Processor Market

Processor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702080 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Processor Market Size

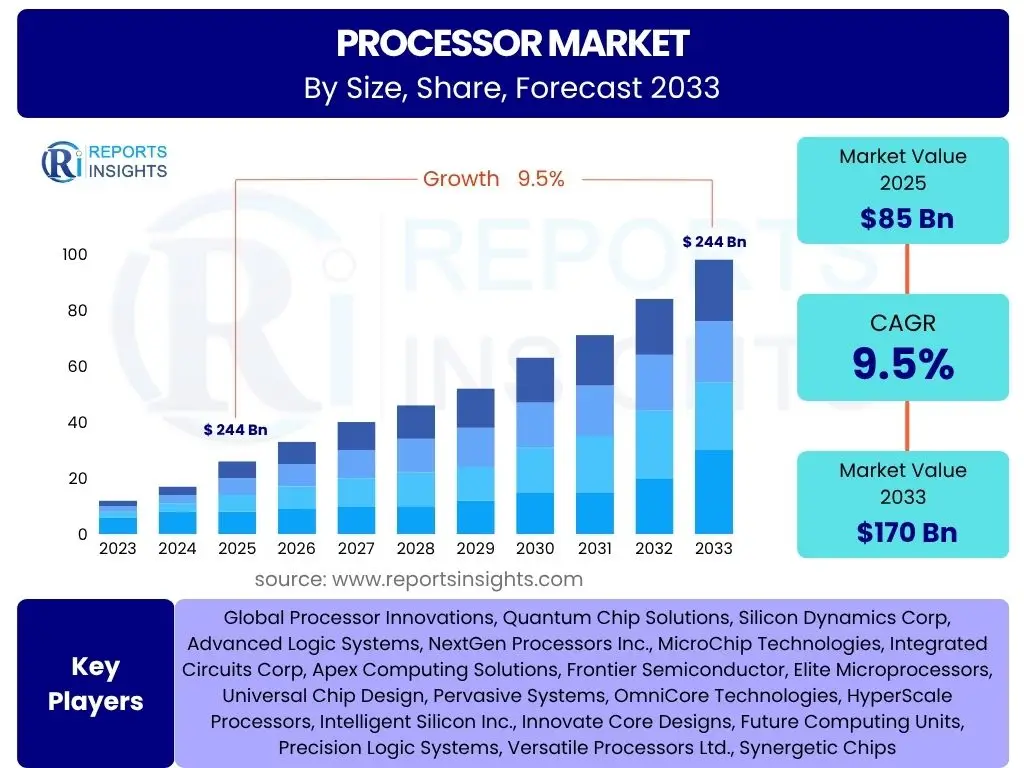

According to Reports Insights Consulting Pvt Ltd, The Processor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 85 Billion in 2025 and is projected to reach USD 170 Billion by the end of the forecast period in 2033.

Key Processor Market Trends & Insights

The Processor market is undergoing a significant transformation, driven by the escalating demand for advanced computing capabilities across various industries. Common user inquiries often focus on understanding the primary technological shifts, the increasing specialization of processing units, and the evolving design paradigms that dictate performance and efficiency. Key trends indicate a clear move towards heterogenous computing architectures, where specialized processors are integrated to handle specific workloads, moving beyond the traditional reliance on general-purpose CPUs.

Furthermore, the market is observing a strong emphasis on miniaturization and power efficiency, crucial for the proliferation of edge computing and IoT devices. Users are keenly interested in how these trends will impact device autonomy, battery life, and overall system responsiveness. The rise of open-source processor architectures, such as RISC-V, also represents a notable trend, democratizing chip design and fostering innovation by lowering barriers to entry. These developments are collectively shaping the next generation of computing infrastructure, from hyperscale data centers to ultra-low-power wearables.

- Increased specialization of processors (e.g., NPUs for AI, DPUs for data processing, VPUs for vision tasks)

- Prevalence of chiplet and modular design architectures for enhanced scalability and customizability

- Growing integration of edge AI and on-device inferencing capabilities for real-time processing

- Persistent focus on ultra-low power consumption and energy-efficient designs across all processor types

- Accelerated adoption of open-source instruction set architectures (ISAs) like RISC-V

- Enhancement of hardware-level security features and trusted execution environments

- Development of neuromorphic and quantum computing processors for specialized applications

AI Impact Analysis on Processor

Artificial Intelligence (AI) is profoundly reshaping the processor market, driving an unprecedented demand for specialized and high-performance computing hardware. Users frequently ask how AI applications are influencing chip design, what types of processors are best suited for AI workloads, and whether traditional CPUs will remain relevant in an AI-centric world. The consensus indicates that AI is not replacing general-purpose processors but rather necessitating their augmentation with purpose-built accelerators. This has led to the proliferation of Neural Processing Units (NPUs), powerful Graphics Processing Units (GPUs), and custom ASICs specifically designed to handle the intensive computational demands of machine learning training and inference.

The impact of AI extends beyond just computational power; it is also influencing processor architecture, memory hierarchies, and interconnect technologies to optimize data flow and reduce latency. Concerns revolve around the energy consumption of AI workloads and the need for more efficient AI hardware, especially for edge deployment where power and thermal budgets are constrained. The market is responding with innovative designs that balance raw computational throughput with power efficiency, often employing heterogeneous computing models where CPUs, GPUs, and NPUs work in tandem. This transformative shift underscores AI's role as a primary catalyst for innovation and growth within the processor industry, driving advancements that benefit a wide array of applications from autonomous systems to sophisticated data analytics.

- Proliferation of dedicated Neural Processing Units (NPUs) and AI accelerators on-chip.

- Significant increase in demand for high-performance Graphics Processing Units (GPUs) for AI training.

- Shift towards heterogeneous computing architectures integrating CPUs, GPUs, and specialized AI cores.

- Optimization of processors for efficient AI inference at the edge, reducing reliance on cloud connectivity.

- Development of new memory technologies (e.g., HBM) to support high-bandwidth AI workloads.

- Emergence of AI-driven tools and methodologies for processor design and verification.

- Increased focus on energy efficiency for AI computations, particularly in mobile and embedded systems.

Key Takeaways Processor Market Size & Forecast

The Processor market is poised for robust and sustained growth, driven by fundamental shifts in computing paradigms and pervasive digital transformation initiatives. Common user questions often revolve around understanding the core implications of the market forecast: where will the most significant growth occur, what technological advancements will be paramount, and how will geopolitical and economic factors influence this trajectory? The key takeaway is a market characterized by continuous innovation, where the demand for higher performance, greater efficiency, and specialized capabilities is unrelenting across all sectors. The forecast indicates that AI and IoT will serve as primary engines for this growth, necessitating more powerful and diverse processing solutions.

Furthermore, the market's future will be heavily influenced by strategic investments in advanced manufacturing technologies and research and development into novel architectures. The ability of manufacturers to navigate supply chain complexities and geopolitical trade policies will also be critical. Ultimately, the market is moving towards a highly integrated and intelligent ecosystem where processors are not merely computational units but foundational components enabling pervasive connectivity, autonomous systems, and advanced data processing at every scale, from the cloud to the extreme edge. This necessitates a strategic focus on resilient supply chains and diversified manufacturing capabilities.

- The Processor market demonstrates a strong and consistent growth trajectory, propelled by escalating demand across diverse industries.

- Artificial Intelligence (AI) and the Internet of Things (IoT) are identified as the primary catalysts for market expansion.

- Significant investments in research and development for next-generation processor architectures, including chiplets and custom ASICs, are paramount.

- New market niches are emerging rapidly, particularly in automotive AI, industrial automation, and specialized healthcare devices.

- Geopolitical influences and the imperative for resilient supply chains are increasingly shaping manufacturing and procurement strategies.

- Energy efficiency and sustainable design practices are becoming critical differentiators in processor development.

Processor Market Drivers Analysis

The Processor market's growth is fundamentally propelled by several interconnected factors that create sustained demand for advanced computing capabilities. The ubiquitous expansion of digital technologies, coupled with the increasing complexity of data, necessitates more powerful, efficient, and specialized processing units. These drivers collectively foster an environment of continuous innovation and investment in semiconductor research and development, pushing the boundaries of what processors can achieve. The convergence of these drivers is not only expanding existing market segments but also creating entirely new application areas, from smart infrastructure to immersive digital experiences.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for Artificial Intelligence (AI) and Machine Learning (ML) applications | +2.5% | Global, particularly North America, APAC | Short to Mid-term (2025-2030) |

| Proliferation of Internet of Things (IoT) and Edge Computing devices | +1.8% | North America, APAC, Europe | Mid-term (2027-2033) |

| Expansion of Data Centers and Cloud Infrastructure worldwide | +2.0% | Global | Long-term (2025-2033) |

| Advancements in 5G technology and increased connectivity | +1.2% | APAC, Europe, North America | Short to Mid-term (2025-2030) |

| Increasing adoption of autonomous vehicles and advanced driver-assistance systems (ADAS) | +0.8% | Europe, North America, APAC | Long-term (2028-2033) |

Processor Market Restraints Analysis

Despite the robust growth projections, the Processor market faces several significant restraints that could impede its expansion. These challenges often stem from the inherent complexities of semiconductor manufacturing, geopolitical dynamics, and the high-stakes competitive landscape. Addressing these restraints requires substantial strategic planning, investment in R&D, and international collaboration to ensure a stable and sustainable growth trajectory. The cumulative effect of these factors necessitates continuous adaptation and innovation from market participants to mitigate potential negative impacts on supply, cost, and technological progress.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global supply chain disruptions and geopolitical tensions impacting manufacturing | -1.5% | Global | Short-term (2025-2027) |

| Exorbitant Research & Development (R&D) costs and increasing complexity of chip design | -1.0% | Global | Long-term (2025-2033) |

| Intense market competition leading to pricing pressures and margin erosion | -0.7% | APAC, North America | Short to Mid-term (2025-2030) |

| Growing environmental concerns related to energy consumption and e-waste | -0.5% | Europe, North America | Long-term (2028-2033) |

| Shortage of skilled talent and specialized workforce in the semiconductor industry | -0.3% | Global | Mid-term (2027-2032) |

Processor Market Opportunities Analysis

The Processor market is rich with emerging opportunities that can unlock new growth avenues and drive significant innovation. These opportunities arise from technological breakthroughs, unmet market needs, and evolving industrial requirements. Capitalizing on these prospects requires strategic foresight, agile product development, and strong partnerships across the value chain. The ability to innovate and adapt to these nascent demands will be crucial for companies seeking to gain a competitive edge and expand their market footprint in the coming years, particularly in specialized and high-value segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of quantum computing processors and related infrastructure | +1.0% | Global, particularly North America, Europe | Long-term (2030-2033) |

| Development of specialized processors for healthcare, bioinformatics, and medical devices | +0.9% | North America, Europe, APAC | Mid to Long-term (2027-2033) |

| Expansion into new edge device categories and niche IoT applications (e.g., smart agriculture) | +1.5% | APAC, Latin America, Africa | Short to Mid-term (2025-2030) |

| Focus on sustainable and energy-efficient chip designs to meet green computing demands | +0.8% | Europe, Global | Mid-term (2026-2031) |

| Growing demand for customizable and domain-specific architectures (DSAs) for specific workloads | +1.2% | North America, Global | Long-term (2028-2033) |

Processor Market Challenges Impact Analysis

The Processor market faces an array of complex challenges that demand continuous innovation and strategic responses from manufacturers and stakeholders. These challenges range from fundamental physics limitations to rapidly evolving cybersecurity threats and the imperative to balance performance with power efficiency. Overcoming these hurdles is essential for maintaining growth momentum and delivering next-generation computing solutions. The dynamic nature of technological advancement and global market forces means that these challenges are continuously evolving, requiring constant vigilance and adaptability within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Approaching physical limits of silicon miniaturization and lithography advancements | -1.3% | Global | Long-term (2028-2033) |

| Increasing cybersecurity threats and the need for robust hardware-level security | -1.0% | Global | Short to Mid-term (2025-2030) |

| Balancing escalating performance demands with stringent power efficiency requirements | -0.8% | Global | Mid-term (2026-2031) |

| Fragmented regulatory landscape and complex international trade policies | -0.6% | Global | Short-term (2025-2027) |

| Rapid technological obsolescence and short product lifecycles | -0.4% | Global | Short to Mid-term (2025-2030) |

Processor Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Processor market, providing an in-depth analysis of its current landscape, historical performance, and future projections. It covers critical market attributes, including size, growth rate, key trends, and a detailed segmentation breakdown. The report offers strategic insights into market drivers, restraints, opportunities, and challenges, providing a holistic view for stakeholders to make informed decisions. It also profiles leading market players and highlights regional market dynamics, offering a complete picture of the global processor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 85 Billion |

| Market Forecast in 2033 | USD 170 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Processor Innovations, Quantum Chip Solutions, Silicon Dynamics Corp, Advanced Logic Systems, NextGen Processors Inc., MicroChip Technologies, Integrated Circuits Corp, Apex Computing Solutions, Frontier Semiconductor, Elite Microprocessors, Universal Chip Design, Pervasive Systems, OmniCore Technologies, HyperScale Processors, Intelligent Silicon Inc., Innovate Core Designs, Future Computing Units, Precision Logic Systems, Versatile Processors Ltd., Synergetic Chips |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Processor market is extensively segmented to reflect the diverse range of processing units, architectural designs, and their varied applications across numerous industries and end-use devices. This granular segmentation provides a detailed understanding of market dynamics, identifying specific growth areas and competitive landscapes within each category. The breakdown by type, architecture, application, and end-use device illustrates the increasing specialization and differentiation within the processor ecosystem, catering to distinct performance, power, and cost requirements across the technological spectrum. Analyzing these segments is crucial for identifying targeted opportunities and understanding the evolving demands of specific market verticals.

- By Type:

- Central Processing Units (CPUs)

- Graphics Processing Units (GPUs)

- Neural Processing Units (NPUs)

- Digital Signal Processors (DSPs)

- Field-Programmable Gate Arrays (FPGAs)

- Systems on Chip (SoCs)

- Other Processors (e.g., Data Processing Units (DPUs), Custom Accelerators)

- By Architecture:

- x86 Architecture

- ARM Architecture

- RISC-V Architecture

- Other Architectures (e.g., MIPS, PowerPC)

- By Application:

- Consumer Electronics (Smartphones, PCs, Laptops, Tablets, Wearables, Gaming Consoles)

- Automotive (Infotainment Systems, Advanced Driver-Assistance Systems (ADAS), Autonomous Driving)

- Industrial (Industrial Automation, Robotics, Manufacturing, Smart Factory Solutions)

- Healthcare (Medical Imaging, Diagnostic Equipment, Wearable Health Devices, Life Sciences)

- Data Centers & Cloud Computing (Servers, Storage Systems, Networking Equipment)

- Telecommunications (5G Infrastructure, Network Routers, Base Stations)

- Aerospace & Defense

- Other Applications (e.g., Smart Home Devices, Retail & Logistics, Energy Management)

- By End-Use Device:

- Desktop & Laptops

- Mobile Devices (Smartphones, Tablets)

- Servers & Workstations

- Embedded Systems

- High-Performance Computing (HPC) Systems

Regional Highlights

- North America: This region stands as a powerhouse in processor innovation and demand, primarily driven by a robust ecosystem of technology giants, significant investments in AI and cloud computing, and early adoption of advanced semiconductor technologies. The presence of major research institutions and leading chip designers fuels continuous advancements, particularly in high-performance computing, data centers, and specialized AI processors. Stringent regulatory frameworks for data security also drive demand for secure hardware.

- Europe: Characterized by a strong focus on industrial automation, automotive electronics, and energy-efficient solutions, Europe is a key market for specialized processors. There is a growing emphasis on developing sustainable computing solutions and fostering the adoption of open-source architectures like RISC-V. Government initiatives aimed at strengthening domestic semiconductor manufacturing capabilities and investing in next-generation technologies like quantum computing are also notable.

- Asia Pacific (APAC): APAC holds the largest market share due to its vast consumer electronics manufacturing base, rapid industrialization, and booming digital infrastructure. Countries like China, South Korea, Japan, and Taiwan are at the forefront of semiconductor production and design. The widespread adoption of 5G technology, IoT devices, and cloud services further propels demand across the region. Government support for semiconductor self-sufficiency and substantial investments in R&D contribute significantly to market growth.

- Latin America: An emerging market, Latin America is experiencing increasing demand for processors driven by growing digital transformation across sectors, expanding internet penetration, and rising adoption of cloud services and mobile devices. Investments in smart city projects and improving telecommunications infrastructure contribute to the region's nascent but promising growth trajectory, particularly for consumer and embedded processors.

- Middle East and Africa (MEA): The MEA region is witnessing substantial investments in data center development, smart city initiatives, and diversified economies seeking to reduce reliance on traditional industries. This drives demand for high-performance processors for cloud services, AI applications, and IoT deployments. Government-led digital transformation agendas are key drivers for processor adoption across various sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Processor Market.- Global Processor Innovations

- Quantum Chip Solutions

- Silicon Dynamics Corp

- Advanced Logic Systems

- NextGen Processors Inc.

- MicroChip Technologies

- Integrated Circuits Corp

- Apex Computing Solutions

- Frontier Semiconductor

- Elite Microprocessors

- Universal Chip Design

- Pervasive Systems

- OmniCore Technologies

- HyperScale Processors

- Intelligent Silicon Inc.

- Innovate Core Designs

- Future Computing Units

- Precision Logic Systems

- Versatile Processors Ltd.

- Synergetic Chips

Frequently Asked Questions

What are the primary growth drivers for the processor market?

The processor market's growth is primarily driven by the escalating demand for Artificial Intelligence (AI) and Machine Learning (ML) applications, the widespread proliferation of IoT and edge computing devices, the continuous expansion of data centers and cloud infrastructure, and advancements in 5G technology. These factors collectively necessitate more powerful, efficient, and specialized processing capabilities across various industries and applications.

How is artificial intelligence transforming processor technology?

Artificial intelligence is fundamentally transforming processor technology by driving the development of specialized hardware like Neural Processing Units (NPUs) and high-performance Graphics Processing Units (GPUs). It promotes heterogeneous computing architectures where CPUs, GPUs, and NPUs work synergistically, and optimizes processors for efficient AI inference at the edge. AI also influences chip design and verification processes, leading to more intelligent and optimized silicon solutions.

What is the significance of chiplet architecture in modern processors?

Chiplet architecture is highly significant in modern processors as it allows complex processors to be built from smaller, modular components (chiplets) rather than a single monolithic die. This approach enhances manufacturing flexibility, improves yields, enables easier integration of diverse functionalities (e.g., CPU, GPU, memory controller, I/O), and facilitates customizability. It also helps overcome the physical limits of silicon miniaturization, leading to more powerful and cost-effective designs.

Which regions are dominating the processor market, and why?

The Asia Pacific (APAC) region currently dominates the processor market, largely due to its vast consumer electronics manufacturing capabilities, rapid industrialization, and significant investments in semiconductor production and digital infrastructure. North America is also a major player, driven by strong R&D, cloud computing, and AI innovation. Europe contributes through its focus on industrial automation and energy-efficient processor designs.

What challenges are impacting the growth of the processor industry?

The processor industry faces several challenges, including the increasing physical limits of silicon miniaturization, complex and costly R&D processes, global supply chain disruptions due to geopolitical tensions, and intense market competition leading to pricing pressures. Additionally, balancing escalating performance demands with stringent power efficiency requirements and addressing evolving cybersecurity threats pose significant hurdles for sustained growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted