Power Distribution Unit Market

Power Distribution Unit Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700297 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

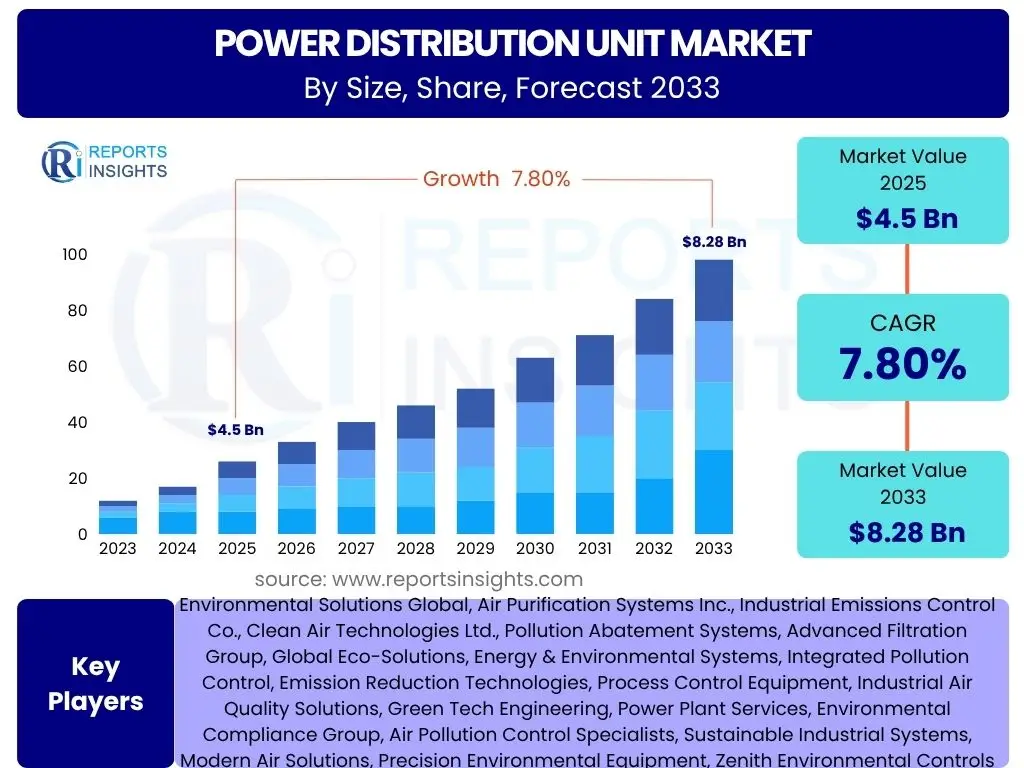

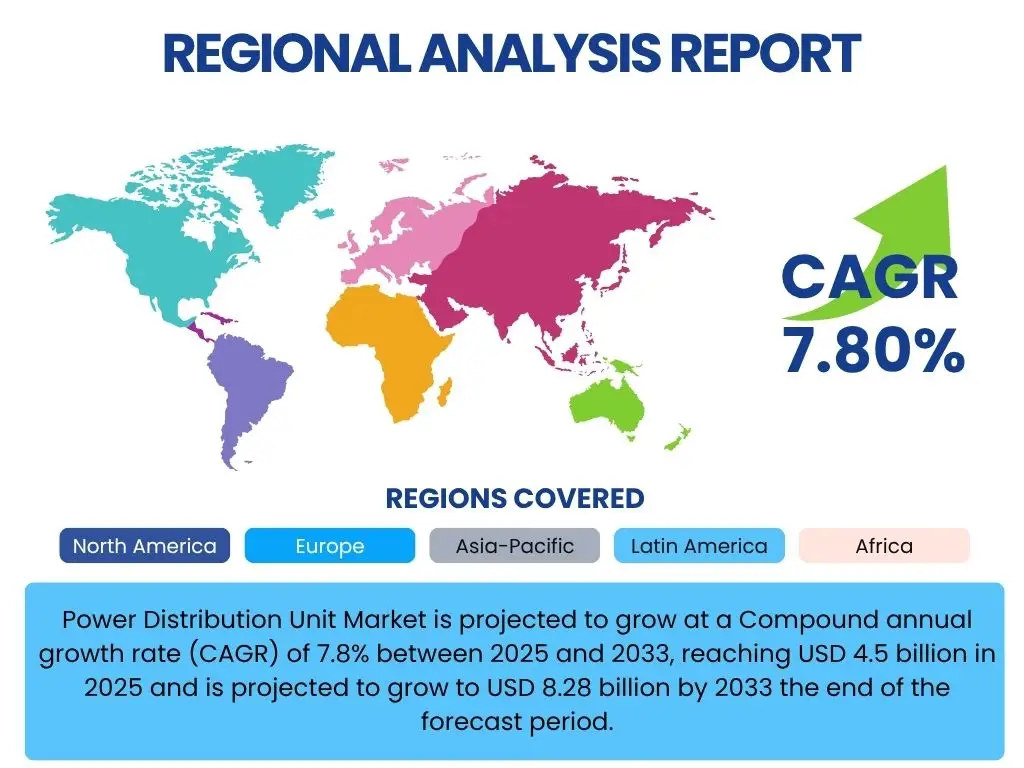

Power Distribution Unit Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, reaching USD 4.5 billion in 2025 and is projected to grow to USD 8.28 billion by 2033 the end of the forecast period.

Key Power Distribution Unit Market Trends & Insights

The Power Distribution Unit (PDU) market is undergoing significant transformation, driven by an accelerating global digital infrastructure and the imperative for enhanced energy efficiency. Emerging trends highlight a shift towards intelligent and network-enabled PDUs that offer advanced monitoring capabilities, alongside a growing demand for higher power densities to support modern data center requirements. The widespread adoption of cloud computing, edge computing, and AI-driven applications is fundamentally reshaping power management strategies, pushing for more flexible, scalable, and resilient power distribution solutions. Furthermore, sustainability initiatives are influencing design, with a focus on energy-efficient components and remote management features to optimize power consumption and reduce operational costs across diverse industries.

- Increasing demand for intelligent and smart PDUs with advanced monitoring.

- Rising adoption of high-density PDUs to support expanding data centers and colocation facilities.

- Growing focus on energy efficiency and sustainability in power infrastructure.

- Proliferation of edge computing and IoT devices necessitating distributed power solutions.

- Integration of advanced analytics for predictive maintenance and optimized power usage.

AI Impact Analysis on Power Distribution Unit

Artificial Intelligence (AI) is profoundly influencing the Power Distribution Unit (PDU) market by enabling more sophisticated and autonomous power management systems. AI-driven analytics enhance the monitoring and control capabilities of PDUs, allowing for real-time insights into power consumption patterns, anomaly detection, and predictive failure analysis. This intelligence facilitates dynamic load balancing, optimizes energy distribution, and significantly improves the overall efficiency and reliability of data centers and critical infrastructure. The integration of AI also supports the development of self-optimizing PDUs that can automatically adjust to changing power demands, minimizing human intervention and preventing potential downtime, thereby transforming conventional power management into a proactive and intelligent operation.

- Enhanced predictive maintenance and fault detection through AI-driven analytics.

- Optimization of power consumption and efficiency via intelligent load balancing.

- Automated power management and dynamic resource allocation in data centers.

- Improved capacity planning and infrastructure utilization based on AI insights.

- Development of self-healing power systems reducing manual intervention.

Key Takeaways Power Distribution Unit Market Size & Forecast

- The global Power Distribution Unit market is poised for robust expansion over the forecast period.

- Projected to reach USD 4.5 billion in 2025, demonstrating strong foundational demand.

- Expected to grow significantly to USD 8.28 billion by 2033, indicating sustained market momentum.

- Anticipated to achieve a Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033.

- Growth is primarily driven by escalating data center investments and digital transformation initiatives.

- Increasing adoption of advanced and intelligent PDUs contributes substantially to market expansion.

Power Distribution Unit Market Drivers Analysis

The Power Distribution Unit (PDU) market is experiencing significant growth propelled by several key drivers that reflect the evolving landscape of digital infrastructure. A primary catalyst is the exponential increase in data generation and processing, necessitating the expansion and modernization of data centers globally. This surge in data demands robust and efficient power management solutions, making PDUs indispensable. Furthermore, the burgeoning adoption of cloud computing services across various industries, coupled with the rapid proliferation of edge computing deployments, is creating new requirements for reliable and scalable power distribution at both centralized and distributed levels. The relentless pursuit of energy efficiency and operational cost reduction by businesses also fuels the demand for advanced PDUs that offer enhanced monitoring, control, and intelligent power optimization capabilities. These factors collectively underscore the critical role of PDUs in supporting the backbone of modern digital operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid expansion of data centers and cloud infrastructure. | +2.5% | Global, particularly North America, Asia Pacific, and Europe. | Long-term (2025-2033) |

| Increasing demand for energy-efficient and intelligent power management solutions. | +2.0% | Global, especially developed economies with stringent energy regulations. | Medium to Long-term |

| Growth of edge computing and IoT devices across industries. | +1.5% | North America, Europe, Asia Pacific (manufacturing, smart cities). | Medium-term |

| Rising adoption of advanced technologies like AI, ML, and big data analytics. | +1.0% | Global, concentrated in tech-driven economies. | Medium to Long-term |

| Digital transformation initiatives across various industry verticals. | +0.8% | Global, particularly emerging economies adopting new digital frameworks. | Medium to Long-term |

Power Distribution Unit Market Restraints Analysis

Despite robust growth drivers, the Power Distribution Unit (PDU) market faces certain restraints that could temper its expansion. One significant challenge is the high initial investment required for deploying advanced and intelligent PDUs, particularly for small and medium-sized enterprises (SMEs) or organizations with limited capital budgets. The complexity of integrating sophisticated PDU systems with existing legacy infrastructure also presents a barrier, often necessitating substantial upgrades and specialized technical expertise. Concerns regarding data security and privacy, especially with network-enabled PDUs that transmit critical operational data, pose another hurdle, as organizations prioritize protecting their sensitive information from cyber threats. Furthermore, the intense price competition among manufacturers, driven by a growing number of market players, can exert downward pressure on profit margins, potentially impacting innovation and market growth. Addressing these restraints will be crucial for unlocking the market's full potential and ensuring broader adoption of advanced PDU solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial deployment costs for advanced PDUs. | -1.2% | Global, more pronounced in developing regions and for SMEs. | Short to Medium-term |

| Complexity of integration with existing legacy IT infrastructure. | -0.8% | Mature markets with extensive legacy systems (e.g., older data centers in Europe, North America). | Medium-term |

| Concerns over data security and privacy for network-enabled PDUs. | -0.7% | Global, particularly in industries handling sensitive data (finance, healthcare). | Medium to Long-term |

| Intense price competition and commoditization of basic PDU models. | -0.5% | Global, affecting profitability across all regions. | Short to Medium-term |

Power Distribution Unit Market Opportunities Analysis

Significant opportunities abound within the Power Distribution Unit (PDU) market, driven by technological advancements and evolving industry needs. The burgeoning demand for smart cities and smart infrastructure initiatives globally presents a substantial avenue for PDU manufacturers, as these complex ecosystems require intelligent and reliable power distribution systems for everything from public utilities to connected devices. The ongoing transition towards 5G technology is another potent opportunity, as it necessitates the deployment of numerous small cells and edge data centers, each requiring efficient and compact PDU solutions. Furthermore, the increasing focus on sustainability and green computing initiatives is propelling the development and adoption of energy-efficient PDUs that contribute to reduced carbon footprints and lower operational costs for organizations. The rising trend of modular data centers, which offer scalability and rapid deployment, also opens doors for specialized PDU solutions designed for flexible, pre-integrated power management. These emerging trends and technological shifts create fertile ground for innovation and market expansion for PDU providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of smart cities and smart infrastructure projects. | +1.8% | Asia Pacific, Middle East, Europe (rapid urbanization and government initiatives). | Long-term |

| Expansion of 5G networks and related edge data center deployments. | +1.5% | Global, especially North America, Asia Pacific, and developed European countries. | Medium to Long-term |

| Increasing adoption of modular and containerized data centers. | +1.2% | Global, appealing to diverse industries requiring rapid deployment. | Medium-term |

| Focus on green computing and demand for eco-friendly power solutions. | +1.0% | Europe, North America (due to strict environmental regulations and corporate mandates). | Medium to Long-term |

Power Distribution Unit Market Challenges Impact Analysis

The Power Distribution Unit (PDU) market faces several critical challenges that demand strategic responses from industry players. The rapid pace of technological change within the data center and IT infrastructure landscape presents a significant challenge, as PDU manufacturers must constantly innovate to keep pace with evolving power demands, connectivity standards, and energy efficiency requirements. Ensuring interoperability between PDUs from different vendors and with existing data center infrastructure can also be a complex issue, leading to integration headaches and potential compatibility problems for end-users. Furthermore, the increasing complexity of modern PDU features, such as advanced monitoring, remote management, and integrated security protocols, necessitates a highly skilled workforce for installation, maintenance, and troubleshooting, which can be a limiting factor in regions facing talent shortages. Finally, stringent regulatory compliance standards related to energy consumption, environmental impact, and safety can impose additional costs and design constraints on manufacturers, requiring continuous adaptation to diverse regional mandates. Successfully navigating these challenges will be vital for sustained growth in the PDU market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid technological obsolescence and need for continuous innovation. | -1.0% | Global, impacting R&D investments and product lifecycle. | Ongoing, Long-term |

| Interoperability issues with diverse IT infrastructure and legacy systems. | -0.9% | Global, particularly for large enterprises with heterogeneous environments. | Medium-term |

| Shortage of skilled professionals for installation and maintenance of advanced PDUs. | -0.8% | Global, more pronounced in rapidly developing or remote regions. | Medium to Long-term |

| Compliance with evolving environmental and safety regulations. | -0.6% | Europe, North America, and increasingly Asia Pacific due to stricter mandates. | Ongoing, Short to Medium-term |

Power Distribution Unit Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Power Distribution Unit market, offering a detailed analysis of its historical performance, current landscape, and future projections. The report provides critical insights into market size, growth drivers, restraints, opportunities, and challenges, enabling stakeholders to make informed strategic decisions. It encompasses a granular segmentation analysis across various parameters, alongside an in-depth regional assessment highlighting key market trends and competitive strategies of leading players. This updated scope ensures a thorough understanding of market evolution and potential growth avenues within the PDU industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 billion |

| Market Forecast in 2033 | USD 8.28 billion |

| Growth Rate | 7.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eaton, Schneider Electric, Vertiv Group, Legrand, Cyber Power Systems, Tripp Lite (Eaton subsidiary), Raritan Inc (Legrand subsidiary), Server Technology (Legrand subsidiary), APC (Schneider Electric subsidiary), Enlogic (Vertiv subsidiary), GE Digital, Hewlett Packard Enterprise, Siemens, ABB, DELTA Electronics, Leviton Manufacturing, Chatsworth Products, Rittal, Belden, Emerson Electric |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Distribution Unit (PDU) market is comprehensively segmented to provide granular insights into its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper understanding of specific product preferences, power requirements across different applications, and the varying demands from end-use industries. By dissecting the market along these critical parameters, the report offers a detailed landscape of market opportunities and competitive positioning for stakeholders seeking to optimize their strategies. Each segment, from the type of PDU to its power phase and application, reveals unique growth trajectories and market characteristics, highlighting key areas for investment and innovation.

The market is primarily segmented by Type, distinguishing between the functionalities offered by different PDU models. This segment provides a crucial understanding of how technology adoption influences market share and growth.

- By Type:

- Basic PDU: Offers fundamental power distribution without monitoring or control capabilities, often used for simple rack power needs.

- Monitored PDU: Provides local or remote monitoring of power consumption at the PDU level, offering insights into overall rack power usage.

- Metered PDU: Features local display or network interface for power metering at the outlet or phase level, enabling more precise energy management.

- Switched PDU: Combines metering with remote outlet switching capabilities, allowing power cycling or individual outlet control for connected devices.

- Intelligent PDU: Represents the most advanced category, integrating monitoring, metering, switching, and often environmental sensors, along with network connectivity and advanced analytics for comprehensive power management.

Segmentation by Power Phase is vital for understanding the capacity and application suitability of PDUs, catering to different scales of IT infrastructure from small server rooms to large data centers.

- By Power Phase:

- Single-Phase: Commonly used for lower power density applications, smaller server racks, and network closets, typically found in SMBs or remote offices.

- Three-Phase: Essential for high-density power requirements in large data centers, enterprise facilities, and industrial environments, providing more efficient power delivery for heavy loads.

The By Power Rating segment highlights the varying power demands across different IT and industrial setups, guiding product development and deployment strategies for manufacturers.

- By Power Rating:

- Less than 10 kVA: Suitable for small to medium-sized racks, edge deployments, and office IT infrastructure where power demands are moderate.

- 10 kVA to 25 kVA: Represents a mid-range capacity, often utilized in growing enterprise data centers and colocation facilities requiring robust yet flexible power delivery.

- More than 25 kVA: Designed for hyperscale data centers, large industrial applications, and environments with very high-density computing needs, ensuring massive power distribution capabilities.

Application-based segmentation provides clarity on the primary end-uses of PDUs, revealing the market's reliance on sectors like data centers and telecommunications due to their critical power infrastructure needs. The breakdown within data centers further refines understanding of specific power management requirements.

- By Application:

- Data Centers:

- Enterprise Data Centers: Privately owned and operated data centers supporting an organization's internal IT operations.

- Colocation Data Centers: Facilities where businesses can rent space for their servers and other computing hardware.

- Hyperscale Data Centers: Massive data centers designed to support cloud computing and big data operations for large technology companies.

- Industrial Applications: Includes power distribution in manufacturing plants, heavy industries, and automation facilities requiring robust and reliable power solutions.

- Commercial Buildings: Covers power management in office complexes, retail spaces, educational institutions, and healthcare facilities for their IT and general power needs.

- Telecommunication and IT: Encompasses infrastructure for telecom networks, internet service providers, and general IT services beyond dedicated data centers.

- Other Applications: Includes niche applications such as broadcast studios, laboratories, and specialized research facilities.

Finally, the segmentation by End-Use Industry offers insights into the vertical markets driving PDU adoption, showcasing diversified demand from sectors ranging from finance to manufacturing, each with unique power reliability and efficiency requirements.

- By End-Use Industry:

- BFSI (Banking, Financial Services, and Insurance): Demands high reliability and uptime for critical financial transactions and data.

- Healthcare: Requires stable and redundant power for medical equipment, patient data, and operational systems.

- Manufacturing: Utilizes PDUs for automation, control systems, and machinery in production environments.

- Energy & Utilities: Essential for managing power infrastructure in power plants, smart grids, and utility distribution networks.

- Government & Public Sector: Supports IT infrastructure for public services, defense, and administrative functions.

- Retail & Consumer Goods: Powers POS systems, inventory management, and digital signage in retail environments.

- Media & Entertainment: Critical for broadcasting, streaming, content creation, and data storage for media assets.

- IT & Telecommunications: The core user of PDUs, supporting vast networks, servers, and communication equipment.

- Others: Includes sectors like transportation, logistics, education, and hospitality, requiring diverse PDU solutions.

Regional Highlights

The global Power Distribution Unit (PDU) market exhibits distinct regional dynamics, with certain geographies leading in adoption and technological advancements due to concentrated digital infrastructure investments, regulatory frameworks, and economic growth. Understanding these regional nuances is crucial for strategic market penetration and investment decisions. Each major region contributes uniquely to the market's overall trajectory, influenced by factors such as data center proliferation, smart city initiatives, and the pace of digital transformation across industries.

-

North America: This region stands as a dominant force in the PDU market, primarily driven by the presence of numerous hyperscale data centers, a robust cloud computing ecosystem, and significant investments in edge computing infrastructure. The United States, in particular, leads in terms of technological adoption and the expansion of digital services, necessitating advanced, high-density, and intelligent PDUs. Canada also contributes to regional growth with its expanding IT sector and focus on energy efficiency. The early adoption of smart PDU technologies and the continuous upgrade of existing data center infrastructure to meet escalating power demands are key factors that make North America a critical market.

-

Europe: Europe represents another significant market for PDUs, characterized by strong regulatory emphasis on energy efficiency and sustainability. Countries like Germany, the UK, France, and the Netherlands are at the forefront of data center development, driven by strict data localization laws and increasing cloud adoption. The region is witnessing a surge in modular and green data center deployments, fostering demand for eco-friendly and intelligent PDU solutions. Government initiatives supporting digital transformation and a mature IT infrastructure further bolster the market in this region, with a growing focus on secure and reliable power distribution.

-

Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the PDU market, fueled by rapid digitalization, massive data generation, and booming internet penetration, particularly in emerging economies like China, India, and Southeast Asian countries. The region is experiencing unprecedented data center construction, driven by expanding cloud services, e-commerce, and gaming industries. Government support for digital infrastructure projects and the rising number of smart city initiatives are also significant contributors. Japan, South Korea, and Australia represent mature markets with advanced infrastructure, while emerging economies present substantial opportunities for new PDU deployments and technological upgrades.

-

Latin America: This region is demonstrating steady growth in the PDU market, primarily influenced by increasing internet penetration, growing demand for cloud services, and foreign investments in digital infrastructure. Countries like Brazil and Mexico are leading the charge in data center development and digital transformation across various sectors. While the market is still developing compared to other regions, the rising adoption of IoT and edge computing, coupled with government efforts to improve digital connectivity, suggests promising opportunities for PDU manufacturers seeking to establish a foothold.

-

Middle East and Africa (MEA): The MEA region is emerging as a dynamic market for PDUs, driven by ambitious government-led digital transformation agendas, diversification of economies away from oil, and significant investments in smart city projects (e.g., in Saudi Arabia and UAE). The construction of new data centers and the expansion of telecommunications infrastructure are key growth catalysts. While the African continent is relatively nascent, increasing urbanization and connectivity initiatives are creating demand for reliable power solutions, making MEA an increasingly important region for PDU market expansion, especially with a focus on resilient and efficient power management systems.

Top Key Players:

The market research report covers the analysis of key stake holders of the Power Distribution Unit Market. Some of the leading players profiled in the report include -:- Eaton

- Schneider Electric

- Vertiv Group

- Legrand

- Cyber Power Systems

- Tripp Lite (Eaton subsidiary)

- Raritan Inc (Legrand subsidiary)

- Server Technology (Legrand subsidiary)

- APC (Schneider Electric subsidiary)

- Enlogic (Vertiv subsidiary)

- GE Digital

- Hewlett Packard Enterprise

- Siemens

- ABB

- DELTA Electronics

- Leviton Manufacturing

- Chatsworth Products

- Rittal

- Belden

- Emerson Electric

Frequently Asked Questions:

What is a Power Distribution Unit (PDU) and why is it important?

A Power Distribution Unit (PDU) is a device equipped with multiple outlets designed to distribute electric power to computers, servers, networking hardware, and other IT equipment within a rack or cabinet. Its importance lies in providing reliable, organized, and often monitored power to critical infrastructure, preventing overloads, and facilitating efficient power management, thereby ensuring uptime and operational continuity for data centers and IT environments.

What are the different types of PDUs available in the market?

The PDU market offers various types tailored to different needs. Basic PDUs provide fundamental power distribution. Monitored PDUs allow for local or remote power consumption tracking. Metered PDUs offer more granular power data at the outlet or phase level. Switched PDUs add remote control capabilities for individual outlets, enabling power cycling. Intelligent PDUs combine monitoring, metering, and switching with advanced features like environmental sensing and network connectivity for comprehensive power management and automation.

How does the growth of data centers influence the PDU market?

The rapid expansion of data centers globally is a primary driver for the PDU market. As data centers scale up to meet increasing demands for cloud computing, AI, and big data, there's a corresponding need for more efficient, high-density, and intelligent power distribution solutions. Each new server rack and IT deployment requires robust PDUs to ensure reliable power delivery, optimize energy consumption, and manage growing power loads, directly fueling market growth and innovation in PDU technology.

What role does energy efficiency play in the PDU market?

Energy efficiency is a pivotal factor shaping the PDU market, driven by rising energy costs and growing environmental concerns. Modern PDUs are designed to minimize power loss, offering features like individual outlet metering, real-time power monitoring, and remote management to identify and reduce wasted energy. This focus helps organizations lower operational expenditures, reduce their carbon footprint, and comply with energy efficiency regulations, making energy-efficient PDUs a key differentiator and a significant market trend.

What are the key opportunities for innovation in the Power Distribution Unit market?

Key opportunities for innovation in the PDU market include the integration of artificial intelligence and machine learning for predictive analytics and autonomous power management, enhancing remote monitoring and control capabilities for edge computing deployments, and developing more compact and higher-density units to support increasing rack power requirements. Furthermore, advancements in cybersecurity features for networked PDUs and the development of more sustainable, eco-friendly designs that contribute to green computing initiatives present significant avenues for future growth and product differentiation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted