Polyethylene Naphthalate Market

Polyethylene Naphthalate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706288 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Polyethylene Naphthalate Market Size

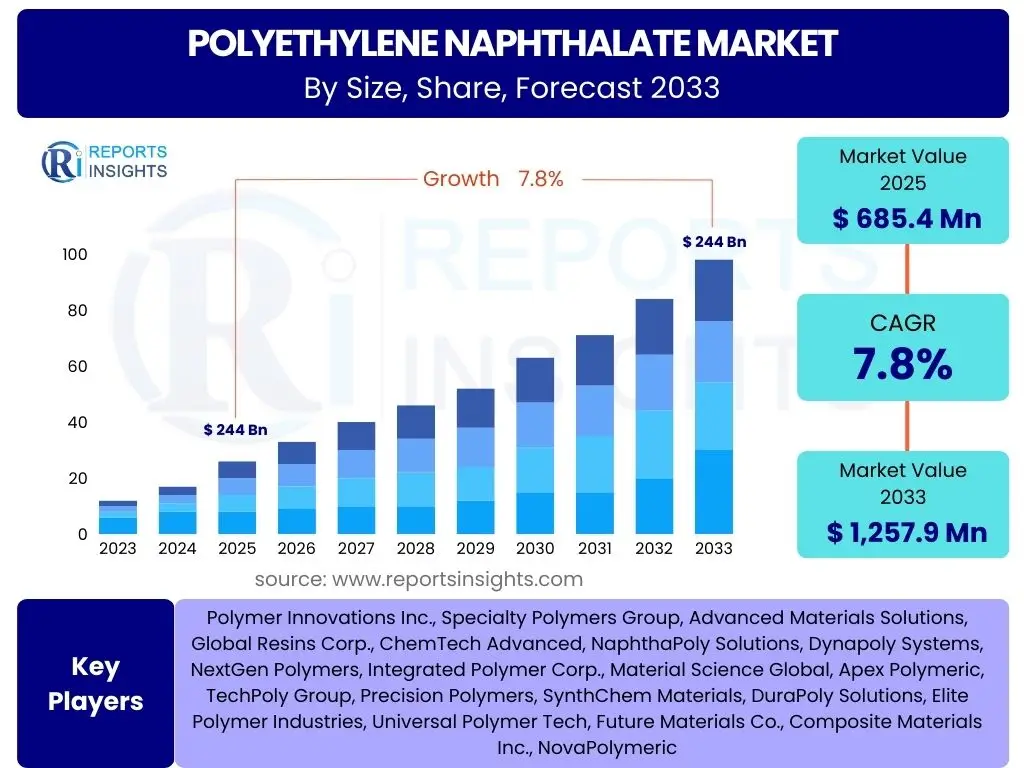

According to Reports Insights Consulting Pvt Ltd, The Polyethylene Naphthalate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 685.4 million in 2025 and is projected to reach USD 1,257.9 million by the end of the forecast period in 2033.

Key Polyethylene Naphthalate Market Trends & Insights

The Polyethylene Naphthalate (PEN) market is currently experiencing significant growth driven by increasing demand for high-performance materials across diverse industries. A prominent trend is the rising adoption of PEN in advanced packaging solutions due to its superior barrier properties against gases and moisture, extended shelf life, and improved product integrity. This is particularly evident in the food and beverage sector for sensitive products and in medical packaging where sterilization and product protection are paramount. Furthermore, the push for lightweighting and enhanced durability in components is fueling PEN’s integration into automotive and aerospace applications.

Another crucial trend is the expanding application of PEN in the electronics industry, especially for flexible displays, printed circuit boards (PCBs), and capacitors. Its excellent thermal stability, electrical insulation properties, and dimensional stability at high temperatures make it an ideal candidate for next-generation electronic devices. There is also an ongoing emphasis on developing more sustainable and recyclable PEN variants, although challenges in establishing widespread recycling infrastructure for specialized polymers persist. Innovations in polymerization techniques and processing methods are also contributing to the market's evolution, allowing for broader and more cost-effective applications.

- Growing demand for high-barrier packaging solutions.

- Increased adoption in flexible electronics and advanced displays.

- Lightweighting initiatives in the automotive and aerospace sectors.

- Expansion into high-performance medical device components.

- Focus on enhanced thermal and mechanical stability in end-use applications.

- Research and development efforts in sustainable PEN formulations.

AI Impact Analysis on Polyethylene Naphthalate

Artificial intelligence is progressively influencing the Polyethylene Naphthalate sector by optimizing various stages of the polymer lifecycle, from research and development to manufacturing and supply chain management. In the R&D phase, AI algorithms are being employed to accelerate the discovery and design of novel PEN formulations with enhanced properties, predicting material behaviors under different conditions, and simulating polymerization processes to identify optimal synthesis routes. This predictive capability significantly reduces the time and cost associated with traditional experimental methods, leading to faster innovation in PEN grades tailored for specific high-performance applications.

Within manufacturing, AI’s impact is evident in process optimization, quality control, and predictive maintenance. Machine learning models analyze real-time sensor data from production lines to fine-tune reaction parameters, minimize defects, and improve batch consistency, thereby enhancing overall production efficiency and reducing waste. Furthermore, AI-driven predictive maintenance systems anticipate equipment failures, allowing for proactive interventions that reduce downtime and maintenance costs. In the supply chain, AI is used for demand forecasting, inventory management, and logistics optimization, ensuring a more resilient and efficient flow of raw materials and finished PEN products globally, mitigating risks associated with market fluctuations and supply disruptions.

- Accelerated material discovery and formulation design through AI-driven simulations.

- Optimization of PEN manufacturing processes for improved efficiency and yield.

- Enhanced quality control and defect detection using machine learning algorithms.

- Predictive maintenance of production equipment, minimizing operational downtime.

- Advanced supply chain forecasting and logistics optimization for PEN raw materials and products.

Key Takeaways Polyethylene Naphthalate Market Size & Forecast

The Polyethylene Naphthalate market is poised for robust growth through 2033, primarily driven by its superior material properties that cater to demanding high-performance applications. Its inherent characteristics, such as excellent thermal stability, gas barrier properties, and mechanical strength, make it indispensable in sectors requiring materials that withstand extreme conditions and offer extended product lifecycles. This growth trajectory indicates a strong market confidence in PEN's unique capabilities, positioning it as a preferred material over conventional polymers in specialized niches.

Geographically, Asia Pacific is anticipated to remain the dominant market due to its thriving electronics manufacturing and expanding packaging industries. However, North America and Europe are expected to show significant growth in high-value applications such as automotive and aerospace, fueled by stringent regulatory requirements and continuous innovation in material science. The market’s expansion is also critically linked to ongoing research and development efforts aimed at improving PEN's cost-effectiveness and exploring new sustainable production methods, addressing key restraints and opening new avenues for broader adoption.

- Polyethylene Naphthalate market demonstrates strong growth potential, projecting nearly a doubling in market size by 2033.

- Key growth drivers include superior thermal stability, excellent barrier properties, and high mechanical strength.

- Primary applications in advanced packaging, electronics, and automotive sectors are propelling demand.

- Asia Pacific maintains market leadership, with significant growth in North America and Europe.

- Continuous innovation in material science and processing techniques is crucial for market expansion.

Polyethylene Naphthalate Market Drivers Analysis

The inherent material properties of Polyethylene Naphthalate constitute a primary driver for its market expansion. PEN exhibits exceptional thermal stability, allowing it to maintain its structural integrity and performance under high temperatures, which is critical for applications in electronics, automotive engine components, and certain industrial processes. This superior heat resistance differentiates it from other polyesters like PET, making it a preferred choice where temperature extremes are a factor. Additionally, PEN offers excellent barrier properties against oxygen, carbon dioxide, and moisture, significantly enhancing the shelf life of sensitive products, particularly in food, beverage, and pharmaceutical packaging.

Growing demand from the electronics and automotive industries further propels the PEN market. In electronics, PEN's dimensional stability, low thermal expansion, and electrical insulation properties make it ideal for flexible printed circuit boards, high-performance capacitors, and display substrates, especially in the evolving landscape of flexible and wearable electronics. The automotive sector utilizes PEN for tire cord fabrics, belts, hoses, and interior components due to its high tensile strength, fatigue resistance, and ability to withstand harsh environmental conditions, contributing to vehicle lightweighting and improved fuel efficiency.

Moreover, the increasing need for durable and high-performance packaging across various sectors, including medical and industrial, significantly contributes to PEN demand. Its robust mechanical properties and resistance to chemicals make it suitable for medical device packaging requiring sterilization, and for industrial applications such as high-strength tapes and protective films. As industries continue to seek materials that offer extended product lifespan and enhanced performance under challenging conditions, the intrinsic advantages of PEN position it as a material of choice.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Superior Barrier Properties (Gas & Moisture) | +2.5% | Global, particularly APAC & Europe | Short to Medium Term (2025-2029) |

| High Thermal Stability & Mechanical Strength | +2.0% | North America, Europe, APAC (Electronics & Automotive) | Medium to Long Term (2027-2033) |

| Growing Demand in Electronics Industry | +1.5% | APAC (China, South Korea, Japan), North America | Short to Medium Term (2025-2030) |

| Increasing Use in Automotive Applications | +1.0% | Europe, North America, APAC (China, India) | Medium Term (2026-2031) |

| Rise of High-Performance Packaging | +0.8% | Global | Short to Medium Term (2025-2029) |

Polyethylene Naphthalate Market Restraints Analysis

One of the most significant restraints for the Polyethylene Naphthalate market is its relatively higher production cost compared to conventional polymers like polyethylene terephthalate (PET). The raw material precursors for PEN, primarily dimethyl-2,6-naphthalenedicarboxylate (NDC), are more expensive and less widely available than those for PET. This cost disadvantage limits PEN's adoption in mass-market applications where cost-effectiveness is a primary decision-making factor, confining its use predominantly to niche, high-performance segments where its superior properties justify the premium pricing. This economic barrier makes it challenging for PEN to compete directly with lower-cost alternatives, especially in price-sensitive regions or industries.

Another considerable restraint is the limited production capacity and complex manufacturing processes associated with PEN. The specialized nature of its synthesis requires specific infrastructure and expertise, which are not as readily available as for more common polymers. This limited capacity can lead to supply constraints, potentially hindering market growth when demand surges. Furthermore, the processing of PEN can be more challenging than PET due to its higher melting point and stiffness, requiring specialized equipment and precise control, which adds to manufacturing complexity and potentially higher operational costs for converters.

Competition from other advanced polymers also acts as a restraint. While PEN offers unique benefits, other high-performance polymers, such as polyimides, liquid crystal polymers (LCPs), and specialized polycarbonates, also compete for market share in high-temperature or barrier applications. These alternative materials may offer similar performance characteristics or even superior properties in certain niche applications, posing a competitive threat. Additionally, the lack of well-established recycling infrastructure specifically for PEN, unlike PET, presents an environmental and economic challenge, potentially limiting its appeal as industries increasingly prioritize circular economy principles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Cost Compared to PET | -1.8% | Global | Long Term (2025-2033) |

| Limited Production Capacity & Supply Chain | -1.2% | Global (Specific to NDC availability) | Short to Medium Term (2025-2028) |

| Processing Complexity & Equipment Requirements | -0.9% | Global (Impacts converters) | Short to Medium Term (2025-2029) |

| Competition from Alternative High-Performance Polymers | -0.7% | Global | Medium to Long Term (2027-2033) |

| Lack of Widespread Recycling Infrastructure | -0.5% | Global | Long Term (2028-2033) |

Polyethylene Naphthalate Market Opportunities Analysis

The emergence of new and niche applications presents significant growth opportunities for the Polyethylene Naphthalate market. PEN’s unique combination of high thermal stability, excellent barrier properties, and mechanical strength makes it an ideal candidate for cutting-edge technologies. For instance, its use in flexible solar cells and organic light-emitting diode (OLED) displays is expanding, driven by the increasing demand for lightweight, durable, and efficient renewable energy solutions and advanced electronic interfaces. Furthermore, as industries like aerospace and defense seek lighter and stronger materials for critical components, PEN's properties make it a viable alternative to traditional materials, opening up new revenue streams.

Advancements in polymerization techniques and processing technologies offer another substantial opportunity for market expansion. Research and development efforts focused on improving the efficiency of PEN synthesis, reducing production costs, and enhancing its processability could significantly broaden its applicability. Innovations such as melt-phase polymerization improvements or the development of new catalyst systems can lead to more cost-effective PEN grades, making the material more accessible for a wider range of applications and reducing the cost gap with less performing alternatives. This continuous innovation is crucial for PEN to penetrate new markets beyond its traditional strongholds.

Geographic expansion and strategic partnerships also represent key opportunities. While Asia Pacific leads in electronics manufacturing, there is growing potential for PEN in emerging economies where industrialization and consumer demand for high-quality products are on the rise. Collaborations between PEN manufacturers, material research institutes, and end-use industry players can facilitate the development of customized PEN solutions, tailored to specific industry needs, and accelerate market penetration. Exploring opportunities in composites, medical implants, and specialized industrial films, where PEN’s properties are particularly advantageous, can diversify its application base and drive sustainable growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications (Flexible Electronics, Solar Cells) | +1.5% | Global, especially APAC | Medium to Long Term (2027-2033) |

| Advancements in Polymerization & Processing Techniques | +1.0% | Global (R&D centers in NA, Europe, Japan) | Medium Term (2026-2031) |

| Demand for Sustainable & Recyclable PEN Solutions | +0.8% | Europe, North America | Long Term (2028-2033) |

| Growth in Niche High-Performance Industrial Markets | +0.7% | Global | Short to Medium Term (2025-2030) |

| Geographic Expansion into Developing Economies | +0.5% | Latin America, MEA, Southeast Asia | Long Term (2029-2033) |

Polyethylene Naphthalate Market Challenges Impact Analysis

One of the primary challenges confronting the Polyethylene Naphthalate market is its relatively high manufacturing cost and the associated pricing pressure from more established, lower-cost polymers. The specialized production processes and the reliance on a less ubiquitous precursor, Naphthalene-2,6-dicarboxylic acid (NDCA) or its derivatives, contribute significantly to the higher per-unit cost of PEN compared to PET. This cost differential limits PEN's ability to penetrate broader consumer markets, restricting its widespread adoption despite its superior performance. Manufacturers face the ongoing challenge of optimizing production to reduce costs without compromising material integrity, thereby enhancing PEN’s competitive positioning.

Another significant challenge is the limited awareness and adoption of PEN beyond specialized applications and niche markets. Many industries and designers might be more familiar with traditional polymers, or they might perceive PEN as too expensive for their needs, overlooking its long-term benefits in terms of durability, performance, and reduced material usage due to its strength. Educating the market about PEN's unique properties and the long-term cost efficiencies it can provide, such as reduced material consumption, extended product lifespan, and enhanced product quality, remains a crucial hurdle. This also includes the need to establish clearer application guidelines and design considerations for engineers and product developers.

Environmental concerns, particularly regarding the end-of-life management and recyclability of specialized polymers like PEN, pose a growing challenge. While PEN is theoretically recyclable, the lack of dedicated collection streams and recycling infrastructure for naphthalate-based polymers presents a significant barrier. Unlike PET, which has a well-developed recycling ecosystem, PEN often ends up in landfills or incineration, counteracting sustainability goals. Developing viable and scalable recycling technologies, including chemical recycling methods, and establishing a robust circular economy framework for PEN will be critical to address these environmental challenges and enhance the material's appeal in a sustainability-conscious market. Furthermore, global economic volatility and geopolitical tensions can disrupt the supply chain for raw materials, impacting production and pricing stability for PEN manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost and Price Sensitivity | -1.5% | Global | Long Term (2025-2033) |

| Limited Market Awareness and Adoption Beyond Niche | -1.0% | Global | Medium to Long Term (2026-2033) |

| Absence of Dedicated Recycling Infrastructure | -0.8% | Global | Long Term (2028-2033) |

| Fluctuations in Raw Material Prices | -0.6% | Global | Short to Medium Term (2025-2029) |

| Intense Competition from Alternative Materials | -0.4% | Global | Short to Medium Term (2025-2030) |

Polyethylene Naphthalate Market - Updated Report Scope

This market insights report provides an in-depth analysis of the global Polyethylene Naphthalate market, encompassing market size estimations, growth projections, key trends, drivers, restraints, opportunities, and challenges. It offers a comprehensive segmentation analysis by type, application, and end-use industry, alongside a detailed regional outlook. The report also profiles leading market players, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.4 million |

| Market Forecast in 2033 | USD 1,257.9 million |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Polymer Innovations Inc., Specialty Polymers Group, Advanced Materials Solutions, Global Resins Corp., ChemTech Advanced, NaphthaPoly Solutions, Dynapoly Systems, NextGen Polymers, Integrated Polymer Corp., Material Science Global, Apex Polymeric, TechPoly Group, Precision Polymers, SynthChem Materials, DuraPoly Solutions, Elite Polymer Industries, Universal Polymer Tech, Future Materials Co., Composite Materials Inc., NovaPolymeric |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyethylene Naphthalate market is segmented to provide a granular view of its various facets, enabling a detailed understanding of demand drivers and market dynamics across different product forms, application areas, and end-use industries. This comprehensive segmentation highlights the specific niches where PEN's unique properties are most leveraged and where future growth opportunities are likely to emerge. Understanding these segments is crucial for stakeholders to tailor strategies, identify high-potential areas, and optimize resource allocation.

- By Type:

- Film: Used in high-barrier packaging, flexible electronics, and industrial films.

- Fiber: Employed in tire cords, industrial belting, and high-strength textiles.

- Resin: Utilized for molding high-performance components and as a base for other PEN products.

- By Application:

- Packaging: Includes food & beverage packaging (e.g., bottles, films), medical packaging (e.g., sterile pouches, blister packs), and industrial packaging.

- Electronics: Encompasses flexible displays, high-temperature capacitors, printed circuit boards (PCBs), and insulators.

- Automotive: Applied in tire cords, power transmission belts, hoses, and interior components requiring high durability and temperature resistance.

- Medical: Used in various medical devices and components such as syringes, bottles, and analytical equipment.

- Industrial: Covers applications like high-performance tapes, labels, and specialized protective coatings.

- Others: Includes aerospace components, sporting goods, and niche engineering plastics.

- By End-Use Industry:

- Consumer Goods: Primarily for packaging of food, beverages, and household products.

- Healthcare: For medical devices, pharmaceutical packaging, and diagnostic tools.

- Automotive: Components for vehicles, including tires and engine parts.

- Electrical & Electronics: For various electronic devices, components, and wiring.

- Construction: In specialized films or composites for building materials.

- Others: Includes aerospace, defense, and niche industrial manufacturing.

Regional Highlights

- North America: This region is characterized by high demand for PEN in advanced automotive applications, sophisticated electronics, and high-performance medical devices. Stringent regulations regarding material performance and a robust R&D infrastructure drive innovation and adoption of premium materials like PEN. The focus on lightweighting and fuel efficiency in the automotive sector, alongside the growth of flexible electronics, will continue to fuel demand.

- Europe: Europe represents a significant market for Polyethylene Naphthalate, largely driven by its mature automotive industry, the increasing demand for sustainable and high-barrier packaging, and stringent environmental regulations promoting durable materials. Germany, France, and the UK are key contributors, focusing on high-value applications and advanced manufacturing processes. The region's emphasis on circular economy principles may also spur demand for more recyclable PEN solutions in the long term.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for Polyethylene Naphthalate, primarily due to the rapid expansion of its electronics manufacturing base, particularly in China, South Korea, and Japan. The region's thriving packaging industry, coupled with increasing consumer demand for quality and extended shelf-life products, also significantly contributes to PEN consumption. Countries like India and Southeast Asian nations are emerging as key markets, driven by industrialization and rising disposable incomes.

- Latin America: The Polyethylene Naphthalate market in Latin America is in an nascent stage but is expected to witness steady growth, driven by the expansion of its manufacturing sectors and increasing investments in packaging and automotive industries. Brazil and Mexico are leading the regional demand, focusing on improved packaging solutions and local automotive production.

- Middle East and Africa (MEA): This region is projected to experience gradual growth in the PEN market, primarily influenced by investments in infrastructure, industrial diversification, and increasing demand for packaged goods. The adoption of PEN will be driven by specialized industrial applications and the growing healthcare sector, though the market size remains relatively smaller compared to other regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyethylene Naphthalate Market.- Polymer Innovations Inc.

- Specialty Polymers Group

- Advanced Materials Solutions

- Global Resins Corp.

- ChemTech Advanced

- NaphthaPoly Solutions

- Dynapoly Systems

- NextGen Polymers

- Integrated Polymer Corp.

- Material Science Global

- Apex Polymeric

- TechPoly Group

- Precision Polymers

- SynthChem Materials

- DuraPoly Solutions

- Elite Polymer Industries

- Universal Polymer Tech

- Future Materials Co.

- Composite Materials Inc.

- NovaPolymeric

Frequently Asked Questions

Analyze common user questions about the Polyethylene Naphthalate market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Polyethylene Naphthalate (PEN) and what are its primary uses?

Polyethylene Naphthalate (PEN) is a high-performance polyester resin renowned for its superior thermal stability, excellent barrier properties against gases and moisture, and high mechanical strength. Its primary uses span advanced packaging (food, medical), flexible electronics (displays, PCBs), automotive components (tire cords, belts), and high-strength industrial applications requiring durability and resistance to extreme conditions.

How does PEN differ from Polyethylene Terephthalate (PET)?

PEN offers superior performance characteristics compared to PET, particularly in terms of higher thermal resistance, enhanced barrier properties against gases (like oxygen and CO2), greater UV resistance, and improved mechanical strength. While PET is widely used for general-purpose packaging due to its cost-effectiveness, PEN is preferred for demanding applications where these advanced properties are critical, often justifying its higher cost.

What are the key drivers for the Polyethylene Naphthalate market growth?

The Polyethylene Naphthalate market is primarily driven by increasing demand from high-growth industries such as electronics, automotive, and specialized packaging, all seeking materials with superior thermal stability, barrier properties, and mechanical performance. The continuous innovation in these sectors, along with the push for lightweighting and enhanced product durability, further propels PEN adoption.

What challenges does the Polyethylene Naphthalate market face?

The PEN market faces challenges including its relatively high production cost compared to commodity polymers, leading to price sensitivity in broader applications. Other challenges include limited production capacity, complex manufacturing processes, the absence of a widespread recycling infrastructure for PEN, and intense competition from other advanced high-performance polymers.

What is the future outlook for the Polyethylene Naphthalate market?

The future outlook for the Polyethylene Naphthalate market is positive, with sustained growth projected due to its indispensable role in high-performance and specialty applications. Emerging opportunities in flexible electronics, advanced composites, and medical devices, coupled with ongoing R&D efforts to improve cost-effectiveness and recyclability, are expected to further expand its market footprint globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted