Polyelectrolyte Market

Polyelectrolyte Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709498 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

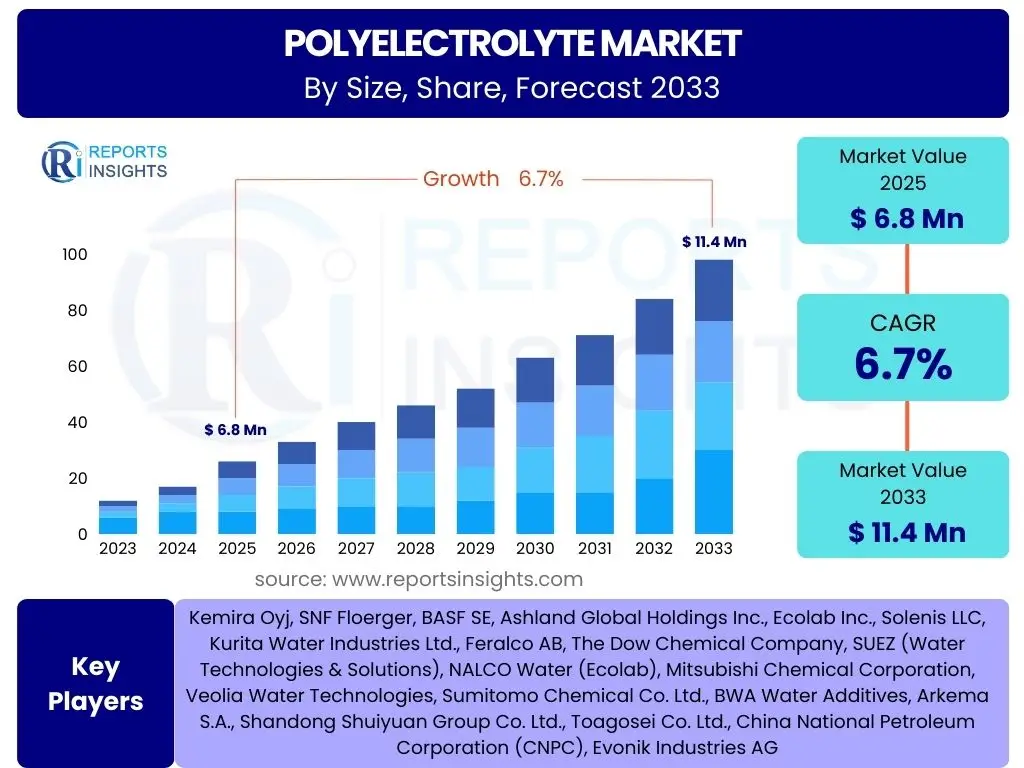

Polyelectrolyte Market Size

According to Reports Insights Consulting Pvt Ltd, The Polyelectrolyte Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 11.4 Billion by the end of the forecast period in 2033. This growth trajectory is significantly influenced by increasing global demand for advanced water and wastewater treatment solutions, alongside expanding applications in various industrial sectors. The market expansion is also propelled by ongoing technological advancements in polymer chemistry, leading to the development of more efficient and environmentally friendly polyelectrolyte formulations.

The consistent rise in industrialization and urbanization globally contributes to a greater volume of wastewater requiring treatment, thereby fueling the demand for polyelectrolytes. Furthermore, stringent environmental regulations imposed by governments worldwide to control pollution and promote sustainable practices are compelling industries to adopt effective treatment chemicals. This regulatory landscape acts as a significant catalyst for market growth, ensuring continuous investment in polyelectrolyte technologies to meet compliance standards and achieve operational efficiency.

Key Polyelectrolyte Market Trends & Insights

The polyelectrolyte market is undergoing significant transformation, driven by a confluence of environmental imperatives, technological advancements, and evolving industrial requirements. Common inquiries from users often center on the sustainability aspects, the shift towards bio-based solutions, and the impact of digital technologies on production and application. Industry stakeholders are particularly keen on understanding how these trends will shape demand, influence product development, and redefine competitive landscapes over the forecast period. The market is increasingly prioritizing solutions that offer both high performance and reduced environmental footprint, aligning with global sustainability goals and consumer preferences.

A notable trend involves the development of specialized polyelectrolytes tailored for specific, challenging applications, such as enhanced oil recovery in mature oilfields or highly selective separation processes in industrial settings. This customization addresses the need for greater efficiency and cost-effectiveness, moving beyond generic solutions. Furthermore, the integration of advanced analytical techniques and process monitoring systems is optimizing polyelectrolyte dosage and performance, leading to more efficient resource utilization and reduced operational costs for end-users. These innovations are critical for maintaining competitive edge and expanding market reach in diverse sectors.

- Increasing adoption of bio-based and sustainable polyelectrolytes.

- Growing demand for high-performance polyelectrolytes in niche applications.

- Development of smart polyelectrolyte systems with enhanced responsiveness.

- Shift towards integrated water management solutions incorporating polyelectrolytes.

- Technological advancements in manufacturing processes leading to cost reduction and efficiency.

AI Impact Analysis on Polyelectrolyte

The integration of Artificial Intelligence (AI) across various industrial sectors is rapidly transforming traditional processes, and the polyelectrolyte market is no exception. User questions frequently revolve around how AI can enhance the efficiency of polyelectrolyte applications, optimize formulation development, and streamline supply chains. There is significant interest in AI's potential to address complex challenges such as predictive maintenance of treatment systems, real-time dosage optimization, and the discovery of novel polymer structures. The overarching expectation is that AI will unlock new levels of precision, cost-effectiveness, and environmental sustainability in polyelectrolyte-dependent operations.

AI's influence extends beyond mere process optimization; it is also anticipated to accelerate research and development cycles. Machine learning algorithms can analyze vast datasets of chemical properties, reaction pathways, and performance metrics to predict the efficacy of new polyelectrolyte formulations, significantly reducing the need for extensive physical experimentation. This capability not only shortens time-to-market for innovative products but also allows for the development of highly customized solutions that meet very specific industrial requirements. Furthermore, AI-driven analytics can provide insights into market trends and customer needs, guiding strategic product development and positioning.

- Enhanced process optimization for polyelectrolyte dosage and application in water treatment plants.

- Accelerated discovery and development of novel polyelectrolyte formulations with desired properties.

- Predictive maintenance and fault detection in systems using polyelectrolytes, reducing downtime.

- Optimized supply chain management and inventory control for raw materials and finished products.

- Improved quality control and performance monitoring of polyelectrolyte solutions.

Key Takeaways Polyelectrolyte Market Size & Forecast

The polyelectrolyte market is poised for robust growth, driven by escalating demand for water and wastewater treatment, coupled with expansion in various industrial sectors. Users frequently inquire about the primary growth drivers, the most promising application areas, and the overarching implications for market participants regarding investment and strategic planning. The market's resilience is evident in its ability to adapt to stringent environmental regulations and the increasing global focus on resource efficiency. Key insights suggest that innovation in sustainable and high-performance polyelectrolyte solutions will be crucial for capturing future market share.

Furthermore, the forecast indicates a sustained emphasis on research and development to address complex industrial challenges and environmental concerns. Emerging economies, particularly in Asia Pacific and Latin America, are expected to present significant growth opportunities due to rapid industrialization and improving infrastructure. Stakeholders must consider the regional nuances in regulatory frameworks and application needs to effectively penetrate and expand within these diverse markets. Strategic partnerships and targeted product development will be essential for capitalizing on these regional growth pockets.

- Significant market expansion driven by global water scarcity and environmental regulations.

- Strong growth potential in developing economies due to rapid industrialization and urbanization.

- Increasing focus on sustainable and bio-based polyelectrolyte solutions.

- Water and wastewater treatment remains the largest and fastest-growing application segment.

- Technological advancements in polymer chemistry are critical for competitive differentiation.

Polyelectrolyte Market Drivers Analysis

The global polyelectrolyte market is primarily propelled by the escalating demand for advanced water and wastewater treatment solutions across municipal and industrial sectors. With increasing population density and industrial activities, the generation of wastewater has surged, necessitating efficient treatment methods to meet stringent discharge standards and address water scarcity issues. Polyelectrolytes play a critical role in coagulation, flocculation, and sludge dewatering processes, making them indispensable for effective water management. This fundamental need forms a robust foundation for sustained market growth.

Another significant driver is the expansion of key end-use industries, including oil and gas, pulp and paper, mining, and personal care. In the oil and gas sector, polyelectrolytes are crucial for enhanced oil recovery (EOR), drilling fluid additives, and produced water treatment. The pulp and paper industry utilizes them for retention, drainage, and effluent treatment. The mining sector relies on polyelectrolytes for mineral processing and tailings management. The continuous growth and technological advancements within these industries translate directly into higher consumption of polyelectrolytes, supporting the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Water & Wastewater Treatment | +2.8% | Global, particularly Asia Pacific, Europe, North America | Long-term |

| Stringent Environmental Regulations | +1.9% | Europe, North America, China, India | Medium to Long-term |

| Expansion of Industrial Applications (Oil & Gas, Pulp & Paper, Mining) | +1.5% | Asia Pacific, North America, Middle East & Africa | Medium-term |

| Technological Advancements in Polymer Chemistry | +0.5% | Global | Medium to Long-term |

Polyelectrolyte Market Restraints Analysis

Despite robust growth prospects, the polyelectrolyte market faces several significant restraints that could impede its expansion. One primary concern is the price volatility of raw materials, such as acrylic acid, acrylamide, and ethylene. These petrochemical-derived feedstocks are subject to fluctuations in crude oil prices and supply chain disruptions, directly impacting the manufacturing costs of polyelectrolytes. Such price instability can erode profit margins for manufacturers and lead to unpredictable pricing for end-users, potentially slowing adoption or encouraging the search for alternative solutions. Managing these input costs remains a persistent challenge for market players.

Another notable restraint is the increasing environmental scrutiny and concerns regarding the biodegradability and ecotoxicity of synthetic polyelectrolytes. While highly effective in their applications, some conventional polyelectrolytes have raised questions about their long-term environmental impact. This has led to stricter regulatory frameworks in certain regions, compelling manufacturers to invest in research and development for more eco-friendly, bio-based, and biodegradable alternatives. The transition towards sustainable options, while beneficial in the long run, presents initial investment costs and technological hurdles that can act as short-to-medium-term restraints on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Volatility of Raw Materials | -1.2% | Global | Medium-term |

| Environmental Concerns & Stringent Regulations on Synthetic Polymers | -0.9% | Europe, North America | Long-term |

| Availability of Alternative Treatment Technologies | -0.6% | Global | Medium-term |

| High Capital Investment for Manufacturing Facilities | -0.3% | Developing Economies | Long-term |

Polyelectrolyte Market Opportunities Analysis

The polyelectrolyte market is ripe with opportunities, particularly driven by the accelerating shift towards sustainable and bio-based solutions. As environmental consciousness grows and regulatory pressures intensify, there is a burgeoning demand for polyelectrolytes derived from renewable resources that offer biodegradability and reduced ecological impact. This trend presents a significant avenue for innovation and market differentiation, allowing companies to cater to environmentally conscious industries and align with global sustainability goals. Investment in green chemistry and novel bio-polymer research is expected to unlock substantial market potential in this segment.

Furthermore, the expansion into emerging applications and untapped markets represents another key opportunity. Polyelectrolytes are finding new uses in sectors such as cosmetics, pharmaceuticals, food processing, and agriculture, where their unique properties can enhance product performance or process efficiency. Geographically, rapidly industrializing regions in Asia Pacific, Latin America, and Africa offer substantial growth prospects due to increasing infrastructure development, burgeoning manufacturing sectors, and rising demand for effective water management solutions. Strategic penetration into these regions, coupled with localized product development, can unlock significant revenue streams and broaden the overall market footprint for polyelectrolyte manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Biodegradable Polyelectrolytes | +1.5% | Global | Long-term |

| Emerging Applications in New Industries (e.g., Personal Care, Food & Beverage) | +1.0% | North America, Europe, Asia Pacific | Medium to Long-term |

| Market Expansion in Developing Economies | +0.8% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Advancements in Smart Polymer Technologies | +0.4% | Global | Long-term |

Polyelectrolyte Market Challenges Impact Analysis

The polyelectrolyte market faces several significant challenges that could hinder its growth and operational efficiency. One of the primary hurdles is the complex and evolving regulatory landscape governing chemical manufacturing and discharge, particularly concerning environmental protection and safety standards. Different regions and countries have varying regulations on chemical use, waste disposal, and product safety, which complicates market entry and necessitates substantial investment in compliance. Adapting to these diverse and frequently updated regulations can be costly and time-consuming, affecting product development cycles and market expansion strategies for manufacturers.

Another key challenge involves the intense competition from established players and the presence of alternative treatment technologies. The market is characterized by several large, integrated chemical companies that possess significant R&D capabilities and global distribution networks. This competitive intensity can make it difficult for new entrants or smaller players to gain market share. Furthermore, while polyelectrolytes are highly effective, alternative physical, biological, or membrane-based treatment methods sometimes offer competitive advantages in specific scenarios, posing a threat to the market dominance of chemical solutions. Continuous innovation and differentiation are therefore crucial for maintaining competitive edge in this dynamic environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Varied Regulatory Frameworks | -1.0% | Global, particularly Europe, North America | Long-term |

| Intense Competition and Market Consolidation | -0.8% | Global | Medium-term |

| Disposal and Waste Management Issues of Polymer-containing Sludge | -0.7% | Global | Long-term |

| Demand for Cost-Effective and High-Performance Solutions | -0.5% | Developing Economies | Medium-term |

Polyelectrolyte Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global polyelectrolyte market, offering detailed insights into market size, growth trends, competitive landscape, and key segments. It covers the historical performance from 2019 to 2023, establishes the base year in 2024, and provides forward-looking projections up to 2033. The report segments the market by product type, form, application, and end-use industry, providing a granular view of market dynamics. Furthermore, it includes an extensive analysis of regional market trends and profiles leading companies to offer a holistic understanding of the industry landscape. The scope emphasizes the latest technological advancements, regulatory impacts, and emerging opportunities shaping the future of the polyelectrolyte sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 11.4 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kemira Oyj, SNF Floerger, BASF SE, Ashland Global Holdings Inc., Ecolab Inc., Solenis LLC, Kurita Water Industries Ltd., Feralco AB, The Dow Chemical Company, SUEZ (Water Technologies & Solutions), NALCO Water (Ecolab), Mitsubishi Chemical Corporation, Veolia Water Technologies, Sumitomo Chemical Co. Ltd., BWA Water Additives, Arkema S.A., Shandong Shuiyuan Group Co. Ltd., Toagosei Co. Ltd., China National Petroleum Corporation (CNPC), Evonik Industries AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global polyelectrolyte market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper analysis of market trends, growth drivers, and opportunities across various product types, forms, applications, and end-use industries. Understanding these segments is crucial for strategic decision-making, allowing stakeholders to identify high-growth areas and tailor their product offerings to specific market needs. The analysis also highlights the varying demands and adoption rates of polyelectrolytes across different industrial sectors and geographical regions, underscoring the market's complexity and vast potential.

The market is predominantly segmented by the chemical nature of polyelectrolytes, distinguishing between anionic, cationic, non-ionic, and amphoteric types, each offering unique properties suitable for different applications. The physical form, whether liquid or powder, also plays a significant role in market preferences based on ease of handling, storage, and dosage requirements. Furthermore, the segmentation by application, with water and wastewater treatment being the largest segment, provides insights into the primary consumption areas, while end-use industries categorize the market based on the ultimate consumers of polyelectrolyte products. This multi-dimensional segmentation ensures a granular and accurate assessment of the market landscape.

- By Type:

- Anionic Polyelectrolytes: Widely used for municipal and industrial wastewater treatment, particularly for solids removal and sludge dewatering.

- Cationic Polyelectrolytes: Essential for primary clarification, sludge conditioning, and improving drainage in paper production.

- Non-ionic Polyelectrolytes: Utilized in specific applications where charge neutrality is preferred, such as high shear environments or certain mining processes.

- Amphoteric Polyelectrolytes: Offer versatility across a range of pH conditions, finding applications in personal care and specialized industrial processes.

- By Form:

- Liquid: Preferred for ease of handling and automated dosing in large-scale operations.

- Powder: Offers advantages in terms of storage and transportation costs, often requiring on-site dissolution.

- By Application:

- Water & Wastewater Treatment: Dominant application, crucial for flocculation, coagulation, and sludge dewatering.

- Oil & Gas: Used in drilling fluids, enhanced oil recovery, and produced water treatment.

- Pulp & Paper: Improves retention, drainage, and paper strength, also used in effluent treatment.

- Mining: Key for mineral processing, tailings management, and water recovery.

- Personal Care: Employed as thickeners, binders, and film-formers in cosmetics and hygiene products.

- Textile: Used in dyeing processes and wastewater treatment from textile manufacturing.

- Others (Agriculture, Food Processing): Emerging applications in soil conditioning, crop protection, and food product formulation.

- By End-Use Industry:

- Municipal: Public sector water treatment plants for potable water and sewage.

- Industrial: Manufacturing, energy, mining, and other industries requiring process water and effluent treatment.

Regional Highlights

- North America: This region represents a mature market with significant demand for polyelectrolytes, driven by stringent environmental regulations, particularly for industrial wastewater treatment and municipal water purification. The presence of a robust oil and gas industry also contributes significantly to market consumption. The United States and Canada are key markets, characterized by technological advancements and high adoption rates of specialized polyelectrolyte solutions.

- Europe: Europe is another key market, emphasizing sustainable practices and advanced wastewater treatment technologies. Strict regulations governing chemical use and water discharge propel the demand for high-performance and eco-friendly polyelectrolytes. Germany, France, and the UK are prominent countries, focusing on innovation in bio-based polyelectrolytes and circular economy initiatives within the water sector.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing region, fueled by rapid industrialization, urbanization, and increasing investment in infrastructure development. Countries like China and India are experiencing a surge in demand for water treatment solutions due to growing population and industrial expansion. The region also presents significant opportunities in the pulp and paper, textile, and mining industries.

- Latin America: This region exhibits a steady growth trajectory, primarily driven by increasing industrial activities, especially in mining and oil and gas sectors, and the ongoing development of water and wastewater treatment infrastructure. Brazil and Mexico are leading markets, with growing environmental awareness and rising demand for effective water management solutions.

- Middle East & Africa (MEA): The MEA region is characterized by high water scarcity, which drives substantial investments in desalination and industrial water treatment. The booming oil and gas industry in the Middle East is a significant consumer of polyelectrolytes for various applications. South Africa and Saudi Arabia are key contributors to market growth, focusing on robust water infrastructure development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyelectrolyte Market.- Kemira Oyj

- SNF Floerger

- BASF SE

- Ashland Global Holdings Inc.

- Ecolab Inc.

- Solenis LLC

- Kurita Water Industries Ltd.

- Feralco AB

- The Dow Chemical Company

- SUEZ (Water Technologies & Solutions)

- NALCO Water (Ecolab)

- Mitsubishi Chemical Corporation

- Veolia Water Technologies

- Sumitomo Chemical Co. Ltd.

- BWA Water Additives

- Arkema S.A.

- Shandong Shuiyuan Group Co. Ltd.

- Toagosei Co. Ltd.

- China National Petroleum Corporation (CNPC)

- Evonik Industries AG

Frequently Asked Questions

What are polyelectrolytes and what are their primary uses?

Polyelectrolytes are polymers whose repeating units bear an electrolyte group, meaning they can dissociate into charged ions in aqueous solutions. Their primary uses include water and wastewater treatment for flocculation, coagulation, and sludge dewatering, as well as applications in the oil and gas, pulp and paper, mining, and personal care industries, where they act as thickeners, dispersants, or retention aids.

What are the different types of polyelectrolytes available in the market?

Polyelectrolytes are primarily categorized into four types based on the charge of their dissociating groups: anionic (negatively charged), cationic (positively charged), non-ionic (uncharged but still polymeric), and amphoteric (containing both positive and negative charges). Each type offers specific properties and is suited for different applications depending on the charge of the particles to be treated and the environmental conditions.

Which factors are driving the growth of the polyelectrolyte market?

The market growth is primarily driven by the increasing global demand for effective water and wastewater treatment solutions due to water scarcity and pollution. Stringent environmental regulations, rapid industrialization, and expanding applications in diverse sectors such as oil & gas, pulp & paper, and personal care also contribute significantly to market expansion.

What are the key challenges facing the polyelectrolyte industry?

Key challenges include the price volatility of raw materials, which impacts manufacturing costs, and increasing environmental concerns regarding the biodegradability and ecotoxicity of synthetic polyelectrolytes. Additionally, complex and varied regulatory frameworks across regions and intense market competition from established players pose significant hurdles.

What are the emerging opportunities in the polyelectrolyte market?

Significant opportunities arise from the development of bio-based and biodegradable polyelectrolytes that align with sustainability goals. Furthermore, market expansion into emerging applications within new industries like cosmetics and agriculture, coupled with growth in rapidly industrializing economies, presents substantial prospects for manufacturers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted