Process Oil Market

Process Oil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706111 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

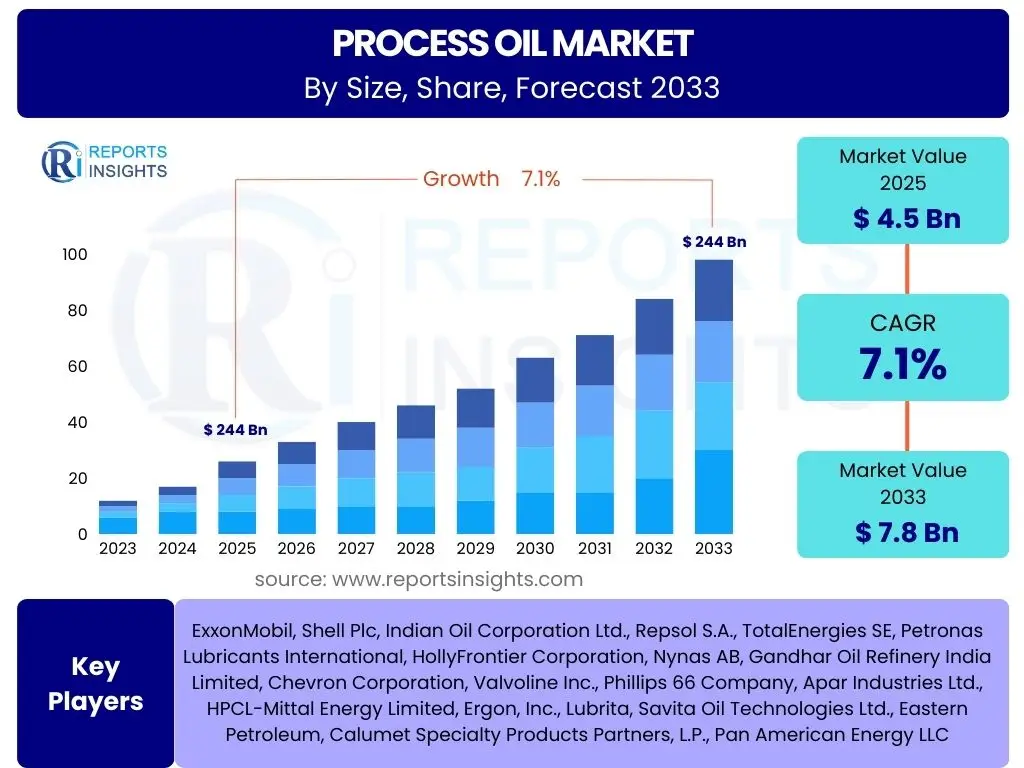

Process Oil Market Size

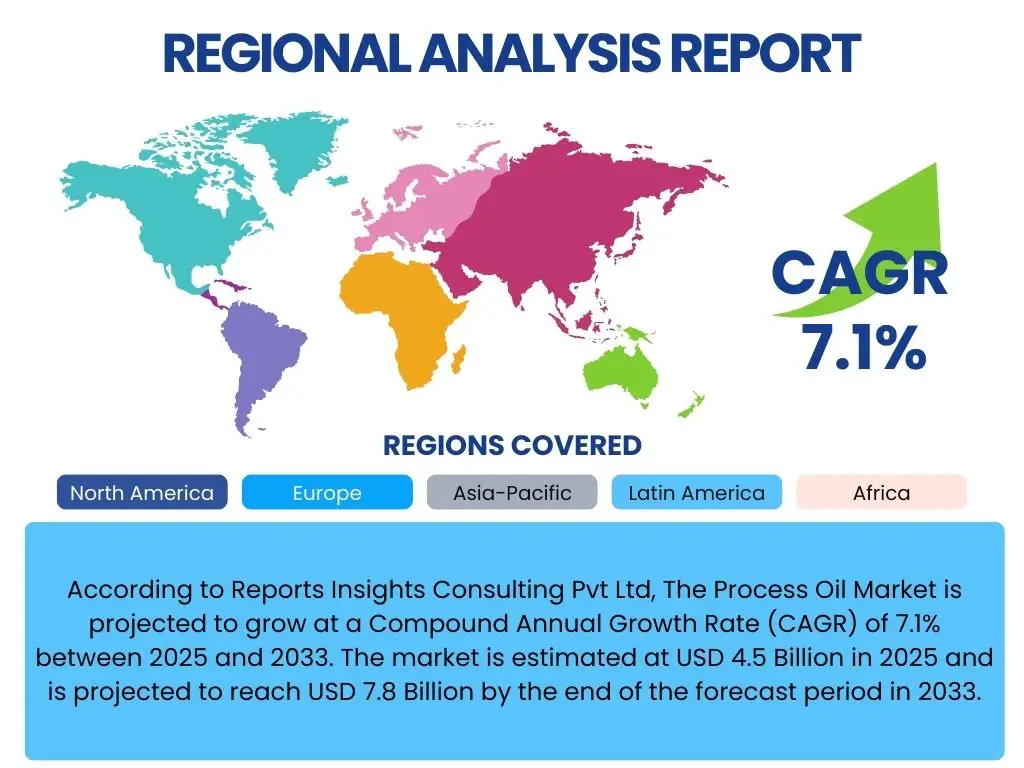

According to Reports Insights Consulting Pvt Ltd, The Process Oil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.1% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 7.8 Billion by the end of the forecast period in 2033.

Key Process Oil Market Trends & Insights

The Process Oil Market is undergoing significant transformations, driven by evolving industrial demands and stringent environmental regulations. Users frequently inquire about the forces shaping market dynamics, including the shift towards sustainable practices, the impact of advanced materials, and the expansion of key end-use industries. Insights reveal a strong emphasis on developing eco-friendly and high-performance process oils, alongside a growing demand from the automotive, construction, and manufacturing sectors. The market is also seeing increasing adoption of specialty oils for niche applications, reflecting a move towards customized solutions that offer improved efficiency and product longevity.

Technological advancements in the formulation of process oils are playing a crucial role, allowing manufacturers to meet specific performance requirements for various applications, such as tire manufacturing, plastics processing, and adhesive production. Furthermore, the global push for reduced carbon footprints and enhanced worker safety is compelling companies to invest in low-PAH (Polycyclic Aromatic Hydrocarbon) and bio-based alternatives. This regulatory pressure, coupled with consumer preferences for sustainable products, is fundamentally altering the product landscape and driving innovation.

- Growing demand for eco-friendly and bio-based process oils driven by environmental regulations.

- Increasing consumption from the automotive and tire manufacturing industries.

- Rising adoption of high-performance process oils for specialty applications.

- Technological advancements leading to improved oil formulations and properties.

- Expansion of industrial and manufacturing activities in emerging economies.

AI Impact Analysis on Process Oil

The integration of Artificial intelligence (AI) is emerging as a transformative force across various industries, and the Process Oil Market is no exception. Users are keen to understand how AI can enhance operational efficiency, optimize production processes, and contribute to the development of new products. Key themes frequently discussed include the application of predictive analytics for maintenance, AI-driven insights for raw material sourcing, and the use of machine learning in refining and blending processes to achieve precise oil specifications. There is a strong expectation that AI will lead to more intelligent factories and supply chains, reducing waste and improving overall productivity.

AI's influence extends to accelerating research and development, allowing for faster identification of optimal formulations and predicting material performance characteristics with greater accuracy. This can significantly shorten the time-to-market for innovative process oil products. Furthermore, AI-powered quality control systems can monitor production in real-time, detecting anomalies and ensuring consistent product quality, which is critical in sensitive applications. While the adoption is still in its nascent stages, the potential for AI to revolutionize various facets of the process oil value chain, from raw material procurement to distribution and customer service, is substantial.

- Optimized production processes through AI-driven predictive analytics for energy efficiency and yield.

- Enhanced supply chain management and logistics, including demand forecasting and inventory optimization.

- Improved quality control and consistency in process oil formulations using machine learning algorithms.

- Accelerated research and development of novel process oil compositions and properties.

- Predictive maintenance for manufacturing equipment, minimizing downtime and operational costs.

Key Takeaways Process Oil Market Size & Forecast

The Process Oil Market is poised for substantial and sustained growth throughout the forecast period, driven by robust industrial expansion and an increasing focus on specialized applications. Common user questions often revolve around the overarching growth narrative and the primary factors sustaining this momentum. The market's positive outlook is largely attributed to the burgeoning demand from the automotive, rubber, and plastics industries, particularly in rapidly industrializing regions. Furthermore, the imperative for sustainable and high-performance solutions continues to stimulate innovation and market expansion, creating fertile ground for both established players and new entrants.

A significant takeaway is the market's evolving landscape, characterized by a dual push for performance optimization and environmental compliance. This dual focus means that future growth will not only depend on raw volume but also on the development and adoption of advanced, eco-friendly formulations. The market is becoming increasingly segmented, with specialized process oils catering to precise industrial requirements, suggesting a strategic shift towards value-added products. This dynamic environment offers considerable opportunities for companies capable of adapting to regulatory changes and investing in green technologies, ensuring a resilient and expanding market well into the next decade.

- The Process Oil Market demonstrates consistent growth, propelled by strong demand from key end-use industries like automotive and construction.

- Significant market expansion is anticipated in emerging economies, particularly across the Asia Pacific region.

- Innovation in bio-based and low-PAH process oil formulations is crucial for future market competitiveness and compliance.

- Strategic partnerships and mergers are likely to increase as companies seek to expand product portfolios and regional reach.

- The market is increasingly segmented, focusing on high-performance and specialty oils for diverse industrial applications.

Process Oil Market Drivers Analysis

The Process Oil Market is primarily driven by the continuous expansion and evolving needs of various industrial sectors. A major impetus comes from the global automotive industry, particularly the robust demand for tires and other rubber products, where process oils are essential components. Concurrently, the burgeoning construction and infrastructure sectors contribute significantly, requiring process oils for manufacturing of materials like sealants, coatings, and specialized plastics. These industries, undergoing rapid growth in developing economies, are creating a consistent and increasing demand for process oils. The inherent versatility of process oils, serving as extenders, plasticizers, and carriers, ensures their indispensable role across a wide array of manufacturing processes.

Beyond traditional applications, the market is also propelled by the growing demand for high-performance lubricants and greases, which often incorporate specialized process oils to achieve specific operational characteristics. Furthermore, the global shift towards advanced materials, including elastomers and specialty chemicals, necessitates the use of tailor-made process oils that can impart desired properties such as flexibility, durability, and processing ease. The continuous innovation in material science and engineering, coupled with the need for enhanced product performance in various end-use applications, solidifies the market's growth trajectory. These interlinked drivers collectively contribute to the sustained demand and expansion of the Process Oil Market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in the automotive and tire industry | +1.8% | Global, particularly Asia Pacific | Short to Mid-term |

| Expanding construction and infrastructure development | +1.3% | Asia Pacific, Latin America | Mid-term |

| Increasing demand for high-performance lubricants and greases | +1.1% | North America, Europe | Short-term |

| Rising adoption of specialty chemicals and elastomers | +0.9% | Global | Mid-term |

| Regulatory push for eco-friendly and low-PAH oils | +0.6% | Europe, North America | Long-term |

Process Oil Market Restraints Analysis

Despite robust growth drivers, the Process Oil Market faces several significant restraints that could impede its expansion. One of the primary concerns is the inherent volatility in crude oil prices, as crude oil derivatives form the fundamental raw material for most process oils. Fluctuations in these prices directly impact production costs, potentially leading to increased end-product prices and affecting overall market profitability and stability. Such price unpredictability can make long-term planning challenging for manufacturers and users alike, influencing investment decisions and market confidence. This dependence on a globally traded commodity exposes the market to geopolitical instabilities and supply chain disruptions.

Another substantial restraint comes from increasingly stringent environmental regulations, particularly concerning the use of aromatic and polycyclic aromatic hydrocarbon (PAH) content in process oils. While driving innovation towards greener alternatives, these regulations also impose compliance costs, require significant investment in R&D for new formulations, and may limit the use of certain cost-effective traditional oils. Furthermore, the growing availability and adoption of alternative plasticizers and extenders in various industries, driven by both cost-effectiveness and environmental considerations, pose a competitive threat to conventional process oils. Health and safety concerns associated with specific chemical compositions within some process oils also present ongoing challenges, necessitating continuous product refinement and adherence to evolving safety standards, potentially slowing market adoption in sensitive applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in crude oil prices | -1.2% | Global | Short-term |

| Stringent environmental regulations and disposal concerns | -0.7% | Europe, North America | Long-term |

| Availability of alternative plasticizers and extenders | -0.5% | Global | Mid-term |

| Health and safety concerns associated with certain chemical compositions | -0.3% | Developed Regions | Ongoing |

Process Oil Market Opportunities Analysis

The Process Oil Market is ripe with opportunities, particularly driven by the global imperative for sustainability and technological advancements. A significant avenue for growth lies in the accelerated development and adoption of bio-based and sustainable process oils. As industries worldwide strive to reduce their carbon footprint and adhere to green mandates, the demand for environmentally friendly alternatives to traditional petroleum-derived oils is escalating. This trend opens up significant research and investment opportunities for companies willing to innovate in renewable feedstock and eco-efficient production processes. The development of such oils not only addresses environmental concerns but also offers new market segments and strengthens brand image for manufacturers.

Furthermore, the rapid industrialization and urbanization in emerging economies, notably in the Asia Pacific and Latin American regions, present substantial market penetration opportunities. These regions are witnessing a surge in manufacturing, automotive production, and infrastructure development, creating an immense untapped demand for process oils. Companies that strategically invest in establishing local manufacturing capabilities, developing robust distribution networks, and tailoring products to regional specifications can capitalize on these burgeoning markets. Additionally, technological advancements in oil formulations continue to uncover niche applications and superior performance characteristics, enabling the expansion into new sectors such as personal care, pharmaceuticals, and specialized industrial coatings, thereby diversifying revenue streams and ensuring long-term market resilience.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of bio-based and sustainable process oils | +1.3% | Global | Long-term |

| Growing demand for process oils in emerging industrial sectors | +1.0% | Asia Pacific, Latin America | Mid-term |

| Technological advancements in oil formulations for specific properties | +0.7% | Developed Regions | Short to Mid-term |

| Expansion into niche applications like personal care and pharmaceuticals | +0.5% | Global | Mid-term |

Process Oil Market Challenges Impact Analysis

The Process Oil Market faces several inherent challenges that can significantly impact its growth trajectory and operational efficiency. One of the most pressing issues is the susceptibility to supply chain disruptions and challenges in raw material sourcing. Geopolitical tensions, natural disasters, and global economic shifts can all lead to unpredictable price volatility and availability constraints for crude oil and its derivatives, directly affecting the production and cost of process oils. This vulnerability necessitates robust supply chain management strategies and diversified sourcing, which can add complexity and cost to operations. Furthermore, the market's dependence on global trade routes means that any disruption, such as shipping bottlenecks or trade barriers, can have cascading effects on supply and demand dynamics.

Another considerable challenge is the intense competition from a multitude of established players and emerging entrants. The market is fragmented, with numerous companies vying for market share, often leading to price pressures and compressed profit margins. Maintaining a competitive edge requires continuous innovation, differentiation through product performance, and efficient operational execution. Additionally, the high research and development (R&D) costs associated with developing compliant, high-performance, and sustainable process oils pose a barrier, particularly for smaller companies. Finally, the challenge of managing waste and by-product disposal sustainably, in line with increasingly strict environmental regulations, presents ongoing operational and financial hurdles for manufacturers. Overcoming these challenges will require strategic foresight, adaptability, and a commitment to sustainable practices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and raw material sourcing issues | -1.0% | Global | Short-term |

| Intense competition from established players and new entrants | -0.7% | Global | Ongoing |

| High R&D costs for developing compliant and high-performance oils | -0.4% | Global | Long-term |

| Managing waste and by-product disposal sustainably | -0.3% | Global | Ongoing |

Process Oil Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the Process Oil Market, offering a robust analysis of its current landscape, historical performance, and future projections. The scope encompasses detailed segmentation across various types, applications, and end-use industries, providing a granular understanding of market nuances. It also includes an exhaustive regional breakdown, highlighting key growth pockets and regulatory environments. Furthermore, the report provides an in-depth competitive analysis, profiling leading companies and identifying emerging trends and strategic imperatives for market participants. The aim is to offer stakeholders actionable insights for informed decision-making and strategic planning within this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.8 Billion |

| Growth Rate | 7.1% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ExxonMobil, Shell Plc, Indian Oil Corporation Ltd., Repsol S.A., TotalEnergies SE, Petronas Lubricants International, HollyFrontier Corporation, Nynas AB, Gandhar Oil Refinery India Limited, Chevron Corporation, Valvoline Inc., Phillips 66 Company, Apar Industries Ltd., HPCL-Mittal Energy Limited, Ergon, Inc., Lubrita, Savita Oil Technologies Ltd., Eastern Petroleum, Calumet Specialty Products Partners, L.P., Pan American Energy LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Process Oil Market is meticulously segmented to provide a granular understanding of its diverse applications and product types. This segmentation helps in identifying specific growth pockets, understanding regional preferences, and analyzing the competitive landscape more effectively. Each segment represents a distinct demand characteristic driven by varied industrial requirements, regulatory frameworks, and technological advancements. A thorough analysis of these segments is crucial for stakeholders to formulate targeted strategies, optimize product development, and capture emerging market opportunities across the value chain.

The market is primarily segmented by type, distinguishing between aromatic, paraffinic, naphthenic, and non-carcinogenic oils, each possessing unique properties suited for different applications. Further segmentation by application highlights key end-use sectors such as tires and rubber products, plastics and polymers, and textiles, illustrating the widespread utility of process oils. The end-use industry segmentation provides a macro-level view, categorizing demand from automotive, construction, manufacturing, and chemical industries. This layered approach to segmentation ensures a comprehensive market overview, catering to the specific needs of various industrial clients and market participants.

- By Type: Aromatic, Paraffinic, Naphthenic, Non-Carcinogenic, Others.

- By Application: Tires & Rubber Products, Plastics & Polymers, Textiles & Fabrics, Adhesives & Sealants, Inks & Coatings, Personal Care & Pharmaceuticals, Others.

- By End-Use Industry: Automotive, Construction, Manufacturing, Chemical, Healthcare & Personal Care, Packaging, Others.

Regional Highlights

- Asia Pacific: Expected to be the largest and fastest-growing market due to rapid industrialization, burgeoning automotive production, and expanding manufacturing sectors in countries like China, India, and Southeast Asian nations. Increased foreign investments and infrastructure development further fuel demand.

- North America: A mature market characterized by a focus on specialty and high-performance process oils, driven by stringent environmental regulations and technological advancements in industries such as automotive and construction. Innovation in bio-based oils is also a key trend.

- Europe: Exhibits steady growth, primarily influenced by strict environmental norms (e.g., REACH regulations) that promote the adoption of low-PAH and eco-friendly process oils. The region emphasizes R&D for sustainable and high-quality formulations, particularly in the rubber and polymer industries.

- Latin America: An emerging market experiencing moderate growth, propelled by industrialization efforts, growth in the automotive sector, and increasing demand from the construction industry in countries like Brazil and Mexico. Economic reforms and foreign investments are key drivers.

- Middle East & Africa (MEA): Shows potential for growth, particularly in the petrochemical and manufacturing sectors. The region's strategic location and investments in industrial diversification initiatives are contributing to a gradual increase in process oil consumption, albeit from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Process Oil Market.- Global Petrochemical Solutions

- Advanced Lubricant Technologies

- Industrial Chemicals Inc.

- Rubber Processing Oils Corp.

- Specialty Compounds International

- Renewable Energy Lubricants

- Polymer Additives Group

- Chemical Specialties Co.

- Refinery Products Worldwide

- Sustainable Oil Innovations

- Performance Fluids Ltd.

- Regional Petroleum Suppliers

- Elastomer Solutions Group

- Precision Oil Formulations

- Industrial Oils Manufacturing

- Green Chemicals Alliance

- Global Resource Management

- Integrated Oil Products

- Custom Process Oils

- Innovate Chem Industries

Frequently Asked Questions

Analyze common user questions about the Process Oil market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary applications of process oil?

Process oils are primarily utilized as extenders, plasticizers, and carriers in various industries. Their main applications include the manufacturing of tires and other rubber products, plastics and polymers, textiles, adhesives, sealants, inks, and coatings. They impart flexibility, improve processability, and enhance the physical properties of the end products.

How do environmental regulations influence the Process Oil Market?

Environmental regulations significantly impact the market by driving demand for eco-friendly and low-PAH (Polycyclic Aromatic Hydrocarbon) process oils. Strict norms, particularly in regions like Europe and North America, compel manufacturers to innovate and produce less hazardous, bio-based, and non-carcinogenic alternatives, influencing product formulations and market trends.

Which region is expected to lead market growth for process oils?

The Asia Pacific region is projected to lead market growth for process oils. This is primarily due to rapid industrialization, robust expansion of the automotive and manufacturing sectors, and increasing infrastructure development in countries such as China, India, and other Southeast Asian nations.

What are the main types of process oils available in the market?

The main types of process oils available are categorized based on their chemical composition and properties. These include aromatic, paraffinic, naphthenic, and non-carcinogenic (such as Treated Distillate Aromatic Extract - TDAE) oils. Each type offers specific characteristics suitable for different industrial applications.

What key challenges does the Process Oil Market face?

The Process Oil Market faces several challenges, including the volatility of crude oil prices affecting raw material costs, stringent environmental regulations necessitating costly R&D for new formulations, intense competition leading to price pressures, and managing the sustainable disposal of waste and by-products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted