of Asia | Short to Mid-term (2025-2029) |

| Increasing Investment in Collection and Sorting Infrastructure | +0.8% | Global | Short to Mid-term (2025-2029) |

Recycled PET Market Challenges Impact Analysis

The Recycled PET market faces several significant challenges that can impact its growth trajectory and operational efficiency. One prominent challenge is the logistical complexity involved in collecting, sorting, and transporting post-consumer PET waste. The fragmented nature of waste collection systems, particularly in developing regions, leads to high transportation costs and inefficiencies, making it difficult to ensure a consistent and high-quality supply of feedstock for recycling facilities. This logistical hurdle directly affects the scalability of recycling operations and the overall competitiveness of rPET against virgin materials.

Another critical challenge revolves around maintaining consistent quality of rPET, especially for sensitive applications like food-grade packaging. Contamination from other plastics, labels, and food residues requires rigorous sorting and decontamination processes, which can be expensive and technically demanding. Ensuring that rPET meets stringent regulatory and industry standards for purity and performance is a continuous battle. Furthermore, competition from other recycled plastics, such as recycled HDPE or PP, for specific applications, combined with the energy-intensive nature of some recycling processes, adds further pressure on profitability and environmental footprint. Overcoming these challenges necessitates significant investment in infrastructure, technological innovation, and collaborative efforts across the value chain to streamline processes and enhance material quality.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Logistical Complexity of Collection and Sorting Infrastructure | -1.0% | Global, especially emerging markets | Short to Mid-term (2025-2029) |

| Maintaining Consistent Quality for Food-Grade and High-Value Applications | -0.9% | Global | Short-term (2025-2027) |

| Competition from Other Recycled Plastics and Virgin Material | -0.7% | Global | Short-term (2025-2027) |

| High Energy Consumption in Recycling Processes | -0.6% | Europe, North America (due to energy costs) | Mid-term (2027-2033) |

| Public Misconceptions and Lack of Awareness about Recycling Processes | -0.5% | Global | Mid-term (2027-2033) |

Recycled PET Market - Updated Report Scope

This report provides an in-depth analysis of the Recycled PET market, offering a comprehensive overview of its current state and future projections. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges, providing a holistic perspective on the industry's ecosystem. The scope encompasses detailed segmentation analysis by various parameters, coupled with an extensive regional assessment to highlight growth hotspots and market specifics across different geographies. The report further profiles leading market players, offering insights into their strategies, product portfolios, and market positioning, enabling stakeholders to make informed decisions and identify lucrative investment avenues within the evolving Recycled PET landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 17.0 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Indorama Ventures Public Company Limited, Plastipak Holdings Inc., Alpek S.A.B. de C.V., Veolia Environnement S.A., Evergreen Plastics Inc., PET Recycling Team GmbH, Clear Path Recycling LLC, CarbonLite Recycling LLC, Biffa Plc, Phoenix Technologies International LLC, Loop Industries Inc., Tomra Systems ASA, KW Plastics, Starlinger & Co GmbH, POLYMETRIX AG, RecyPET S.A., Clean Tech UK, FENC (Far Eastern New Century), Suez S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Recycled PET market is comprehensively segmented to provide a granular understanding of its dynamics across different dimensions. These segmentations allow for a detailed analysis of market performance based on the type of rPET produced, the original source of the PET waste, its diverse applications across various product categories, and the specific end-use industries driving demand. Such a detailed breakdown aids in identifying key growth areas, understanding consumer preferences, and pinpointing technological requirements within specific market niches. This comprehensive approach ensures that all facets of the market's structure and operational flow are thoroughly explored, offering valuable insights for strategic planning.

Analyzing the market through these segments reveals critical trends. For instance, the demand for clear rPET, particularly for food-grade applications, is a major growth driver, reflecting consumer and regulatory emphasis on sustainable packaging. Similarly, the increasing use of rPET in fibers for textiles demonstrates its versatility beyond traditional bottle applications. Understanding these interdependencies and growth patterns within each segment is crucial for stakeholders to identify emerging opportunities and tailor their strategies to specific market needs. This structured approach allows for precise market sizing and forecasting within each category, offering a complete picture of the Recycled PET industry's evolution.

- By Type:

- Clear rPET

- Colored rPET

- By Source:

- Bottles

- Films & Sheets

- Fibers

- Others (e.g., strapping, automotive components)

- By Application:

- Bottles & Containers

- Beverage Bottles

- Food Jars

- Other Containers

- Films & Sheets

- Thermoforming Sheets

- Packaging Films

- Fibers

- Polyester Fibers (for textiles)

- Non-Woven Fabrics

- Strapping

- Others (e.g., Automotive Interior, Construction Materials)

- Bottles & Containers

- By End-Use Industry:

- Food & Beverage

- Packaging (Non-Food)

- Automotive

- Textile

- Consumer Goods

- Others (e.g., Industrial, Building & Construction)

Regional Highlights

- North America: This region is characterized by robust demand for rPET driven by increasing consumer awareness regarding plastic waste and stringent state-level regulations. Key factors include significant corporate sustainability commitments by major brands and expanding collection infrastructure. The U.S. and Canada are leaders in adopting rPET in packaging and textile industries.

- Europe: Europe stands as a frontrunner in the Recycled PET market, propelled by strong regulatory frameworks such as the EU's Plastic Strategy, ambitious recycling targets, and well-established circular economy initiatives. Countries like Germany, France, and the UK demonstrate high collection rates and advanced recycling technologies, especially for food-grade rPET.

- Asia Pacific (APAC): The APAC region is poised for significant growth, attributed to rapid industrialization, growing environmental concerns, and increasing investment in recycling infrastructure, particularly in China, India, and Japan. While challenges in waste collection exist, the sheer volume of plastic consumption and emerging policies are fostering a burgeoning market for rPET.

- Latin America: This region is experiencing nascent but growing adoption of rPET, driven by increasing awareness and nascent regulatory developments aimed at reducing plastic pollution. Countries like Brazil and Mexico are showing potential with emerging recycling initiatives and growing demand from the beverage industry.

- Middle East and Africa (MEA): The MEA region is at an early stage of rPET adoption but holds considerable potential due to increasing environmental awareness, burgeoning packaging industries, and strategic investments in recycling facilities, particularly in the UAE and South Africa. Regulatory frameworks are gradually evolving to support a circular economy.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Recycled PET Market.- Indorama Ventures Public Company Limited

- Plastipak Holdings Inc.

- Alpek S.A.B. de C.V.

- Veolia Environnement S.A.

- Evergreen Plastics Inc.

- PET Recycling Team GmbH

- Clear Path Recycling LLC

- CarbonLite Recycling LLC

- Biffa Plc

- Phoenix Technologies International LLC

- Loop Industries Inc.

- Tomra Systems ASA

- KW Plastics

- Starlinger & Co GmbH

- POLYMETRIX AG

- RecyPET S.A.

- Clean Tech UK

- FENC (Far Eastern New Century)

- Suez S.A.

- Avangard Innovative

Frequently Asked Questions

What is Recycled PET (rPET) and why is it important?

Recycled PET (rPET) is polyethylene terephthalate plastic that has been recovered and reprocessed from post-consumer waste. Its importance stems from its role in promoting a circular economy, significantly reducing greenhouse gas emissions, conserving energy, and decreasing reliance on virgin fossil-based resources compared to virgin PET production. It helps mitigate plastic pollution and offers a sustainable material solution for various industries.

What are the primary applications of Recycled PET?

The primary applications of Recycled PET include beverage bottles and food containers (bottle-to-bottle recycling), packaging films and sheets (e.g., thermoformed trays), textile fibers (e.g., polyester fabrics for clothing and carpets), and strapping. Emerging applications are expanding into automotive components, construction materials, and other consumer goods, diversifying its market presence.

What are the key drivers for the growth of the Recycled PET market?

The key drivers for market growth are stringent environmental regulations and policies promoting circularity, increasing corporate sustainability commitments from major brands, growing consumer demand for eco-friendly products, and advancements in recycling technologies that improve rPET quality and expand its applications. These factors collectively create a strong impetus for market expansion.

What challenges does the Recycled PET market face?

Challenges include inconsistent supply and quality of post-consumer PET waste due to varied collection systems and contamination, the volatility of virgin PET prices which can affect rPET competitiveness, high capital investment and operational costs for advanced recycling facilities, and the logistical complexities of waste collection and sorting. Maintaining consistent, high-purity rPET for all applications remains a technical hurdle.

How is Artificial Intelligence (AI) impacting the Recycled PET industry?

AI is significantly impacting the rPET industry by enhancing the efficiency and quality of recycling processes. This includes AI-powered optical sorting systems for highly accurate waste separation, predictive maintenance for machinery to reduce downtime, optimized logistics for waste collection, and data analytics for feedstock quality assessment and market forecasting. AI's role is crucial in improving purity, reducing costs, and scaling recycling operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted