Polyether Polyol Market

Polyether Polyol Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709335 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

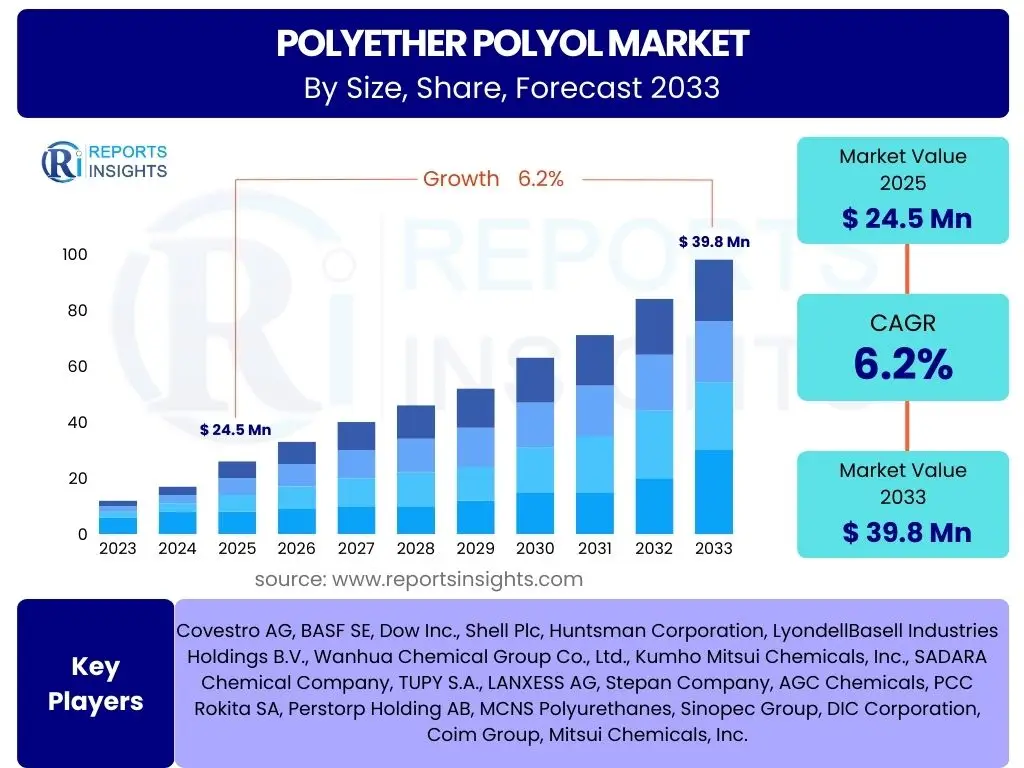

Polyether Polyol Market Size

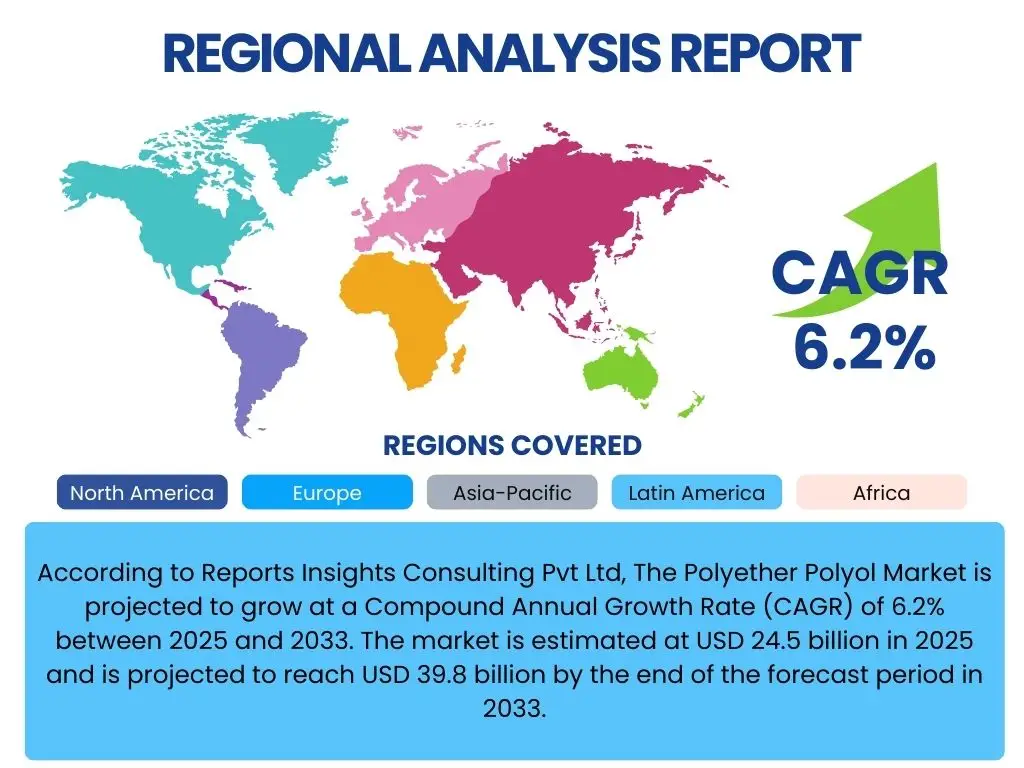

According to Reports Insights Consulting Pvt Ltd, The Polyether Polyol Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 24.5 billion in 2025 and is projected to reach USD 39.8 billion by the end of the forecast period in 2033.

Key Polyether Polyol Market Trends & Insights

The Polyether Polyol market is experiencing a significant transformation driven by evolving end-user demands and increasing focus on sustainability. Key trends indicate a robust demand from the automotive sector, particularly for lightweight and durable materials in electric vehicles, and from the construction industry for enhanced insulation solutions. Furthermore, the development of bio-based polyols is emerging as a crucial trend, addressing environmental concerns and offering sustainable alternatives to traditional petroleum-derived products. Advancements in manufacturing processes, including digitalization and automation, are also contributing to efficiency and cost-effectiveness across the value chain.

Regulatory pressures concerning environmental impact and volatile raw material prices are compelling market players to invest in R&D for novel formulations and alternative feedstocks. The expanding middle class in emerging economies is fueling demand for consumer goods, furniture, and appliances, which extensively use polyether polyols in various forms. This dynamic landscape necessitates continuous innovation and strategic partnerships to maintain competitiveness and capture new growth opportunities, especially in high-performance and specialty applications.

- Growing demand for flexible and rigid foams in diverse end-use industries.

- Increasing adoption of bio-based and sustainable polyether polyols.

- Technological advancements in manufacturing processes for improved efficiency.

- Emphasis on lightweighting solutions in the automotive sector, especially for EVs.

- Expansion of construction activities, driving demand for insulation materials.

- Rising demand for high-performance specialty polyols in CASE applications.

AI Impact Analysis on Polyether Polyol

The integration of Artificial Intelligence (AI) across the Polyether Polyol value chain is poised to revolutionize various aspects, from research and development to manufacturing and supply chain management. Users are particularly interested in how AI can accelerate the discovery of new polyol formulations, optimize reaction conditions for improved yield and purity, and predict material properties with greater accuracy. Predictive modeling capabilities of AI can significantly reduce the time and cost associated with traditional experimentation, enabling faster market introduction of innovative products tailored to specific application requirements, such as enhanced durability or specific viscoelastic properties. This could lead to a new generation of polyols with superior performance characteristics.

In manufacturing, AI-powered systems are expected to enable smart factories, facilitating predictive maintenance of equipment, real-time quality control, and optimized production scheduling to minimize waste and energy consumption. Users also anticipate AI's role in improving supply chain resilience and efficiency through advanced demand forecasting, inventory optimization, and intelligent logistics. Concerns often revolve around the initial investment costs, the need for specialized data scientists and engineers, and ensuring data privacy and security in an interconnected operational environment. However, the overarching expectation is that AI will unlock significant operational efficiencies, enhance product innovation, and provide a competitive edge in a globalized market.

- Accelerated R&D for novel polyol formulations and material discovery.

- Optimization of chemical processes for improved yield, purity, and energy efficiency.

- Predictive maintenance in manufacturing plants to reduce downtime and costs.

- Enhanced supply chain management through advanced demand forecasting and logistics.

- Real-time quality control and anomaly detection in production.

- Development of customized polyols with AI-driven property prediction.

Key Takeaways Polyether Polyol Market Size & Forecast

The Polyether Polyol market is poised for steady growth through 2033, driven by a confluence of factors including robust demand from key end-use industries and an accelerating shift towards sustainable solutions. The projected CAGR of 6.2% reflects the continued necessity of polyether polyols in critical applications such as automotive, construction, and furniture, where their versatility and performance characteristics are indispensable. This growth is underpinned by global urbanization, infrastructure development, and the expansion of the automotive sector, particularly in emerging economies, which continue to drive consumption of polyol-based products.

Key takeaways highlight the strategic importance of innovation in bio-based and recycled content polyols as manufacturers respond to environmental regulations and consumer preferences for greener products. While raw material price volatility and supply chain disruptions present ongoing challenges, the market demonstrates resilience and adaptability through technological advancements and diversification of application areas. Stakeholders should focus on capitalizing on opportunities in high-growth regions and investing in R&D to develop specialty polyols that meet evolving performance and sustainability criteria, ensuring long-term market leadership and profitability.

- Consistent market expansion projected at a 6.2% CAGR from 2025 to 2033.

- Significant market valuation, reaching USD 39.8 billion by 2033.

- Demand primarily fueled by automotive, construction, and furniture industries.

- Increasing focus on sustainable and bio-based polyols as a major growth avenue.

- Technological innovation and specialty product development are crucial for competitive advantage.

- Emerging economies present substantial growth opportunities.

Polyether Polyol Market Drivers Analysis

The global Polyether Polyol market is significantly propelled by the burgeoning demand for flexible and rigid polyurethane foams across various sectors. Flexible foams, extensively used in furniture, bedding, and automotive seating, benefit from increasing consumer spending and rising disposable incomes, especially in developing regions. The automotive industry’s drive towards lightweighting to enhance fuel efficiency and reduce emissions further boosts the demand for high-performance polyether polyols. Simultaneously, rigid foams, critical for insulation in construction, refrigeration, and industrial applications, are experiencing robust growth due to stringent energy efficiency regulations and a global push for sustainable building practices.

Furthermore, the expansion of the construction industry, particularly in Asia Pacific and Latin America, directly translates into higher consumption of polyether polyols for insulation, sealants, and coatings. Urbanization trends and the need for new infrastructure are fueling this growth. The versatility and superior properties of polyether polyols, such as improved durability, flexibility, and insulation capabilities, make them indispensable components in these high-growth end-use applications, ensuring their sustained demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Flexible and Rigid Foams | +1.8% | Global, particularly APAC, North America, Europe | Short-term to Long-term |

| Increasing Automotive Production and EV Adoption | +1.5% | APAC (China, India), Europe, North America | Mid-term to Long-term |

| Expansion of the Construction Industry and Insulation Needs | +1.2% | APAC, Middle East & Africa, Europe | Short-term to Long-term |

| Technological Advancements and Specialty Applications | +0.9% | North America, Europe, Japan, China | Mid-term |

Polyether Polyol Market Restraints Analysis

The Polyether Polyol market faces significant restraints, primarily stemming from the volatility of raw material prices. Propylene oxide, a key feedstock, is derived from crude oil, making its price susceptible to fluctuations in global oil markets, geopolitical instabilities, and supply-demand imbalances. These price variations directly impact manufacturing costs for polyether polyols, subsequently affecting the profitability margins of producers and potentially leading to higher end-product costs for consumers. Such unpredictability can hinder investment decisions and long-term planning within the industry, forcing companies to absorb costs or pass them on, thereby affecting market competitiveness.

Environmental regulations and concerns regarding the sustainability of petroleum-derived chemicals also pose a substantial restraint. Increasing pressure to reduce carbon footprint and minimize reliance on fossil fuels pushes manufacturers to invest in costly R&D for bio-based alternatives, which may not yet be cost-competitive or scalable enough to meet market demand. Additionally, the availability of substitutes, such as polyester polyols in certain applications or alternative insulation materials, can cap growth in specific segments. These factors collectively require manufacturers to adopt agile strategies to mitigate risks and adapt to a rapidly evolving regulatory and economic landscape.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (e.g., Propylene Oxide) | -1.1% | Global | Short-term to Mid-term |

| Stringent Environmental Regulations | -0.8% | Europe, North America, Japan | Mid-term to Long-term |

| Competition from Substitute Materials | -0.5% | Global | Mid-term |

| Supply Chain Disruptions and Logistics Challenges | -0.4% | Global | Short-term |

Polyether Polyol Market Opportunities Analysis

Significant opportunities in the Polyether Polyol market are emerging from the escalating demand for sustainable and bio-based products. As environmental awareness grows and regulatory frameworks become more stringent, manufacturers are investing heavily in research and development to produce polyether polyols derived from renewable resources like vegetable oils and algae. These bio-based alternatives not only offer a reduced carbon footprint but also appeal to environmentally conscious consumers and industries aiming for green certifications. The development and commercialization of these innovative products can open new market segments and enhance brand value for pioneering companies, positioning them favorably for future growth.

Furthermore, the rapid industrialization and urbanization in emerging economies, particularly across Asia Pacific, Latin America, and the Middle East, present substantial growth avenues. These regions are experiencing booming construction sectors, increasing automotive production, and rising demand for consumer goods, all of which are significant end-users of polyether polyols. Strategic investments in these markets, coupled with localized production facilities and tailored product offerings, can enable companies to capture a larger market share. Innovations in high-performance applications, such as for wind energy blades, aerospace components, and specialized adhesives, also represent niche but high-value opportunities for specialty polyol manufacturers seeking to differentiate their offerings.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Bio-based Polyether Polyols | +1.3% | Global, particularly Europe, North America | Mid-term to Long-term |

| Growing Demand from Emerging Economies | +1.0% | APAC (China, India, Southeast Asia), Latin America | Short-term to Long-term |

| Innovation in High-Performance and Specialty Applications | +0.8% | North America, Europe, Japan | Mid-term |

| Recycling Technologies for Polyurethane Products | +0.6% | Europe, North America | Long-term |

Polyether Polyol Market Challenges Impact Analysis

The Polyether Polyol market grapples with several significant challenges that can impede its growth trajectory. One primary concern is the escalating cost of compliance with evolving environmental and safety regulations. Stricter norms regarding emissions, waste disposal, and the use of certain chemicals necessitate substantial investments in process upgrades, R&D for cleaner technologies, and robust safety protocols. These compliance costs can erode profit margins, particularly for smaller players, and act as a barrier to market entry for new innovators, potentially stifling competition and innovation within the industry.

Another critical challenge is the intense competition and overcapacity in certain regional markets, particularly in Asia. The proliferation of new manufacturing facilities, often driven by government incentives, can lead to supply exceeding demand, exerting downward pressure on prices and profitability. This competitive landscape forces companies to differentiate through product innovation, cost efficiency, or expansion into niche, high-value applications. Moreover, managing complex global supply chains, susceptible to geopolitical events, trade disputes, and natural disasters, remains a persistent challenge, threatening timely delivery of raw materials and finished products, and adding to operational complexities and costs across the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Landscape and Compliance Costs | -0.9% | Global, particularly Europe, North America | Mid-term to Long-term |

| Intense Competition and Market Saturation in Key Regions | -0.7% | APAC (China), Europe | Short-term to Mid-term |

| Complex Global Supply Chain Management | -0.6% | Global | Short-term to Mid-term |

| Development of Cost-Effective Bio-based Alternatives | -0.5% | Global | Mid-term to Long-term |

Polyether Polyol Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global Polyether Polyol market, covering historical performance, current market dynamics, and future growth projections from 2025 to 2033. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. The report segments the market by product type, application, end-use industry, and geography, offering granular insights into various market segments and their potential for growth. Key competitive analysis, including market share, strategies, and recent developments of prominent players, is also included to provide a clear understanding of the competitive ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 39.8 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Covestro AG, BASF SE, Dow Inc., Shell Plc, Huntsman Corporation, LyondellBasell Industries Holdings B.V., Wanhua Chemical Group Co., Ltd., Kumho Mitsui Chemicals, Inc., SADARA Chemical Company, TUPY S.A., LANXESS AG, Stepan Company, AGC Chemicals, PCC Rokita SA, Perstorp Holding AB, MCNS Polyurethanes, Sinopec Group, DIC Corporation, Coim Group, Mitsui Chemicals, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyether Polyol market is extensively segmented to provide granular insights into its diverse applications and product types, catering to a wide range of industrial requirements. This segmentation allows for a detailed examination of market dynamics within specific categories, highlighting growth areas and technological preferences. The primary classifications include product type, which differentiates between flexible, rigid, and CASE polyether polyols, each possessing distinct properties and end-use applications. Further segmentation by application and end-use industry provides a clearer picture of demand drivers across sectors such as automotive, construction, and furniture, offering strategic perspectives for market participants.

- By Type:

- Flexible Polyether Polyols

- Rigid Polyether Polyols

- CASE (Coatings, Adhesives, Sealants, Elastomers) Polyether Polyols

- By Application:

- Flexible Foam

- Furniture

- Bedding

- Automotive Seating

- Packaging

- Rigid Foam

- Construction Insulation

- Refrigeration

- Industrial Insulation

- CASE

- Coatings

- Adhesives

- Sealants

- Elastomers

- Binders

- Flexible Foam

- By End-Use Industry:

- Automotive

- Construction

- Furniture & Bedding

- Packaging

- Footwear

- Electronics

- Others

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market due to rapid industrialization, urbanization, and significant growth in the automotive, construction, and electronics sectors, particularly in China, India, and Southeast Asian countries. Increasing disposable incomes are also fueling demand for consumer goods.

- North America: A mature market characterized by stringent environmental regulations driving innovation in sustainable polyols and high demand from the automotive, construction, and furniture industries. The region focuses on specialty and high-performance polyols.

- Europe: Driven by strict energy efficiency standards in the construction sector and a strong automotive industry. Emphasis on sustainability and circular economy principles is boosting research and adoption of bio-based and recycled content polyols. Germany, France, and the UK are key contributors.

- Latin America: Expected to show steady growth with increasing investments in infrastructure development, rising automotive production, and expanding consumer markets in Brazil, Mexico, and Argentina.

- Middle East and Africa (MEA): Emerging as a significant market due to ongoing construction projects, particularly in the GCC countries, and growing demand for insulation materials to meet energy efficiency requirements in hot climates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyether Polyol Market.- Covestro AG

- BASF SE

- Dow Inc.

- Shell Plc

- Huntsman Corporation

- LyondellBasell Industries Holdings B.V.

- Wanhua Chemical Group Co., Ltd.

- Kumho Mitsui Chemicals, Inc.

- SADARA Chemical Company

- TUPY S.A.

- LANXESS AG

- Stepan Company

- AGC Chemicals

- PCC Rokita SA

- Perstorp Holding AB

- MCNS Polyurethanes

- Sinopec Group

- DIC Corporation

- Coim Group

- Mitsui Chemicals, Inc.

Frequently Asked Questions

What are polyether polyols primarily used for?

Polyether polyols are primarily used in the production of polyurethane foams, which find extensive applications in flexible products like furniture, bedding, and automotive seating, as well as rigid products such as insulation for construction and refrigeration.

How does the automotive industry influence the demand for polyether polyols?

The automotive industry significantly influences demand for polyether polyols due to their use in comfortable seating, interior components, and lightweighting solutions for enhanced fuel efficiency and electric vehicle performance.

What are bio-based polyether polyols?

Bio-based polyether polyols are sustainable alternatives derived from renewable resources like vegetable oils (e.g., soybean, castor oil) instead of traditional petroleum feedstocks. They aim to reduce environmental impact and carbon footprint.

What factors are restraining the growth of the polyether polyol market?

Key restraints include the volatility of raw material prices (especially propylene oxide), stringent environmental regulations, and competition from substitute materials in certain applications.

Which regions are expected to drive future growth in the polyether polyol market?

Asia Pacific, particularly countries like China and India, is projected to be the leading growth region due to rapid industrialization, urbanization, and expanding end-use industries such as construction and automotive.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted