Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702119 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Size

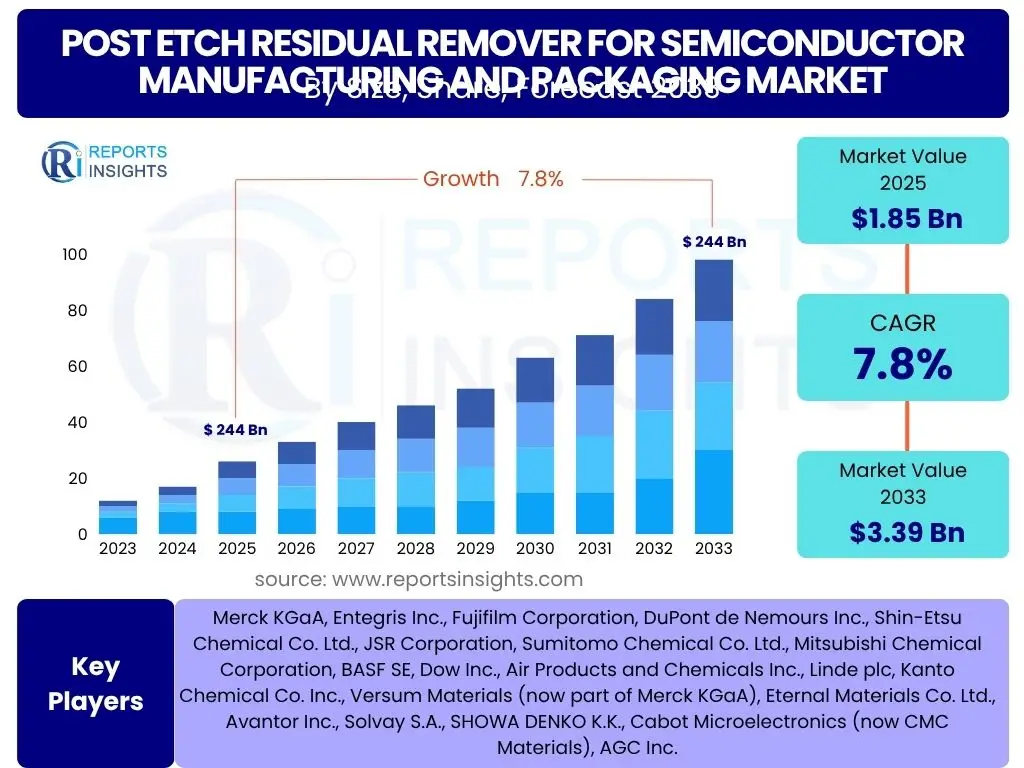

According to Reports Insights Consulting Pvt Ltd, The Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.39 Billion by the end of the forecast period in 2033.

Key Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Trends & Insights

The semiconductor industry's relentless pursuit of miniaturization and increased device complexity is a primary driver shaping the market for post etch residual removers. Advancements in fabrication processes, such as the transition to Gate-All-Around (GAA) architectures and 3D stacking technologies, necessitate highly selective and efficient cleaning solutions. This trend drives innovation towards novel chemistries that can remove microscopic residues without damaging sensitive underlying structures or compromising material integrity, ensuring optimal device performance and yield. Furthermore, there is a growing emphasis on environmentally friendly formulations, pushing manufacturers to develop safer, less toxic, and more sustainable post etch removal solutions.

Another significant trend is the expansion of advanced packaging techniques, including fan-out wafer-level packaging (FOWLP) and 3D integration. These packaging methods introduce new challenges for residue removal, requiring specialized solutions that can handle diverse materials and complex interconnections. The integration of artificial intelligence and machine learning in process control and materials development is also emerging, enabling more precise application and optimization of these critical chemicals. The increasing demand for high-performance computing, artificial intelligence accelerators, 5G infrastructure, and automotive electronics further fuels the need for high-quality semiconductor components, thereby stimulating growth in the residual remover market.

- Miniaturization and advanced node adoption (e.g., 5nm, 3nm, 2nm) driving demand for highly selective removers.

- Increased complexity of 3D architectures (FinFET, GAAFET) necessitating specialized cleaning.

- Growth in advanced packaging technologies (e.g., 3D IC, FOWLP) expanding application scope.

- Development of eco-friendly and sustainable chemical formulations.

- Integration of automation and AI for process optimization and quality control.

- Shift towards dry or vapor-phase cleaning methods for reduced chemical consumption.

- Supply chain resilience and localized manufacturing initiatives impacting regional market dynamics.

AI Impact Analysis on Post Etch Residual Remover for Semiconductor Manufacturing and Packaging

Users frequently inquire about how artificial intelligence (AI) is transforming the post etch residual remover market, particularly regarding process efficiency, material innovation, and quality control. There is a strong interest in AI's capability to optimize chemical formulations, predict material interactions, and enhance manufacturing yields. Concerns often revolve around the practical implementation challenges, data requirements, and the specific types of AI applications that offer the most significant benefits in a highly precise and sensitive manufacturing environment. Users seek to understand if AI can genuinely lead to more sustainable and cost-effective solutions while maintaining or improving product quality in semiconductor fabrication.

AI's influence in the post etch residual remover market is primarily manifested through enhanced process optimization, predictive analytics, and accelerated materials discovery. AI algorithms can analyze vast datasets from fabrication processes, identifying optimal chemical concentrations, temperatures, and exposure times for residue removal, thereby minimizing material waste and improving throughput. Predictive maintenance models, powered by AI, can anticipate equipment failures or process deviations that might lead to incomplete residue removal, allowing for proactive adjustments and reducing costly reworks. Furthermore, AI and machine learning are being utilized to simulate molecular interactions and predict the performance of new chemical formulations, significantly shortening the research and development cycles for next-generation removers. This accelerates the introduction of more effective and environmentally compliant solutions to meet the evolving demands of advanced semiconductor manufacturing. The integration of AI also supports real-time quality control, ensuring consistent and precise removal, which is critical for achieving high yields in complex chip designs.

- Process Optimization: AI algorithms refine removal parameters (e.g., time, temperature, concentration) for optimal efficacy and yield.

- Materials Discovery: AI accelerates the identification and development of new, more selective, and eco-friendly chemical formulations.

- Predictive Analytics: AI models predict residue formation patterns and potential removal issues, enabling proactive adjustments.

- Quality Control: AI-driven vision systems and data analysis enhance real-time inspection and defect detection.

- Automation & Robotics: AI integration enables intelligent automation of cleaning steps, reducing human error and contamination.

- Resource Efficiency: AI helps optimize chemical usage, water consumption, and waste management in cleaning processes.

Key Takeaways Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Size & Forecast

Common user questions regarding key takeaways from the Post Etch Residual Remover market forecast frequently center on the underlying factors driving projected growth, the most impactful technological shifts, and the critical success factors for market participants. There is significant interest in understanding how macroeconomic trends and specific industry developments, such as advancements in chip architecture and packaging, are translating into tangible market opportunities. Users also seek clarity on the competitive landscape and the strategic imperatives for companies operating within this specialized segment of the semiconductor supply chain, particularly concerning innovation and sustainability.

The Post Etch Residual Remover market is poised for robust growth, driven primarily by the escalating demand for advanced semiconductors across various end-use applications, including artificial intelligence, 5G, IoT, and high-performance computing. The continuous push for device miniaturization and the adoption of complex 3D architectures necessitate highly sophisticated and selective removal chemistries, creating a sustained demand for innovative solutions. Furthermore, the industry's increasing focus on environmental sustainability and workplace safety is compelling manufacturers to invest in developing and implementing greener chemical formulations. This dual pressure of technological advancement and environmental responsibility defines the strategic direction for market players, emphasizing R&D in novel materials and process optimization. The market's future trajectory is deeply intertwined with the overall health and technological progression of the global semiconductor industry, making it a critical enabling segment for next-generation electronic devices.

- The market is experiencing substantial growth, fueled by global semiconductor demand and technological advancements.

- Miniaturization and complex 3D chip designs are primary drivers for specialized residual removers.

- Sustainability and eco-friendly solutions are becoming critical differentiating factors.

- Significant investment in R&D for novel chemical formulations and process optimization is essential for market leadership.

- Advanced packaging technologies present new and expanding application areas for residual removers.

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Drivers Analysis

The relentless pursuit of Moore's Law, characterized by the continuous miniaturization of semiconductor devices and the increasing density of transistors on a chip, is a fundamental driver for the post etch residual remover market. As feature sizes shrink to nanoscale dimensions (e.g., 5nm, 3nm), the precision and selectivity required for removing post-etch residues become paramount. These ultra-small geometries are highly susceptible to defects caused by even minute contaminants, necessitating highly advanced and effective cleaning chemistries that can remove complex inorganic and organic residues without damaging the delicate device structures. This technological imperative drives chemical suppliers to innovate constantly, developing new formulations capable of meeting the stringent demands of advanced manufacturing nodes.

Furthermore, the escalating global demand for electronic devices across diverse sectors, including consumer electronics, automotive, telecommunications (5G), and artificial intelligence, directly translates into increased semiconductor production. This heightened production volume inherently increases the consumption of essential fabrication materials, including post etch residual removers. The rapid expansion of emerging technologies that rely on high-performance semiconductors, such as AI processors, IoT devices, and advanced driver-assistance systems (ADAS), further amplifies this demand. Additionally, the shift towards more complex chip architectures, such as Gate-All-Around (GAA) FETs and 3D NAND flash, introduces new challenges for residue removal, requiring specialized solutions that can clean intricate geometries and multi-layered structures, thus driving innovation and market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization & Advanced Node Adoption | +1.8% | Global, particularly APAC (Korea, Taiwan) & North America | Short to Long Term (2025-2033) |

| Growth in Semiconductor Manufacturing & Device Demand | +1.5% | Global, especially China, Taiwan, South Korea, US | Short to Long Term (2025-2033) | Increasing Complexity of Chip Architectures (3D IC, GAA) | +1.2% | Global, focused on advanced manufacturing regions | Medium to Long Term (2027-2033) |

| Rising Adoption of Advanced Packaging Technologies | +1.0% | APAC (China, Taiwan, South Korea), North America | Medium to Long Term (2026-2033) |

| Strict Quality & Yield Requirements in Fabs | +0.8% | Global | Short to Long Term (2025-2033) |

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Restraints Analysis

The significant research and development (R&D) costs associated with developing new and highly specialized post etch residual removers pose a considerable restraint on market growth. As semiconductor technology advances, the demand for more selective, effective, and environmentally compliant cleaning solutions intensifies. Developing these advanced chemistries requires extensive laboratory research, costly material sourcing, and rigorous testing to ensure compatibility with new materials and processes, such as low-k dielectrics or novel interconnects. This high R&D expenditure translates into higher product costs, which can be a barrier for adoption, particularly for manufacturers operating on thinner margins or those in less advanced technological nodes. The time-consuming nature of regulatory approvals and qualification processes also adds to the cost and complexity, slowing down market entry for innovative solutions.

Another critical restraint is the increasingly stringent environmental regulations and safety concerns associated with chemical handling and disposal. Many traditional post etch removers contain hazardous or toxic components that pose risks to both human health and the environment. Governments and regulatory bodies worldwide are imposing stricter rules on the use, storage, and disposal of such chemicals, compelling manufacturers to invest heavily in compliance, waste treatment facilities, and the development of greener alternatives. While this drives innovation towards more sustainable solutions, the transition can be slow and expensive, requiring significant capital investment and process re-engineering. Furthermore, supply chain vulnerabilities, including geopolitical tensions, raw material price volatility, and logistical challenges, can disrupt the availability and increase the cost of key chemical ingredients, thereby impacting the production and pricing of residual removers and potentially hindering market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Qualification Costs | -0.9% | Global | Short to Long Term (2025-2033) |

| Stringent Environmental Regulations & Safety Concerns | -0.8% | Europe, North America, parts of Asia | Short to Long Term (2025-2033) |

| Intellectual Property & Proprietary Formulations | -0.5% | Global | Medium to Long Term (2026-2033) |

| Supply Chain Disruptions and Raw Material Volatility | -0.7% | Global | Short to Medium Term (2025-2028) |

| Cyclical Nature of the Semiconductor Industry | -0.6% | Global | Short to Medium Term (2025-2028) |

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Opportunities Analysis

The growing emphasis on environmental sustainability within the semiconductor industry presents a significant opportunity for the development and adoption of eco-friendly post etch residual removers. As manufacturers face increasing pressure from regulatory bodies and consumers to reduce their environmental footprint, there is a strong demand for solutions that are less hazardous, biodegradable, and recyclable. This drives innovation in green chemistry, leading to the creation of novel formulations that minimize the use of volatile organic compounds (VOCs), reduce water consumption, and generate less toxic waste. Companies that invest in and successfully commercialize these sustainable solutions can gain a competitive advantage, attracting environmentally conscious customers and potentially benefiting from governmental incentives or a more favorable regulatory landscape. The shift towards sustainable manufacturing practices is a long-term trend offering substantial growth prospects.

The continuous evolution of semiconductor device architectures, including advanced logic and memory chips, 3D integrated circuits (3D ICs), and Gate-All-Around (GAA) structures, creates new and complex cleaning challenges that current solutions may not adequately address. This technological advancement presents a substantial opportunity for chemical suppliers to innovate and develop highly specialized post etch removers tailored to these next-generation designs. These new removers must exhibit exceptional selectivity, compatibility with novel materials (e.g., high-k dielectrics, advanced metals), and superior residue removal capabilities for intricate geometries. Furthermore, the expansion of the semiconductor industry into emerging markets and applications such as artificial intelligence, quantum computing, and advanced automotive electronics also opens new avenues for demand. Strategic partnerships between chemical suppliers, equipment manufacturers, and chipmakers can accelerate the development and adoption of these advanced cleaning solutions, unlocking significant market potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-Friendly & Sustainable Solutions | +1.5% | Global, particularly Europe, North America, East Asia | Medium to Long Term (2026-2033) |

| Innovation for Next-Gen Device Architectures (GAA, 3D IC) | +1.3% | Global, focused on advanced fabs | Short to Long Term (2025-2033) |

| Expansion into Emerging Semiconductor Applications (AI, IoT, Automotive) | +1.1% | Global | Short to Long Term (2025-2033) |

| Strategic Partnerships & Collaborations | +0.9% | Global | Medium Term (2026-2030) |

| Growth in Specialty Materials & Advanced Packaging | +0.7% | APAC, North America | Short to Long Term (2025-2033) |

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market Challenges Impact Analysis

A significant challenge in the post etch residual remover market is achieving optimal selectivity without damaging critical device layers. As semiconductor designs become more intricate and integrate a wider array of materials, the post etch cleaning process must precisely remove unwanted residues while preserving the integrity of underlying and adjacent sensitive materials, such as low-k dielectrics or delicate metallic interconnects. Any unintentional etching or damage to these critical layers can lead to device failure, reduced yield, and significant manufacturing losses. Developing chemical formulations that can differentiate between various materials at the nanoscale level and selectively remove only the residues, without compromising the device's functional components, demands immense R&D effort and poses a continuous technical hurdle for chemical suppliers. This challenge becomes even more pronounced with the introduction of novel materials and complex 3D structures.

Another substantial challenge is the rapid pace of technological change and the associated need for continuous innovation. The semiconductor industry is characterized by fast-evolving process technologies and new device architectures that quickly render existing chemical solutions obsolete. This necessitates a continuous and rapid development cycle for post etch removers, requiring significant investment in R&D, advanced analytical tools, and expert personnel. Chemical suppliers must anticipate future material requirements and process flows, collaborating closely with chip manufacturers to develop and qualify new solutions in parallel with device advancements. Furthermore, managing the cost-performance trade-off is a perpetual challenge; while chipmakers demand highly effective and selective removers, they also seek cost-efficient solutions. Balancing superior cleaning performance with competitive pricing, especially for high-volume manufacturing, remains a critical hurdle for market participants, impacting adoption rates and market penetration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving High Selectivity & Preventing Material Damage | -1.2% | Global | Short to Long Term (2025-2033) |

| Rapid Technological Obsolescence & Need for Innovation | -1.0% | Global | Short to Long Term (2025-2033) |

| Balancing Performance with Cost-Effectiveness | -0.8% | Global | Short to Long Term (2025-2033) |

| Waste Management & Recycling Complexities | -0.7% | Europe, North America, East Asia | Medium to Long Term (2026-2033) |

| Intensifying Competition & Market Fragmentation | -0.6% | Global | Short to Medium Term (2025-2028) |

Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market - Updated Report Scope

This report offers an in-depth analysis of the global Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market, providing comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It covers historical data from 2019 to 2023, with a forecast extending from 2025 to 2033, enabling a thorough understanding of market dynamics and future projections. The report details market segmentation by type, application, and end-use industry, along with a granular regional analysis. It also profiles leading companies, highlighting their competitive strategies and product portfolios, to offer a complete market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.39 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Merck KGaA, Entegris Inc., Fujifilm Corporation, DuPont de Nemours Inc., Shin-Etsu Chemical Co. Ltd., JSR Corporation, Sumitomo Chemical Co. Ltd., Mitsubishi Chemical Corporation, BASF SE, Dow Inc., Air Products and Chemicals Inc., Linde plc, Kanto Chemical Co. Inc., Versum Materials (now part of Merck KGaA), Eternal Materials Co. Ltd., Avantor Inc., Solvay S.A., SHOWA DENKO K.K., Cabot Microelectronics (now CMC Materials), AGC Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of market dynamics across different chemical compositions, physical forms, and crucial application areas within the semiconductor fabrication process, as well as distinct end-use industries. Each segment reflects unique technological requirements and market trends, influencing the demand for specific types of residual removers and highlighting areas of high growth or particular innovation. Understanding these segments is vital for stakeholders to identify niche opportunities and tailor their product development and marketing strategies effectively.

- By Chemistry:

- Organic Solvent-based: Traditionally used, offering good solvency for various residues.

- Inorganic Acid/Alkaline-based: Effective for specific inorganic residues, often highly corrosive.

- Fluorine-based: Utilized for silicon-containing residues, particularly in advanced nodes.

- Other Chemistries: Includes novel formulations, often eco-friendlier or highly specialized.

- By Type:

- Liquid Removers: Dominant form, applied through wet chemical processes.

- Dry/Plasma Removers: Gaining traction for reduced chemical usage and precise etching.

- By Application:

- Front-End-of-Line (FEOL): Critical for transistor formation, involves complex residue removal.

- Back-End-of-Line (BEOL): Focuses on interconnects, requiring removers compatible with various metals and dielectrics.

- Advanced Packaging: Solutions for wafer-level packaging, 3D ICs, and other advanced integration schemes.

- By End-Use Industry:

- Logic Devices: Processors, microcontrollers, and other computational chips.

- Memory Devices: DRAM, NAND flash, and emerging memory technologies.

- Power Devices: Components for power management and conversion.

- MEMS: Micro-electro-mechanical systems for sensors and actuators.

- Optoelectronics: Devices related to light emission or detection.

- Others: Includes discrete components, analog ICs, etc.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to the concentration of major semiconductor manufacturing hubs (Taiwan, South Korea, China, Japan). Continuous investments in new fabs and advanced technology nodes drive significant demand for post etch residual removers. The region is at the forefront of semiconductor innovation and production capacity.

- North America: A key region for semiconductor research and development, and advanced manufacturing. Home to leading chip designers and a growing number of new fab investments (e.g., in Arizona, Texas), driving demand for high-performance and specialized chemical solutions. Strong emphasis on sustainable manufacturing practices.

- Europe: A significant market driven by strong automotive, industrial, and power electronics sectors. Initiatives like the European Chips Act aim to boost domestic semiconductor manufacturing, which will increase the demand for specialized chemicals, including post etch residual removers. Focus on environmental regulations shapes product development.

- Latin America & Middle East and Africa (MEA): Currently smaller markets, but with emerging opportunities as regional digitalization and industrialization efforts progress. Potential for growth exists with future investments in local semiconductor assembly, test, and potentially fabrication facilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Post Etch Residual Remover for Semiconductor Manufacturing and Packaging Market.- Merck KGaA

- Entegris Inc.

- Fujifilm Corporation

- DuPont de Nemours Inc.

- Shin-Etsu Chemical Co. Ltd.

- JSR Corporation

- Sumitomo Chemical Co. Ltd.

- Mitsubishi Chemical Corporation

- BASF SE

- Dow Inc.

- Air Products and Chemicals Inc.

- Linde plc

- Kanto Chemical Co. Inc.

- Versum Materials (now part of Merck KGaA)

- Eternal Materials Co. Ltd.

- Avantor Inc.

- Solvay S.A.

- SHOWA DENKO K.K.

- Cabot Microelectronics (now CMC Materials)

- AGC Inc.

Frequently Asked Questions

What is a post etch residual remover in semiconductor manufacturing?

A post etch residual remover is a specialized chemical solution used in semiconductor fabrication to clean microscopic residues left on a wafer surface after the plasma or wet etching process. These residues, typically polymeric, organic, or inorganic materials, must be completely removed to prevent defects, ensure proper electrical conductivity, and maintain device performance and yield for advanced integrated circuits.

What are the primary types of post etch residual removers available?

Post etch residual removers are primarily categorized by their chemistry (e.g., organic solvent-based, inorganic acid/alkaline-based, fluorine-based) and physical form (liquid or dry/plasma-based). Each type is designed to target specific residue compositions and be compatible with various semiconductor materials and process flows.

How do advanced chip architectures impact the demand for these removers?

Advanced chip architectures like FinFETs, Gate-All-Around (GAA) structures, and 3D ICs introduce complex, high-aspect-ratio geometries and novel material stacks. This complexity increases the challenge of residue removal, demanding highly selective and efficient removers that can clean intricate patterns without damaging delicate structures, thereby driving demand for innovative solutions.

What role does sustainability play in the post etch residual remover market?

Sustainability is increasingly vital, driving the development of eco-friendly and safer formulations. Manufacturers are seeking removers with reduced hazardous chemicals, lower VOC emissions, improved biodegradability, and enhanced recyclability to meet stringent environmental regulations and corporate sustainability goals, fostering green chemistry innovation.

Which regions are key players in the post etch residual remover market?

Asia Pacific (APAC), particularly Taiwan, South Korea, China, and Japan, is the dominant region due to its extensive semiconductor manufacturing capacity. North America and Europe are also significant players, driven by advanced R&D, high-end fabrication, and strategic investments in domestic chip production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted