PET Container Market

PET Container Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706164 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

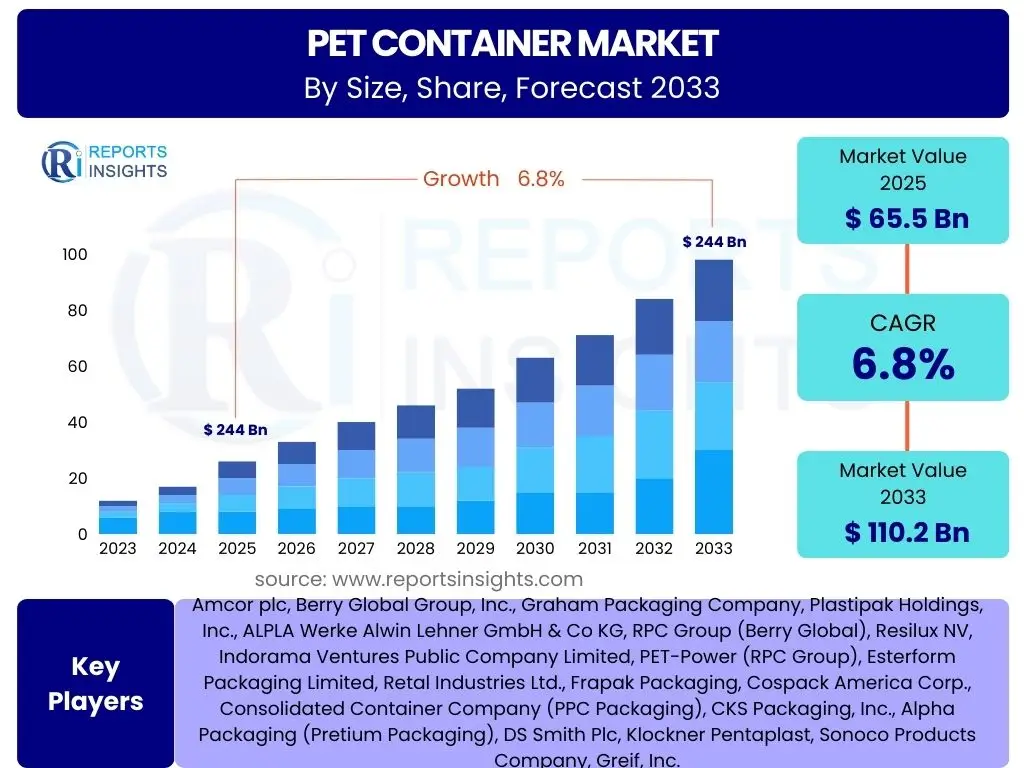

PET Container Market Size

According to Reports Insights Consulting Pvt Ltd, The PET Container Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 65.5 Billion in 2025 and is projected to reach USD 110.2 Billion by the end of the forecast period in 2033. This substantial growth is attributed to the increasing demand for packaged food and beverages, coupled with the rising adoption of PET containers across diverse end-use industries due to their advantageous properties such as lightweight, shatter resistance, and recyclability. The market expansion is further bolstered by a heightened focus on sustainable packaging solutions and the continuous innovation in PET barrier technologies that extend product shelf life and ensure product integrity.

Key PET Container Market Trends & Insights

Stakeholders frequently inquire about the evolving landscape of PET container usage, particularly focusing on sustainable practices, material innovation, and shifts in consumer preferences. Common questions revolve around the integration of recycled content, the impact of lightweighting initiatives, and how e-commerce influences packaging design and demand. Users are also keen to understand the expansion of PET into novel applications and the ongoing advancements in its functional properties, reflecting a broader industry push towards efficiency, environmental responsibility, and consumer convenience. The market is witnessing significant transformations driven by regulatory pressures for circularity and consumer demand for eco-friendly packaging solutions.

- Increasing adoption of recycled PET (rPET) and bio-based PET materials across various applications.

- Significant focus on lightweighting and optimizing the design for enhanced recyclability and reduced material consumption.

- Rapid growth in e-commerce driving the demand for robust, secure, and visually appealing PET packaging solutions.

- Expansion of PET container applications into new segments such as pharmaceuticals, home care, and industrial chemicals.

- Development and integration of advanced barrier technologies to improve shelf-life and protect sensitive contents.

- Rising consumer preference for convenient, portable, and resealable packaging formats.

- Implementation of smart packaging features, including QR codes and NFC tags, for enhanced traceability and consumer engagement.

AI Impact Analysis on PET Container

Market participants often inquire about the transformative potential of artificial intelligence within the PET container industry, with a strong emphasis on operational efficiency, supply chain resilience, and innovative design. Key user concerns include how AI can enhance manufacturing precision, optimize logistics, and contribute to circular economy initiatives through advanced sorting and material identification technologies. There is significant interest in AI's capacity to drive predictive analytics for demand forecasting, thereby reducing waste and improving resource allocation throughout the value chain. Furthermore, users seek to understand AI's role in developing more sustainable and functional PET container designs by simulating material properties and performance under various conditions.

- Enhanced predictive maintenance and anomaly detection in PET manufacturing lines, reducing downtime and improving efficiency.

- Optimized supply chain management and logistics through AI-driven demand forecasting and route optimization, minimizing transportation costs.

- Improved quality control and defect detection during production processes using AI-powered visual inspection systems.

- Advanced sorting and identification technologies leveraging AI to increase the purity and efficiency of PET recycling streams.

- AI-driven design and simulation tools facilitating the creation of lightweight, structurally optimized, and sustainable PET containers.

- Personalized packaging solutions enabled by AI analytics, tailoring designs and volumes to specific consumer preferences.

- Real-time monitoring and analysis of energy consumption in PET production, leading to optimized energy usage and reduced environmental footprint.

Key Takeaways PET Container Market Size & Forecast

User inquiries regarding the PET container market forecast often center on the primary growth catalysts, the long-term viability of the material, and its adaptability to evolving sustainability mandates. A central theme is the material's continued dominance in key sectors despite increasing scrutiny on plastics, owing to its recyclability and cost-effectiveness. Stakeholders are particularly interested in understanding how technological advancements, particularly in recycling and barrier properties, will sustain market expansion. The analysis reveals a resilient market driven by consumer convenience and industrial efficiency, with a clear trajectory towards more sustainable practices and circular economy principles. The market's future is closely tied to advancements in recycling infrastructure and the successful integration of higher proportions of recycled content.

- The PET container market is set for robust growth, driven by escalating demand for packaged consumer goods.

- Sustainability initiatives, particularly the push for rPET content, are pivotal in shaping market dynamics and consumer perception.

- Innovations in barrier technologies and lightweighting are crucial for maintaining PET's competitive edge and expanding its application scope.

- The e-commerce boom continues to be a significant catalyst for increased PET container consumption, particularly for beverages and food.

- Regulatory frameworks and consumer awareness regarding plastic waste will increasingly influence market strategies and product development.

PET Container Market Drivers Analysis

The PET container market is propelled by a confluence of factors, primarily the global rise in demand for packaged food and beverages, driven by urbanization, population growth, and changing lifestyles. Consumers' increasing preference for convenience, portability, and safety features in packaging further boosts PET adoption. Additionally, the inherent properties of PET, such as its lightweight nature, shatter resistance, and excellent barrier capabilities, make it an attractive choice for various applications. Continuous advancements in PET manufacturing and recycling technologies also contribute significantly to its market expansion, enabling more sustainable and cost-effective production methods.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for packaged food and beverages | +2.1% | Global, particularly Asia Pacific & Latin America | Short to Mid-Term |

| Increasing preference for lightweight and shatterproof packaging | +1.8% | North America & Europe | Mid-Term |

| Rising consumer awareness regarding product safety and hygiene | +1.5% | Asia Pacific & Europe | Short to Mid-Term |

| Technological advancements in PET barrier properties for extended shelf-life | +1.2% | Global | Mid to Long-Term |

| Expansion of e-commerce retail channels and logistics requirements | +1.0% | Global | Short-Term |

| Favorable cost-to-performance ratio compared to alternative materials | +0.9% | Global | Short to Mid-Term |

PET Container Market Restraints Analysis

Despite its advantages, the PET container market faces several restraints that could potentially impede its growth trajectory. Key among these are the escalating environmental concerns surrounding plastic waste and the subsequent implementation of stringent government regulations, including bans on single-use plastics and taxes on virgin plastic content in various regions. The inherent volatility in raw material prices, primarily PET resin, also poses a challenge for manufacturers, impacting production costs and profit margins. Furthermore, intense competition from alternative packaging materials like glass, metal, and carton, which are often perceived as more sustainable, continues to pressure the PET container market. Public perception issues related to plastic pollution also contribute to negative sentiment, influencing consumer choices and brand strategies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent government regulations and bans on single-use plastics | -1.5% | Europe, North America, parts of Asia Pacific | Short to Mid-Term |

| Volatility in raw material (PET resin) prices due to supply chain dynamics | -1.0% | Global | Short-Term |

| Competition from alternative packaging materials (glass, metal, cartons) | -0.8% | Global | Mid-Term |

| Public perception and negative media portrayal regarding plastic waste | -0.7% | Global, particularly developed economies | Short to Mid-Term |

PET Container Market Opportunities Analysis

The PET container market is ripe with opportunities for innovation and expansion, particularly driven by the accelerating global shift towards a circular economy. A significant avenue for growth lies in the increasing adoption of recycled PET (rPET) and the development of bio-based PET, addressing sustainability demands and reducing reliance on virgin plastics. Furthermore, the market can expand into new, high-value end-use applications, such as pharmaceuticals, nutraceuticals, and specialized homecare products, where PET's barrier properties and design flexibility offer distinct advantages. Continued technological advancements in barrier solutions, active packaging, and smart packaging also present opportunities to enhance product protection, extend shelf life, and engage consumers more effectively, ultimately unlocking new revenue streams and market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of recycled PET (rPET) and bio-based PET materials | +1.7% | Global, especially Europe & North America | Mid to Long-Term |

| Expansion into new end-use applications (e.g., healthcare, personal care, industrial chemicals) | +1.4% | Asia Pacific & Latin America | Mid-Term |

| Technological innovations in barrier and active packaging for sensitive products | +1.2% | North America & Europe | Long-Term |

| Development of advanced recycling technologies (chemical recycling) | +1.0% | Global | Long-Term |

PET Container Market Challenges Impact Analysis

The PET container market faces several formidable challenges that necessitate strategic responses from industry players. A primary concern is the significant gap in collection and sorting infrastructure for effective PET recycling, particularly evident in emerging economies, which hampers the industry's ability to achieve true circularity at scale. Furthermore, the persistent negative public perception of plastic waste, amplified by media coverage and environmental activism, directly impacts brand reputation and consumer willingness to purchase products in PET packaging. Operational challenges, such as the high energy consumption inherent in the PET manufacturing process and the complexity of managing global supply chains amidst geopolitical instability, also add layers of difficulty. Overcoming these challenges requires collaborative efforts across the value chain, significant investment in infrastructure, and effective communication strategies to reshape public opinion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inadequate collection and sorting infrastructure for recycling in emerging economies | -1.3% | Asia Pacific & MEA | Long-Term |

| Consumer perception and negative media portrayal of plastic waste and pollution | -1.0% | Global | Short to Mid-Term |

| High energy consumption during the PET manufacturing process | -0.7% | Global | Mid-Term |

| Ensuring consistent quality and supply of food-grade rPET for various applications | -0.6% | Global | Mid-Term |

PET Container Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global PET Container Market, offering an in-depth analysis of its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, significant drivers, inherent restraints, emerging opportunities, and prevailing challenges that shape the industry landscape. The scope includes a detailed segmentation analysis across various parameters such as type, end-use industry, material type, and application, providing a granular view of market composition. Furthermore, the report highlights regional market nuances and profiles leading market players, offering a holistic understanding for strategic decision-making and investment planning within the PET container sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.5 Billion |

| Market Forecast in 2033 | USD 110.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Group, Inc., Graham Packaging Company, Plastipak Holdings, Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, RPC Group (Berry Global), Resilux NV, Indorama Ventures Public Company Limited, PET-Power (RPC Group), Esterform Packaging Limited, Retal Industries Ltd., Frapak Packaging, Cospack America Corp., Consolidated Container Company (PPC Packaging), CKS Packaging, Inc., Alpha Packaging (Pretium Packaging), DS Smith Plc, Klockner Pentaplast, Sonoco Products Company, Greif, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global PET container market is meticulously segmented to provide a granular understanding of its diverse landscape and to identify specific growth drivers and market dynamics within each category. This comprehensive segmentation allows for precise market sizing, trend analysis, and competitive assessment across various dimensions. By dissecting the market based on container types, end-use industries, material compositions, and specific applications, stakeholders can gain deeper insights into the demand patterns, technological advancements, and regulatory influences impacting different facets of the market. This detailed breakdown facilitates strategic planning, product development, and targeted market entry strategies for participants within the PET packaging ecosystem.

- By Type: This segment classifies PET containers based on their physical form and intended use.

- Bottles & Jars: Predominantly used for beverages, food, personal care, and pharmaceuticals due to their versatility and resealable nature.

- Trays & Clamshells: Common in food packaging for fresh produce, bakery items, and ready meals, valued for transparency and protection.

- Other Containers: Includes specialized forms like tubs, pots, and custom-molded containers for various industrial and consumer goods.

- By End-Use Industry: This segment categorizes PET container consumption based on the primary sector utilizing the packaging.

- Beverages: The largest segment, encompassing Carbonated Soft Drinks, Bottled Water, Juices & Other Beverages, driven by high consumption rates.

- Food: Includes packaging for Edible Oils, Sauces & Dressings, Spreads, and Other Food Products, where transparency and barrier properties are crucial.

- Personal Care & Cosmetics: Used for shampoos, lotions, creams, and make-up, valuing aesthetic appeal and chemical resistance.

- Pharmaceuticals: Employed for syrups, pills, and other medical products, demanding high levels of safety and sterility.

- Homecare: Covers detergents, cleaners, and other household products, requiring robust and chemical-resistant containers.

- Industrial Chemicals: Used for packaging various non-food industrial liquids and materials.

- Others: Encompasses miscellaneous applications such as automotive fluids, sports nutrition, and pet care products.

- By Material Type: This segment differentiates between the raw material source of PET containers.

- Virgin PET: Produced directly from petrochemical feedstocks, offering consistent quality and clarity.

- Recycled PET (rPET): Derived from post-consumer PET waste, crucial for achieving sustainability goals and reducing environmental impact.

- By Application: This segment broadly categorizes the functional purpose of the PET containers.

- Packaging: Encompasses all applications where PET is used to contain and protect products for retail and consumer use.

- Storage: Refers to applications where PET containers are used for long-term or bulk storage of various materials.

Regional Highlights

- North America: This region represents a mature and significant market for PET containers, characterized by high consumer spending and a strong emphasis on sustainable packaging solutions. There is substantial adoption of rPET in beverage and food packaging, driven by corporate sustainability targets and increasing consumer awareness. The market benefits from advanced recycling infrastructure, though efforts continue to enhance collection rates and processing capabilities. Innovation in lightweighting and barrier technologies is also a key regional trend.

- Europe: Leading the global transition towards a circular economy, Europe is a pivotal region for the PET container market, defined by stringent regulations and ambitious recycling targets. The European Union's directives on single-use plastics and mandatory rPET content in bottles are powerful drivers for innovation in collection, sorting, and advanced recycling technologies. High demand for sustainable and recyclable packaging solutions from both consumers and brand owners further stimulates market growth and material innovation.

- Asia Pacific (APAC): The Asia Pacific region is the fastest-growing market for PET containers, fueled by rapid urbanization, increasing disposable incomes, and the burgeoning growth of packaged food and beverage industries. Countries like China, India, and Southeast Asian nations are witnessing significant expansion in manufacturing capacities and consumer demand. While challenges exist concerning waste management and recycling infrastructure, there is a growing recognition and investment in developing sustainable practices and improving collection systems across the region.

- Latin America: The PET container market in Latin America is experiencing robust growth, primarily driven by expanding beverage and food sectors and an increasing demand for convenient and affordable packaged goods. Brazil and Mexico are key contributors to the regional market. While recycling rates are improving, infrastructure development remains a focus area to support the growing consumption of PET containers. Consumer preference for lightweight and shatterproof packaging also contributes to market expansion.

- Middle East and Africa (MEA): This emerging market for PET containers is characterized by rising demand for packaged consumer goods due to population growth, urbanization, and changing consumption patterns. Investments in manufacturing facilities are increasing to meet the growing demand. While recycling infrastructure is still developing in many parts of the region, there is a growing emphasis on adopting sustainable practices and improving waste management systems, presenting long-term opportunities for PET container manufacturers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PET Container Market.- Amcor plc

- Berry Global Group, Inc.

- Graham Packaging Company

- Plastipak Holdings, Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Resilux NV

- Indorama Ventures Public Company Limited

- Esterform Packaging Limited

- Retal Industries Ltd.

- Frapak Packaging

- Cospack America Corp.

- Consolidated Container Company (PPC Packaging)

- CKS Packaging, Inc.

- Alpha Packaging (Pretium Packaging)

- DS Smith Plc

- Klockner Pentaplast

- Sonoco Products Company

- Greif, Inc.

- Silgan Holdings Inc.

- Ball Corporation

Frequently Asked Questions

Analyze common user questions about the PET Container market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size and growth forecast for PET containers?

The global PET Container Market is estimated at USD 65.5 Billion in 2025 and is projected to reach USD 110.2 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period. This growth is driven by increasing demand for packaged food and beverages, along with the material's advantageous properties.

How is sustainability influencing the PET container market?

Sustainability is a major driver, with increasing adoption of recycled PET (rPET) and bio-based PET materials. The industry is focusing on lightweighting, design for recyclability, and developing advanced recycling technologies to meet environmental regulations and consumer demand for eco-friendly packaging solutions.

What role does recycled PET (rPET) play in the market?

Recycled PET (rPET) is pivotal for the market's sustainable growth, significantly reducing reliance on virgin plastics and lowering the carbon footprint. Its adoption is increasing across various end-use industries, supported by regulatory mandates and brand commitments to circularity, making it a key component of future PET container production.

What are the primary challenges faced by the PET container industry?

Key challenges include stringent government regulations against single-use plastics, volatility in raw material prices, intense competition from alternative packaging materials, and the need for significant investment in collection and sorting infrastructure, particularly in developing regions, to enhance recycling efficiency.

Which regions are driving the growth of the PET container market?

The Asia Pacific region is the fastest-growing market due to urbanization and rising disposable incomes. North America and Europe continue to be significant markets, driven by mature consumer bases and strong sustainability initiatives, including high adoption of rPET and advanced recycling technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted