Power Electronic Market

Power Electronic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704051 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Power Electronic Market Size

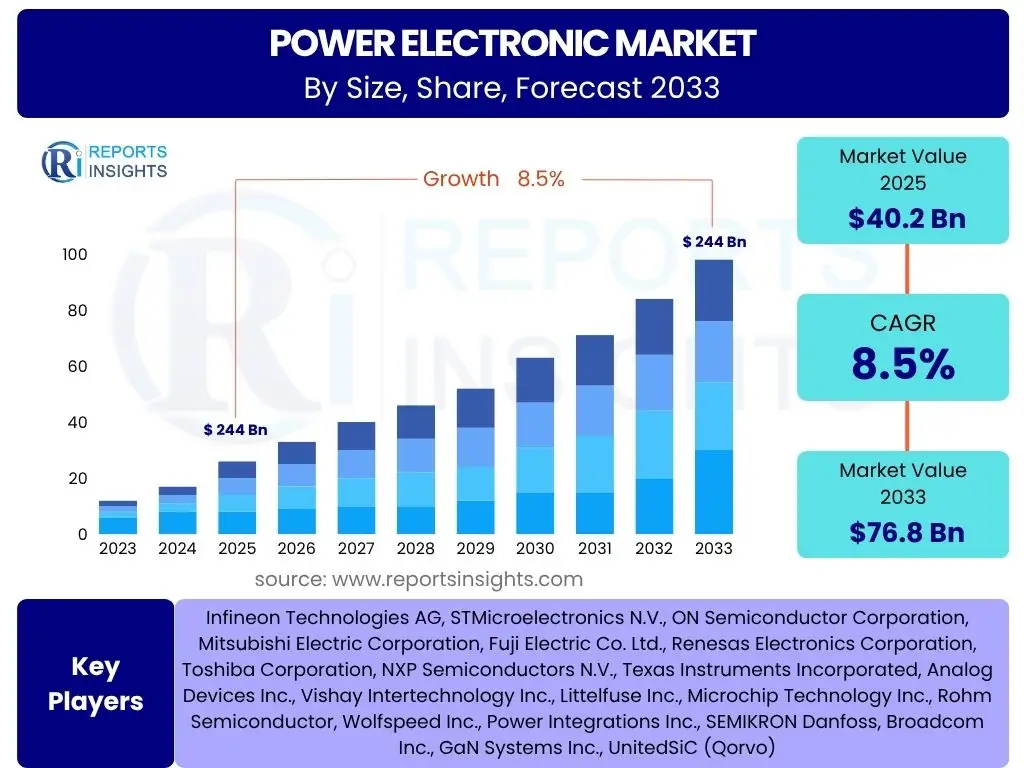

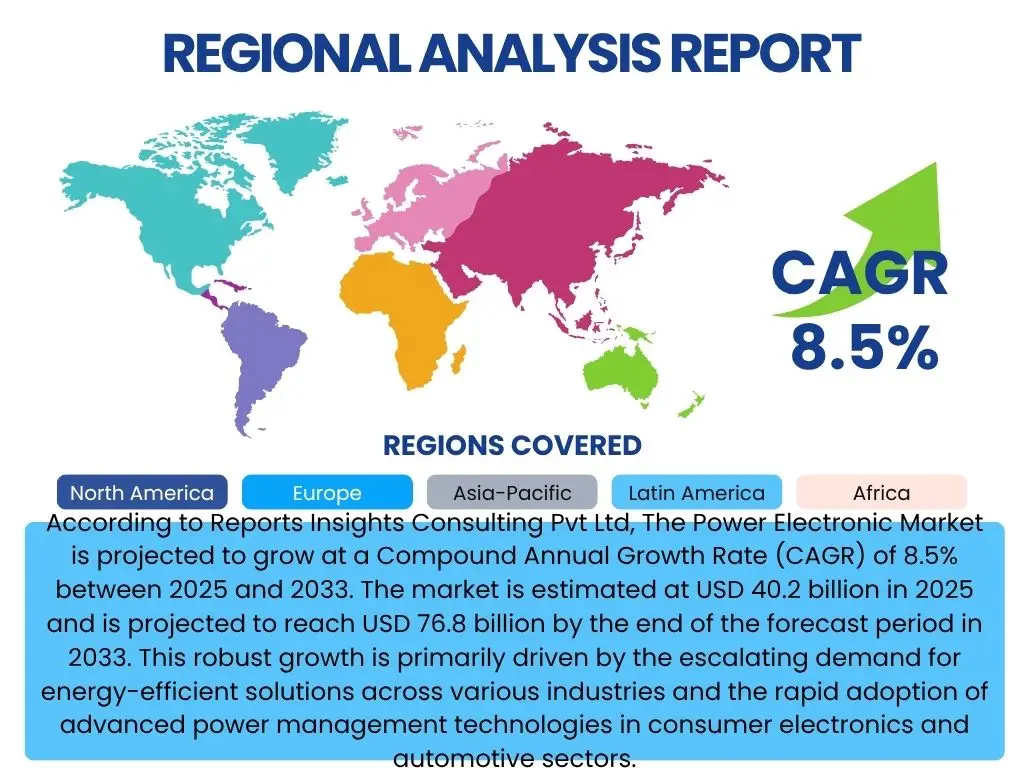

According to Reports Insights Consulting Pvt Ltd, The Power Electronic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 40.2 billion in 2025 and is projected to reach USD 76.8 billion by the end of the forecast period in 2033. This robust growth is primarily driven by the escalating demand for energy-efficient solutions across various industries and the rapid adoption of advanced power management technologies in consumer electronics and automotive sectors.

Key Power Electronic Market Trends & Insights

Current inquiries regarding the Power Electronic market frequently revolve around the evolution of semiconductor materials, the integration of power electronics into new application areas, and the overarching push for greater energy efficiency. Users are particularly interested in how emerging technologies are shaping the market's future and contributing to sustainable development. The market is witnessing a significant shift towards more compact, reliable, and high-performance solutions, driven by innovation in component design and manufacturing processes. This includes advancements in packaging technologies and thermal management solutions, which are critical for enhancing the overall efficiency and longevity of power electronic devices.

Furthermore, there is a clear trend towards the adoption of Wide Bandgap (WBG) materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), due to their superior performance characteristics compared to traditional silicon-based components. These materials enable higher switching frequencies, reduced power losses, and operation at elevated temperatures, making them ideal for high-power and high-frequency applications. The increased investment in research and development for these advanced materials underscores their pivotal role in the future growth of the power electronic market. Moreover, the decentralization of power generation and the expansion of smart grid initiatives are creating new demands for sophisticated power electronic converters and inverters, ensuring efficient power flow and grid stability.

- Increased adoption of Wide Bandgap (WBG) semiconductors (SiC, GaN) for higher efficiency and power density.

- Rapid electrification of the automotive sector, particularly electric vehicles (EVs) and charging infrastructure.

- Growing integration of power electronics in renewable energy systems, including solar inverters and wind turbine converters.

- Miniaturization of power modules and components to meet the demand for compact and lightweight designs.

- Emphasis on digital control and advanced packaging technologies for enhanced performance and reliability.

- Expansion of industrial automation and robotics requiring precise and efficient motor control.

AI Impact Analysis on Power Electronic

User queries regarding the influence of Artificial Intelligence (AI) on power electronics often center on how AI can optimize system performance, enhance reliability, and enable smarter energy management. There is significant interest in AI's role in predictive maintenance for power devices, real-time control optimization, and the design phase of power electronic converters. The integration of AI algorithms facilitates more intelligent and adaptive control strategies, allowing power electronic systems to operate closer to their optimal efficiency points across varying load conditions. This contributes directly to reduced energy consumption and extended component lifespan.

AI also plays a crucial role in accelerating the design and simulation of complex power electronic circuits by analyzing vast datasets of design parameters and performance metrics, thereby reducing development cycles. Furthermore, AI-driven diagnostics and fault detection capabilities are transforming the maintenance of power electronic systems, moving from reactive repairs to predictive interventions. This proactive approach minimizes downtime and enhances operational reliability, particularly in critical applications such as data centers, renewable energy installations, and electric vehicle drivetrains. The ongoing evolution of AI models and increased computational power are expected to unlock further advancements in the autonomous operation and optimization of power electronic systems.

- AI-driven optimization of power converter control algorithms for enhanced efficiency and stability.

- Predictive maintenance and fault detection in power electronic systems using machine learning models.

- Accelerated design and simulation of power electronic circuits through AI-assisted tools.

- Real-time adaptive power management and load balancing in smart grids and data centers.

- Enhanced thermal management and performance monitoring through AI-based analytics.

Key Takeaways Power Electronic Market Size & Forecast

Common user questions regarding the market forecast often highlight concerns about sustained growth, technological innovation, and the long-term viability of specific market segments. The key insights reveal a highly dynamic market poised for substantial expansion, underpinned by fundamental shifts in energy consumption patterns and technological advancements. The forecast signifies a strong, sustained growth trajectory for the Power Electronic market, driven by its indispensable role in the global transition towards electrification and energy efficiency. Demand for higher power density, increased reliability, and superior thermal performance will continue to shape product development and market dynamics.

The market's resilience is further supported by diversified application areas, ranging from high-volume consumer electronics to mission-critical industrial and automotive systems. Investments in research and development of next-generation materials like SiC and GaN are pivotal, indicating a future where power electronics are even more compact, efficient, and capable of operating under extreme conditions. The increasing penetration of renewable energy sources and the global push for electric vehicles are not merely trends but foundational pillars of this market's growth. Stakeholders are advised to focus on innovation in packaging, thermal management, and advanced control techniques to capitalize on these opportunities.

- Robust market growth projected at an 8.5% CAGR, reaching USD 76.8 billion by 2033.

- Electric vehicle adoption and renewable energy integration are primary long-term growth accelerators.

- Technological advancements in Wide Bandgap (WBG) materials are transforming performance capabilities.

- Growing emphasis on energy efficiency and power density across all applications.

- Significant opportunities in industrial automation, data centers, and grid infrastructure modernization.

Power Electronic Market Drivers Analysis

The Power Electronic market is primarily propelled by several synergistic factors that reflect global energy and technological transitions. The increasing adoption of electric vehicles (EVs) globally stands as a monumental driver, creating unprecedented demand for highly efficient power converters, inverters, and on-board chargers. Concurrently, the expansive deployment of renewable energy sources, such as solar photovoltaic systems and wind turbines, necessitates advanced power electronics for efficient energy conversion, grid integration, and storage solutions. These drivers are fundamentally reshaping the energy landscape and placing power electronics at the core of sustainable infrastructure development.

Furthermore, the relentless demand for energy efficiency across all sectors is a foundational driver. Power electronics enable significant reductions in energy waste in a myriad of applications, from consumer electronics and home appliances to industrial motor drives and data centers. Governments and industries worldwide are imposing stricter energy efficiency standards, compelling manufacturers to integrate more sophisticated power management solutions. This regulatory push, combined with the economic benefits of lower operational costs, creates a strong incentive for widespread adoption of power electronic components. The ongoing digitalization and automation of industries also contribute significantly, as modern manufacturing processes and robotics rely heavily on precise and efficient power control systems facilitated by advanced power electronics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Electric Vehicle (EV) Adoption | +2.5% | North America, Europe, Asia Pacific (China, Japan, South Korea) | Short to Long Term (2025-2033) |

| Growing Integration of Renewable Energy Sources | +2.0% | Europe, Asia Pacific (China, India), North America | Short to Long Term (2025-2033) |

| Increasing Demand for Energy Efficiency | +1.5% | Global | Ongoing (2025-2033) |

| Expansion of Industrial Automation and Robotics | +1.0% | Asia Pacific, Europe, North America | Medium to Long Term (2027-2033) |

Power Electronic Market Restraints Analysis

Despite robust growth prospects, the Power Electronic market faces certain restraints that could impact its expansion. One significant challenge is the inherent complexity and high cost associated with designing and manufacturing advanced power electronic systems, particularly those utilizing Wide Bandgap (WBG) materials. The specialized fabrication processes and the need for sophisticated thermal management solutions drive up production costs, which can limit broader adoption in price-sensitive applications. Furthermore, the steep learning curve and expertise required for designing and integrating these advanced components also act as a barrier for smaller enterprises or those transitioning from traditional silicon-based solutions, necessitating substantial investment in training and infrastructure.

Another notable restraint pertains to potential supply chain disruptions and the availability of critical raw materials. The global semiconductor industry has recently experienced severe component shortages, which directly impacts the production of power electronic devices. Reliance on a limited number of suppliers for highly specialized components or rare earth elements can expose the market to vulnerabilities arising from geopolitical tensions, natural disasters, or unexpected surges in demand. Such disruptions can lead to production delays, increased costs, and ultimately, slower market growth. Additionally, the challenge of managing increasing power densities in smaller form factors presents thermal management complexities that require innovative and often costly cooling solutions, adding to the overall system design burden and potential limitations in performance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Costs & Design Complexity | -0.8% | Global | Short to Medium Term (2025-2029) |

| Supply Chain Vulnerabilities & Component Shortages | -0.7% | Global | Short to Medium Term (2025-2028) |

| Challenges in Thermal Management for High Power Density | -0.5% | Global | Ongoing (2025-2033) |

Power Electronic Market Opportunities Analysis

The Power Electronic market is brimming with promising opportunities driven by technological innovation and evolving application landscapes. A significant opportunity lies in the continuous advancement and widespread commercialization of Wide Bandgap (WBG) semiconductors, specifically Silicon Carbide (SiC) and Gallium Nitride (GaN). As manufacturing processes mature and costs decrease, these materials are set to revolutionize various applications by enabling power converters with significantly higher efficiencies, smaller footprints, and improved reliability, thereby unlocking new design possibilities and market segments previously unattainable with traditional silicon. This includes high-power fast charging solutions for EVs, more efficient power supplies for data centers, and advanced inverters for renewable energy systems.

Another burgeoning opportunity is the expanding ecosystem of smart grids and energy storage systems. As countries invest heavily in modernizing their electrical infrastructure to accommodate decentralized power generation and enhance grid resilience, the demand for sophisticated power electronic solutions for grid-tied inverters, energy management systems, and battery storage integration will surge. The development of advanced packaging technologies, which allow for higher power density and better thermal performance, also presents a substantial opportunity for manufacturers to create more compact and robust power modules. Furthermore, the emergence of new applications in areas such as aerospace and defense, medical devices, and even space exploration, where extreme operating conditions and stringent reliability requirements are paramount, offers niche yet high-value growth avenues for specialized power electronic components.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Adoption of Wide Bandgap (WBG) Technologies | +1.8% | Global | Short to Long Term (2025-2033) |

| Investments in Smart Grid and Energy Storage Infrastructure | +1.5% | North America, Europe, Asia Pacific (China, India) | Medium to Long Term (2027-2033) |

| Emergence of New High-Reliability Applications | +0.7% | North America, Europe, Asia Pacific (Japan) | Medium to Long Term (2028-2033) |

Power Electronic Market Challenges Impact Analysis

The Power Electronic market faces several inherent challenges that demand continuous innovation and strategic adaptation from industry players. One significant challenge is the ongoing pressure for miniaturization and increasing power density. As devices become smaller, dissipating heat effectively becomes exponentially more difficult. This thermal management challenge is critical because excessive heat can degrade performance, reduce reliability, and shorten the lifespan of power electronic components. Developing advanced cooling solutions and efficient packaging techniques is crucial, but often adds to the complexity and cost of the final product, potentially limiting widespread adoption in certain applications.

Another pervasive challenge is the shortage of a skilled workforce proficient in power electronics design, manufacturing, and integration. The rapid pace of technological advancements, particularly with the transition to Wide Bandgap materials and complex digital control systems, creates a gap between the demand for specialized engineers and the available talent pool. This scarcity can hinder innovation, slow down product development cycles, and increase operational costs for companies. Furthermore, navigating the complex landscape of regulatory compliance and standardization across different regions and industries poses another significant hurdle. Ensuring that power electronic devices meet diverse safety, electromagnetic compatibility (EMC), and energy efficiency standards requires substantial investment in testing and certification, adding layers of complexity to market entry and product deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and Power Density Requirements | -0.6% | Global | Ongoing (2025-2033) |

| Skilled Workforce Shortage | -0.5% | Global | Short to Long Term (2025-2033) |

| Complex Regulatory Compliance and Standardization | -0.4% | Global | Ongoing (2025-2033) |

Power Electronic Market - Updated Report Scope

This report provides a comprehensive analysis of the global Power Electronic market, offering detailed insights into market dynamics, key trends, segmentation, and regional landscapes. It encompasses an in-depth assessment of market drivers, restraints, opportunities, and challenges, along with a thorough competitive analysis of leading market players. The scope includes both current market sizing and future projections, highlighting the transformative impact of emerging technologies and changing industrial demands.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 40.2 billion |

| Market Forecast in 2033 | USD 76.8 billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, STMicroelectronics N.V., ON Semiconductor Corporation, Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Renesas Electronics Corporation, Toshiba Corporation, NXP Semiconductors N.V., Texas Instruments Incorporated, Analog Devices Inc., Vishay Intertechnology Inc., Littelfuse Inc., Microchip Technology Inc., Rohm Semiconductor, Wolfspeed Inc., Power Integrations Inc., SEMIKRON Danfoss, Broadcom Inc., GaN Systems Inc., UnitedSiC (Qorvo) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Electronic market is meticulously segmented to provide a granular view of its various components and their respective contributions to overall market growth. This comprehensive segmentation allows for a deeper understanding of market dynamics across different technologies, materials, applications, and power ranges. Each segment represents a distinct area of innovation and demand, driven by specific industrial requirements and technological advancements. Understanding these segments is crucial for stakeholders to identify lucrative opportunities and tailor their strategies effectively.

The segmentation by device type distinguishes between Power ICs, Power Modules, and Power Discretes, reflecting varying levels of integration and power handling capabilities. Material segmentation, particularly focusing on Silicon, Silicon Carbide, and Gallium Nitride, highlights the shift towards high-performance WBG semiconductors. Application-based segmentation provides insight into the diverse end-use industries driving demand, from high-volume consumer electronics to high-power automotive and industrial sectors. Lastly, power range segmentation categorizes devices by their operational power levels, which influences design choices and material selection. This multi-faceted approach ensures a thorough and actionable market analysis.

- By Device Type: Power ICs, Power Modules, Power Discretes

- By Material: Silicon (Si), Silicon Carbide (SiC), Gallium Nitride (GaN), Other Materials

- By Application: Automotive, Consumer Electronics, Industrial, IT & Telecom, Energy & Power, Aerospace & Defense, Healthcare

- By Power Range: Low Power, Medium Power, High Power

Regional Highlights

- North America: This region demonstrates strong growth, driven by significant investments in electric vehicle infrastructure, smart grid modernization, and advanced data centers. The presence of key technology developers and a robust research ecosystem further supports market expansion. Adoption of SiC and GaN in automotive and renewable energy applications is particularly prominent.

- Europe: Europe is a leading market, propelled by stringent energy efficiency regulations, ambitious renewable energy targets, and robust automotive industry electrification initiatives. Countries like Germany and the Nordic nations are at the forefront of adopting advanced power electronic solutions for industrial automation and sustainable energy systems.

- Asia Pacific (APAC): APAC is expected to be the fastest-growing market due to rapid industrialization, burgeoning consumer electronics manufacturing, and extensive investments in electric mobility and renewable energy, particularly in China, India, Japan, and South Korea. Government support for domestic manufacturing and a large population base contribute significantly to demand.

- Latin America: This region shows steady growth, primarily driven by increasing industrialization, expanding telecommunications infrastructure, and emerging renewable energy projects. While smaller than other regions, consistent growth in automotive and consumer electronics sectors provides a stable foundation.

- Middle East and Africa (MEA): The MEA region is experiencing growth mainly due to diversifying economies, significant investments in energy infrastructure, and a push towards renewable energy sources. Projects related to smart cities and industrial development are creating new opportunities for power electronic applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Electronic Market.- Infineon Technologies AG

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd.

- Renesas Electronics Corporation

- Toshiba Corporation

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Vishay Intertechnology Inc.

- Littelfuse Inc.

- Microchip Technology Inc.

- Rohm Semiconductor

- Wolfspeed Inc.

- Power Integrations Inc.

- SEMIKRON Danfoss

- Broadcom Inc.

- GaN Systems Inc.

- UnitedSiC (Qorvo)

Frequently Asked Questions

Analyze common user questions about the Power Electronic market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are power electronics?

Power electronics refers to the application of solid-state electronics to control and convert electric power. They enable efficient conversion between AC and DC, regulate voltage and current, and manage power flow in various systems, ranging from small consumer devices to large industrial applications and energy grids.

What is driving the growth of the Power Electronic market?

Key growth drivers include the rapid global adoption of electric vehicles (EVs), the increasing integration of renewable energy sources such as solar and wind power, a pervasive demand for higher energy efficiency across all industries, and the expansion of industrial automation and robotics.

How do Wide Bandgap (WBG) materials like SiC and GaN impact the market?

Wide Bandgap (WBG) materials such as Silicon Carbide (SiC) and Gallium Nitride (GaN) are revolutionizing power electronics by enabling devices that operate at higher switching frequencies, higher temperatures, and with significantly lower power losses compared to traditional silicon. This leads to more compact, efficient, and reliable power systems, particularly beneficial for EVs, fast chargers, and data centers.

Which industries are the primary consumers of power electronics?

Power electronics are widely used across numerous industries, including automotive (especially EVs and charging infrastructure), consumer electronics (smartphones, home appliances), industrial (motor drives, power supplies, automation), IT & Telecom (data centers, telecom equipment), and Energy & Power (renewable energy inverters, grid infrastructure, energy storage).

What is the market forecast for the Power Electronic market by 2033?

The Power Electronic market is projected to reach USD 76.8 billion by the end of 2033, growing at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. This growth is driven by continuous technological advancements and increasing demand for energy-efficient solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted