Private LTE Market

Private LTE Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706678 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Private LTE Market Size

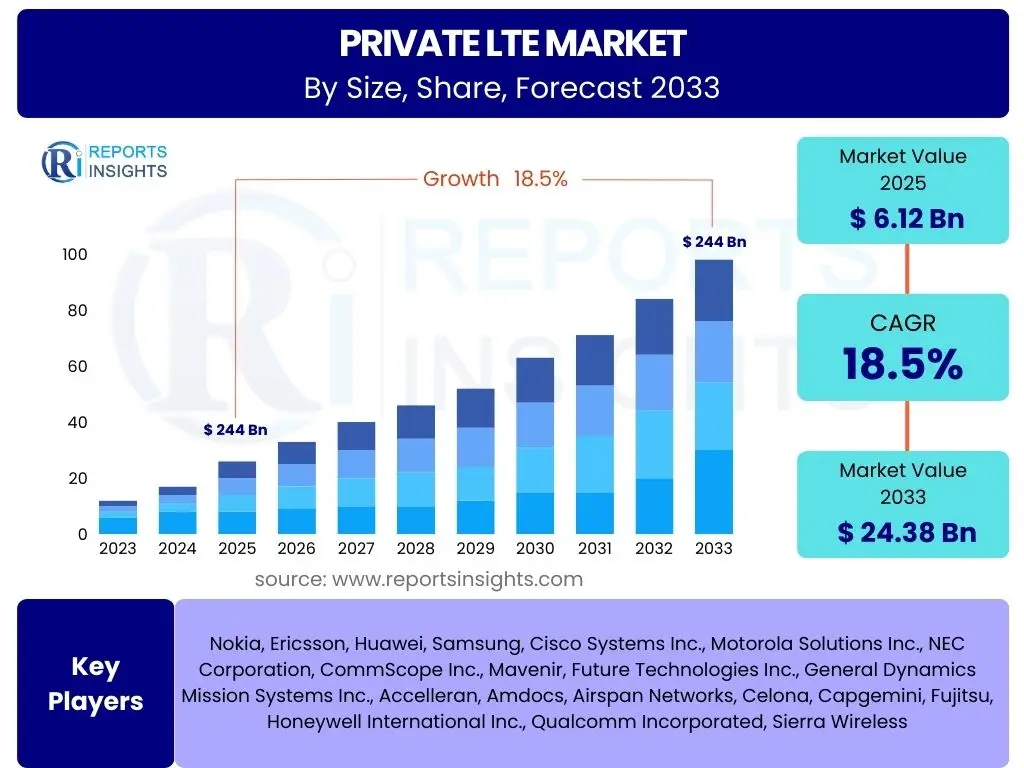

According to Reports Insights Consulting Pvt Ltd, The Private LTE Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 6.12 billion in 2025 and is projected to reach USD 24.38 billion by the end of the forecast period in 2033.

Key Private LTE Market Trends & Insights

The Private LTE market is experiencing significant evolution, driven by the increasing demand for secure, reliable, and high-performance wireless connectivity in enterprise and industrial environments. Key trends indicate a strong focus on enhancing operational efficiency, enabling advanced automation, and ensuring data privacy within closed networks. Industries such as manufacturing, mining, oil and gas, and public safety are at the forefront of adoption, leveraging private LTE for mission-critical communications, real-time data processing, and asset tracking.

Furthermore, the market is witnessing a convergence with 5G technologies, as enterprises seek to future-proof their networks with capabilities like ultra-low latency, massive machine-type communications, and enhanced mobile broadband. The rise of edge computing, artificial intelligence integration, and the "as-a-service" deployment models are also shaping the landscape, making private LTE solutions more accessible and adaptable for diverse business needs. This strategic shift towards dedicated networks underscores a broader industrial digital transformation.

- Growing adoption in industrial automation and Industry 4.0 initiatives.

- Increasing demand for secure and reliable mission-critical communications.

- Convergence with private 5G technologies for advanced capabilities.

- Integration of edge computing for localized data processing and reduced latency.

- Shift towards "Network as a Service" and managed service models.

- Expansion into new verticals such as smart logistics, agriculture, and healthcare.

- Enhanced focus on cybersecurity and data sovereignty within private networks.

AI Impact Analysis on Private LTE

Artificial Intelligence (AI) is poised to revolutionize Private LTE networks by significantly enhancing their operational intelligence, efficiency, and security. Users are keen to understand how AI can optimize network performance, automate complex management tasks, and provide predictive insights, reducing operational expenditures and improving service reliability. The integration of AI algorithms enables self-optimizing networks, where traffic flow, resource allocation, and antenna configurations are dynamically adjusted for peak performance, ensuring consistent quality of service for critical applications.

Beyond optimization, AI also plays a crucial role in bolstering the security posture of Private LTE networks. Concerns about cyber threats and data breaches in private deployments are addressed through AI-powered anomaly detection, intrusion prevention systems, and predictive threat intelligence. Furthermore, AI facilitates advanced analytics on network data, providing valuable insights for capacity planning, fault prediction, and even new service creation. The synergy between AI and Private LTE is expected to drive greater automation, resilience, and adaptability, transforming how these networks are deployed and managed.

- Predictive maintenance for network infrastructure, reducing downtime.

- Automated network optimization and resource allocation for improved performance.

- Enhanced cybersecurity through AI-driven anomaly detection and threat intelligence.

- Intelligent traffic management and load balancing for optimal data flow.

- AI-powered edge analytics for real-time decision-making in industrial applications.

- Automated fault diagnosis and self-healing network capabilities.

- Optimization of energy consumption through intelligent power management.

Key Takeaways Private LTE Market Size & Forecast

The Private LTE market is on a robust growth trajectory, fundamentally driven by the escalating need for dedicated, high-performance, and secure wireless networks across diverse industries. The projected significant increase in market valuation underscores its critical role as an enabler for digital transformation initiatives, particularly where public networks cannot meet stringent requirements for latency, reliability, or security. This growth is a direct reflection of enterprises seeking greater control over their connectivity infrastructure to support advanced applications like industrial automation, real-time analytics, and mission-critical communications.

The forecast highlights that Private LTE is not merely a niche solution but a foundational technology poised for widespread adoption, particularly as it converges with 5G capabilities. Key stakeholders are increasingly recognizing its strategic value in fostering innovation, enhancing operational efficiency, and creating competitive advantages. The market's expansion is indicative of a broader industry shift towards specialized, enterprise-grade connectivity tailored to the unique demands of Industry 4.0, IoT deployments, and sovereign data management.

- Market size projected to grow from USD 6.12 billion in 2025 to USD 24.38 billion by 2033.

- CAGR of 18.5% indicates strong and sustained market expansion.

- Significant growth driven by industrial and enterprise demand for secure, reliable connectivity.

- Private LTE is a critical enabler for Industry 4.0 and digital transformation.

- Increasing enterprise investment in dedicated network infrastructure for operational control.

Private LTE Market Drivers Analysis

The Private LTE market is primarily propelled by the escalating demand for dedicated, secure, and reliable wireless connectivity that conventional public networks or Wi-Fi solutions often cannot provide. Industries such as manufacturing, utilities, mining, and public safety require robust communication infrastructures to support mission-critical applications, real-time data processing, and extensive IoT deployments. Private LTE networks offer superior control over network performance, capacity, and security, making them ideal for environments where operational continuity and data integrity are paramount.

Another significant driver is the global push towards digital transformation and the adoption of Industry 4.0 paradigms. Enterprises are investing heavily in automation, robotics, and advanced analytics, all of which necessitate a low-latency, high-bandwidth, and highly secure network backbone. Private LTE, with its predictable performance and ability to operate independently of public infrastructure, empowers organizations to build smart factories, automated logistics hubs, and connected work sites, fostering innovation and improving operational efficiency across the board.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for secure & reliable connectivity | +5.2% | Global, especially critical infrastructure sectors | 2025-2033 |

| Rapid adoption of Industry 4.0 and IoT | +4.8% | North America, Europe, Asia Pacific (APAC) | 2025-2033 |

| Need for enhanced control over network & data | +3.5% | Global, particularly enterprise segments | 2026-2033 |

| Cost-effectiveness compared to wired alternatives for remote sites | +2.1% | Remote/Rural Areas, Mining, Oil & Gas | 2027-2033 |

| Increased focus on public safety & critical communications | +1.9% | North America, Europe, parts of APAC | 2025-2030 |

Private LTE Market Restraints Analysis

Despite its significant growth potential, the Private LTE market faces several restraints that could impede its expansion. One primary challenge is the high initial capital expenditure required for deploying private networks, encompassing infrastructure, spectrum licensing, and specialized equipment. This substantial upfront investment can deter smaller enterprises or organizations with limited budgets, making them opt for less robust but more affordable alternatives like enhanced Wi-Fi solutions or public network slicing, especially if their connectivity demands are not strictly mission-critical.

Another significant restraint involves the complexity of spectrum availability and regulatory frameworks. Access to dedicated or shared spectrum is crucial for private LTE deployments, but regulations vary widely across different countries and regions. Obtaining necessary licenses can be a time-consuming and intricate process, adding layers of complexity and cost. Furthermore, a shortage of skilled professionals with expertise in deploying, managing, and maintaining private cellular networks presents a bottleneck, leading to increased operational challenges and potentially higher long-term costs for businesses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital expenditure (CapEx) | -3.7% | Global, particularly SMEs | 2025-2030 |

| Complexity of spectrum availability and licensing | -2.8% | Region-specific (e.g., Europe, parts of APAC) | 2025-2033 |

| Lack of skilled personnel for deployment & maintenance | -2.1% | Global, developing regions more affected | 2025-2033 |

| Competition from advanced Wi-Fi technologies (Wi-Fi 6/7) | -1.5% | Global, especially indoor enterprise environments | 2025-2030 |

Private LTE Market Opportunities Analysis

The Private LTE market is presented with significant opportunities, primarily driven by the ongoing evolution to 5G and the increasing demand for specialized, high-performance network solutions across various new applications. The advent of Private 5G, building upon the foundations of Private LTE, offers enhanced capabilities such as ultra-reliable low-latency communication (URLLC), massive machine-type communication (mMTC), and enhanced mobile broadband (eMBB). These advancements unlock new possibilities for highly sensitive industrial applications, including real-time automation in smart factories, remote-controlled robotics, and precision agriculture, thereby expanding the market's addressable scope beyond traditional deployments.

Another major opportunity lies in the expansion of "Network as a Service" (NaaS) and managed service models. These models lower the entry barrier for enterprises by reducing upfront capital expenditures and simplifying network management. Companies can leverage third-party expertise for deployment, operation, and maintenance of their private networks, making the technology more accessible to a broader range of businesses, including small and medium-sized enterprises (SMEs). This shift allows organizations to focus on their core competencies while benefiting from robust, tailored connectivity, creating a flexible and scalable pathway for private LTE adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolution towards Private 5G deployments | +4.5% | Global, high-tech industrial sectors | 2026-2033 |

| Growth of Network as a Service (NaaS) models | +3.8% | Global, appealing to SMEs and large enterprises | 2025-2033 |

| Untapped potential in new vertical markets (e.g., logistics, healthcare, retail) | +2.9% | Global, particularly emerging economies | 2027-2033 |

| Integration with edge computing for enhanced capabilities | +2.2% | North America, Europe, APAC advanced manufacturing | 2025-2030 |

| Government initiatives for critical infrastructure modernization | +1.7% | Developed countries (e.g., US, Germany, Japan) | 2025-2030 |

Private LTE Market Challenges Impact Analysis

The Private LTE market faces significant challenges, primarily centered around regulatory complexities and interoperability issues. The fragmented and varied regulatory landscape for spectrum allocation across different countries can be a substantial barrier, complicating international deployments and increasing the time and cost associated with obtaining necessary licenses. Different regions may have distinct approaches to shared spectrum (e.g., CBRS in the US, local licensing in Germany), which requires vendors and enterprises to navigate a complex web of rules, hindering standardization and broader adoption.

Another key challenge is the integration of private LTE networks with existing legacy systems and diverse operational technologies (OT) within industrial environments. Many enterprises operate with a mix of older equipment and proprietary systems that may not seamlessly integrate with new cellular infrastructure. This necessitates significant customization, extensive testing, and potentially costly upgrades, adding layers of complexity and risk to deployment projects. Overcoming these integration hurdles requires deep technical expertise and close collaboration between IT and OT departments, which can be a slow and arduous process for many organizations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory complexities & fragmented spectrum policies | -2.5% | Global, varying by country/region | 2025-2033 |

| Interoperability issues with legacy systems & OT | -1.8% | Global, particularly mature industrial sectors | 2025-2030 |

| Security concerns and cyber vulnerabilities | -1.2% | Global, highly sensitive data environments | 2025-2033 |

| High cost of deployment and operational complexity for SMEs | -0.9% | Global, less developed regions and smaller enterprises | 2025-2030 |

Private LTE Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Private LTE market, offering a detailed overview of its current size, historical growth, and future projections. The scope encompasses a thorough examination of key market trends, growth drivers, and prevailing restraints that influence market dynamics. Additionally, the report identifies significant opportunities and emerging challenges, providing a holistic perspective on the industry landscape. Special emphasis is placed on the impact of artificial intelligence on private LTE networks and the evolving regional market landscapes. The report also includes a detailed segmentation analysis, breaking down the market by component, application, technology, and end-user, to offer granular insights into market segments and their potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.12 Billion |

| Market Forecast in 2033 | USD 24.38 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nokia, Ericsson, Huawei, Samsung, Cisco Systems Inc., Motorola Solutions Inc., NEC Corporation, CommScope Inc., Mavenir, Future Technologies Inc., General Dynamics Mission Systems Inc., Accelleran, Amdocs, Airspan Networks, Celona, Capgemini, Fujitsu, Honeywell International Inc., Qualcomm Incorporated, Sierra Wireless |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Private LTE market is comprehensively segmented to provide granular insights into its diverse components, technological applications, and end-user adoption patterns. This segmentation allows for a nuanced understanding of market dynamics, enabling businesses to identify specific growth areas and tailor their strategies effectively. By breaking down the market, stakeholders can discern which technologies are gaining traction, which industries are leading adoption, and what types of services are in highest demand, reflecting the evolving needs of various sectors requiring dedicated connectivity.

Segmentation by component highlights the intricate ecosystem of hardware (such as radios, core network equipment, antennas), software (network management, security, orchestration), and services (professional and managed services) that constitute a private LTE deployment. This categorization is crucial for understanding the value chain and identifying areas for innovation or strategic partnerships. The distinction between FDD and TDD technologies further refines the understanding of spectrum utilization and deployment scenarios, catering to different regional and application-specific requirements.

Furthermore, segmenting by application (e.g., manufacturing, public safety, energy & utilities) and end-user (enterprise, government) provides a clear picture of vertical-specific demand and market maturity. This detailed analysis helps in forecasting future growth trajectories for each segment, understanding investment patterns, and recognizing the unique operational challenges and opportunities pertinent to each industry and type of organization opting for private LTE solutions.

- By Component:

- Hardware

- Software

- Services

- By Technology:

- FDD (Frequency Division Duplex)

- TDD (Time Division Duplex)

- By Application:

- Manufacturing

- Mining

- Oil & Gas

- Energy & Utilities

- Public Safety & Government

- Transportation & Logistics

- Healthcare

- Defense

- Smart Cities & Campuses

- Others

- By End-User:

- Enterprise

- Government

Regional Highlights

- North America: This region is a leading adopter of Private LTE due to a robust industrial base, significant investments in digital transformation, and the availability of dedicated spectrum (like CBRS in the U.S.). High demand from manufacturing, utilities, and public safety sectors, alongside early technology adoption, drives market growth.

- Europe: Driven by strong manufacturing industries (e.g., Germany's Industry 4.0 initiatives) and a focus on critical infrastructure modernization, Europe shows substantial growth. Supportive regulatory environments in some countries for local spectrum licensing further boost private LTE deployments.

- Asia Pacific (APAC): Experiencing rapid expansion, particularly in countries like China, Japan, and India, fueled by large-scale manufacturing, smart city projects, and significant government investments in digital infrastructure. Emerging economies in the region are also contributing to growth through industrial automation.

- Latin America: This region is an emerging market, with growing interest from resource-intensive industries such as mining and oil & gas, seeking to enhance operational efficiency and safety through dedicated connectivity. Infrastructure development and digital inclusion initiatives are also contributing factors.

- Middle East and Africa (MEA): Growth in MEA is largely driven by large-scale industrial projects, smart city developments (e.g., in UAE, Saudi Arabia), and the modernization of public safety and defense communication systems. Investments in oil & gas and mining sectors are also key contributors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Private LTE Market.- Nokia

- Ericsson

- Huawei

- Samsung

- Cisco Systems Inc.

- Motorola Solutions Inc.

- NEC Corporation

- CommScope Inc.

- Mavenir

- Future Technologies Inc.

- General Dynamics Mission Systems Inc.

- Accelleran

- Amdocs

- Airspan Networks

- Celona

- Capgemini

- Fujitsu

- Honeywell International Inc.

- Qualcomm Incorporated

- Sierra Wireless

Frequently Asked Questions

What is Private LTE and how does it differ from Wi-Fi or public cellular networks?

Private LTE is a dedicated cellular network deployed for a specific organization or enterprise, offering enhanced security, reliability, and control over data and communications. Unlike public cellular networks, it is not shared with the general public. Compared to Wi-Fi, Private LTE provides superior coverage, mobility, deep penetration, predictable latency, and robust security, making it ideal for mission-critical industrial and enterprise applications that require dedicated bandwidth and guaranteed performance.

Which industries are primarily adopting Private LTE technology?

Key industries adopting Private LTE include manufacturing (for Industry 4.0 and automation), mining (for remote operations and safety), oil & gas (for critical communications and monitoring), energy & utilities (for smart grid management), public safety (for secure emergency communications), and transportation & logistics (for asset tracking and fleet management). Its capabilities align well with the demanding connectivity needs of these sectors.

What are the main benefits of deploying a Private LTE network?

The primary benefits of Private LTE networks include enhanced security and data privacy, guaranteed quality of service and low latency for critical applications, superior coverage and mobility across large sites, independent network control, and high reliability. These features are crucial for supporting advanced automation, real-time data analytics, and mission-critical communications that cannot tolerate network disruptions or compromises.

What is the role of 5G in the future of Private LTE?

5G represents the next evolution for Private LTE networks, often referred to as Private 5G. It builds upon LTE's foundation by introducing enhanced capabilities such as ultra-reliable low-latency communication (URLLC), massive machine-type communication (mMTC), and even higher bandwidth. This enables more advanced applications like hyper-automated factories, remote surgery, and sophisticated real-time robotics, expanding the potential and capabilities of private cellular networks significantly.

What is the typical cost associated with Private LTE deployment?

The typical cost of Private LTE deployment varies significantly based on factors such as network size, coverage area, required capacity, choice of hardware/software vendors, and spectrum licensing. Initial capital expenditure can be substantial, including core network equipment, radios, antennas, and professional services. However, operational costs can be lower over time due to efficient network management and reduced reliance on public services. "Network as a Service" models are emerging to lower upfront costs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted