Polycarbonate Resin Market

Polycarbonate Resin Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707199 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

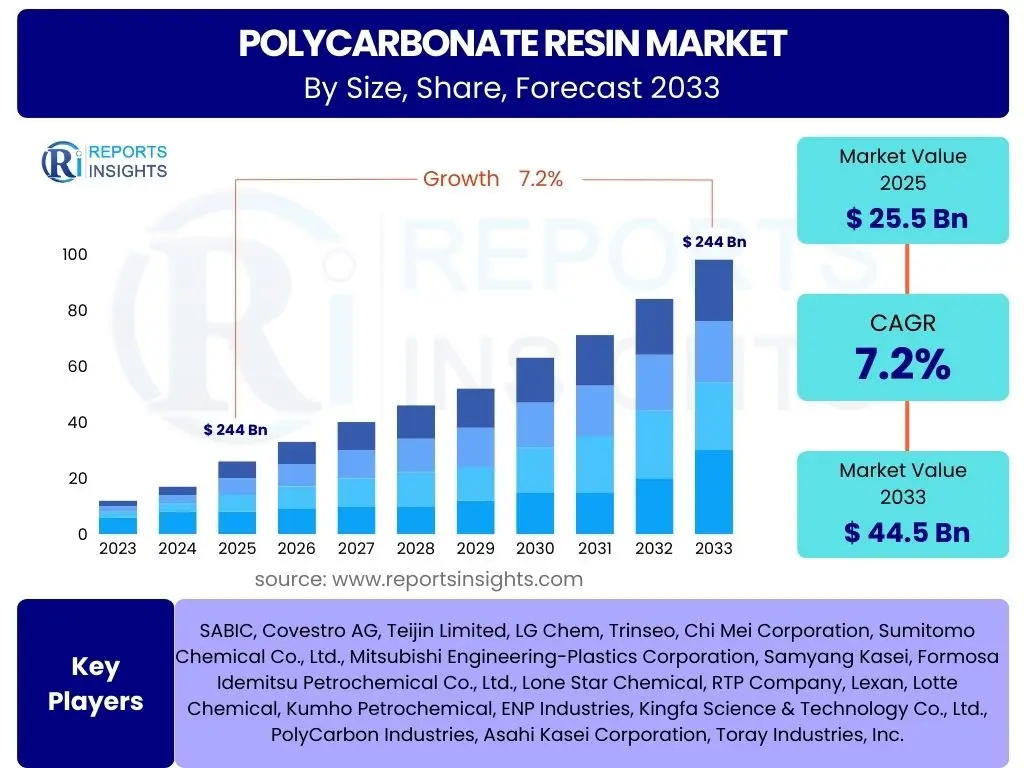

Polycarbonate Resin Market Size

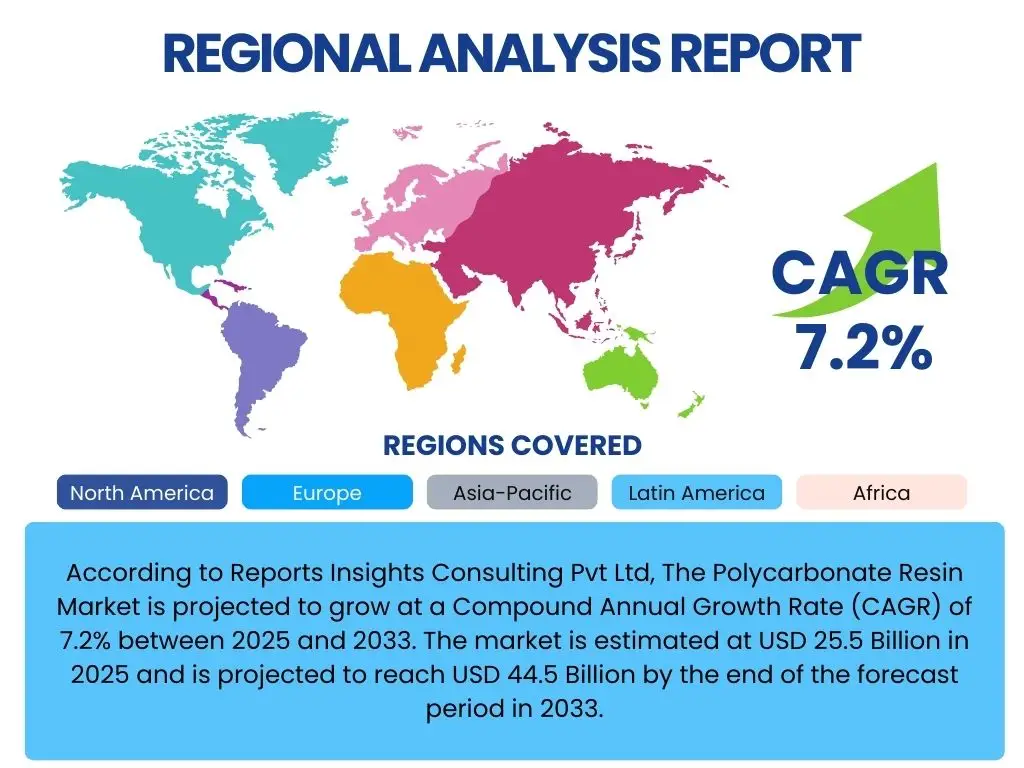

According to Reports Insights Consulting Pvt Ltd, The Polycarbonate Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 44.5 Billion by the end of the forecast period in 2033.

Key Polycarbonate Resin Market Trends & Insights

Common user questions regarding market trends in polycarbonate resin often revolve around the adoption of sustainable materials, the impact of lightweighting initiatives in key industries, and the expansion into new application areas. Users frequently inquire about the shift towards bio-based and recycled polycarbonate grades driven by environmental regulations and consumer demand for eco-friendly products. Another significant area of interest is the increasing use of polycarbonate in electric vehicles (EVs) and advanced electronics, where its unique properties offer considerable advantages over traditional materials. The market is also seeing a surge in demand for high-performance grades suitable for medical devices and optical applications, requiring enhanced purity and optical clarity.

The market landscape is dynamically evolving with innovations in manufacturing processes and material formulations, addressing performance requirements and sustainability goals. There is a growing emphasis on circular economy principles, leading to increased investment in chemical recycling technologies for polycarbonate. Furthermore, the integration of smart features in consumer electronics and automotive components necessitates advanced polycarbonate solutions that can accommodate sophisticated designs and functionalities. Geopolitical factors and supply chain resilience are also shaping market trends, with a focus on diversifying sourcing and localized production to mitigate risks. The expansion of 5G infrastructure globally is creating new avenues for polycarbonate in telecommunications equipment, demanding materials with superior dielectric properties.

- Growing Adoption of Bio-based and Recycled Polycarbonate: Increasing environmental consciousness and stringent regulations are driving demand for sustainable polycarbonate options, leading to innovations in production methods.

- Lightweighting Trend in Automotive and Aerospace: The imperative to improve fuel efficiency and reduce emissions is accelerating the adoption of polycarbonate for vehicle components, replacing heavier materials.

- Expansion in Consumer Electronics: The continuous evolution of smartphones, laptops, and wearables necessitates high-performance, durable, and aesthetically versatile polycarbonate for casings and displays.

- Rising Demand from the Healthcare Sector: Polycarbonate's sterilizability, biocompatibility, and clarity make it ideal for medical devices, drug delivery systems, and diagnostic equipment.

- Advancements in Optical Applications: Superior optical properties are fueling demand in LED lighting, lenses, and transparent panels, particularly in architectural and automotive glazing.

- Innovation in Flame Retardant Grades: Increasing safety standards, especially in construction and electronics, are boosting the development and adoption of high-performance flame-retardant polycarbonate.

- Proliferation of 5G Technology: The rollout of 5G infrastructure is driving demand for specialized polycarbonate in antennas, base stations, and telecommunications enclosures due to its excellent dielectric properties.

AI Impact Analysis on Polycarbonate Resin

Common user questions related to the impact of AI on the Polycarbonate Resin market primarily focus on how artificial intelligence can optimize manufacturing processes, enhance material development, and improve supply chain efficiency. Users are keenly interested in AI's role in predictive analytics for demand forecasting, enabling manufacturers to better align production with market needs and reduce waste. Queries also extend to AI-driven quality control, where machine vision and deep learning algorithms can identify defects with greater precision and speed, leading to higher product consistency and reduced material loss. The potential for AI to accelerate R&D cycles for new polycarbonate formulations, including sustainable and high-performance grades, is another significant area of user inquiry, anticipating faster market introduction of innovative products.

AI's influence is anticipated to revolutionize several facets of the polycarbonate resin industry, from raw material procurement to end-product delivery. In manufacturing, AI can optimize processing parameters such as temperature, pressure, and molding cycles, leading to improved energy efficiency and reduced operational costs. Furthermore, AI algorithms can analyze vast datasets from material testing to predict performance characteristics of new polymer blends, significantly shortening the development timeline for specialized polycarbonate resins. Supply chain management benefits immensely from AI through real-time tracking, risk assessment, and dynamic route optimization, ensuring timely delivery and minimizing disruptions. As the industry moves towards more complex and customized solutions, AI will be instrumental in enabling mass customization and personalized product development, ultimately enhancing competitive advantage and fostering innovation across the value chain.

- Optimized Manufacturing Processes: AI-driven predictive maintenance and process control can reduce downtime, enhance energy efficiency, and improve yield rates in polycarbonate production.

- Accelerated Material R&D: AI and machine learning algorithms can analyze complex data to identify new polycarbonate formulations with desired properties, shortening product development cycles.

- Enhanced Quality Control: AI-powered vision systems can detect subtle defects in polycarbonate products with high precision, ensuring consistent product quality and reducing waste.

- Improved Supply Chain Management: AI algorithms can optimize logistics, inventory management, and demand forecasting, leading to more resilient and efficient supply chains for polycarbonate resins.

- Sustainability Initiatives: AI can support the development of advanced recycling processes for polycarbonate by optimizing sorting and chemical breakdown, contributing to a circular economy.

- Predictive Analytics for Market Trends: AI tools can analyze market data to predict future demand and trends for polycarbonate, informing strategic business decisions and investment.

Key Takeaways Polycarbonate Resin Market Size & Forecast

Common user questions regarding the key takeaways from the Polycarbonate Resin market size and forecast often center on the primary growth catalysts, the resilience of demand across diverse applications, and the strategic implications for industry players. Users are keen to understand which end-use sectors will drive the most significant growth and how evolving consumer preferences and technological advancements are shaping future market expansion. There is also considerable interest in identifying potential market saturation points or disruptive technologies that could alter the long-term forecast, and how manufacturers are adapting to these dynamics to sustain profitability and market share. The focus is on understanding both the quantitative growth projections and the qualitative factors influencing market evolution.

The polycarbonate resin market is poised for robust expansion, primarily fueled by its indispensable role in the rapidly growing electronics, automotive, and construction industries. The emphasis on lightweighting, enhanced durability, and improved optical clarity across these sectors continues to underpin strong demand for polycarbonate. Furthermore, the increasing adoption of sustainable and bio-based variants signifies a pivotal shift towards environmentally conscious manufacturing, presenting both a challenge and a significant opportunity for market participants. The forecast indicates that while traditional applications remain strong, emerging areas like electric vehicles, advanced medical devices, and smart infrastructure will be key growth engines. Strategic investments in research and development, alongside diversified regional expansion, will be crucial for companies to capitalize on these promising market dynamics and navigate competitive pressures effectively.

- Robust Growth Trajectory: The market is projected for significant growth, driven by increasing adoption in high-growth sectors such as automotive, electronics, and medical devices.

- Sustainability as a Core Driver: The shift towards bio-based and recycled polycarbonate is not merely a trend but a fundamental driver influencing product development and market acceptance.

- Diversified Application Portfolio: Resilience in the market is underpinned by its versatile applications, ensuring demand stability even with fluctuations in specific end-use industries.

- Technological Advancements are Key: Continuous innovation in material properties, processing techniques, and specialized grades is critical for maintaining competitive advantage and opening new markets.

- Regional Disparities in Growth: While global growth is strong, specific regions like Asia Pacific are expected to outpace others due to rapid industrialization and infrastructure development.

- Strategic Collaborations and M&A: Partnerships and acquisitions are increasingly vital for expanding product portfolios, enhancing research capabilities, and strengthening market presence.

- Emphasis on Performance and Customization: Demand for specialized, high-performance polycarbonate grades tailored to specific application requirements will continue to drive premium segment growth.

Polycarbonate Resin Market Drivers Analysis

The polycarbonate resin market is primarily driven by escalating demand from critical end-use industries, where its superior properties offer distinct advantages over alternative materials. The rapid expansion of the consumer electronics sector, characterized by continuous innovation in product design and functionality, necessitates lightweight, durable, and aesthetically appealing materials like polycarbonate for casings, displays, and internal components. Simultaneously, the global automotive industry's push towards lightweighting to enhance fuel efficiency and facilitate the transition to electric vehicles significantly boosts the consumption of polycarbonate for structural, interior, and exterior parts, replacing traditional metals and glass.

Beyond electronics and automotive, the construction sector's increasing preference for polycarbonate in glazing, roofing, and safety applications, owing to its high impact resistance and optical clarity, contributes substantially to market growth. Furthermore, the burgeoning healthcare industry's demand for sterile, biocompatible, and high-performance materials for medical devices, diagnostic equipment, and drug delivery systems reinforces polycarbonate's market position. The growing awareness and stringent regulations regarding fire safety also drive the adoption of flame-retardant polycarbonate grades across various applications, further propelling market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Automotive Industry (Lightweighting, EVs) | +1.5% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 (Long-term) |

| Growth of Consumer Electronics (Smartphones, Laptops, Wearables) | +1.2% | Asia Pacific (China, India, South Korea), North America | 2025-2030 (Mid-term) |

| Rising Adoption in Medical Devices and Healthcare | +0.8% | North America, Europe, Developed Asia (Japan, South Korea) | 2025-2033 (Long-term) |

| Expansion of Construction and Building Materials Sector | +0.7% | Asia Pacific (India, Southeast Asia), Middle East | 2025-2032 (Mid-to-long term) |

| Technological Advancements and Product Innovation | +0.5% | Global | 2025-2033 (Ongoing) |

Polycarbonate Resin Market Restraints Analysis

The polycarbonate resin market faces several significant restraints that could impede its growth trajectory. Price volatility of raw materials, particularly Bisphenol A (BPA) and phosgene, which are derived from crude oil, remains a primary concern for manufacturers. Fluctuations in these feedstock prices directly impact production costs and, consequently, the final product pricing, leading to reduced profit margins or increased market prices that may deter buyers. Additionally, environmental regulations concerning the use and disposal of BPA, although largely managed through alternative production methods and material grades, continue to pose a compliance burden and require ongoing investment in research and development to ensure sustainable practices.

Another notable restraint is the intense competition from alternative transparent engineering plastics such as polymethyl methacrylate (PMMA) and polystyrene (PS), which, in certain applications, offer cost advantages or specific property profiles. While polycarbonate often boasts superior performance, the availability of these substitutes can limit market penetration in price-sensitive segments. Furthermore, the high capital expenditure required for establishing and expanding polycarbonate manufacturing facilities, coupled with the complex polymerization processes involved, acts as a barrier to entry for new players, limiting market dynamism and potentially restricting supply growth in response to surging demand. The geopolitical landscape and trade disputes can also disrupt supply chains, impacting raw material availability and export opportunities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Bisphenol A) | -0.9% | Global | 2025-2030 (Short-to-mid term) |

| Stringent Environmental Regulations (BPA Concerns) | -0.6% | Europe, North America | 2025-2033 (Ongoing) |

| Competition from Substitute Materials (PMMA, PS) | -0.5% | Global | 2025-2033 (Long-term) |

| High Capital Investment and Production Complexity | -0.4% | Global | 2025-2033 (Long-term) |

| Supply Chain Disruptions and Geopolitical Risks | -0.3% | Global | 2025-2027 (Short-term) |

Polycarbonate Resin Market Opportunities Analysis

The polycarbonate resin market presents significant opportunities driven by the growing emphasis on sustainability and the development of advanced recycling technologies. The increasing demand for circular economy solutions is spurring innovations in chemical recycling processes for polycarbonate, which can convert post-consumer waste back into virgin-grade materials. This not only addresses environmental concerns related to plastic waste but also provides a more stable and sustainable source of raw materials, reducing reliance on fossil fuels. Furthermore, the rising consumer and regulatory preference for bio-based polymers opens new avenues for the development and commercialization of polycarbonate resins derived from renewable resources, tapping into a nascent yet rapidly expanding market segment.

Beyond sustainability, emerging applications in advanced technologies offer substantial growth prospects. The rapid proliferation of electric vehicles (EVs) creates new demand for high-performance, lightweight polycarbonate solutions in battery housings, interior components, and exterior lighting, where its excellent thermal stability and impact resistance are crucial. Similarly, the ongoing deployment of 5G infrastructure globally necessitates specialized polycarbonate grades for antennas, communication equipment, and optical fibers, leveraging its superior dielectric properties and transparency. Furthermore, advancements in medical device manufacturing, particularly in personalized medicine and wearable health technologies, will continue to expand the scope for innovative polycarbonate applications, demanding materials with enhanced biocompatibility and design flexibility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Recycling Technologies (Chemical Recycling) | +1.0% | Europe, North America, Japan | 2027-2033 (Mid-to-long term) |

| Growth in Bio-based and Sustainable Polycarbonate Grades | +0.8% | Global, particularly Europe and North America | 2026-2033 (Long-term) |

| Rising Demand from Electric Vehicle (EV) Components | +0.9% | Asia Pacific (China), Europe, North America | 2025-2033 (Long-term) |

| Expansion in 5G Telecommunications Infrastructure | +0.7% | Global, particularly Asia Pacific (China, India) | 2025-2030 (Mid-term) |

| Niche Applications in Advanced Medical and Optical Devices | +0.6% | Developed Markets (North America, Europe, Japan) | 2025-2033 (Long-term) |

Polycarbonate Resin Market Challenges Impact Analysis

The polycarbonate resin market faces several complex challenges that demand strategic responses from industry participants. One significant hurdle is the intense price competition, particularly from commodity plastics and other engineering plastics, which can pressure profit margins and limit market share in certain applications. This competitive landscape necessitates continuous innovation and differentiation to justify the premium cost often associated with polycarbonate's superior performance. Furthermore, maintaining consistent quality and meeting diverse regulatory standards across various regions for applications in medical, automotive, and food contact industries presents a formidable challenge, requiring substantial investment in quality control and compliance measures.

Another critical challenge involves the environmental and health concerns associated with Bisphenol A (BPA), a key monomer in traditional polycarbonate production. Although the industry has developed BPA-free polycarbonate alternatives and is investing in chemical recycling, public perception and evolving regulatory frameworks continue to pose a challenge to market acceptance and growth. Managing complex global supply chains for raw materials and finished products, especially amidst geopolitical tensions and logistical bottlenecks, remains a persistent challenge, impacting production schedules and delivery timelines. Finally, the high energy consumption and carbon footprint associated with polycarbonate manufacturing necessitate ongoing efforts towards energy efficiency and sustainable production practices, aligning with global climate change goals but adding to operational complexities and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition from Substitute Materials | -0.8% | Global | 2025-2033 (Long-term) |

| Stringent Regulatory and Environmental Scrutiny (BPA) | -0.7% | Europe, North America, China | 2025-2033 (Ongoing) |

| Supply Chain Volatility and Geopolitical Instability | -0.6% | Global | 2025-2028 (Short-to-mid term) |

| High Energy Consumption in Manufacturing | -0.4% | Global | 2025-2033 (Ongoing) |

| Limited Recyclability of Traditional Polycarbonate | -0.3% | Global | 2025-2030 (Mid-term) |

Polycarbonate Resin Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Polycarbonate Resin market, covering historical data, current market trends, and future growth projections from 2025 to 2033. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive primary and secondary research to deliver actionable insights, including a competitive landscape analysis profiling leading industry players, and a deep dive into the impact of emerging technologies and sustainability initiatives on market dynamics. This updated scope ensures a thorough understanding of the current market scenario and future potential for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 44.5 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SABIC, Covestro AG, Teijin Limited, LG Chem, Trinseo, Chi Mei Corporation, Sumitomo Chemical Co., Ltd., Mitsubishi Engineering-Plastics Corporation, Samyang Kasei, Formosa Idemitsu Petrochemical Co., Ltd., Lone Star Chemical, RTP Company, Lexan, Lotte Chemical, Kumho Petrochemical, ENP Industries, Kingfa Science & Technology Co., Ltd., PolyCarbon Industries, Asahi Kasei Corporation, Toray Industries, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The polycarbonate resin market is meticulously segmented to provide a detailed understanding of its diverse applications and product types, allowing for precise market sizing and forecasting. This segmentation is crucial for identifying distinct revenue streams and strategic opportunities across various industries. By breaking down the market based on grade, application, and manufacturing process, stakeholders can gain granular insights into consumer preferences, technological advancements, and regulatory impacts specific to each segment. This comprehensive approach ensures that the report captures the full complexity and dynamism of the polycarbonate market, enabling targeted business strategies and investment decisions.

Understanding these segmentations highlights the versatility of polycarbonate resin and its indispensable role in modern industrial and consumer products. The distinction between grades, such as optical, medical, and flame retardant, underscores the material's adaptability to specialized performance requirements. Similarly, the detailed application segments, ranging from high-growth sectors like automotive and electronics to specialized areas like medical devices and optical media, illustrate the broad demand landscape. Analyzing the market by manufacturing process provides insights into production efficiencies and technological trends that influence supply dynamics and cost structures. This multi-faceted segmentation offers a holistic view of the market, essential for strategic planning and competitive analysis.

- Grade:

- Optical Grade

- Medical Grade

- General Purpose Grade

- Flame Retardant Grade

- Food Grade

- Others

- Application:

- Automotive

- Interior

- Exterior

- Lighting

- Electrical & Electronics

- Consumer Electronics

- IT

- Appliances

- Building & Construction

- Glazing

- Roofing

- Interior Design

- Medical

- Devices

- Diagnostics

- Drug Delivery

- Packaging

- Bottles

- Films

- Food Containers

- Optical Media

- CDs

- DVDs

- Blu-ray Discs

- Other Applications

- Sports Equipment

- Safety Equipment

- Industrial

- Automotive

- Manufacturing Process:

- Interfacial Polymerization

- Melt Transesterification

Regional Highlights

- North America: Characterized by mature automotive and electronics industries, driving demand for high-performance and specialty polycarbonate grades. The region also sees significant adoption in medical devices and stringent regulatory environments pushing for sustainable solutions. The presence of major R&D hubs fosters innovation and advanced material development.

- Europe: A leader in sustainable and circular economy initiatives, influencing the demand for recycled and bio-based polycarbonate. The automotive, construction, and healthcare sectors are key consumers, with a strong focus on lightweighting and energy efficiency standards. Regulatory landscape regarding BPA use significantly impacts product development.

- Asia Pacific (APAC): The largest and fastest-growing market, propelled by rapid industrialization, urbanization, and a booming consumer electronics manufacturing base, particularly in China, India, and South Korea. Significant investments in infrastructure, automotive manufacturing, and telecommunications further fuel the demand for polycarbonate.

- Latin America: Exhibits steady growth, driven by expanding construction activities and increasing demand from the automotive and packaging industries. Economic development and urbanization are contributing to the rising consumption of polycarbonate, though at a slower pace compared to APAC.

- Middle East and Africa (MEA): Emerging as a promising market, primarily due to ambitious infrastructure development projects, growth in the construction sector, and diversification efforts beyond oil. Demand for polycarbonate in glazing, roofing, and safety applications is gaining traction.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polycarbonate Resin Market.- SABIC

- Covestro AG

- Teijin Limited

- LG Chem

- Trinseo

- Chi Mei Corporation

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Engineering-Plastics Corporation

- Samyang Kasei

- Formosa Idemitsu Petrochemical Co., Ltd.

- Lone Star Chemical

- RTP Company

- Lexan

- Lotte Chemical

- Kumho Petrochemical

- ENP Industries

- Kingfa Science & Technology Co., Ltd.

- PolyCarbon Industries

- Asahi Kasei Corporation

- Toray Industries, Inc.

Frequently Asked Questions

Analyze common user questions about the Polycarbonate Resin market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary drivers of growth for the Polycarbonate Resin Market?

The market's growth is predominantly driven by increasing demand from the automotive sector for lightweighting and EV components, the expanding consumer electronics industry requiring durable and aesthetically pleasing materials, and the growing application in medical devices due to its biocompatibility and sterilizability.

How do sustainability concerns impact the Polycarbonate Resin Market?

Sustainability concerns are a significant influence, driving demand for bio-based and recycled polycarbonate grades. Manufacturers are investing in chemical recycling technologies and developing eco-friendly formulations to meet stringent environmental regulations and consumer preferences for sustainable products.

Which regions are expected to show the most significant growth in the Polycarbonate Resin Market?

The Asia Pacific region, particularly countries like China, India, and South Korea, is projected to exhibit the most significant growth due to rapid industrialization, burgeoning consumer electronics manufacturing, and extensive infrastructure development projects.

What are the main challenges facing the Polycarbonate Resin Market?

Key challenges include volatile raw material prices, intense competition from substitute materials, stringent environmental regulations regarding Bisphenol A (BPA), and the complexities of managing global supply chains. High energy consumption in manufacturing also presents an ongoing challenge for sustainability initiatives.

What are the emerging applications for Polycarbonate Resin?

Emerging applications include advanced components for electric vehicles (EVs), specialized materials for 5G telecommunications infrastructure, high-performance plastics for advanced medical and wearable devices, and innovative solutions for architectural glazing and smart building materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted