Public Cloud Service Market

Public Cloud Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704168 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

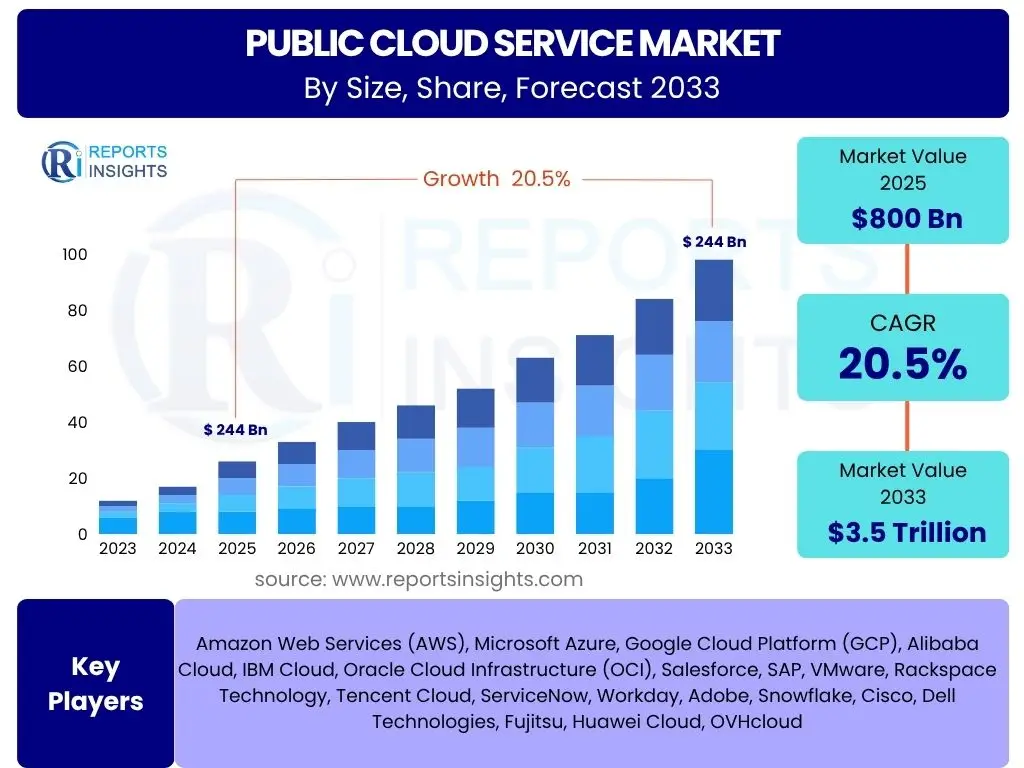

Public Cloud Service Market Size

According to Reports Insights Consulting Pvt Ltd, The Public Cloud Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033. The market is estimated at USD 800 Billion in 2025 and is projected to reach USD 3.5 Trillion by the end of the forecast period in 2033.

Key Public Cloud Service Market Trends & Insights

User inquiries frequently highlight the evolving landscape of public cloud adoption, focusing on strategic shifts and technological advancements. A dominant theme is the increasing sophistication of cloud deployments, moving beyond simple infrastructure provisioning to complex, integrated, and intelligent environments. This includes a pronounced shift towards hybrid and multi-cloud strategies, driven by a need for workload optimization, data sovereignty, and vendor diversification. Furthermore, there has been significant interest in how public cloud platforms are enabling advanced technologies such as artificial intelligence, machine learning, and edge computing, making these capabilities more accessible and scalable for enterprises of all sizes.

Another crucial insight from user questions is the growing emphasis on specialized cloud solutions tailored for specific industries, often incorporating regulatory compliance and data governance features. This indicates a maturation of the public cloud market, where generic solutions are being augmented by highly customized offerings. Sustainability in cloud operations, including energy efficiency and carbon footprint reduction, is also emerging as a significant concern, influencing procurement decisions and highlighting a broader societal responsibility aspect of cloud service providers. The continuous evolution of managed services and serverless computing is further simplifying cloud operations, allowing businesses to focus more on their core competencies.

- Hybrid and Multi-Cloud Adoption: Increased strategic integration of diverse cloud environments for optimal workload placement and resilience.

- Industry-Specific Cloud Solutions: Development of tailored cloud offerings that meet unique regulatory, security, and operational requirements of vertical industries.

- Serverless Computing Expansion: Growing preference for serverless architectures to enhance agility, reduce operational overhead, and optimize cost.

- Edge Computing Integration: Extension of cloud capabilities to the network edge, enabling low-latency data processing for IoT and real-time applications.

- Cloud Sustainability Initiatives: Focus on energy-efficient data centers and carbon-neutral cloud operations.

- AI and Machine Learning as a Service (AIaaS/MLaaS): Deep integration of advanced AI and ML capabilities directly into public cloud platforms.

- Enhanced Cloud Security and Compliance: Continuous innovation in security measures and governance tools to address evolving threats and regulatory landscapes.

AI Impact Analysis on Public Cloud Service

Common user questions regarding the impact of Artificial Intelligence (AI) on public cloud services often revolve around how AI is transforming cloud capabilities, what new services are emerging, and the implications for data management and processing. Users are keen to understand how AI is both a significant consumer of cloud resources, driving demand for compute and storage, and simultaneously a powerful enabler, enhancing cloud platform functionalities. The integration of AI tools, platforms, and models directly into cloud ecosystems is a key theme, making advanced analytics, natural language processing, and computer vision accessible to a wider range of businesses without significant upfront infrastructure investment. This integration allows enterprises to leverage sophisticated AI capabilities on a pay-as-you-go model, accelerating their digital transformation initiatives.

Furthermore, inquiries frequently touch upon the ways AI is optimizing cloud operations themselves, from resource allocation and cost management to predictive maintenance and security anomaly detection. This internal application of AI by cloud providers results in more efficient, resilient, and secure cloud environments. There is also a strong interest in how AI, when combined with public cloud scalability, facilitates the processing of massive datasets, enabling deeper insights and faster innovation across various industries. The synergy between AI and public cloud is seen as a foundational element for future enterprise IT strategies, supporting everything from autonomous systems to personalized customer experiences. Concerns typically center on the ethical implications of AI, data privacy, and the specialized skills required to fully leverage AI on cloud platforms.

- Increased Demand for Compute and Storage: AI workloads, particularly for training large models, necessitate vast computational resources and data storage, directly driving public cloud consumption.

- Democratization of AI: Public cloud platforms offer AI-as-a-Service (AIaaS), making complex AI/ML capabilities accessible to businesses without specialized infrastructure.

- Enhanced Cloud Service Offerings: AI is integrated into existing cloud services to improve performance, security, and automation, such as intelligent monitoring and predictive analytics.

- Optimization of Cloud Infrastructure: AI algorithms are employed by cloud providers for dynamic resource allocation, cost optimization, and energy management within data centers.

- Facilitation of Big Data Analytics: The scalability of public cloud, combined with AI, enables efficient processing and analysis of massive, diverse datasets.

- New AI-Driven Workloads: Emergence of new applications and services, such as generative AI, requiring specialized AI models and accelerated computing from the cloud.

- Development of Specialized AI Hardware: Increased demand for cloud instances powered by GPUs, TPUs, and other AI accelerators.

Key Takeaways Public Cloud Service Market Size & Forecast

Analysis of user inquiries concerning the public cloud market size and forecast reveals a predominant interest in understanding the sheer scale of projected growth and its underlying drivers. Users are keen to identify the primary catalysts propelling this expansion, such as digital transformation initiatives, the proliferation of data, and the increasing adoption of cloud-native applications across various sectors. A key takeaway is the consistent and robust double-digit growth anticipated, indicating that public cloud is not merely a transient trend but a fundamental shift in enterprise IT infrastructure and service delivery. This sustained growth underscores the indispensable role of cloud computing in modern business operations, offering unparalleled scalability, flexibility, and cost efficiency.

Furthermore, user questions often delve into the implications of this growth for different market segments and regions. It is evident that while large enterprises continue to be significant consumers, small and medium-sized enterprises (SMEs) are increasingly leveraging public cloud services to level the playing field, accessing enterprise-grade technology without prohibitive upfront investments. The forecast highlights a continuing trend of cloud providers expanding their global footprints and diversifying their service portfolios to capture new market opportunities, particularly in emerging economies and highly regulated industries. The market's trajectory suggests a future where cloud computing is the default mode for IT infrastructure, enabling innovation and resilience on a global scale.

- Unprecedented Growth Trajectory: The public cloud market is poised for significant expansion, driven by continuous digital transformation across industries.

- Strategic Imperative for Businesses: Cloud adoption is no longer optional but a critical component for achieving agility, scalability, and competitive advantage.

- Broad Sector Adoption: Growth is comprehensive, spanning various industries from traditional enterprises to digital-native startups, demonstrating widespread utility.

- Investment in Innovation: Cloud providers are heavily investing in advanced technologies like AI, IoT, and edge computing to enhance service offerings and create new market segments.

- Focus on Verticalization: Increasing emphasis on developing industry-specific cloud solutions to meet specialized needs and compliance requirements.

Public Cloud Service Market Drivers Analysis

The public cloud service market's robust expansion is primarily fueled by the accelerating pace of digital transformation across industries worldwide. Enterprises are increasingly migrating legacy systems and developing new, cloud-native applications to enhance operational efficiency, foster innovation, and improve customer experiences. The inherent scalability, flexibility, and cost-effectiveness offered by public cloud platforms provide a compelling alternative to traditional on-premise IT infrastructure, enabling businesses to adapt quickly to dynamic market conditions without significant upfront capital expenditures. This shift is further bolstered by the growing recognition that public cloud can support diverse workloads, from routine business applications to complex analytical processing, making it a versatile foundation for modern IT strategies.

Another significant driver is the widespread adoption of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), Big Data analytics, and the Internet of Things (IoT). These technologies generate vast amounts of data and require immense computational power, which public cloud platforms are uniquely positioned to provide on demand. The ability to access sophisticated AI/ML models, scalable data lakes, and powerful processing capabilities as a service allows organizations to rapidly develop and deploy innovative solutions, democratizing access to cutting-edge technology. Furthermore, the increasing remote work trends and the need for business continuity have highlighted the critical role of cloud services in ensuring seamless operations and global collaboration, pushing organizations further into the public cloud ecosystem.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Digital Transformation Initiatives | +5.0% | Global, especially North America & APAC | Short to Mid-term (2025-2029) |

| Growing Adoption of AI, ML, and IoT | +4.5% | Global, all developed and emerging economies | Mid to Long-term (2027-2033) |

| Increased Demand for Scalability & Flexibility | +4.0% | Global, across all enterprise sizes | Short to Mid-term (2025-2030) |

| Cost Efficiency & Reduced Operational Expenditure | +3.5% | Global, particularly SMEs & cost-sensitive markets | Short to Mid-term (2025-2028) |

| Proliferation of Remote Work & Hybrid Models | +3.0% | Global, highly impactful in North America & Europe | Short-term (2025-2027) |

| Focus on Core Business Operations | +2.5% | Global, across all enterprise types | Mid-term (2026-2031) |

| Rise of Cloud-Native Application Development | +2.0% | Global, especially tech-forward sectors | Mid to Long-term (2028-2033) |

Public Cloud Service Market Restraints Analysis

Despite the pervasive growth of the public cloud market, several significant restraints pose challenges to its unbridled expansion. Paramount among these are persistent data security and privacy concerns. Organizations, particularly those handling sensitive customer or proprietary information, remain wary of storing critical data on third-party public infrastructure, fearing breaches, unauthorized access, or compliance violations. This apprehension is often exacerbated by the complex and evolving global regulatory landscape concerning data residency and protection, such as GDPR, HIPAA, and CCPA, which can complicate multi-region cloud deployments and necessitate stringent governance frameworks that not all providers uniformly offer.

Another notable restraint is the issue of vendor lock-in. Once an organization commits to a specific public cloud provider's ecosystem, migrating applications and data to another provider can be complex, costly, and time-consuming due to proprietary APIs, services, and data formats. This perceived lack of portability limits flexibility and can result in dependency on a single vendor, potentially leading to higher long-term costs and reduced negotiating power. Furthermore, managing the costs associated with large-scale public cloud adoption can become unexpectedly complex for some organizations, particularly when consumption scales rapidly and requires sophisticated optimization strategies. The initial allure of pay-as-you-go can sometimes lead to 'bill shock' if resources are not effectively monitored and managed, presenting a hurdle for continued or expanded adoption for some enterprises.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -3.5% | Global, highly relevant in highly regulated industries (BFSI, Healthcare) | Short to Long-term (2025-2033) |

| Vendor Lock-in and Portability Challenges | -3.0% | Global, particularly for large enterprises with complex IT | Mid to Long-term (2026-2033) |

| Complex Cloud Cost Management | -2.5% | Global, affecting organizations scaling cloud usage | Short to Mid-term (2025-2029) |

| Regulatory and Compliance Complexity | -2.0% | Global, especially in Europe (GDPR) and specific industries | Short to Long-term (2025-2033) |

| Network Latency and Performance Issues for Edge Computing | -1.5% | Regions with limited network infrastructure, remote areas | Short to Mid-term (2025-2030) |

| Skill Gap in Cloud Expertise | -1.0% | Global, impacting pace of adoption in all regions | Short to Long-term (2025-2033) |

| Legacy System Integration Challenges | -0.5% | Mature markets with extensive on-premise infrastructure | Mid-term (2026-2031) |

Public Cloud Service Market Opportunities Analysis

The public cloud service market presents substantial opportunities for continued expansion and innovation. A primary avenue for growth lies in the increasing demand for specialized, industry-specific cloud solutions. As sectors like healthcare, finance, and manufacturing face unique regulatory requirements and operational complexities, tailored cloud offerings that combine industry expertise with cloud scalability are gaining traction. These vertical cloud solutions can address compliance needs, facilitate data exchange within specific ecosystems, and accelerate digital transformation for niche markets, offering new revenue streams for cloud providers and specialized benefits for customers.

Another significant opportunity stems from the burgeoning adoption of hybrid and multi-cloud strategies. While previously seen as a potential restraint, the growing maturity of multi-cloud management platforms and services allows organizations to leverage the best-of-breed services from multiple providers while maintaining control over data placement and ensuring business continuity. This trend fosters an environment for new tools, integration services, and consulting expertise that facilitate seamless operations across disparate cloud environments. Furthermore, the expansion of edge computing, driven by IoT and 5G, creates a vast opportunity for public cloud providers to extend their compute and storage capabilities closer to data sources, enabling low-latency processing and real-time analytics for a multitude of new applications and use cases, from smart factories to autonomous vehicles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Industry-Specific Cloud Solutions | +4.0% | Global, strong in BFSI, Healthcare, Manufacturing | Mid to Long-term (2027-2033) |

| Growth in Hybrid and Multi-Cloud Management Platforms | +3.5% | Global, especially for large enterprises with diverse workloads | Short to Mid-term (2025-2030) |

| Integration with Edge Computing and 5G Technologies | +3.0% | Global, particularly in smart cities, industrial IoT, autonomous vehicles | Mid to Long-term (2028-2033) |

| Development of Advanced Cloud Security Services | +2.5% | Global, driven by increasing cyber threats | Short to Long-term (2025-2033) |

| Increased Adoption by Small and Medium Enterprises (SMEs) | +2.0% | Emerging economies, underserved markets, and traditional businesses | Short to Mid-term (2025-2029) |

| Focus on Cloud Sustainability and Green Initiatives | +1.5% | Europe, North America, environmentally conscious regions | Mid to Long-term (2027-2033) |

| Growth in Managed Cloud Services | +1.0% | Global, for organizations lacking in-house cloud expertise | Short to Mid-term (2025-2030) |

Public Cloud Service Market Challenges Impact Analysis

The public cloud service market, while experiencing substantial growth, faces several significant challenges that necessitate strategic responses from providers and adopters alike. Cybersecurity threats represent a persistent and escalating challenge, with sophisticated attacks targeting cloud infrastructure, data, and applications becoming more frequent. Organizations migrating to the cloud must contend with the shared responsibility model, ensuring their data and applications are adequately protected, while providers continuously invest in advanced security measures to maintain trust. This constant arms race against cybercriminals demands continuous innovation and vigilance, potentially impacting both adoption rates and operational costs for businesses.

Another critical challenge is the inherent complexity associated with managing multi-cloud environments and ensuring seamless interoperability between different cloud providers and on-premise systems. While multi-cloud offers benefits, it can lead to increased operational overhead, fragmented management tools, and challenges in data synchronization and application portability. This complexity can deter organizations with limited IT resources or expertise from fully realizing the benefits of a diverse cloud strategy. Furthermore, the global talent shortage in cloud architecture, security, and specialized AI/ML skills poses a significant impediment to organizations looking to fully leverage public cloud capabilities, slowing down adoption and innovation within enterprises.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving Cybersecurity Threats and Data Breaches | -3.0% | Global, critical for all cloud users | Short to Long-term (2025-2033) |

| Complex Multi-Cloud Management and Interoperability | -2.5% | Global, especially for large, diversified IT environments | Mid-term (2026-2031) |

| Shortage of Cloud-Skilled IT Professionals | -2.0% | Global, impacting pace of enterprise cloud adoption | Short to Long-term (2025-2033) |

| Ensuring Data Sovereignty and Compliance Across Borders | -1.5% | Europe, Asia Pacific, highly regulated industries | Short to Long-term (2025-2033) |

| Cost Optimization and Governance in Large-Scale Deployments | -1.0% | Global, for organizations with extensive cloud usage | Short to Mid-term (2025-2029) |

| Performance Consistency in Distributed Environments | -0.5% | Global, especially for real-time applications and edge computing | Mid-term (2026-2031) |

Public Cloud Service Market - Updated Report Scope

This report provides a comprehensive analysis of the Public Cloud Service market, offering in-depth insights into its size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It meticulously forecasts market trends from 2025 to 2033, building upon historical data from 2019 to 2023. The scope encompasses detailed segmentation analysis by service model, deployment model, organization size, and end-use industry, providing a granular view of market dynamics. Furthermore, the report profiles key players, offering strategic intelligence on their market positioning and competitive landscape. It aims to equip stakeholders with actionable insights to navigate the evolving public cloud ecosystem effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 800 Billion |

| Market Forecast in 2033 | USD 3.5 Trillion |

| Growth Rate | 20.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), Alibaba Cloud, IBM Cloud, Oracle Cloud Infrastructure (OCI), Salesforce, SAP, VMware, Rackspace Technology, Tencent Cloud, ServiceNow, Workday, Adobe, Snowflake, Cisco, Dell Technologies, Fujitsu, Huawei Cloud, OVHcloud |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The public cloud service market is extensively segmented to provide a nuanced understanding of its diverse components and adoption patterns. This granular approach allows for targeted analysis of market opportunities and challenges across different service models, deployment strategies, organizational scales, and end-use industries. The segmentation highlights distinct growth drivers and competitive landscapes within each category, reflecting the varied needs and priorities of cloud consumers.

- Service Model:

- Infrastructure-as-a-Service (IaaS): Provides virtualized computing resources over the internet, including virtual machines, storage, and networking.

- Platform-as-a-Service (PaaS): Offers a complete development and deployment environment in the cloud, with resources that enable organizations to deliver everything from simple cloud-based apps to sophisticated, cloud-enabled enterprise applications.

- Software-as-a-Service (SaaS): Delivers fully functional applications over the internet, accessible via a web browser, eliminating the need for installation and maintenance on local devices.

- Deployment Model:

- Public Cloud: Services delivered over the open internet and available to anyone who wants to purchase them.

- Hybrid Cloud: A mix of public cloud, private cloud, and on-premises infrastructure with orchestration between them.

- Multi-Cloud: The use of two or more cloud computing services from different cloud providers.

- Organization Size:

- Small & Medium Enterprises (SMEs): Businesses with limited IT budgets and infrastructure, leveraging cloud for scalability and cost efficiency.

- Large Enterprises: Corporations with extensive IT needs, adopting cloud for digital transformation, global reach, and innovation.

- End-Use Industry:

- BFSI (Banking, Financial Services & Insurance): Utilizing cloud for data analytics, customer engagement, and regulatory compliance.

- IT & Telecommunications: Core adopters, leveraging cloud for network infrastructure, software development, and service delivery.

- Healthcare & Life Sciences: Employing cloud for patient data management, research, and telemedicine.

- Retail & Consumer Goods: Using cloud for e-commerce platforms, supply chain management, and personalized customer experiences.

- Manufacturing: Adopting cloud for IoT data processing, operational efficiency, and smart factory initiatives.

- Government & Public Sector: Migrating to cloud for improved citizen services, data management, and operational resilience.

- Education: Utilizing cloud for e-learning platforms, research, and administrative systems.

- Media & Entertainment: Leveraging cloud for content delivery, streaming services, and media production workflows.

- Others: Includes diverse sectors like Energy & Utilities, Automotive, and Logistics, adapting cloud for specific operational needs.

Regional Highlights

- North America: This region maintains a dominant position in the public cloud service market, characterized by early adoption, high digital maturity, and the presence of numerous leading cloud service providers. Strong investment in AI, IoT, and advanced analytics further fuels growth, particularly in the IT and telecommunications, healthcare, and financial services sectors. The United States accounts for the largest share due to its robust technology infrastructure and innovative enterprise landscape.

- Europe: Europe is a rapidly expanding market, driven by stringent data protection regulations like GDPR, which incentivize cloud providers to offer region-specific compliant solutions. Digital transformation initiatives across various industries, coupled with growing investments in cloud-native applications and hybrid cloud strategies, contribute significantly to market growth. Countries like the UK, Germany, and France are key contributors, focusing on secure and sovereign cloud solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid digitalization, increasing internet penetration, and the expansion of local and international cloud providers. Emerging economies like India and Southeast Asian countries are experiencing exponential growth due to their large unserved markets and government initiatives promoting cloud adoption. China, with its vast internal market and strong domestic cloud ecosystem, remains a significant player. The region's focus on mobile-first strategies and burgeoning startup ecosystems further propels cloud consumption.

- Latin America: This region shows significant potential for growth, driven by increasing awareness of cloud benefits, digital transformation efforts in traditional industries, and expanding internet infrastructure. Countries like Brazil and Mexico are leading the adoption, particularly in sectors such as retail, finance, and government, as businesses seek cost efficiencies and improved scalability.

- Middle East and Africa (MEA): The MEA region is experiencing substantial growth in public cloud services, largely due to government-led smart city initiatives, economic diversification efforts, and increasing investment in digital infrastructure. Countries in the Gulf Cooperation Council (GCC) are at the forefront of cloud adoption, with a strong emphasis on data localization and sovereign cloud solutions for sectors like oil and gas, government, and finance.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Public Cloud Service Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud Platform (GCP)

- Alibaba Cloud

- IBM Cloud

- Oracle Cloud Infrastructure (OCI)

- Salesforce

- SAP

- VMware

- Rackspace Technology

- Tencent Cloud

- ServiceNow

- Workday

- Adobe

- Snowflake

- Cisco

- Dell Technologies

- Fujitsu

- Huawei Cloud

- OVHcloud

Frequently Asked Questions

Analyze common user questions about the Public Cloud Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Public Cloud Service?

Public cloud service refers to computing services offered by third-party providers over the public internet, making them available to anyone who wants to use or purchase them. These services can include infrastructure (IaaS), platforms (PaaS), or software (SaaS) and are often delivered on a pay-as-you-go model.

What are the primary benefits of adopting Public Cloud Services?

The main benefits include scalability and flexibility, allowing businesses to easily scale resources up or down as needed; cost efficiency, by converting capital expenditures to operational expenditures; enhanced reliability and security, due to providers' robust infrastructure; and accelerated innovation through access to advanced technologies like AI and machine learning.

What are the main challenges associated with Public Cloud adoption?

Key challenges include ensuring data security and privacy in a shared environment, managing complex cloud costs effectively, addressing vendor lock-in concerns, navigating evolving regulatory compliance requirements, and mitigating the shortage of skilled cloud professionals.

How is AI impacting the Public Cloud Service market?

AI significantly impacts the public cloud by driving demand for high-performance computing and storage, offering AI-as-a-Service to democratize AI capabilities, enhancing cloud infrastructure optimization, and enabling new AI-driven applications and workloads. It positions public cloud as the ideal platform for AI development and deployment.

What are the future trends shaping the Public Cloud Service market?

Future trends include continued growth in hybrid and multi-cloud strategies, expansion into specialized industry-specific cloud solutions, deeper integration with edge computing and 5G, increasing focus on cloud sustainability, and the proliferation of serverless computing architectures for greater agility and efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted