Oil and Gas Pipeline Steel Market

Oil and Gas Pipeline Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700972 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

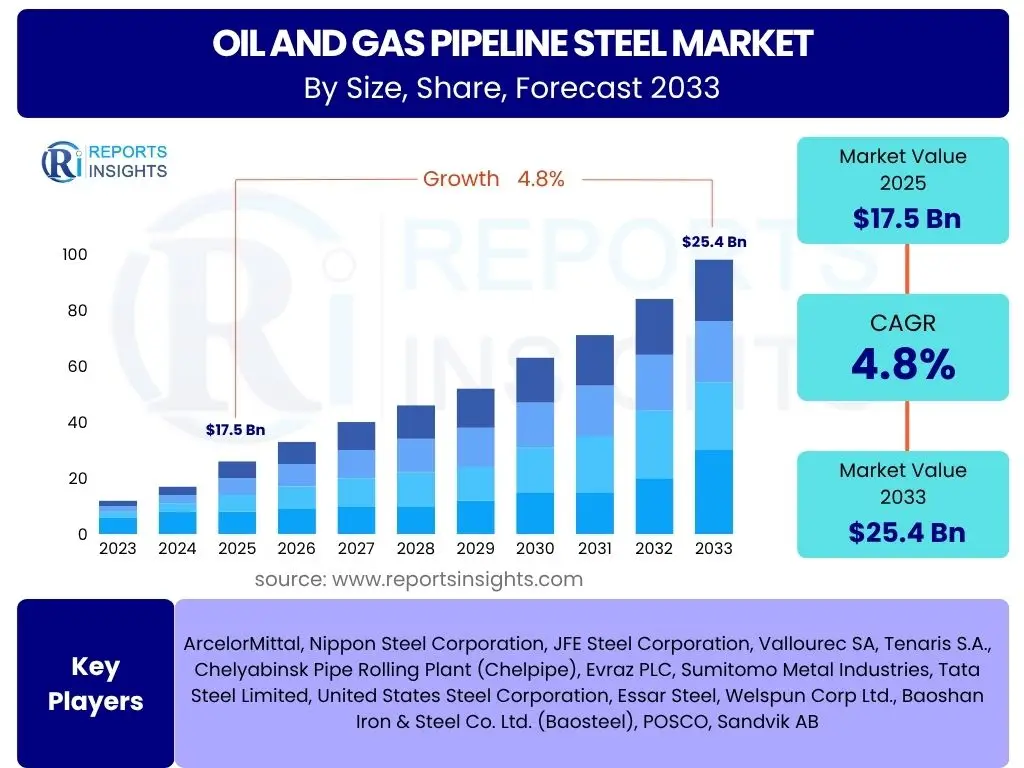

Oil and Gas Pipeline Steel Market Size

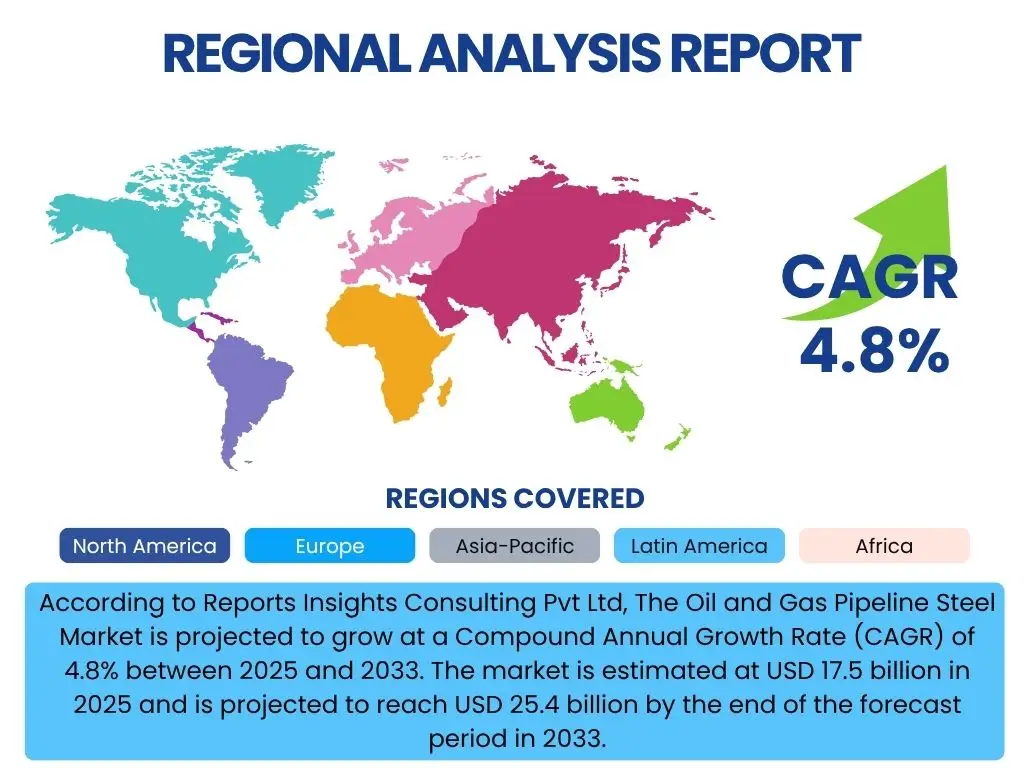

According to Reports Insights Consulting Pvt Ltd, The Oil and Gas Pipeline Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 17.5 billion in 2025 and is projected to reach USD 25.4 billion by the end of the forecast period in 2033.

Key Oil and Gas Pipeline Steel Market Trends & Insights

The Oil and Gas Pipeline Steel market is undergoing significant transformation, driven by a confluence of technological advancements, evolving energy landscapes, and stringent environmental mandates. Common user inquiries often focus on the adoption of high-strength materials, the impact of digitalization on pipeline integrity, and the implications of the global energy transition, particularly the rise of hydrogen and carbon capture infrastructure. These questions highlight a market that is not merely expanding in volume but also innovating in response to complex operational and sustainability demands, pushing for more durable, efficient, and environmentally compliant pipeline solutions.

A key trend involves the increasing demand for high-grade steel, such as X80 and X100, which offers enhanced strength-to-weight ratios, allowing for reduced wall thickness and material consumption while maintaining or improving operational pressures. This contributes to lower construction costs and improved environmental footprints. Furthermore, the industry is witnessing a shift towards smarter pipeline infrastructure, incorporating advanced sensor technologies and real-time monitoring systems to enhance safety, detect anomalies early, and optimize maintenance schedules. This digital integration is crucial for maintaining the integrity of extensive and aging pipeline networks.

Another prominent trend is the growing emphasis on pipelines designed for new energy carriers. As the world transitions towards a low-carbon economy, investments in hydrogen transportation and carbon capture, utilization, and storage (CCUS) infrastructure are gaining momentum. This creates a specialized demand for pipeline steel that can withstand the unique characteristics of these substances, such as hydrogen embrittlement. Concurrently, strict environmental regulations worldwide are compelling pipeline operators to adopt advanced coating technologies and corrosion-resistant materials, reducing leaks and ensuring long-term operational integrity, thereby safeguarding ecological systems.

- Increased adoption of High-Strength Low-Alloy (HSLA) steel grades (e.g., X80, X100) for enhanced efficiency and reduced material usage.

- Integration of advanced coating technologies (e.g., FBE, 3LPE, DUAL FBE) for superior corrosion protection and extended pipeline lifespan.

- Digitalization and smart pipeline solutions, incorporating sensors, IoT, and real-time monitoring for improved integrity management.

- Growing demand for specialized steel grades for new energy carriers like hydrogen and Carbon Capture, Utilization, and Storage (CCUS).

- Emphasis on environmental compliance and safety standards, driving innovation in leak detection and repair technologies.

- Replacement and upgrade of aging pipeline infrastructure in mature regions to enhance operational safety and efficiency.

AI Impact Analysis on Oil and Gas Pipeline Steel

Common user questions regarding AI's impact on the Oil and Gas Pipeline Steel market frequently revolve around its potential to revolutionize operational efficiency, enhance safety, and optimize resource allocation. Users are keen to understand how artificial intelligence can move beyond conventional analytics to provide predictive insights for pipeline integrity, material performance, and supply chain management. There is also significant interest in AI's role in detecting anomalies, improving maintenance strategies, and even influencing the design and manufacturing processes of pipeline steel, thereby fostering a more resilient and responsive industry ecosystem.

Artificial intelligence is poised to significantly enhance pipeline integrity management. AI-powered algorithms can analyze vast datasets from sensor networks, drones, and inspection tools to predict potential failures, corrosion rates, and stress points within pipelines. This predictive maintenance capability allows operators to schedule interventions proactively, minimizing downtime, reducing repair costs, and, most critically, preventing catastrophic incidents. Beyond just detection, AI can optimize the routing and design of new pipelines by simulating various environmental conditions and material stresses, leading to more robust and efficient infrastructure layouts from the outset.

Furthermore, AI is transforming the manufacturing processes of pipeline steel itself. Machine learning models can optimize furnace operations, rolling schedules, and material compositions to achieve desired mechanical properties with greater precision and consistency, reducing waste and improving product quality. In the supply chain, AI can forecast demand, optimize inventory levels, and streamline logistics, ensuring timely delivery of steel products to construction sites and minimizing project delays. This holistic integration of AI, from production to operation, promises a new era of efficiency, safety, and sustainability for the Oil and Gas Pipeline Steel market.

- Enhanced Predictive Maintenance: AI algorithms analyze sensor data and historical trends to forecast potential pipeline failures, enabling proactive repairs and reducing downtime.

- Optimized Inspection and Monitoring: AI-powered drones and robotic systems improve the accuracy and speed of pipeline inspections, detecting anomalies and defects with higher precision.

- Advanced Material Design and Manufacturing: AI can simulate and optimize steel compositions and production processes, leading to the development of stronger, more durable, and cost-effective pipeline materials.

- Improved Supply Chain Efficiency: AI models predict demand fluctuations, optimize inventory management, and streamline logistics for steel procurement and delivery.

- Enhanced Safety and Risk Management: AI assists in real-time risk assessment, identifies high-risk segments, and provides data-driven recommendations to improve operational safety protocols.

Key Takeaways Oil and Gas Pipeline Steel Market Size & Forecast

Common user inquiries about the Oil and Gas Pipeline Steel market size and forecast often aim to identify the primary drivers of growth, significant regional contributions, and the overarching factors influencing long-term market trajectory. Insights reveal that persistent global energy demand, coupled with extensive infrastructure development initiatives and the crucial need for aging pipeline replacement, are fundamental pillars supporting market expansion. The market's future is also intrinsically linked to the energy transition, as new pipelines are required for emerging energy carriers like hydrogen and for carbon capture technologies, signifying a diversification of demand beyond traditional oil and gas transportation.

A significant takeaway is the dual influence of traditional and transitional energy demands. While conventional oil and gas projects continue to drive substantial demand for pipeline steel, the burgeoning investments in cleaner energy infrastructure are opening entirely new avenues for growth. This includes the development of dedicated pipelines for hydrogen, ammonia, and CO2, which necessitate specialized steel grades and construction methodologies. This dual-pronged demand ensures sustained market vitality, albeit with an evolving product mix and technical specifications.

Furthermore, the emphasis on enhancing pipeline integrity and safety through advanced materials and digital solutions is a critical theme. The forecast indicates that investments will increasingly flow into high-strength, corrosion-resistant steel, along with sophisticated monitoring and maintenance technologies. This trend not only reflects regulatory pressures but also a strategic imperative for operators to minimize environmental risks and ensure reliable energy delivery. Geographically, emerging economies in Asia Pacific and the Middle East are expected to drive substantial demand due to rapid industrialization and expansion of energy infrastructure, complementing the ongoing replacement cycles in mature markets.

- Sustained global energy demand, encompassing both conventional hydrocarbons and emerging clean energy sources, underpins consistent market growth.

- Significant investments in new pipeline infrastructure, particularly in developing economies, are a major driver of market expansion.

- The crucial need for replacement and modernization of aging pipeline networks in mature regions ensures a steady demand for pipeline steel.

- Growth is increasingly influenced by the development of pipelines for hydrogen, carbon capture (CCUS), and other transition fuels, diversifying steel demand.

- Technological advancements in steel manufacturing, resulting in higher strength and corrosion resistance, are key to meeting evolving industry standards and environmental regulations.

- Emphasis on enhanced safety, environmental protection, and operational efficiency drives demand for premium, durable pipeline steel products and smart pipeline solutions.

Oil and Gas Pipeline Steel Market Drivers Analysis

The Oil and Gas Pipeline Steel market is fundamentally driven by the escalating global demand for energy, which necessitates the continuous expansion and maintenance of infrastructure for transporting hydrocarbons. Urbanization and industrial growth across developing economies further amplify this demand, as new energy supply routes and distribution networks are critical for economic development. This foundational demand forms the bedrock of the pipeline steel market, ensuring ongoing investment in both new project development and the enhancement of existing systems.

A significant contributing factor is the extensive network of aging pipeline infrastructure in mature oil and gas producing regions, particularly in North America and Europe. Many of these pipelines, some decades old, require substantial replacement and modernization to meet contemporary safety, environmental, and operational standards. This presents a continuous demand cycle for pipeline steel, independent of new field developments, ensuring sustained market activity even during periods of lower oil and gas exploration.

Moreover, the global energy transition, rather than diminishing demand, is creating new drivers. The increasing focus on clean energy solutions, such as hydrogen as a fuel source and carbon capture, utilization, and storage (CCUS) technologies, mandates the construction of specialized pipelines. These new energy carriers require specific steel grades and robust infrastructure, thereby opening new opportunities and diversifying the application spectrum for pipeline steel manufacturers. Government policies and strategic energy security initiatives worldwide also play a pivotal role in accelerating pipeline projects, securing future growth for the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Consumption | +1.5% | Global | Long-term |

| Expansion of Oil & Gas Infrastructure | +1.2% | Asia Pacific, Middle East & Africa | Medium-term |

| Replacement of Aging Infrastructure | +1.0% | North America, Europe | Long-term |

| Growth in Hydrogen & CCUS Pipelines | +0.8% | Europe, North America | Long-term |

Oil and Gas Pipeline Steel Market Restraints Analysis

The Oil and Gas Pipeline Steel market faces significant headwinds from the inherent volatility of crude oil and natural gas prices. Fluctuations in energy commodity prices directly influence the profitability and investment appetite of upstream and midstream companies. Prolonged periods of low prices can lead to deferment or cancellation of new pipeline projects, as well as reduced budgets for maintenance and expansion of existing networks, thereby impacting the demand for pipeline steel. This unpredictability creates a challenging environment for long-term planning and investment within the market.

Another major restraint is the increasing stringency of environmental regulations and growing public opposition to new fossil fuel infrastructure projects. Environmental advocacy groups and local communities often challenge pipeline construction due to concerns about land disturbance, potential spills, and greenhouse gas emissions. This can lead to protracted permitting processes, legal battles, and project delays or cancellations, significantly increasing project costs and timeline uncertainties for pipeline developers, which in turn stifles demand for steel.

Furthermore, the accelerating global transition towards renewable energy sources and the associated decline in long-term demand projections for fossil fuels pose a structural restraint. While pipelines for natural gas may serve as transitional infrastructure, the overall strategic shift away from oil and coal reduces the impetus for extensive new crude oil pipeline networks. High capital expenditures required for pipeline construction, coupled with geopolitical instability in key producing regions, also contribute to market hesitation, compelling companies to exercise caution in new investments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Crude Oil and Natural Gas Price Volatility | -1.3% | Global | Short to Medium-term |

| Strict Environmental Regulations & Opposition | -1.0% | North America, Europe | Long-term |

| Global Shift to Renewable Energy Sources | -0.8% | Global | Long-term |

| High Capital Expenditure for Projects | -0.6% | Global | Long-term |

Oil and Gas Pipeline Steel Market Opportunities Analysis

The burgeoning global emphasis on decarbonization presents a significant opportunity for the Oil and Gas Pipeline Steel market, specifically through the development of infrastructure for hydrogen transportation and Carbon Capture, Utilization, and Storage (CCUS). As nations commit to net-zero emissions, investments in dedicated pipelines for green hydrogen and captured CO2 are projected to surge. This transition creates a new and substantial demand segment for specialized steel grades capable of safely and efficiently handling these new energy carriers, driving material innovation and new project development.

Digitalization and the integration of smart technologies offer another transformative opportunity. The deployment of advanced sensors, IoT devices, artificial intelligence, and big data analytics in pipeline networks enhances operational efficiency, improves safety, and reduces environmental risks. Smart pipelines require steel that can accommodate these technologies, potentially incorporating features for seamless sensor integration or enhanced data transmission. This evolution not only creates demand for new pipelines but also drives upgrades and modernization of existing infrastructure, ensuring long-term market relevance.

Furthermore, the vast and growing energy needs of emerging economies, particularly in Asia Pacific and parts of Africa, represent substantial market expansion opportunities. Rapid industrialization and urbanization in these regions necessitate the construction of extensive new energy infrastructure, including pipelines for oil, gas, and increasingly, imported LNG. Unlike mature markets focused on replacement, these regions offer greenfield project potential, providing significant avenues for growth in pipeline steel demand. Lastly, continuous material science innovations aimed at developing more corrosion-resistant, high-strength, and durable pipeline steels present opportunities for market players to offer premium, value-added products that meet evolving performance and safety standards.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Hydrogen & CCUS Infrastructure Development | +1.8% | Europe, North America, Asia Pacific | Long-term |

| Digitalization & Smart Pipeline Solutions | +1.1% | Global | Medium to Long-term |

| Expansion in Emerging Economies | +0.9% | Asia Pacific, Latin America, Middle East | Long-term |

| Material Science Innovations & Advanced Coatings | +0.8% | Global | Long-term |

Oil and Gas Pipeline Steel Market Challenges Impact Analysis

The Oil and Gas Pipeline Steel market faces a persistent challenge from fluctuations in raw material prices, particularly for iron ore and scrap steel. These primary inputs are subject to global supply-demand dynamics, geopolitical events, and economic cycles, leading to unpredictable and sometimes sharp price swings. Such volatility directly impacts the production costs for steel manufacturers, which can erode profit margins or necessitate price increases for pipeline steel, making projects more expensive and potentially delaying investment decisions by pipeline operators. Managing this cost uncertainty is a continuous hurdle for market players.

Another significant challenge is the increasing scrutiny and stringent regulatory environment governing pipeline construction and operation worldwide. Governments and international bodies are imposing stricter safety, environmental, and operational standards to prevent leaks, spills, and other incidents. Compliance with these evolving regulations often requires significant investment in advanced materials, enhanced quality control, and sophisticated monitoring technologies. The complexity and cost of adhering to these mandates can deter new projects and increase the operational burden for existing infrastructure, affecting market growth.

Furthermore, geopolitical instability and supply chain disruptions pose considerable challenges. Conflicts, trade disputes, and even natural disasters can disrupt the global supply chain for raw materials, specialized components, or finished steel products, leading to delays and increased logistics costs. Skilled labor shortages in specialized welding, pipe laying, and maintenance exacerbate these issues, impacting project execution timelines and overall efficiency. These factors collectively contribute to a complex operating environment, demanding robust risk management strategies from market participants to ensure project viability and timely completion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.0% | Global | Short-term |

| Stringent Safety & Regulatory Compliance | -0.8% | Global | Long-term |

| Supply Chain Disruptions & Geopolitical Risks | -0.7% | Global | Short to Medium-term |

| Skilled Labor Shortages | -0.5% | North America, Europe | Long-term |

Oil and Gas Pipeline Steel Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Oil and Gas Pipeline Steel market, covering its historical performance, current dynamics, and future projections. It examines key market segments, identifies growth drivers, restraints, opportunities, and challenges, and assesses the impact of emerging trends such as digitalization and the energy transition. The report also offers regional insights and profiles leading market players to provide a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.5 Billion |

| Market Forecast in 2033 | USD 25.4 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, JFE Steel Corporation, Vallourec SA, Tenaris S.A., Chelyabinsk Pipe Rolling Plant (Chelpipe), Evraz PLC, Sumitomo Metal Industries, Tata Steel Limited, United States Steel Corporation, Essar Steel, Welspun Corp Ltd., Baoshan Iron & Steel Co. Ltd. (Baosteel), POSCO, Sandvik AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Oil and Gas Pipeline Steel market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of demand patterns, technological shifts, and competitive landscapes across various product types, manufacturing processes, applications, and regional specificities. Understanding these segments is crucial for stakeholders to identify niche opportunities, allocate resources efficiently, and formulate targeted business strategies within this complex industry.

The segmentation by manufacturing process differentiates between Electric Resistance Welded (ERW), Submerged Arc Welded (SAW), and Seamless pipes. ERW pipes are typically used for smaller diameters and lower pressure applications, offering cost-effectiveness. SAW pipes, encompassing Longitudinal SAW (LSAW) and Spiral SAW (SSAW), are preferred for large-diameter, high-pressure, and long-distance pipelines due to their superior strength and ductility. Seamless pipes, produced without a weld, offer exceptional integrity and are ideal for critical applications requiring high pressure and temperature resistance. Each process caters to distinct operational demands and project requirements, influencing material specifications and market share.

Further segmentation by application highlights the diverse end-uses of pipeline steel, including oil and gas transportation, as well as emerging sectors like hydrogen and carbon capture pipelines. The demand for specific steel grades and pipe dimensions varies significantly depending on the fluid being transported, its pressure, temperature, and corrosive properties. For instance, hydrogen pipelines require steel resistant to embrittlement, while carbon capture pipelines may need different specifications for CO2 transport. Moreover, segmentation by end-use location, distinguishing between onshore and offshore projects, reveals varying construction complexities, regulatory requirements, and cost structures, which directly impact the choice of materials and project scale. This detailed breakdown ensures a comprehensive market overview, allowing for a nuanced understanding of industry dynamics.

- By Manufacturing Process:

- Electric Resistance Welded (ERW): Often used for small to medium diameter pipelines, known for cost-effectiveness and good dimensional accuracy.

- Submerged Arc Welded (SAW):

- Longitudinal Submerged Arc Welded (LSAW): Preferred for large diameter, high-pressure long-distance pipelines due to excellent strength and toughness.

- Spiral Submerged Arc Welded (SSAW): Cost-effective for large diameters, allowing for flexibility in manufacturing pipe lengths.

- Seamless: Produced without a weld, offering superior integrity for high-pressure, high-temperature, and critical applications.

- By Product Type:

- Line Pipe: Primary segment for oil, gas, and product transmission over long distances.

- Flowline: Connects wellheads to gathering facilities.

- Riser Pipe: Used in offshore applications to connect subsea pipelines to platforms.

- By Diameter:

- Small Diameter (Below 24 inches): Typically used for distribution networks, gathering lines, and specialized applications.

- Large Diameter (24 inches and above): Predominantly used for long-distance transmission pipelines carrying significant volumes.

- By Material Grade:

- API 5L Grades: Ranging from lower strength (A, B, X42) to high-strength (X70, X80, X100, X120), suited for various pressure and environmental conditions.

- Other Grades: Including proprietary grades developed for specific applications like sour service or extremely low temperatures.

- By Application:

- Oil Pipelines: Crude oil and refined petroleum products.

- Gas Pipelines: Natural gas transmission and distribution.

- Refinery Pipelines: Internal refinery processes.

- Biofuel Pipelines: Transportation of biofuels.

- Hydrogen Pipelines: Dedicated infrastructure for hydrogen transport.

- Carbon Capture Pipelines: For transporting captured CO2 for storage or utilization.

- By End-Use Location:

- Onshore: Extensive networks across land, often involving diverse terrains.

- Offshore:

- Shallow Water: Pipelines in continental shelf areas.

- Deepwater: Projects in significant water depths requiring specialized laying techniques.

- Ultra-Deepwater: Extreme depths, demanding highly robust and corrosion-resistant materials.

Regional Highlights

- North America: The North American market for oil and gas pipeline steel is characterized by a mature energy infrastructure and significant ongoing investments in the replacement and modernization of aging pipelines. The region's vast existing network, coupled with shale oil and gas production, drives consistent demand. Additionally, increasing regulatory scrutiny on pipeline safety and environmental performance necessitates the adoption of high-strength, corrosion-resistant steel grades and advanced inspection technologies. The emerging focus on hydrogen and CCUS projects, particularly in the U.S. and Canada, presents new growth avenues for specialized pipeline steel, though regulatory complexities and environmental opposition remain notable challenges.

- Europe: Europe's Oil and Gas Pipeline Steel market is heavily influenced by the region's ambitious decarbonization targets and energy security imperatives. While new long-distance conventional oil and gas pipelines may face headwinds, the demand for natural gas infrastructure remains significant for energy transition purposes. A primary driver in Europe is the extensive development of hydrogen backbone networks and carbon capture infrastructure, requiring specialized steel grades capable of handling these novel substances. The region is at the forefront of investing in green hydrogen production and transport, leading to unique material requirements and research initiatives.

Stringent environmental regulations and a strong public desire for sustainable energy solutions mean that any new pipeline projects, or upgrades to existing ones, must adhere to the highest environmental and safety standards. This translates into a preference for advanced coating technologies and materials that minimize environmental impact and maximize operational lifespan. The emphasis on cross-border energy interconnectivity, particularly for gas and future hydrogen flows, also sustains demand for high-quality pipeline steel across the continent.

Furthermore, the decommissioning and repurposing of old fossil fuel infrastructure, alongside the development of new energy hubs, create a dynamic market. Northern European countries, in particular, are pioneering projects for offshore wind integration and associated hydrogen production, which will necessitate significant investments in connecting infrastructure, including subsea pipelines made from advanced steel. This evolving energy landscape positions Europe as a critical market for high-performance and future-proof pipeline steel solutions.

- Asia Pacific (APAC): The Asia Pacific region represents the largest and fastest-growing market for Oil and Gas Pipeline Steel, driven by surging energy demand, rapid industrialization, and extensive infrastructure development across economies like China, India, and Southeast Asian nations. These countries are heavily investing in expanding their energy access and distribution networks, including substantial cross-country and intra-country oil and gas pipelines, as well as LNG regasification terminals and associated pipelines.

Urbanization and economic growth are directly translating into increased energy consumption, necessitating vast new pipeline projects to transport fuels from production centers or import terminals to industrial and residential areas. While the region is also investing in renewables, the foundational demand for conventional oil and gas remains robust, particularly for base load power and industrial feedstock. This creates a continuous need for high volumes of pipeline steel, often sourced domestically or from other regional suppliers, making it a highly competitive market.

Key initiatives include China's continued pipeline build-out for natural gas import and distribution, India's ambitious national gas grid expansion, and various inter-regional energy connectivity projects. The sheer scale of development projects, coupled with a focus on improving energy security, positions APAC as the primary growth engine for the global pipeline steel market over the forecast period. The increasing adoption of higher-grade steels for these projects also reflects a growing emphasis on safety and operational efficiency within the region.

- Latin America: The Latin American Oil and Gas Pipeline Steel market is significantly influenced by the region's substantial hydrocarbon reserves, particularly in countries like Brazil, Argentina (Vaca Muerta shale play), and Mexico. Investment in pipeline infrastructure is primarily driven by the need to transport crude oil and natural gas from production fields to processing facilities, export terminals, and industrial consumption centers. Economic fluctuations and political stability can impact project timelines and foreign investment, but the underlying need for energy infrastructure remains strong.

Projects aimed at enhancing domestic energy supply, reducing reliance on imports, and boosting export capabilities are key drivers. For instance, the development of shale gas fields in Argentina requires extensive gathering and transmission pipeline networks. Similarly, Mexico's energy reforms and growing industrial demand necessitate upgrades and expansions to its gas pipeline grid. Brazil, with its deepwater pre-salt discoveries, drives demand for subsea pipeline steel and related infrastructure.

Despite challenges related to financing and regulatory frameworks, the long-term potential for pipeline steel in Latin America is positive, especially as economic stability improves and energy demand continues to rise. The region's focus on unlocking its vast resource potential means that pipeline development will remain a critical component of its energy strategy, ensuring a steady demand for various types of pipeline steel.

- Middle East and Africa (MEA): The Middle East and Africa represent a critical region for the Oil and Gas Pipeline Steel market, primarily due to the Middle East's role as a major global hydrocarbon producer and Africa's burgeoning energy needs and resource discoveries. In the Middle East, substantial investments are being made in upgrading existing oil and gas infrastructure, expanding production capacities, and developing new export routes. Large-scale projects, including cross-border pipelines and those connecting new oil and gas fields, are constant drivers of demand for high-quality pipeline steel.

Countries like Saudi Arabia, UAE, Qatar, and Iraq are undertaking significant projects to enhance their energy infrastructure, focusing on both crude oil and natural gas production and export. The region is also exploring opportunities in hydrogen and CCUS, which could further diversify the demand for pipeline steel. Given the harsh operating environments, there is a strong emphasis on corrosion-resistant and durable steel grades to ensure long-term operational integrity and safety.

In Africa, new oil and gas discoveries, particularly in East and West Africa, are fueling demand for new pipeline construction to bring resources to market. Countries like Nigeria, Mozambique, Tanzania, and Uganda are planning or undertaking significant pipeline projects for both domestic consumption and export. While financing and political stability can pose challenges, the continent's immense untapped energy potential ensures that it will remain a significant and growing market for pipeline steel as infrastructure development continues to accelerate across the region.

The United States leads demand in North America due to its extensive network of existing pipelines requiring upgrades and new projects to connect burgeoning production areas. Canada also contributes significantly, driven by its vast oil sands and natural gas resources, along with ongoing pipeline expansions to facilitate exports. Both countries are exploring carbon capture and hydrogen transportation, creating opportunities for the market to diversify beyond traditional oil and gas. The emphasis on pipeline integrity management and the implementation of stringent safety regulations further stimulate demand for higher-grade and more durable steel products.

Investment trends in the region indicate a shift towards optimizing existing assets, enhancing environmental compliance, and exploring pathways for new energy carriers. While growth in conventional oil and gas pipeline construction might moderate compared to historical peaks, the demand for sophisticated steel solutions for maintenance, integrity management, and next-generation energy infrastructure is set to remain robust. This makes North America a key market for innovations in pipeline steel technology and services.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Oil and Gas Pipeline Steel Market.- ArcelorMittal

- Nippon Steel Corporation

- JFE Steel Corporation

- Vallourec SA

- Tenaris S.A.

- Chelyabinsk Pipe Rolling Plant (Chelpipe)

- Evraz PLC

- Sumitomo Metal Industries

- Tata Steel Limited

- United States Steel Corporation

- Essar Steel

- Welspun Corp Ltd.

- Baoshan Iron & Steel Co. Ltd. (Baosteel)

- POSCO

- Sandvik AB

- Jindal SAW Ltd.

- Borusan Mannesmann Boru Sanayi ve Ticaret A.S.

- Saarstahl AG

- Sutorp GmbH

- APL Apollo Tubes Limited

Frequently Asked Questions

Analyze common user questions about the Oil and Gas Pipeline Steel market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary factor driving the Oil and Gas Pipeline Steel market growth?

The primary driver is the sustained global demand for energy, encompassing both conventional oil and gas, and emerging energy carriers like hydrogen, necessitating continuous expansion and maintenance of transportation infrastructure. Additionally, the critical need to replace aging pipeline networks in mature regions significantly contributes to market growth.

How do environmental regulations impact the Oil and Gas Pipeline Steel market?

Environmental regulations impose stricter standards for pipeline construction and operation, leading to increased demand for high-strength, corrosion-resistant steel, advanced coatings, and real-time monitoring technologies. While potentially increasing project costs and complexity, these regulations drive innovation and ensure greater safety and environmental protection.

What role does Artificial Intelligence (AI) play in the pipeline steel industry?

AI is increasingly vital for predictive maintenance, defect detection, and optimizing inspection processes for pipelines, enhancing operational efficiency and safety. It also aids in the advanced design of new steel materials and optimizes manufacturing processes, contributing to superior product quality and reduced waste.

Which regions are expected to exhibit the most significant growth in the Oil and Gas Pipeline Steel market?

The Asia Pacific (APAC) region, driven by rapid industrialization and surging energy demand in countries like China and India, is projected to be the largest and fastest-growing market. The Middle East and Africa (MEA) also show strong growth due to extensive hydrocarbon production and infrastructure development projects.

How is the transition to cleaner energy sources affecting the demand for pipeline steel?

The energy transition is creating new demand segments for specialized pipeline steel. While conventional oil and gas pipelines remain crucial, there's a growing need for pipelines designed to transport hydrogen, ammonia, and captured CO2 (for CCUS), diversifying the market and driving innovation in material properties.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted