Polyphenylene Ether Market

Polyphenylene Ether Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706758 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

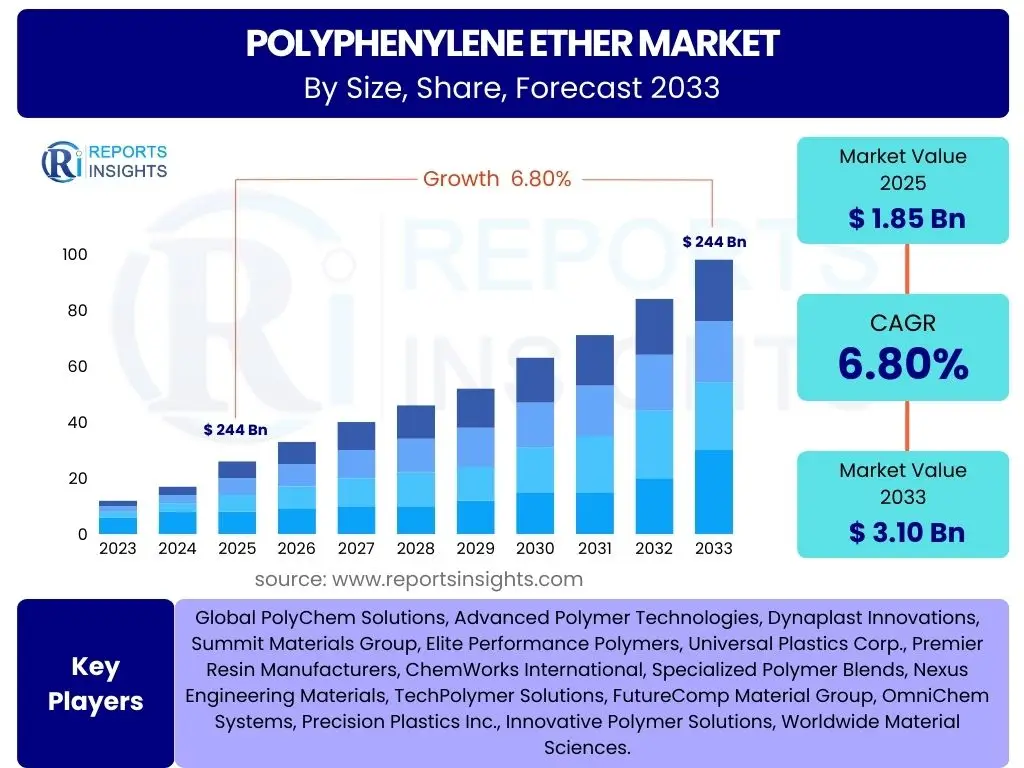

Polyphenylene Ether Market Size

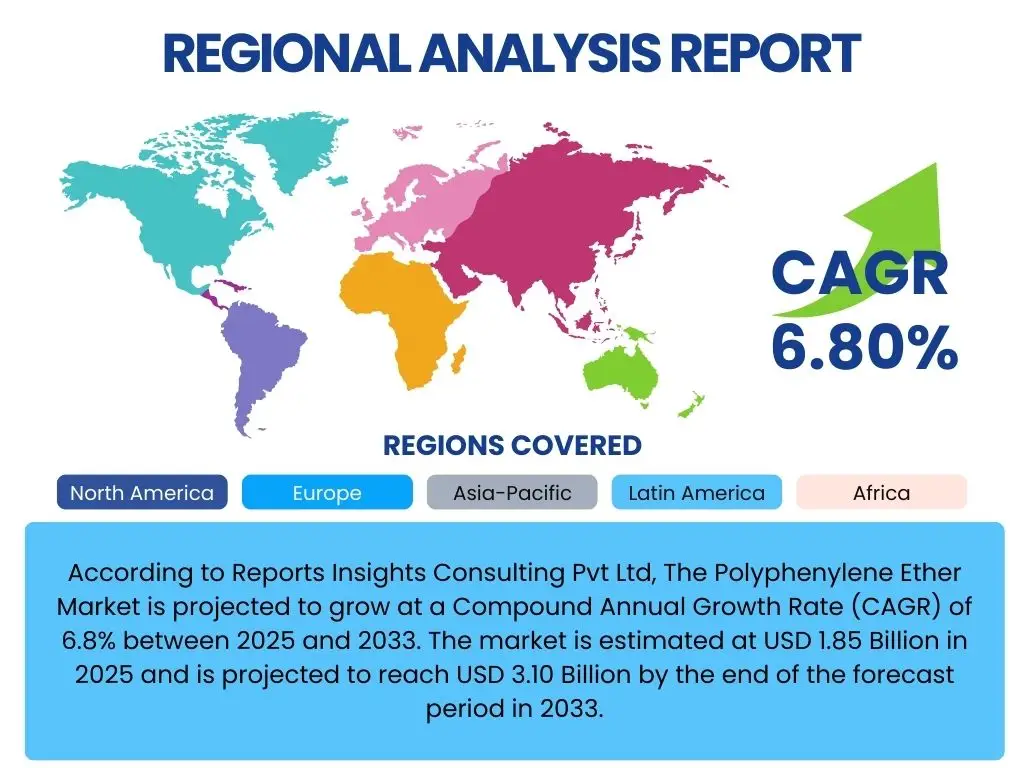

According to Reports Insights Consulting Pvt Ltd, The Polyphenylene Ether Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.10 Billion by the end of the forecast period in 2033.

Key Polyphenylene Ether Market Trends & Insights

The Polyphenylene Ether (PPE) market is experiencing dynamic shifts driven by advancements in material science and evolving industrial demands. Users frequently inquire about the trajectory of high-performance plastics, especially those offering a unique combination of thermal stability, mechanical strength, and dielectric properties. There is a keen interest in how PPE adapts to the burgeoning needs of electric vehicles, miniaturized electronics, and sustainable manufacturing practices, reflecting a broader industry push towards efficiency and environmental responsibility.

Key discussions revolve around the adoption of PPE blends in lightweighting initiatives within the automotive sector, driven by stringent emission regulations and the rapid expansion of electric vehicle production. Furthermore, the robust demand for superior dielectric materials in 5G communication infrastructure and advanced electronic components is significantly influencing PPE market trends. Innovators are also exploring novel processing techniques and compounding methods to enhance PPE's properties and expand its application versatility.

- Growing adoption in electric and hybrid vehicles for lightweighting and thermal management.

- Increased demand from the electronics sector for miniaturization and high-frequency applications, particularly in 5G technology.

- Shift towards sustainable and recyclable PPE grades and blends.

- Expansion into new medical device applications due to excellent sterilizability and biocompatibility.

- Development of specialized PPE compounds for additive manufacturing (3D printing).

AI Impact Analysis on Polyphenylene Ether

User inquiries concerning artificial intelligence's influence on the Polyphenylene Ether market often center on its potential to revolutionize material discovery, optimize manufacturing processes, and enhance supply chain efficiencies. Stakeholders are particularly interested in how AI can accelerate the development of new PPE formulations with tailored properties, addressing specific performance requirements in demanding applications such as high-temperature environments or specialized electronics.

The application of AI and machine learning algorithms is increasingly critical in predicting material behaviors, simulating molecular structures, and optimizing polymerization processes, leading to reduced R&D cycles and improved product quality. Furthermore, AI-driven analytics are being employed to refine production parameters, minimize waste, and enable predictive maintenance for manufacturing equipment, thereby boosting overall operational effectiveness. This integration signals a transformative shift towards more intelligent and adaptive production ecosystems within the PPE industry.

- AI-driven acceleration in novel PPE formulation discovery and optimization.

- Enhanced manufacturing process efficiency and predictive maintenance through machine learning.

- Improved supply chain management and logistics optimization using AI analytics.

- Automated quality control and defect detection in PPE production.

- Simulation and modeling of PPE material performance for specific applications.

Key Takeaways Polyphenylene Ether Market Size & Forecast

Users frequently seek concise summaries regarding the growth trajectory and critical factors shaping the Polyphenylene Ether market. The primary takeaway from the market size and forecast analysis is the consistent and robust growth anticipated through 2033, driven by its indispensable role in high-growth industries such as automotive, electronics, and healthcare. The inherent properties of PPE, including its excellent thermal resistance, dimensional stability, and electrical insulation capabilities, position it as a material of choice for demanding applications.

Furthermore, the market's expansion is intrinsically linked to global megatrends like electrification, urbanization, and advancements in digital infrastructure. While challenges such as raw material price volatility and competition from alternative polymers exist, strategic innovations in blending technologies and a focus on sustainable solutions are expected to mitigate these headwinds. The forecast underscores a positive outlook for PPE, with significant opportunities emerging in specialized and performance-critical end-use sectors.

- Robust Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033, indicating strong market expansion.

- Market valuation expected to nearly double from USD 1.85 Billion in 2025 to USD 3.10 Billion by 2033.

- Primary growth catalysts include the electric vehicle revolution, 5G technology rollout, and increasing demand for lightweight materials.

- Innovation in PPE blends and sustainable practices are crucial for continued market penetration and competitive advantage.

- The market exhibits resilience despite challenges, with continuous opportunities in high-performance applications.

Polyphenylene Ether Market Drivers Analysis

The Polyphenylene Ether market is significantly driven by its unique combination of properties, which are increasingly sought after across diverse industrial applications. A prominent driver is the escalating demand from the automotive sector, particularly for lightweighting initiatives aimed at improving fuel efficiency and reducing emissions in traditional vehicles, alongside the critical need for advanced materials in electric vehicles (EVs). PPE's excellent thermal stability, flame retardancy, and electrical insulation properties make it ideal for EV battery components, charging infrastructure, and structural parts.

Another key driver stems from the rapidly evolving electrical and electronics industry. With the ongoing miniaturization of electronic devices and the deployment of 5G communication networks, there is a heightened requirement for materials with superior dielectric strength, low dielectric loss, and dimensional stability at high temperatures. PPE and its blends fulfill these criteria, being essential for connectors, circuit boards, and telecommunication equipment, ensuring reliable performance in high-frequency applications.

Furthermore, the expansion of the healthcare sector and advancements in industrial applications also contribute substantially to market growth. In healthcare, PPE's ability to withstand repeated sterilization cycles makes it suitable for medical devices and equipment. Across various industrial uses, its chemical resistance and mechanical strength are valued for pumps, impellers, and fluid handling systems, underpinning its broad utility and sustained demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive Industry (Lightweighting & EVs) | +1.8% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 |

| Increasing Demand in Electrical & Electronics Sector (5G, Miniaturization) | +1.5% | Asia Pacific (South Korea, Taiwan, China), North America, Europe | 2025-2033 |

| Rising Adoption in Healthcare Applications (Medical Devices) | +0.9% | North America, Europe, Japan | 2025-2030 |

| Infrastructure Development and Construction | +0.7% | Asia Pacific (India, Southeast Asia), Latin America | 2028-2033 |

| Demand for High-Performance Engineering Plastics | +1.0% | Global | 2025-2033 |

Polyphenylene Ether Market Restraints Analysis

Despite its advantageous properties, the Polyphenylene Ether market faces certain restraints that could temper its growth trajectory. One significant challenge is the relatively high manufacturing cost associated with PPE compared to conventional commodity plastics. This elevated cost can limit its adoption in price-sensitive applications, pushing manufacturers to seek more economical, albeit less performant, alternative materials. The complex synthesis process and the specialized equipment required contribute to the overall production expenses, affecting its competitive positioning in certain segments.

Fluctuations in raw material prices, particularly those of benzene, toluene, and other precursor chemicals, represent another notable restraint. These raw materials are largely petroleum-derived, making the PPE production cost vulnerable to global crude oil price volatility and geopolitical factors. Such unpredictability can lead to unstable profit margins for manufacturers and hinder long-term investment planning, potentially slowing down market expansion.

Furthermore, recyclability challenges and competition from other high-performance polymers also act as impediments. While PPE offers excellent durability, its inherent resistance to degradation, combined with the complexity of separating PPE from its common blends (e.g., with polystyrene), complicates recycling efforts. This poses an environmental concern and a barrier in regions with strict circular economy mandates. Concurrently, advancements in alternative engineering plastics like polycarbonates, polyamides, and PBT, which may offer a more favorable cost-to-performance ratio for specific applications, present direct competition to PPE's market share.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost | -0.8% | Global | 2025-2033 |

| Fluctuating Raw Material Prices | -0.7% | Global | 2025-2033 |

| Recyclability Challenges and End-of-Life Management | -0.5% | Europe, North America | 2025-2030 |

| Competition from Alternative Polymers | -0.6% | Global | 2025-2033 |

Polyphenylene Ether Market Opportunities Analysis

The Polyphenylene Ether market is poised for significant growth through several emerging opportunities driven by technological advancements and evolving industrial needs. A key opportunity lies in the burgeoning electric vehicle (EV) sector, where PPE's properties are highly advantageous. As EVs gain traction globally, there is an increasing demand for lightweight, flame-retardant materials for battery modules, charging connectors, and structural components. PPE blends offer superior thermal management and electrical insulation, making them indispensable for ensuring safety and performance in EV applications, thereby opening new high-value avenues for market expansion.

The rapid rollout of 5G infrastructure and advancements in data centers present another substantial opportunity. These technologies demand materials with excellent dielectric properties, low signal loss, and high-temperature performance for components like antennas, connectors, and server racks. PPE and its modified versions are well-suited for these demanding electrical and electronic applications, supporting the transition to faster and more reliable communication networks. This segment promises sustained demand as global digital transformation continues.

Furthermore, the growing emphasis on sustainability and circular economy principles is creating opportunities for the development of bio-based PPE and enhanced recycling technologies. Innovations in depolymerization and chemical recycling methods for PPE waste can not only address environmental concerns but also reduce reliance on virgin fossil-based resources. Companies investing in these areas can gain a competitive edge by meeting the increasing demand for eco-friendly materials and contributing to a more sustainable polymer industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Electric Vehicles and Autonomous Driving | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth in 5G Technology Infrastructure and Data Centers | +1.0% | Asia Pacific, North America, Europe | 2025-2030 |

| Expansion into Renewable Energy Sectors (Solar, Wind) | +0.7% | Europe, North America, China | 2028-2033 |

| Development of Bio-based PPE and Advanced Recycling Technologies | +0.6% | Europe, North America, Japan | 2027-2033 |

Polyphenylene Ether Market Challenges Impact Analysis

The Polyphenylene Ether market, while robust, faces several challenges that require strategic navigation to sustain growth. One prominent challenge involves the complexities of managing global supply chains, which are susceptible to geopolitical tensions, trade disputes, and unforeseen disruptions like pandemics. These factors can lead to raw material shortages, increased logistics costs, and delays in product delivery, impacting manufacturing efficiency and market stability. Maintaining a resilient and diversified supply chain is critical for mitigating these risks.

Another significant challenge is the inherent difficulty in achieving cost-effectiveness for mass production, especially for specialized PPE grades. The intricate polymerization processes and the need for high-purity raw materials contribute to elevated production costs, making it challenging for PPE to compete with lower-cost commodity plastics in certain high-volume applications. Innovating in process optimization and exploring new synthesis routes are essential to reduce manufacturing expenses and broaden market accessibility.

Furthermore, market saturation in traditional segments and the increasing scrutiny over environmental impact pose ongoing challenges. While PPE performs exceptionally in niche high-performance applications, some mature markets may experience slower growth, necessitating diversification into new sectors. Additionally, concerns regarding the end-of-life management of plastics, including PPE, and the push for a circular economy require manufacturers to invest in developing more sustainable practices, such as recyclable PPE formulations or advanced recycling technologies, to meet evolving regulatory and consumer expectations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Volatility | -0.7% | Global | 2025-2030 |

| Achieving Cost-effectiveness for Mass Production | -0.6% | Global | 2025-2033 |

| Market Saturation in Certain Traditional Segments | -0.4% | Europe, North America | 2025-2033 |

| Overcoming End-of-Life Management and Sustainability Issues | -0.5% | Europe, North America, Japan | 2025-2033 |

Polyphenylene Ether Market - Updated Report Scope

This comprehensive market research report on Polyphenylene Ether provides an in-depth analysis of market dynamics, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It offers detailed insights into the historical performance from 2019 to 2023 and projects the market trajectory through 2033, serving as a critical resource for strategic decision-making in the global PPE industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.10 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global PolyChem Solutions, Advanced Polymer Technologies, Dynaplast Innovations, Summit Materials Group, Elite Performance Polymers, Universal Plastics Corp., Premier Resin Manufacturers, ChemWorks International, Specialized Polymer Blends, Nexus Engineering Materials, TechPolymer Solutions, FutureComp Material Group, OmniChem Systems, Precision Plastics Inc., Innovative Polymer Solutions, Worldwide Material Sciences. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyphenylene Ether market is meticulously segmented to provide granular insights into its diverse applications, grades, types, and end-use industries. This comprehensive segmentation allows for a detailed understanding of the specific market dynamics within each category, highlighting areas of high growth potential and specific requirements. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions effectively across the global landscape.

- By Application: This segment analyzes the demand for PPE across various industries, including Automotive (e.g., under-hood components, interior parts, battery casings), Electrical & Electronics (e.g., connectors, circuit breakers, switches, telecommunication equipment), Industrial (e.g., pump impellers, fluid handling systems), Healthcare (e.g., medical instruments, sterilization trays), and Other applications (e.g., consumer goods, water filtration membranes).

- By Grade: The market is divided into Modified PPE and Unmodified PPE. Modified PPE, often blended with other polymers like polystyrene or polyamide, accounts for a larger share due to enhanced properties such as improved processability, impact strength, and chemical resistance. Unmodified PPE, while offering superior thermal and electrical properties, is more challenging to process.

- By Type: This segmentation includes PPE Blends and PPE Resins. PPE Blends are widely used to leverage the beneficial properties of PPE while mitigating its processing limitations, often forming synergistic combinations. PPE Resins refer to the pure polymer, primarily utilized in applications demanding its inherent high-performance characteristics.

- By End-Use: This categorizes the final industries consuming PPE, encompassing Consumer Goods (e.g., appliance parts, office equipment), Industrial (e.g., machinery components, electrical enclosures), Transportation (broader category including automotive, aerospace, rail), Building & Construction (e.g., pipes, fittings, electrical conduits), Medical (e.g., diagnostic equipment, surgical tools), and Other specialized end-uses.

Regional Highlights

-

North America

North America is a significant market for Polyphenylene Ether, driven by robust growth in its automotive, electrical and electronics, and healthcare sectors. The region benefits from substantial investments in research and development, fostering innovation in material science and advanced manufacturing techniques. Demand for lightweight and high-performance materials in the automotive industry, particularly with the accelerating shift towards electric vehicles, is a key growth catalyst. Manufacturers in North America are increasingly adopting PPE for battery components, charging infrastructure, and structural parts due to its superior thermal and electrical insulation properties.

The electronics sector, propelled by the expansion of 5G networks and data centers, also contributes significantly to the demand for PPE. Its excellent dielectric properties and dimensional stability make it ideal for high-frequency connectors, circuit boards, and other critical electronic components. Furthermore, the stringent regulatory landscape and emphasis on quality and safety in the healthcare industry bolster the use of PPE in medical devices and equipment requiring repeated sterilization. The presence of major industry players and a strong innovation ecosystem ensure North America remains a pivotal market.

-

Europe

Europe represents a mature yet continually evolving market for Polyphenylene Ether, distinguished by its stringent environmental regulations and a strong focus on sustainable materials and circular economy principles. The European automotive industry, renowned for its technological advancements, remains a primary consumer of PPE, integrating it into vehicles for lightweighting, enhanced safety, and improved energy efficiency. The region's commitment to reducing carbon emissions further accelerates the adoption of PPE in electric and hybrid vehicle platforms.

The electronics and industrial machinery sectors in Europe also exhibit a steady demand for PPE, driven by the need for high-performance plastics that can withstand harsh operating conditions and provide reliable electrical insulation. Furthermore, Europe is at the forefront of exploring advanced recycling technologies and developing bio-based or recycled content PPE formulations, aligning with its ambitious sustainability goals. This focus on green manufacturing and innovation is expected to open new avenues for PPE applications across various industrial segments.

-

Asia Pacific (APAC)

Asia Pacific emerges as the largest and fastest-growing market for Polyphenylene Ether, propelled by rapid industrialization, urbanization, and a booming manufacturing sector, particularly in countries like China, India, Japan, and South Korea. The region's dominance in electronics manufacturing and assembly fuels a substantial demand for PPE in consumer electronics, telecommunication equipment, and information technology infrastructure. The aggressive rollout of 5G technology and the expansion of data centers across APAC are creating unprecedented opportunities for high-performance dielectric materials.

The burgeoning automotive industry, especially the escalating production of electric and conventional vehicles in China and India, is another major driver for PPE consumption. As these economies grow, so does the demand for sophisticated engineering plastics for various applications, including lightweight components and advanced electrical systems. Investments in infrastructure development, coupled with a large consumer base and increasing disposable incomes, further solidify APAC's position as a critical growth engine for the Polyphenylene Ether market.

-

Latin America

The Latin American Polyphenylene Ether market is characterized by its emerging industrial base and growing investment in manufacturing and infrastructure. Countries such as Brazil and Mexico are experiencing increased demand for engineering plastics, largely influenced by their developing automotive industries and rising consumer goods production. While smaller compared to other regions, the market shows promising growth potential as industrialization efforts continue and foreign investments stimulate local manufacturing capabilities.

The expansion of electrical and electronics assembly plants, alongside construction and building activities, is gradually contributing to the increased adoption of PPE in the region. Challenges such as economic volatility and import dependencies remain, but consistent industrial development and a rising middle class seeking higher quality products are expected to drive a steady increase in demand for performance polymers like PPE over the forecast period.

-

Middle East and Africa (MEA)

The Middle East and Africa (MEA) Polyphenylene Ether market is currently in its nascent stage but is expected to exhibit gradual growth, primarily driven by infrastructure development projects and diversification efforts away from oil-dependent economies. Countries in the Gulf Cooperation Council (GCC) are investing heavily in new industrial zones, smart cities, and advanced manufacturing capabilities, creating a nascent demand for high-performance plastics. The nascent automotive and electronics assembly sectors also contribute to the consumption of PPE.

While the overall market size remains comparatively smaller, opportunities are emerging in niche applications within the energy sector, industrial machinery, and specialized electrical installations. Increased foreign direct investment and initiatives to localize manufacturing processes are anticipated to stimulate further growth. However, market expansion will largely depend on the pace of industrial diversification and the adoption of advanced material technologies across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyphenylene Ether Market.- Global PolyChem Solutions

- Advanced Polymer Technologies

- Dynaplast Innovations

- Summit Materials Group

- Elite Performance Polymers

- Universal Plastics Corp.

- Premier Resin Manufacturers

- ChemWorks International

- Specialized Polymer Blends

- Nexus Engineering Materials

- TechPolymer Solutions

- FutureComp Material Group

- OmniChem Systems

- Precision Plastics Inc.

- Innovative Polymer Solutions

- Worldwide Material Sciences

Frequently Asked Questions

Analyze common user questions about the Polyphenylene Ether market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Polyphenylene Ether (PPE) and its primary uses?

Polyphenylene Ether (PPE) is a high-performance amorphous thermoplastic renowned for its excellent thermal stability, mechanical strength, and electrical properties. It is extensively used in engineering plastics, often blended with other polymers to enhance processability. Primary uses include automotive components (e.g., battery parts, dashboards), electrical and electronics (e.g., connectors, circuit boards, switches), industrial equipment (e.g., pumps, valves), and medical devices (e.g., surgical instruments, sterilization trays).

How is the Polyphenylene Ether market projected to grow?

The Polyphenylene Ether market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 3.10 Billion by 2033. This growth is primarily driven by increasing demand from electric vehicle manufacturing, advanced electronics, and the healthcare sector, alongside continued innovation in material blends.

What are the main drivers of growth for the PPE market?

Key growth drivers for the PPE market include the accelerating adoption of electric vehicles due to their lightweighting and thermal management needs, the rapid expansion of 5G infrastructure and miniaturized electronics requiring superior dielectric materials, and the increasing use of PPE in advanced medical devices requiring high-temperature sterilization and biocompatibility.

What challenges does the Polyphenylene Ether market face?

The Polyphenylene Ether market faces challenges such as its relatively high manufacturing cost compared to other plastics, fluctuations in raw material prices, complexities associated with its recyclability and end-of-life management, and intense competition from alternative high-performance polymers that may offer more favorable cost-to-performance ratios in specific applications.

Which regions are key contributors to the Polyphenylene Ether market?

Asia Pacific is currently the largest and fastest-growing market for Polyphenylene Ether, driven by robust manufacturing in electronics and automotive sectors, particularly in China and India. North America and Europe also remain significant contributors, characterized by strong demand from advanced automotive, electronics, and healthcare industries, coupled with a focus on sustainable material innovations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted