Internet of Thing Telecom Service Market

Internet of Thing Telecom Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704474 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Internet of Thing Telecom Service Market Size

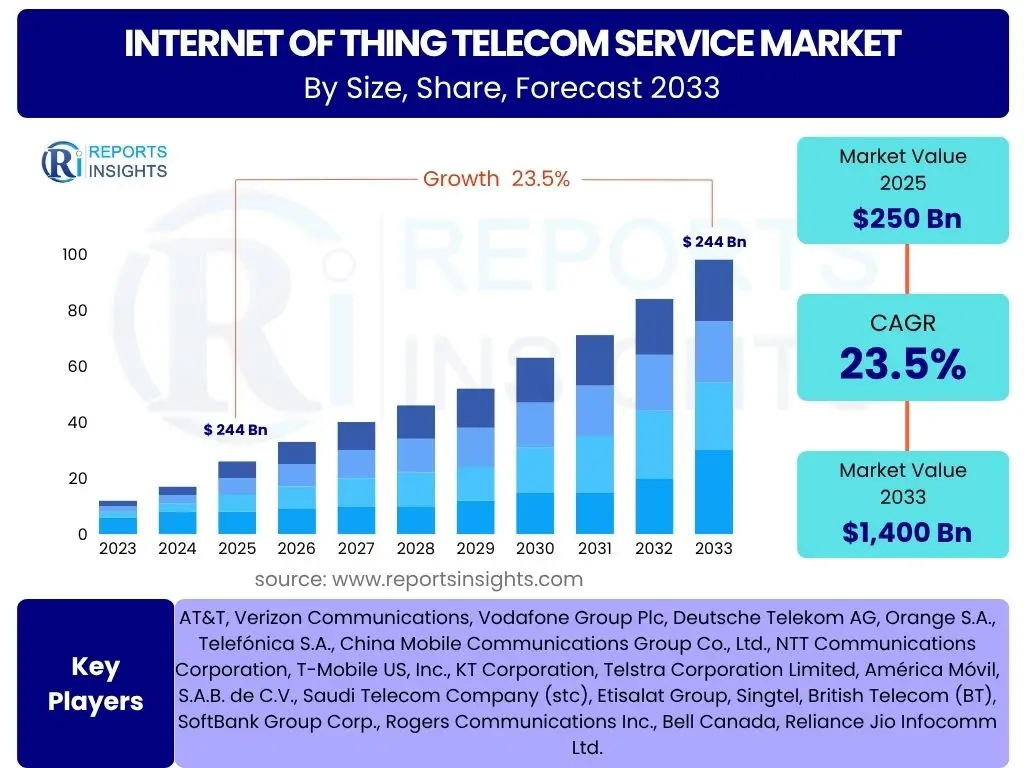

According to Reports Insights Consulting Pvt Ltd, The Internet of Thing Telecom Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033. The market is estimated at USD 250 billion in 2025 and is projected to reach USD 1,400 billion by the end of the forecast period in 2033.

This robust growth trajectory reflects the accelerating adoption of connected devices across various industries and consumer segments. The increasing demand for seamless connectivity, advanced data processing, and real-time insights from a multitude of IoT endpoints is a primary catalyst for this expansion. Furthermore, the continuous development and deployment of next-generation cellular technologies, such as 5G and various low-power wide-area network (LPWAN) solutions, are significantly enhancing the capabilities and scope of IoT applications, driving market value upwards.

The market's expansion is further fueled by the pervasive digitalization initiatives across global economies. Governments and private enterprises alike are investing heavily in smart infrastructure, industrial automation, and enhanced service delivery models that critically rely on robust IoT telecom services. This pervasive integration positions the Internet of Things as a foundational technology for future economic development and efficiency gains, making its associated telecom services an indispensable component of modern digital ecosystems.

Key Internet of Thing Telecom Service Market Trends & Insights

The Internet of Thing Telecom Service market is experiencing transformative shifts driven by technological advancements and evolving enterprise requirements. Analysis of prevalent market inquiries reveals a strong focus on the integration of cutting-edge connectivity options, the expansion of IoT applications into new industry verticals, and the demand for more sophisticated service management platforms. Stakeholders are particularly interested in how current trends will influence deployment scalability, data security, and overall return on investment for IoT initiatives. The shift towards edge computing and the emphasis on sustainable IoT solutions are also emerging as significant areas of interest, reflecting a broader industry push for efficiency and environmental responsibility.

A notable trend involves the deepening convergence of operational technology (OT) and information technology (IT) networks, facilitated by IoT telecom services. This convergence enables comprehensive data collection and analysis from industrial environments, leading to enhanced predictive maintenance, optimized resource allocation, and improved safety protocols. Another critical insight is the increasing complexity of IoT deployments, which necessitates robust, flexible, and secure network infrastructure, prompting telecom operators to offer more integrated, end-to-end solutions rather than just basic connectivity. This comprehensive approach is vital for addressing the diverse needs of various industries, from manufacturing to healthcare, ensuring reliable and efficient data transmission.

Furthermore, the market is witnessing an accelerated adoption of private 5G networks and hybrid cloud architectures to support latency-sensitive and data-intensive IoT applications. Enterprises are seeking greater control over their network environments, desiring dedicated bandwidth and enhanced security features for critical operations. This trend underscores a move beyond generic public network offerings towards tailored, high-performance solutions that can meet specific industry demands. The emphasis on data monetization and value-added services built on top of basic connectivity is also gaining traction, transforming telecom providers into strategic partners capable of delivering actionable insights from IoT data.

- Deployment of 5G and LPWAN technologies for enhanced connectivity and coverage.

- Increased adoption of edge computing to process data closer to the source, reducing latency.

- Growing demand for private IoT networks to ensure security and dedicated performance.

- Expansion of IoT applications in healthcare, manufacturing, and smart city initiatives.

- Emphasis on end-to-end managed IoT services for simplified deployment and operations.

- Rising focus on data analytics and AI-driven insights derived from IoT data.

- Development of sustainable and energy-efficient IoT solutions.

AI Impact Analysis on Internet of Thing Telecom Service

Analysis of common user questions related to the impact of AI on Internet of Thing Telecom Service reveals a high degree of interest in how artificial intelligence can optimize network performance, enhance data security, and enable advanced analytics. Users frequently inquire about AI's role in automating complex operations, predicting maintenance needs for network infrastructure, and personalizing service delivery. There is also significant curiosity regarding AI's potential to manage the massive influx of data generated by IoT devices, converting raw data into actionable insights for various applications. Concerns often revolve around the ethical implications of AI, data privacy, and the need for explainable AI models in critical IoT deployments, highlighting a desire for responsible innovation.

Artificial intelligence is profoundly transforming the operational landscape of IoT telecom services by enabling predictive analytics and proactive network management. AI algorithms can analyze vast datasets from network traffic, device behavior, and environmental conditions to identify anomalies, predict potential failures, and optimize resource allocation in real-time. This capability significantly enhances network reliability, reduces downtime, and improves overall service quality for diverse IoT applications. Moreover, AI-driven automation streamlines the provisioning, configuration, and monitoring of IoT devices and connections, leading to operational efficiencies and reduced manual intervention, which is crucial for managing large-scale deployments.

Beyond operational optimization, AI plays a pivotal role in strengthening the security posture of IoT telecom services. By employing machine learning models, AI can detect sophisticated cyber threats, identify unusual patterns of behavior indicative of attacks, and respond autonomously to mitigate risks. This proactive security framework is essential for protecting sensitive IoT data and ensuring the integrity of connected systems. Furthermore, AI facilitates the extraction of deeper insights from IoT data, enabling telecom service providers to offer value-added services such as personalized analytics, demand forecasting, and intelligent decision support for their enterprise customers, thereby expanding revenue streams and fostering innovation in various industries.

- Enhanced network optimization and intelligent traffic management through AI algorithms.

- Predictive maintenance for telecom infrastructure, minimizing downtime and operational costs.

- Advanced anomaly detection and real-time threat intelligence for robust IoT security.

- Automated provisioning and orchestration of IoT devices and services.

- Deep data analytics and insight generation from massive IoT datasets.

- Personalized service offerings and adaptive pricing models based on AI-driven insights.

- Improved resource allocation and energy efficiency in IoT network operations.

Key Takeaways Internet of Thing Telecom Service Market Size & Forecast

Analysis of common user questions about key takeaways from the Internet of Thing Telecom Service market size and forecast consistently highlights the market's significant growth potential and its pivotal role in enabling the digital transformation across industries. Users are keenly interested in understanding the primary drivers behind this expansion, particularly the impact of 5G rollout and the proliferation of IoT devices. There is also a strong desire for clarity on the most promising vertical applications and regions that are expected to contribute substantially to the market's valuation. The insights sought often revolve around strategic planning, investment opportunities, and competitive landscape shifts driven by the market's upward trajectory.

A primary takeaway is the market's robust and sustained growth, projected to reach substantial valuations by 2033, underpinning the critical importance of reliable and scalable connectivity for the evolving digital economy. This growth is not merely a consequence of increasing device numbers but also reflects the rising complexity and value of IoT applications that demand high-performance, low-latency, and secure communication infrastructures. The ongoing global rollout of advanced cellular technologies, particularly 5G, is a fundamental enabler, promising to unlock new possibilities for real-time applications and massive IoT deployments, further solidifying the market's expansion.

Furthermore, the market's future success is intricately linked to the ability of telecom service providers to offer comprehensive, integrated solutions that extend beyond basic connectivity. This includes managed services, platform capabilities, and robust security frameworks that address the end-to-end needs of diverse industries. The focus is shifting towards value creation through data monetization and enabling specific business outcomes for enterprises. Geographically, while mature markets continue to innovate, emerging economies are expected to exhibit accelerated adoption rates, driven by industrialization and urbanization initiatives. This global demand for interconnected ecosystems will continue to fuel the Internet of Thing Telecom Service market's upward trajectory, making it a cornerstone of digital infrastructure.

- The market is on an aggressive growth trajectory, driven by increasing IoT device penetration and digitalization across sectors.

- 5G technology is a cornerstone enabler, facilitating high-bandwidth, low-latency, and massive IoT connections.

- Enterprise adoption, particularly within industrial IoT (IIoT) and smart cities, represents a significant growth segment.

- The emphasis is shifting from pure connectivity to comprehensive, managed IoT service platforms that include analytics and security.

- Emerging economies are poised for rapid adoption, complementing sustained growth in developed regions.

Internet of Thing Telecom Service Market Drivers Analysis

The Internet of Thing Telecom Service market is propelled by a confluence of powerful drivers that collectively enhance the demand for connected solutions across diverse sectors. These drivers encompass technological advancements, evolving industry needs, and supportive regulatory frameworks, all contributing to the widespread adoption of IoT. The proliferation of smart devices, coupled with the increasing need for real-time data and automated processes, forms the bedrock of this market's expansion. Furthermore, the strategic investments made by enterprises in digital transformation initiatives inherently necessitate robust IoT telecom infrastructure to realize their objectives, pushing the market forward significantly.

A key driver is the continuous rollout and expansion of 5G network infrastructure globally. 5G offers unprecedented speeds, ultra-low latency, and the capacity for massive machine-type communications, making it ideal for a new generation of IoT applications that were previously impractical. This includes critical communications for autonomous vehicles, remote surgery, and advanced industrial automation, all requiring reliable, high-performance connectivity. Complementing 5G, the development and deployment of specialized Low-Power Wide-Area Network (LPWAN) technologies like NB-IoT and LTE-M are also critical drivers, enabling cost-effective and energy-efficient connectivity for a vast array of devices with simpler communication needs, thereby broadening the scope of IoT adoption.

Moreover, the increasing demand for operational efficiency and data-driven decision-making across various industries is fueling the adoption of IoT telecom services. Industries such as manufacturing, healthcare, automotive, and logistics are leveraging IoT solutions to monitor assets, track inventory, optimize supply chains, and enhance customer experiences. Government initiatives promoting smart cities, sustainable infrastructure, and digital public services further accelerate market growth by creating large-scale opportunities for IoT deployments. The competitive landscape among telecom operators to offer comprehensive IoT portfolios, including connectivity, platforms, and managed services, also acts as a significant driver, fostering innovation and making IoT solutions more accessible and appealing to a wider range of customers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Connected Devices | +5.2% | Global | Long-term (5+ years) |

| Global 5G Network Rollout | +4.8% | North America, Europe, APAC | Mid-term (3-5 years) |

| Increased Demand for Real-time Data & Analytics | +4.5% | Global | Long-term (5+ years) |

| Government Initiatives for Smart Cities & Infrastructure | +3.9% | APAC, Europe, Middle East | Mid-term (3-5 years) |

| Growth of Industrial IoT (IIoT) | +3.5% | North America, Europe, APAC | Long-term (5+ years) |

Internet of Thing Telecom Service Market Restraints Analysis

Despite its significant growth potential, the Internet of Thing Telecom Service market faces several restraints that could impede its acceleration. These challenges often revolve around the complexities inherent in deploying and managing large-scale, interconnected systems, alongside concerns regarding data integrity and security. Addressing these fundamental issues is crucial for market participants to unlock the full potential of IoT services and maintain user trust. Without effective mitigation strategies, these restraints could lead to slower adoption rates in certain segments or regions, impacting overall market development.

One prominent restraint is the high initial investment required for deploying robust IoT infrastructure, including network upgrades, device procurement, and platform integration. This capital outlay can be a significant barrier for smaller enterprises or those with limited budgets, slowing down their adoption of comprehensive IoT solutions. Additionally, the fragmented regulatory landscape across different regions and countries poses a considerable challenge. Varying data privacy laws, spectrum allocation rules, and industry-specific regulations necessitate complex compliance efforts, increasing operational costs and potentially delaying cross-border deployments. The absence of universal standards for IoT devices and communication protocols further exacerbates interoperability issues, leading to vendor lock-in and complicating the seamless integration of diverse IoT ecosystems.

Furthermore, data security and privacy concerns remain a critical restraint. The sheer volume and sensitivity of data transmitted by IoT devices make them attractive targets for cyberattacks. Breaches can lead to significant financial losses, reputational damage, and loss of consumer trust. Ensuring robust end-to-end security, from the device to the cloud, across diverse networks and applications, is a complex undertaking that requires continuous investment and expertise. Moreover, the lack of skilled professionals capable of designing, deploying, and managing complex IoT telecom solutions also acts as a bottleneck, hindering the efficient scaling of services. Addressing these multifaceted challenges through standardization, robust security measures, and workforce development is essential for sustained market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Deployment Costs | -3.8% | Global | Mid-term (3-5 years) |

| Data Security & Privacy Concerns | -3.5% | Global | Long-term (5+ years) |

| Lack of Standardization & Interoperability Issues | -3.2% | Global | Mid-term (3-5 years) |

| Regulatory Complexities & Compliance | -2.9% | Europe, North America, APAC | Long-term (5+ years) |

| Shortage of Skilled Professionals | -2.5% | Global | Long-term (5+ years) |

Internet of Thing Telecom Service Market Opportunities Analysis

The Internet of Thing Telecom Service market is rich with opportunities, driven by technological evolution, untapped market segments, and the potential for innovative service offerings. These opportunities are not only expanding the market's reach but also fostering new business models and collaborations across industries. Capitalizing on these emerging areas will be critical for telecom operators and IoT service providers seeking to establish competitive advantages and achieve sustainable growth.

One significant opportunity lies in the burgeoning adoption of edge computing capabilities in conjunction with IoT deployments. By processing data closer to the source, edge computing reduces latency, conserves bandwidth, and enhances data security, making it ideal for real-time and mission-critical IoT applications in sectors like manufacturing, healthcare, and autonomous vehicles. Telecom providers are uniquely positioned to offer edge infrastructure as a service, leveraging their existing network footprint to deploy localized computing resources. Another key area of growth is the expansion into new vertical markets that are increasingly recognizing the value of IoT. This includes precision agriculture, smart logistics, remote patient monitoring in healthcare, and environmental monitoring, each presenting unique demands for connectivity and data services that telecom operators can fulfill with tailored solutions. The development of new low-power IoT technologies, such as NB-IoT and LTE-M, also presents an opportunity by enabling widespread, cost-effective connectivity for a vast array of devices previously uneconomical to connect, opening up massive scale deployments.

Furthermore, the shift towards a service-oriented economy creates substantial opportunities for telecom companies to move beyond basic connectivity and offer comprehensive managed IoT services. This includes device management, data analytics platforms, application enablement, and end-to-end security solutions. By providing a full suite of services, providers can simplify IoT adoption for enterprises, reduce complexity, and unlock higher revenue streams through recurring subscriptions and value-added offerings. Strategic partnerships and collaborations between telecom operators, cloud providers, and specialized IoT solution developers also represent a significant opportunity. These alliances can foster innovation, accelerate market penetration, and enable the delivery of integrated, high-value solutions that meet complex customer needs, driving mutual growth and expanding the overall IoT ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Edge Computing & AI Integration | +4.9% | Global | Mid-term (3-5 years) |

| Expansion into New Vertical Markets (e.g., Agriculture, Healthcare) | +4.6% | Global, Emerging Markets | Long-term (5+ years) |

| Development of Managed IoT Service Platforms | +4.2% | Global | Mid-term (3-5 years) |

| Growth of Private Networks (5G and LPWAN) | +3.7% | North America, Europe, APAC | Long-term (5+ years) |

| Strategic Partnerships & Ecosystem Collaborations | +3.5% | Global | Long-term (5+ years) |

Internet of Thing Telecom Service Market Challenges Impact Analysis

While the Internet of Thing Telecom Service market offers immense potential, it is not without its significant challenges that require strategic navigation. These obstacles can impact deployment scalability, cost-effectiveness, and the overall reliability of IoT solutions. Addressing these issues effectively is crucial for sustained growth and for instilling confidence among end-users and enterprises.

One of the primary challenges facing the IoT telecom service market is the complexity of managing a vast and diverse ecosystem of devices, protocols, and platforms. Ensuring seamless interoperability between various hardware, software, and connectivity standards from different vendors remains a considerable hurdle, often leading to fragmented deployments and integration complexities. This fragmentation can increase development time and costs, deterring widespread adoption, especially for organizations without specialized technical expertise. Furthermore, maintaining consistent Quality of Service (QoS) across a multitude of IoT applications, each with unique latency, bandwidth, and reliability requirements, poses significant technical and operational difficulties for network operators. This is particularly challenging in dynamic environments where network conditions can fluctuate rapidly.

Another critical challenge is related to spectrum availability and efficient spectrum management. As the number of connected devices proliferates, the demand for spectrum increases, leading to potential congestion and interference issues, particularly in densely populated areas. Regulatory bodies and telecom operators must continuously work to allocate and manage spectrum effectively to accommodate the growing needs of IoT while ensuring fair access and preventing degradation of service. Moreover, the energy efficiency and battery life limitations of many IoT devices present a practical challenge, especially for remote deployments or applications requiring long operational periods without human intervention. While LPWAN technologies offer solutions, ongoing innovation in power management and sustainable energy sources is vital to extend device longevity and reduce maintenance overheads, which can otherwise impede the scalability and economic viability of large-scale IoT deployments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Ecosystem & Interoperability | -4.1% | Global | Long-term (5+ years) |

| Maintaining Quality of Service (QoS) | -3.7% | Global | Mid-term (3-5 years) |

| Spectrum Availability & Management | -3.4% | Global | Long-term (5+ years) |

| Battery Life & Power Consumption of Devices | -3.0% | Global | Mid-term (3-5 years) |

| Regulatory and Legal Uncertainties | -2.8% | Europe, North America | Long-term (5+ years) |

Internet of Thing Telecom Service Market - Updated Report Scope

This market insights report provides a comprehensive analysis of the Internet of Thing Telecom Service market, encompassing historical data, current market dynamics, and future growth projections. The scope includes detailed segmentation analysis by connectivity type, service type, application, and end-use industry, offering granular insights into market opportunities and challenges across various segments. The report further covers regional market performances, identifying key growth hubs and their unique contributing factors, along with an extensive profiling of leading market participants and their strategic initiatives. It serves as a vital resource for stakeholders seeking to understand market trends, competitive landscape, and investment potential within the global IoT telecom sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 250 Billion |

| Market Forecast in 2033 | USD 1,400 Billion |

| Growth Rate | 23.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AT&T, Verizon Communications, Vodafone Group Plc, Deutsche Telekom AG, Orange S.A., Telefónica S.A., China Mobile Communications Group Co., Ltd., NTT Communications Corporation, T-Mobile US, Inc., KT Corporation, Telstra Corporation Limited, América Móvil, S.A.B. de C.V., Saudi Telecom Company (stc), Etisalat Group, Singtel, British Telecom (BT), SoftBank Group Corp., Rogers Communications Inc., Bell Canada, Reliance Jio Infocomm Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Internet of Thing Telecom Service market is broadly segmented to provide a granular understanding of its dynamics and opportunities. These segmentations are critical for identifying key growth areas, understanding diverse customer needs, and tailoring solutions for specific applications and industries. The market's structure reflects the variety of technological requirements and deployment scenarios characteristic of the vast IoT ecosystem, enabling a precise analysis of its intricate components.

Each segment within the market showcases unique characteristics and growth drivers. For instance, the 'By Connectivity' segment highlights the evolving landscape of network technologies, from high-bandwidth 5G for mission-critical applications to energy-efficient LPWANs for extensive sensor deployments. This diversity underscores the need for telecom providers to offer a comprehensive portfolio of connectivity options that can cater to varying device capabilities and application demands. Similarly, the 'By Service Type' segment differentiates the value-added services offered beyond basic data transmission, such as connectivity management, professional consulting, and robust security solutions, illustrating the shift towards more integrated and managed service models.

The 'By Application' and 'By End-Use Industry' segments further illuminate the diverse scenarios where IoT telecom services are being leveraged, from enhancing efficiency in industrial settings to improving public safety in smart cities. Understanding these application-specific requirements is paramount for market players to develop targeted products and services that deliver tangible benefits to end-users. This detailed segmentation analysis not only offers a clear picture of the market's current state but also provides a strategic roadmap for future innovation and market penetration across various sectors and use cases, ensuring that service offerings align with industry-specific needs and technological advancements.

- By Connectivity: Cellular (5G, LTE-M, NB-IoT), Satellite, LPWAN (LoRaWAN, Sigfox), Wi-Fi, Bluetooth.

- By Service Type: Connectivity Management, Professional Services, Platform Management, Security Services.

- By Application: Smart Homes, Smart Cities, Connected Cars, Industrial IoT, Healthcare, Agriculture.

- By End-Use Industry: Manufacturing, Automotive, Healthcare, Retail, Energy & Utilities, Government, Agriculture.

Regional Highlights

- North America: Leading region in terms of early adoption and technological innovation, particularly in smart cities, connected cars, and industrial IoT. Strong presence of key market players and robust R&D investments.

- Europe: Characterized by strong regulatory frameworks concerning data privacy and security, fostering trust in IoT deployments. Significant growth in smart manufacturing and sustainable energy management applications.

- Asia Pacific (APAC): The fastest-growing region, driven by rapid urbanization, extensive industrialization, and substantial government investments in digital infrastructure and smart initiatives, especially in China, India, and Japan.

- Latin America: Emerging market with increasing adoption of IoT in agriculture, logistics, and smart utilities, propelled by improving connectivity infrastructure and digital transformation efforts.

- Middle East and Africa (MEA): Demonstrating considerable potential, particularly in smart oil and gas, smart city developments (e.g., NEOM in Saudi Arabia), and leveraging IoT for diversified economies and sustainable resource management.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Internet of Thing Telecom Service Market.- AT&T

- Verizon Communications

- Vodafone Group Plc

- Deutsche Telekom AG

- Orange S.A.

- Telefónica S.A.

- China Mobile Communications Group Co., Ltd.

- NTT Communications Corporation

- T-Mobile US, Inc.

- KT Corporation

- Telstra Corporation Limited

- América Móvil, S.A.B. de C.V.

- Saudi Telecom Company (stc)

- Etisalat Group

- Singtel

- British Telecom (BT)

- SoftBank Group Corp.

- Rogers Communications Inc.

- Bell Canada

- Reliance Jio Infocomm Ltd.

Frequently Asked Questions

What is Internet of Thing Telecom Service?

Internet of Thing Telecom Service refers to the comprehensive suite of connectivity, platform, and managed services provided by telecommunication companies to enable and support the operation of IoT devices and applications. This includes providing the network infrastructure for device communication, data routing, device management, and offering value-added services like security, data analytics, and application enablement, essential for seamless IoT ecosystems.

What are the primary benefits of IoT telecom services for businesses?

Businesses leveraging IoT telecom services gain several critical benefits, including enhanced operational efficiency through real-time monitoring and automation, improved decision-making driven by data insights, increased asset utilization, and the ability to create new revenue streams through innovative connected products and services. These services also contribute to better customer experiences and significant cost reductions.

How does 5G impact the Internet of Thing Telecom Service market?

5G significantly impacts the IoT telecom service market by offering ultra-high bandwidth, extremely low latency, and the capacity to support massive numbers of connected devices. These capabilities enable new, advanced IoT applications such as autonomous vehicles, augmented reality for industrial uses, and real-time remote healthcare, thereby expanding the market's potential and accelerating its growth.

What are the main challenges in deploying Internet of Thing Telecom Services?

Key challenges in deploying Internet of Thing Telecom Services include ensuring robust data security and privacy, managing the complexity of diverse IoT ecosystems and interoperability issues, addressing the high initial investment costs, navigating fragmented regulatory landscapes, and mitigating battery life limitations of various IoT devices.

Which industries are major adopters of Internet of Thing Telecom Services?

Major industry adopters of Internet of Thing Telecom Services include manufacturing (Industrial IoT for asset tracking and predictive maintenance), automotive (connected cars and telematics), healthcare (remote patient monitoring and smart hospitals), smart cities (traffic management, public safety), retail (inventory management, personalized shopping), and energy & utilities (smart grids, smart metering).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted