Power Electronic for Electric Vehicle Market

Power Electronic for Electric Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708880 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

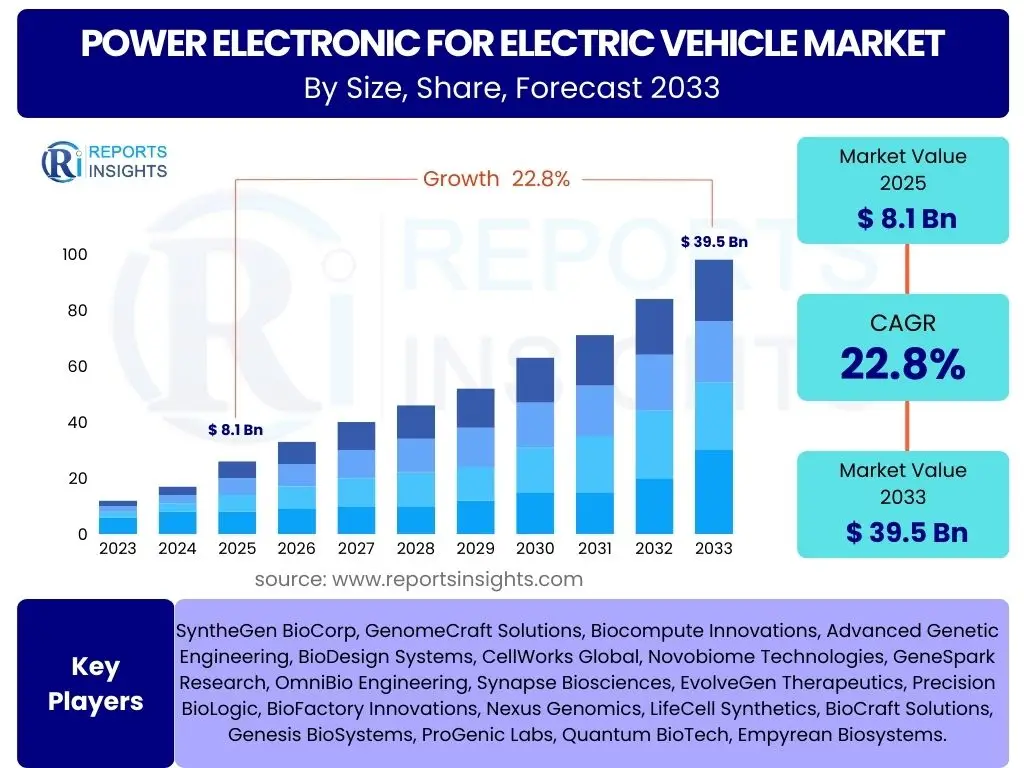

Power Electronic for Electric Vehicle Market Size

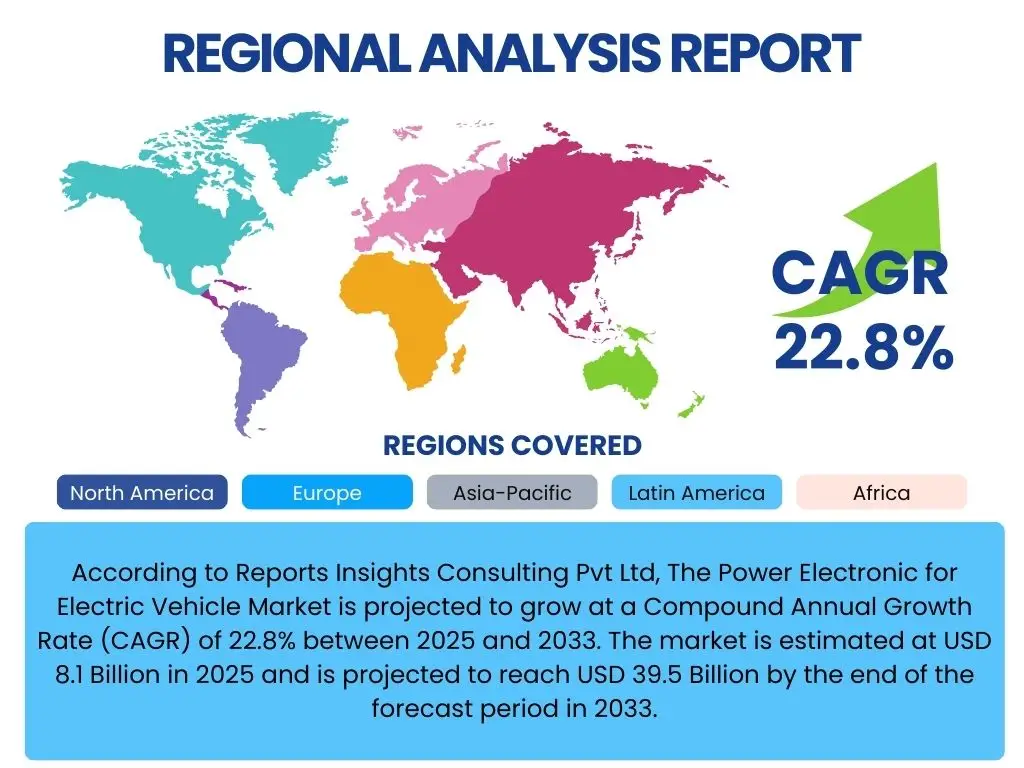

According to Reports Insights Consulting Pvt Ltd, The Power Electronic for Electric Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.8% between 2025 and 2033. The market is estimated at USD 8.1 Billion in 2025 and is projected to reach USD 39.5 Billion by the end of the forecast period in 2033.

Key Power Electronic for Electric Vehicle Market Trends & Insights

The Power Electronic for Electric Vehicle market is witnessing rapid evolution driven by technological advancements and increasing global demand for electric vehicles. Key trends revolve around enhancing efficiency, reducing size and weight, and improving reliability of power conversion systems. The shift towards higher voltage architectures, particularly 800V systems, is a prominent development, enabling faster charging times and optimizing overall vehicle performance. This transition necessitates advanced power semiconductor materials and innovative packaging techniques.

Another significant trend is the increasing adoption of wide bandgap (WBG) semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials offer superior performance characteristics, including higher switching frequencies, reduced energy losses, and better thermal management compared to traditional silicon-based devices. This directly translates to more compact, efficient, and lighter power electronics, which are critical for extending EV range and enhancing power density. Furthermore, there is a growing focus on integrating multiple power electronic components into single modules to simplify system design, reduce manufacturing costs, and further minimize footprint.

- Dominant adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) in inverters and converters.

- Transition towards 800V and higher voltage battery architectures for ultra-fast charging.

- Increased integration of power electronic components (e.g., inverter, DC-DC converter, on-board charger) into multi-functional modules.

- Enhanced focus on advanced thermal management solutions for high-power density systems.

- Development of bi-directional charging capabilities and Vehicle-to-Grid (V2G) technology.

- Miniaturization and weight reduction of power electronic modules.

AI Impact Analysis on Power Electronic for Electric Vehicle

Artificial intelligence is profoundly influencing the design, control, and maintenance of power electronics within electric vehicles, addressing critical areas such as efficiency, reliability, and system optimization. Users are keen to understand how AI can improve the performance and lifespan of these crucial components. AI algorithms are being employed for predictive analytics to monitor the health and performance of power electronic modules, allowing for early detection of potential failures and proactive maintenance, thereby enhancing vehicle reliability and reducing downtime. This extends to optimizing battery management systems (BMS) through intelligent charge and discharge strategies, which can prolong battery life and improve energy utilization.

Furthermore, AI plays a pivotal role in the real-time control of power converters and inverters, enabling adaptive and highly efficient operation under varying driving conditions. This includes advanced control strategies that minimize switching losses and harmonic distortion, thereby maximizing the overall energy efficiency of the powertrain. Users also anticipate AI contributing to the accelerated design and simulation of novel power electronic topologies and materials, leveraging machine learning to explore vast design spaces and identify optimal solutions faster than traditional methods. The integration of AI also promises to enhance cybersecurity measures for connected EV power systems, protecting against potential vulnerabilities.

- Optimization of power converter control algorithms for maximum efficiency and reduced losses.

- Predictive maintenance and fault diagnostics for power electronic components, extending lifespan.

- Enhanced battery management system (BMS) performance through intelligent charging and discharging strategies.

- Accelerated design and simulation of new power electronic topologies and materials using machine learning.

- Real-time thermal management optimization to prevent overheating and ensure component reliability.

- Improvements in manufacturing processes for power electronic modules through AI-driven quality control.

Key Takeaways Power Electronic for Electric Vehicle Market Size & Forecast

The Power Electronic for Electric Vehicle market is poised for exceptional growth, driven by the irreversible global shift towards electric mobility. Key takeaways from the market size and forecast data highlight a consistent and robust expansion across all segments, indicating sustained investment and innovation in the sector. The substantial Compound Annual Growth Rate (CAGR) underscores the critical role power electronics play in enabling the performance, efficiency, and widespread adoption of electric vehicles. Stakeholders should recognize the imperative for continuous technological advancement, particularly in materials science and system integration, to capitalize on this trajectory.

The projected market valuation by 2033 signifies a maturing yet rapidly expanding industry where competition and innovation will intensify. Opportunities abound for companies that can deliver compact, highly efficient, and cost-effective power electronic solutions. Furthermore, the forecast emphasizes the growing demand for solutions that support higher voltage systems and fast-charging capabilities, shaping product development roadmaps. Understanding regional nuances in EV adoption and regulatory landscapes will also be crucial for market participants aiming to maximize their footprint and achieve sustainable growth within this dynamic market.

- The market is on a high-growth trajectory, projected to reach nearly USD 40 Billion by 2033.

- Wide bandgap semiconductors (SiC and GaN) are fundamental to achieving higher efficiency and power density goals.

- Significant investment in R&D for advanced power modules and integrated solutions is critical.

- The increasing adoption of 800V architectures will drive demand for compatible power electronics.

- Regional policies and consumer adoption rates of EVs are primary determinants of market growth.

- Thermal management and reliability remain key challenges and areas for innovation.

Power Electronic for Electric Vehicle Market Drivers Analysis

The growth of the Power Electronic for Electric Vehicle market is significantly propelled by several concurrent factors. Foremost among these is the stringent global environmental regulations aimed at reducing carbon emissions and improving air quality, which directly incentivizes the production and adoption of electric vehicles. Governments worldwide are offering subsidies, tax breaks, and other incentives to both manufacturers and consumers, creating a favorable ecosystem for EV market expansion. This regulatory push, combined with increasing consumer awareness about climate change and the long-term cost benefits of EVs, is fueling unprecedented demand for electric vehicles across various segments.

Furthermore, continuous technological advancements in battery technology, leading to increased energy density and reduced costs, along with significant progress in power semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), are critical market drivers. These material innovations enable the development of more efficient, compact, and lighter power electronic components, directly addressing range anxiety and performance concerns. The expansion of charging infrastructure globally, including fast-charging stations and widespread AC charging points, also serves as a crucial enabler, making EVs more practical and appealing for a broader consumer base.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Adoption of Electric Vehicles | +7.5% | Global, particularly China, Europe, North America | Short-term to Long-term |

| Stringent Government Regulations & Incentives for EVs | +6.0% | Europe, North America, Asia Pacific | Medium-term to Long-term |

| Advancements in Wide Bandgap (WBG) Semiconductor Technology (SiC/GaN) | +5.5% | Global | Short-term to Medium-term |

| Expanding Charging Infrastructure & Energy Storage Solutions | +3.8% | Global | Medium-term |

Power Electronic for Electric Vehicle Market Restraints Analysis

Despite the robust growth, the Power Electronic for Electric Vehicle market faces several significant restraints that could potentially moderate its expansion. One primary concern is the high initial cost associated with advanced power electronic components, especially those utilizing wide bandgap materials like SiC and GaN. While these materials offer superior performance, their manufacturing processes are complex and often result in higher unit costs compared to traditional silicon-based devices. This can contribute to the overall elevated price of electric vehicles, making them less accessible to price-sensitive consumers and potentially slowing mass market adoption, particularly in developing economies.

Another crucial restraint is the volatility and reliability of the global supply chain for key raw materials and specialized components required for power electronics manufacturing. Geopolitical tensions, trade disputes, and natural disasters can disrupt the availability of critical materials such as rare earths, silicon, and specialized packaging components, leading to production delays and increased costs. Furthermore, the complexities associated with thermal management in high-power density applications pose a continuous engineering challenge. Ensuring efficient heat dissipation from compact power electronic modules is vital for their performance and longevity, yet it adds to the design complexity and manufacturing expense, requiring ongoing R&D investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Power Electronic Components | -3.5% | Global, particularly emerging markets | Short-term to Medium-term |

| Supply Chain Volatility and Raw Material Availability | -2.8% | Global | Short-term |

| Complex Thermal Management Challenges in High-Power Density Systems | -2.0% | Global | Medium-term |

| Lack of Standardized Charging Infrastructure in Specific Regions | -1.5% | Latin America, Africa, parts of Asia Pacific | Medium-term |

Power Electronic for Electric Vehicle Market Opportunities Analysis

The Power Electronic for Electric Vehicle market presents numerous compelling opportunities for growth and innovation. One significant area lies in the continued development and widespread adoption of 800V and even higher voltage architectures for electric vehicles. These advanced systems enable ultra-fast charging, reduced cabling weight, and improved overall efficiency, creating a strong demand for power electronic components specifically designed for these high-voltage applications. Companies that can innovate in power modules, inverters, and DC-DC converters compatible with these higher voltages will gain a substantial competitive edge and access to a premium market segment, further enhancing vehicle performance and consumer appeal.

Another substantial opportunity resides in the increasing integration of multiple power electronic functions into single, compact modules. This involves combining components such as inverters, on-board chargers, and DC-DC converters into a single unit, which not only saves space and reduces weight but also simplifies vehicle assembly and lowers manufacturing costs. Furthermore, the emergence of vehicle-to-grid (V2G) and bi-directional charging technologies opens new revenue streams and use cases for EVs, turning them into mobile energy storage units. This requires advanced bi-directional power electronics, creating a specialized market segment with high growth potential, allowing EVs to support grid stability and provide power back to homes or the grid during peak demand or outages.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of 800V and Higher Voltage Architectures | +4.2% | Global, particularly developed EV markets | Medium-term to Long-term |

| Integration of Multiple Power Electronic Functions into Single Modules | +3.7% | Global | Medium-term |

| Expansion of Bi-directional Charging (V2G/V2H) Technologies | +3.0% | Europe, North America, Japan | Medium-term to Long-term |

| Growth in Commercial Electric Vehicle Fleets (Buses, Trucks) | +2.5% | Global, especially China, Europe | Medium-term to Long-term |

Power Electronic for Electric Vehicle Market Challenges Impact Analysis

The Power Electronic for Electric Vehicle market encounters several significant challenges that can impede its growth and complicate market entry for new players. One major challenge is the intense competition among established players and new entrants, which often leads to price pressure on power electronic components. As the market matures, manufacturers are constantly pushed to reduce costs without compromising performance or reliability, necessitating continuous innovation in design and manufacturing processes. This competitive landscape demands significant R&D investment and efficient supply chain management to maintain profitability and market share.

Another critical challenge is the shortage of a skilled workforce with expertise in wide bandgap semiconductor materials and advanced power electronic system integration. The rapid pace of technological change in this field requires specialized engineering talent, which is currently in high demand and short supply. This talent gap can hinder innovation, slow down product development, and increase operational costs. Furthermore, the inherent cybersecurity risks associated with connected electric vehicles and their complex power electronic systems pose a significant challenge. As EVs become more integrated with digital networks, protecting these systems from cyber threats and ensuring data integrity is paramount to maintaining consumer trust and vehicle safety, requiring robust security protocols and continuous updates.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure on Components | -2.2% | Global | Short-term to Medium-term |

| Shortage of Skilled Workforce and Expertise in WBG Technologies | -1.8% | Global | Medium-term |

| Rapid Technological Obsolescence and Need for Continuous Innovation | -1.5% | Global | Short-term to Medium-term |

| Cybersecurity Risks in Connected EV Power Systems | -1.0% | Global | Medium-term to Long-term |

Power Electronic for Electric Vehicle Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Power Electronic for Electric Vehicle market, covering market size, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers detailed segmentation analysis across components, applications, vehicle types, materials, and voltage ranges, alongside a thorough regional assessment. The report also profiles leading industry players, providing insights into their strategies and market positions. It serves as a vital resource for stakeholders seeking to understand market dynamics and make informed strategic decisions in the rapidly evolving EV power electronics landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.1 Billion |

| Market Forecast in 2033 | USD 39.5 Billion |

| Growth Rate | 22.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, STMicroelectronics, ON Semiconductor, NXP Semiconductors, BorgWarner Inc., Continental AG, Robert Bosch GmbH, Denso Corporation, Mitsubishi Electric Corporation, Texas Instruments, Renesas Electronics Corporation, Vishay Intertechnology, Inc., Littelfuse, Inc., ROHM Co., Ltd., Fuji Electric Co., Ltd., Siemens AG, Hitachi Ltd., ABB Ltd., TDK Corporation, Delta Electronics, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Electronic for Electric Vehicle market is comprehensively segmented to provide granular insights into its various facets. This segmentation allows for a detailed understanding of market dynamics across different technologies, applications, vehicle types, and geographical regions. Analyzing these segments helps stakeholders identify specific growth areas, emerging technologies, and target markets, facilitating strategic planning and investment decisions. The various segments collectively paint a complete picture of the market structure and the interdependencies of its components, from raw materials to final vehicle integration.

- By Component: Inverter, Converter (DC-DC Converter, AC-DC Converter), On-Board Charger (OBC), Others (Rectifiers, Controllers)

- By Application: Powertrain (Traction Inverters, Motor Control Units), Charging (On-Board Charging, Off-Board Charging), Auxiliary Systems (HVAC, Power Steering)

- By Vehicle Type: Passenger Electric Vehicle (BEV, PHEV), Commercial Electric Vehicle (Electric Bus, Electric Truck, Electric Van)

- By Material: Silicon (Si), Silicon Carbide (SiC), Gallium Nitride (GaN)

- By Voltage Range: Below 400V, 400V-800V, Above 800V

Regional Highlights

- Asia Pacific (APAC): Dominates the market, primarily driven by China's aggressive EV adoption policies, extensive manufacturing capabilities, and significant investments in electric vehicle infrastructure. India, Japan, and South Korea are also emerging as key growth contributors.

- Europe: Shows strong growth due to stringent emission regulations, substantial government incentives, and a robust consumer shift towards electric mobility, with Germany, Norway, and the UK leading the charge.

- North America: Experiences substantial growth, propelled by increasing consumer demand for EVs, supportive government policies (e.g., IRA in the US), and significant investments in charging infrastructure and EV production facilities.

- Latin America: An emerging market with increasing interest in EVs, though adoption is slower due to economic factors and less developed infrastructure. Brazil and Mexico are key focus countries for future growth.

- Middle East and Africa (MEA): Currently a smaller market, but with growing awareness and nascent government initiatives to promote electric mobility, particularly in the UAE and Saudi Arabia, indicating future potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Electronic for Electric Vehicle Market.- Infineon Technologies AG

- STMicroelectronics

- ON Semiconductor

- NXP Semiconductors

- BorgWarner Inc.

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Mitsubishi Electric Corporation

- Texas Instruments

- Renesas Electronics Corporation

- Vishay Intertechnology, Inc.

- Littelfuse, Inc.

- ROHM Co., Ltd.

- Fuji Electric Co., Ltd.

- Siemens AG

- Hitachi Ltd.

- ABB Ltd.

- TDK Corporation

- Delta Electronics, Inc.

Frequently Asked Questions

What are Power Electronics for Electric Vehicles?

Power electronics for Electric Vehicles (EVs) are crucial components that manage and convert electrical power between various parts of the vehicle, such as the battery, motor, and charging inlet. They include inverters, converters, and on-board chargers, essential for efficient energy flow, motor control, and battery management.

Why are Silicon Carbide (SiC) and Gallium Nitride (GaN) important in EV power electronics?

SiC and GaN are Wide Bandgap (WBG) semiconductors that offer superior performance over traditional silicon. They enable power electronics to operate at higher temperatures and switching frequencies, resulting in greater efficiency, smaller size, reduced weight, and faster charging capabilities for electric vehicles.

How do power electronics contribute to the range and performance of an EV?

By minimizing energy losses during power conversion, efficient power electronics ensure more battery power is delivered to the wheels, thereby extending the EV's driving range. They also enable precise control of the electric motor, contributing to better acceleration and overall vehicle performance.

What role does thermal management play in EV power electronics?

Thermal management is critical for EV power electronics as high power density and efficient operation generate significant heat. Effective cooling prevents overheating, which can degrade component performance and reliability, ensuring the longevity and stable operation of the power electronic modules.

What is the impact of 800V architectures on EV power electronics?

800V architectures in EVs allow for faster charging speeds and improved efficiency by reducing current flow, thus minimizing heat loss and enabling thinner cables. This shift demands power electronics specifically designed to handle higher voltages, driving innovation in compatible components like inverters and DC-DC converters.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted