Geotextile Market

Geotextile Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705440 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Geotextile Market Size

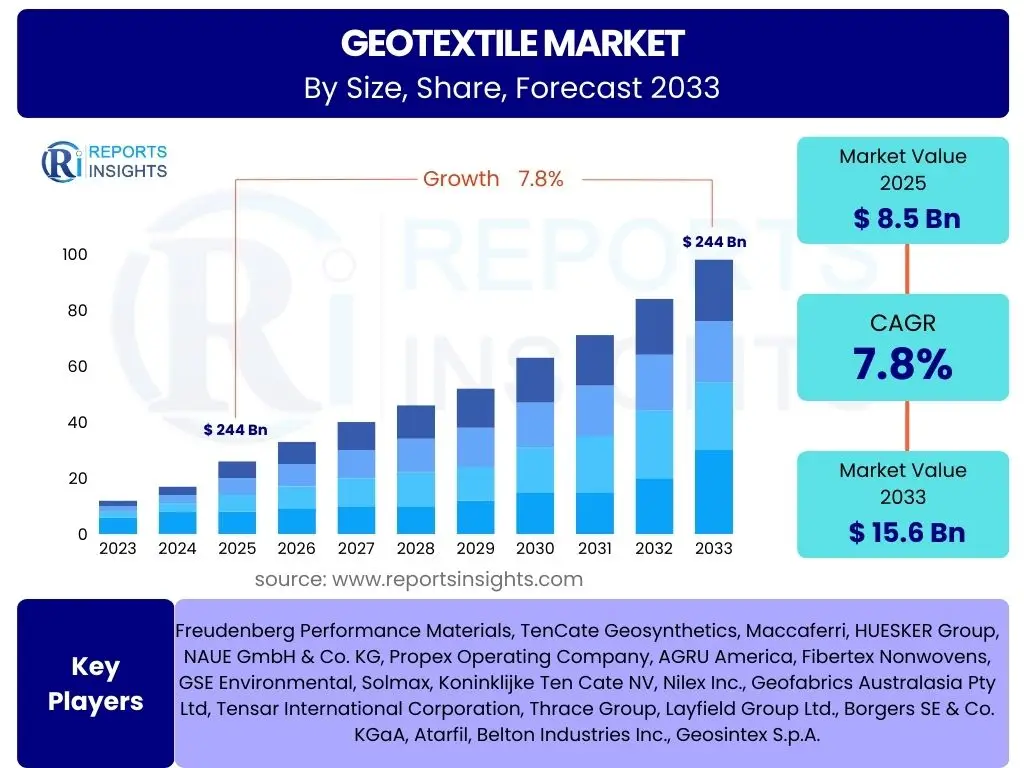

According to Reports Insights Consulting Pvt Ltd, The Geotextile Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 15.6 Billion by the end of the forecast period in 2033.

Key Geotextile Market Trends & Insights

Current market dynamics indicate a significant shift towards sustainable engineering practices and advanced material science within the Geotextile sector. A primary trend observed is the escalating demand for geotextiles in infrastructure development, particularly in emerging economies where extensive road networks, railway lines, and port facilities are being constructed or upgraded. This growth is complemented by increasing global awareness regarding environmental protection and climate change impacts, leading to greater adoption of geotextiles for erosion control, coastal defense, and landfill management.

Another prominent insight is the continuous innovation in geotextile materials and manufacturing processes. Manufacturers are investing in research and development to produce geotextiles with enhanced properties such as improved tensile strength, durability, filtration capabilities, and biodegradability. The integration of smart technologies and the development of composite geotextiles are also gaining traction, offering superior performance for complex engineering challenges. Furthermore, stringent regulatory frameworks promoting sustainable construction and waste management contribute significantly to the market's expansion and technological advancements.

The market is also witnessing a trend of diversification in applications beyond traditional civil engineering. Geotextiles are increasingly being used in agricultural practices for soil stabilization and drainage, in sports facilities, and in landscape architecture, broadening the market's reach and potential. The demand for specialized geotextiles tailored to specific environmental conditions or project requirements is driving customized product offerings, highlighting a shift from generic solutions to highly engineered applications.

- Increased adoption in infrastructure development across developing regions.

- Growing emphasis on sustainable and eco-friendly construction practices.

- Technological advancements leading to enhanced material properties and new product innovations.

- Rising demand for geotextiles in erosion control and environmental protection projects.

- Diversification of applications into agriculture, landscaping, and specialized civil works.

- Development of smart and composite geotextile materials for complex engineering.

- Stringent environmental regulations fostering the use of geotextiles in waste management.

AI Impact Analysis on Geotextile

The integration of Artificial Intelligence (AI) within the geotextile sector is primarily observed in optimizing design, manufacturing, and project management processes rather than directly impacting the material composition itself. Users frequently inquire about AI's potential to enhance the efficiency and precision of civil engineering projects involving geotextiles. AI-powered algorithms can analyze vast datasets from geological surveys, material properties, and environmental conditions to recommend the most suitable geotextile type and optimal design parameters, thereby minimizing material waste and improving structural integrity.

Furthermore, AI can revolutionize the quality control and inspection phases in geotextile manufacturing and installation. Machine learning models, trained on images and sensor data, can detect defects in geotextile rolls or identify inconsistencies during placement on construction sites, ensuring adherence to quality standards and extending the lifespan of infrastructure. Predictive maintenance, another AI application, can forecast the degradation of geotextile layers in real-world conditions, allowing for timely interventions and preventing costly failures, which is a significant concern for infrastructure longevity.

While direct AI applications in geotextile material science are nascent, the indirect impact through process optimization, smart monitoring, and data-driven decision-making is substantial. AI can streamline supply chain logistics for geotextile procurement, optimize production schedules in manufacturing facilities, and even assist in training construction personnel on proper geotextile handling and installation techniques through augmented reality (AR) interfaces. The overall expectation is that AI will contribute to more efficient, cost-effective, and resilient infrastructure projects where geotextiles play a crucial role, addressing user concerns about project delays and performance variability.

- AI-driven optimization of geotextile selection and design for specific projects.

- Enhanced quality control and defect detection in manufacturing via machine learning.

- Predictive maintenance for geotextile-reinforced structures, extending asset lifespan.

- Optimization of supply chain and logistics for geotextile materials.

- Improved project management and real-time monitoring of installation processes.

- Data-driven insights for performance analysis and risk assessment in civil engineering.

Key Takeaways Geotextile Market Size & Forecast

The Geotextile market is poised for robust growth, driven by an accelerating global focus on infrastructure development and sustainable environmental management. A key takeaway from market forecasts is the consistent demand stemming from large-scale public and private sector projects, including road construction, railway expansion, and water management initiatives. The inherent advantages of geotextiles, such as their cost-effectiveness, durability, and versatility in addressing complex geotechnical challenges, underpin this sustained market expansion.

Another significant insight is the geographical disparity in market growth, with emerging economies in Asia Pacific and Latin America demonstrating particularly strong potential due to rapid urbanization and the need for new infrastructure. Conversely, mature markets in North America and Europe will see growth primarily through maintenance, rehabilitation, and increasingly stringent environmental regulations promoting geotextile use in waste management and erosion control. The market's resilience is further highlighted by its ability to adapt to raw material price fluctuations through product innovation and efficiency improvements.

Ultimately, the forecast emphasizes a market driven by both necessity and innovation. The necessity arises from aging infrastructure, climate change impacts necessitating more resilient structures, and population growth requiring expanded services. Innovation, meanwhile, is manifested in advanced material development, improved installation techniques, and the exploration of new application areas. Stakeholders should recognize the long-term growth trajectory anchored in fundamental engineering requirements and evolving environmental imperatives.

- Consistent growth trajectory driven by global infrastructure development.

- Strong demand from road, railway, and water management projects.

- Significant growth opportunities in emerging economies, particularly Asia Pacific.

- Innovation in material science and product development enhancing market value.

- Increasing adoption due to cost-effectiveness and durability benefits.

- Resilience against raw material price volatility through strategic advancements.

- Market expansion supported by environmental regulations and sustainability goals.

Geotextile Market Drivers Analysis

The geotextile market is significantly propelled by the increasing global expenditure on infrastructure development, particularly in burgeoning economies. Governments and private entities are investing heavily in new road networks, railway systems, airports, and urban development projects to support economic growth and accommodate rising populations. Geotextiles offer cost-effective and efficient solutions for soil stabilization, drainage, and erosion control in these large-scale constructions, reducing project timelines and long-term maintenance costs compared to conventional methods.

Furthermore, stringent environmental regulations and a heightened awareness of ecological preservation are driving the adoption of geotextiles in various applications. These materials are crucial for effective waste management, including landfill lining and leachate collection systems, preventing soil and water contamination. They also play a vital role in erosion control for riverbanks, coastal areas, and slopes, mitigating the impact of climate change-related natural disasters and promoting land reclamation.

Technological advancements in polymer science and manufacturing processes have led to the development of geotextiles with enhanced properties such as improved tensile strength, superior filtration capabilities, and increased durability. These innovations enable geotextiles to be used in more demanding applications and challenging environments, further expanding their market penetration. The continuous development of specialized geotextiles tailored for specific engineering needs reinforces their position as essential components in modern civil engineering projects.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Infrastructure Development | +2.1% | Asia Pacific, Latin America, Middle East & Africa | Long-term (5+ years) |

| Rising Environmental Regulations & Awareness | +1.8% | Europe, North America, Developed Asia Pacific | Mid-term (3-5 years) |

| Technological Advancements in Geotextiles | +1.5% | Global | Ongoing (Short to Long-term) |

| Population Growth & Urbanization | +1.2% | Asia Pacific, Africa | Long-term (5+ years) |

| Increased Demand for Waste Management | +0.8% | Global | Mid-term (3-5 years) |

Geotextile Market Restraints Analysis

The geotextile market faces notable restraints, primarily concerning the volatility of raw material prices. The majority of geotextiles are manufactured from petroleum-derived polymers such as polypropylene and polyester. Fluctuations in crude oil prices directly impact the cost of these raw materials, leading to unpredictable manufacturing expenses for geotextile producers. This instability can compress profit margins and potentially deter investment in new production capacities, especially for smaller manufacturers, affecting overall market stability and growth.

Another significant restraint is the lack of standardized regulations and awareness in certain developing regions. While developed countries have established norms and specifications for geotextile application in civil engineering, many emerging markets still lack comprehensive guidelines or adequate enforcement. This can lead to the use of substandard products, poor installation practices, and a general distrust in the long-term performance benefits of geotextiles, hindering wider adoption and market penetration in these regions.

Furthermore, the perceived high initial investment cost for certain specialized geotextile applications or large-scale projects can be a barrier. Although geotextiles offer long-term cost savings through reduced maintenance and extended project lifespans, the upfront capital required for material purchase and specialized installation equipment can be prohibitive for some contractors or project developers, particularly in budget-constrained environments. This challenge often requires extensive education and demonstration of total lifecycle cost benefits to overcome.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | Short to Mid-term (1-5 years) |

| Lack of Awareness & Standardization in Emerging Markets | -0.7% | Africa, Southeast Asia, Latin America | Long-term (5+ years) |

| High Initial Investment Cost | -0.5% | Global, particularly developing nations | Short to Mid-term (1-5 years) |

| Competition from Traditional Construction Methods | -0.3% | Global | Short-term (1-3 years) |

Geotextile Market Opportunities Analysis

The geotextile market is presented with significant opportunities stemming from the increasing focus on sustainable and resilient infrastructure development globally. As climate change impacts intensify, there is a growing need for engineering solutions that can withstand extreme weather events, such as increased rainfall, flooding, and coastal erosion. Geotextiles are integral to these solutions, offering effective and durable methods for erosion control, flood protection barriers, and stabilization of vulnerable land, thus opening new avenues for specialized product development and market expansion in climate adaptation projects.

The burgeoning smart cities initiative and the development of advanced monitoring systems also represent a fertile ground for market growth. The integration of sensors within geotextiles or geotextile-reinforced structures can provide real-time data on stress, strain, temperature, and moisture content, enabling proactive maintenance and improved structural performance. This convergence of traditional materials with advanced technology creates opportunities for manufacturers to offer high-value, data-enabled solutions, appealing to a tech-savvy construction sector.

Furthermore, expanding applications in the agricultural sector, particularly for soil conservation, irrigation efficiency, and land drainage, offer untapped potential. Geotextiles can improve crop yields by preventing soil erosion, optimizing water distribution, and creating stable ground for agricultural machinery. The development of biodegradable geotextiles, addressing environmental concerns regarding plastic pollution, also presents a substantial opportunity for innovation and market differentiation, catering to the demand for eco-friendly construction materials and practices.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sustainable & Resilient Infrastructure Development | +1.9% | Global | Long-term (5+ years) |

| Development of Smart Cities & IoT Integration | +1.5% | Developed Economies, Emerging Smart Cities | Mid to Long-term (3-7 years) |

| Expanding Applications in Agriculture | +1.2% | Developing Economies, Agricultural Regions | Mid-term (3-5 years) |

| Innovation in Biodegradable Geotextiles | +1.0% | Europe, North America, Environmentally Conscious Markets | Long-term (5+ years) |

| Rehabilitation of Aging Infrastructure | +0.7% | North America, Europe | Short to Mid-term (1-5 years) |

Geotextile Market Challenges Impact Analysis

The geotextile market faces significant challenges, notably the intense competition from traditional construction materials and methods. In some regions, conventional aggregate-based solutions or outdated practices may still be preferred due to established supply chains, familiar installation techniques, and lower perceived upfront costs, despite the long-term benefits and efficiency offered by geotextiles. Overcoming this inertia requires substantial educational efforts and demonstration projects to showcase the superior performance and cost-effectiveness of geotextile solutions over their lifecycle.

Another critical challenge is ensuring consistent quality control and adherence to installation standards across diverse projects and regions. The performance of geotextiles is highly dependent on proper design and installation. Variances in site conditions, lack of skilled labor, or insufficient supervision can compromise the integrity and effectiveness of geotextile layers, leading to structural failures and reputational damage. This necessitates robust training programs, clearer industry guidelines, and advanced on-site monitoring technologies to mitigate risks.

Furthermore, the environmental impact associated with the disposal of non-biodegradable geotextiles presents a long-term challenge. As most geotextiles are made from synthetic polymers, their end-of-life management and disposal contribute to plastic waste concerns. While research into biodegradable alternatives is ongoing, the predominant market still relies on non-biodegradable materials. Addressing this challenge requires investment in recycling technologies, the promotion of circular economy principles, and the development of truly sustainable material solutions to align with global environmental objectives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Traditional Methods | -0.8% | Global | Short to Mid-term (1-5 years) |

| Quality Control & Installation Standards | -0.6% | Global, particularly developing nations | Ongoing (Short to Long-term) |

| Environmental Concerns of Non-Biodegradable Geotextiles | -0.4% | Developed Economies, Environmentally Conscious Markets | Long-term (5+ years) |

| Limited Skilled Labor for Specialized Installations | -0.3% | Global | Mid-term (3-5 years) |

Geotextile Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Geotextile market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of market trends, segmentation by product type, material, application, and end-user industry, along with a granular regional analysis to highlight key geographical market dynamics. The report also includes an assessment of the competitive landscape, profiling leading market participants and their strategic initiatives, alongside an impact analysis of emerging technologies such as Artificial Intelligence on the sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 15.6 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Freudenberg Performance Materials, TenCate Geosynthetics, Maccaferri, HUESKER Group, NAUE GmbH & Co. KG, Propex Operating Company, AGRU America, Fibertex Nonwovens, GSE Environmental, Solmax, Koninklijke Ten Cate NV, Nilex Inc., Geofabrics Australasia Pty Ltd, Tensar International Corporation, Thrace Group, Layfield Group Ltd., Borgers SE & Co. KGaA, Atarfil, Belton Industries Inc., Geosintex S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global geotextile market is meticulously segmented to provide a granular understanding of its diverse applications and material compositions, enabling stakeholders to identify specific growth areas and market niches. This segmentation helps in analyzing demand patterns across various product types, materials used, and the broad range of applications and end-user industries that leverage geotextile solutions. Understanding these segments is crucial for strategic planning, product development, and market penetration, as each segment responds to unique drivers and faces distinct challenges.

The market's performance is heavily influenced by the adoption rates within these different segments. For instance, the growth in woven geotextiles is often tied to large-scale infrastructure projects requiring high tensile strength, whereas non-woven geotextiles dominate applications demanding superior filtration and drainage properties. Similarly, the increasing focus on environmental protection is boosting the landfill and erosion control application segments, while the expansion of transportation networks remains a consistent driver for road and railway construction applications. This comprehensive segmentation highlights the versatility and critical role of geotextiles in modern engineering across multiple sectors.

- By Product Type:

- Woven Geotextiles

- Non-woven Geotextiles

- Knitted Geotextiles

- Others (e.g., Composite Geotextiles)

- By Material:

- Polypropylene (PP)

- Polyester (PET)

- Polyethylene (PE)

- Others (e.g., Natural Fibers like Jute, Coir)

- By Application:

- Road Construction & Pavement Overlays

- Erosion Control & Sedimentation

- Drainage & Filtration Systems

- Railway Construction

- Landfill & Waste Containment

- Civil Engineering (e.g., Dams, Reservoirs, Foundations)

- Agriculture & Horticulture

- Coastal Protection & River Works

- Sports Facilities & Landscaping

- By End-User Industry:

- Transportation Infrastructure (Roads, Railways, Airports)

- Environmental Engineering (Landfills, Waste Treatment, Erosion Control)

- Building & Construction (Foundations, Retaining Walls)

- Water Management (Dams, Canals, Reservoirs, Drainage)

- Mining

- Agriculture

Regional Highlights

- North America: The North American geotextile market is characterized by mature infrastructure, a strong emphasis on rehabilitation of aging structures, and stringent environmental regulations. The region witnesses significant demand for geotextiles in erosion control, coastal protection, and waste management applications. Innovations in smart geotextiles and sustainable materials are driving market growth, with government initiatives for infrastructure upgrades contributing significantly.

- Europe: Europe's geotextile market is robust, driven by advanced environmental standards, a focus on sustainable construction, and extensive railway network maintenance. The region is a leader in research and development for eco-friendly and high-performance geotextiles. Demand is particularly strong in civil engineering, water management, and rehabilitation projects, with a growing trend towards biodegradable and recycled content geotextiles.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for geotextiles globally, propelled by rapid urbanization, massive infrastructure development projects (roads, railways, airports, ports), and increasing industrialization in countries like China, India, and Southeast Asian nations. The region's expanding population and economic growth necessitate substantial investment in new construction, fueling demand across all geotextile applications. The "Belt and Road Initiative" in China, for example, is a significant driver.

- Latin America: The Latin American geotextile market is experiencing steady growth, primarily due to rising investments in public infrastructure, mining, and agricultural sectors. Countries like Brazil, Mexico, and Argentina are witnessing increased construction activities, driving the demand for geotextiles in road construction, drainage, and soil stabilization. Awareness and adoption of modern engineering techniques are gradually increasing, presenting significant growth opportunities.

- Middle East and Africa (MEA): The MEA geotextile market is expanding, driven by large-scale construction projects, including new city developments, transportation networks, and oil & gas infrastructure, particularly in the Gulf Cooperation Council (GCC) countries. There is a growing need for water management and erosion control solutions in arid and semi-arid regions. African nations are also investing in infrastructure development to support economic growth, though market maturity varies significantly across the continent.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Geotextile Market.- Freudenberg Performance Materials

- TenCate Geosynthetics

- Maccaferri

- HUESKER Group

- NAUE GmbH & Co. KG

- Propex Operating Company

- AGRU America

- Fibertex Nonwovens

- GSE Environmental

- Solmax

- Koninklijke Ten Cate NV

- Nilex Inc.

- Geofabrics Australasia Pty Ltd

- Tensar International Corporation

- Thrace Group

- Layfield Group Ltd.

- Borgers SE & Co. KGaA

- Atarfil

- Belton Industries Inc.

- Geosintex S.p.A.

Frequently Asked Questions

Analyze common user questions about the Geotextile market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are geotextiles primarily used for?

Geotextiles are permeable synthetic fabrics used extensively in civil engineering and construction applications. Their primary functions include separation, filtration, reinforcement, protection, and drainage, making them essential for soil stabilization, erosion control, road construction, railway beds, landfills, and various water management projects.

What are the main types of geotextiles available?

The main types of geotextiles are woven, non-woven, and knitted. Woven geotextiles are characterized by their high tensile strength, ideal for reinforcement and separation. Non-woven geotextiles offer excellent filtration and drainage properties due to their permeable, felt-like structure. Knitted geotextiles are less common but offer specific properties for specialized applications.

Which factors are driving the growth of the geotextile market?

Key drivers include accelerating global infrastructure development, particularly in emerging economies, increasing adoption of sustainable construction practices, and stringent environmental regulations demanding effective erosion control and waste management solutions. Technological advancements leading to improved material performance also significantly contribute to market expansion.

What challenges does the geotextile market face?

Major challenges include the volatility of raw material prices (primarily petroleum-based polymers), competition from traditional construction methods, and the need for standardized quality control and installation practices, especially in developing regions. The long-term environmental impact of non-biodegradable geotextiles also presents a growing concern for the industry.

How large is the global geotextile market projected to be by 2033?

The global geotextile market is projected to reach an estimated USD 15.6 Billion by the end of 2033. This growth is driven by continued investment in infrastructure, environmental protection initiatives, and ongoing innovations in geotextile materials and applications across various industries worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted