Platelet Aggregation Device Market

Platelet Aggregation Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709072 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Platelet Aggregation Device Market Size

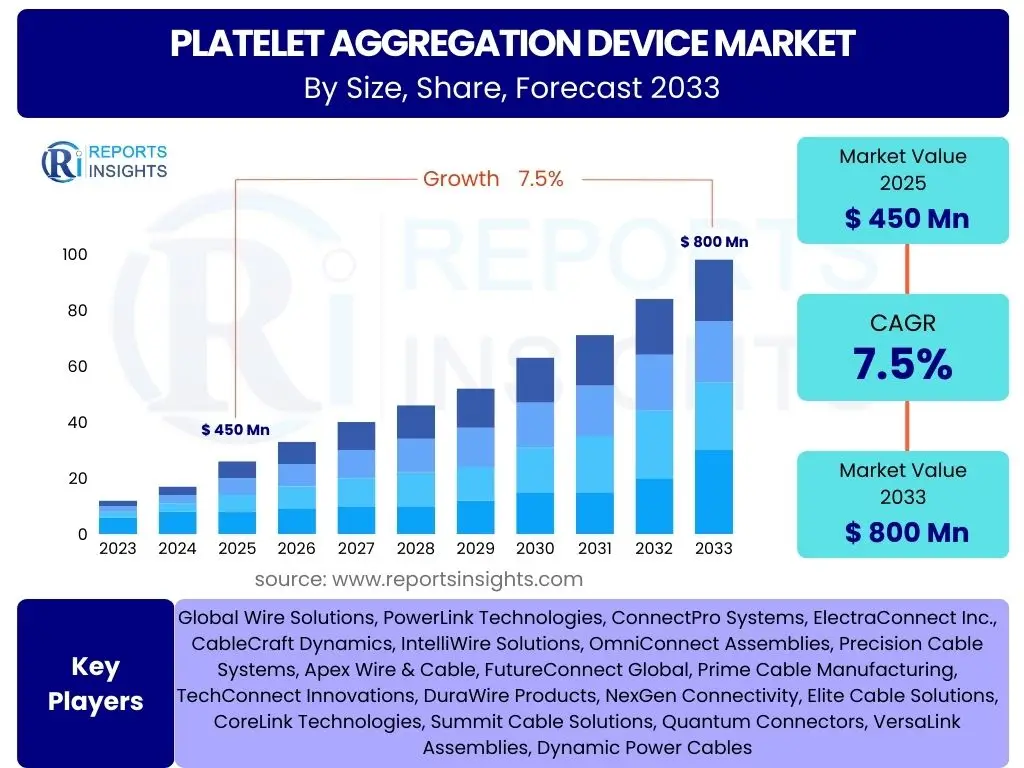

According to Reports Insights Consulting Pvt Ltd, The Platelet Aggregation Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 800 Million by the end of the forecast period in 2033.

Key Platelet Aggregation Device Market Trends & Insights

The Platelet Aggregation Device market is experiencing significant evolution driven by technological advancements and an increasing global burden of cardiovascular and hematological disorders. A prominent trend involves the shift towards automated and semi-automated devices, which offer enhanced accuracy, reduced turnaround times, and simplified operation compared to traditional manual methods. This automation is crucial for clinical laboratories and hospitals seeking to improve efficiency and manage growing patient volumes, particularly in diagnosing and monitoring antiplatelet therapy.

Furthermore, there is a growing demand for point-of-care (POC) platelet aggregation testing, especially in emergency settings and for rapid patient stratification. POC devices provide quick results, enabling immediate clinical decisions and personalized treatment adjustments for patients at risk of thrombotic events or bleeding complications. This trend is fueled by the desire for decentralized testing and the convenience it offers, moving diagnostics closer to the patient and enhancing accessibility in diverse healthcare environments.

Another key insight highlights the increasing adoption of impedance aggregometry and whole blood aggregometry due to their ability to provide a more physiological assessment of platelet function compared to light transmission aggregometry (LTA), which typically requires platelet-rich plasma. These advanced methods offer a comprehensive view of platelet activity, which is vital for patients on complex antiplatelet regimens or those with challenging hemostatic disorders. The integration of advanced data analysis capabilities and connectivity features into newer devices further enhances their utility, facilitating better data management and interpretation in clinical practice.

- Growing adoption of automated and semi-automated platelet aggregation systems.

- Rising demand for point-of-care (POC) testing solutions for rapid diagnostics.

- Increasing preference for whole blood and impedance aggregometry for physiological assessment.

- Technological advancements in device miniaturization and improved data interpretation.

- Expansion of applications in drug discovery and personalized medicine for antiplatelet therapies.

AI Impact Analysis on Platelet Aggregation Device

The integration of Artificial Intelligence (AI) into the Platelet Aggregation Device market is poised to revolutionize diagnostics, offering enhanced precision and predictive capabilities. Users are keen to understand how AI can transform raw data from these devices into actionable clinical insights, moving beyond simple aggregation measurements to identify subtle patterns indicative of specific pathologies or treatment responses. AI algorithms can process vast amounts of platelet function data, identifying biomarkers and trends that might be imperceptible to human analysis, thereby improving diagnostic accuracy for complex coagulation disorders and optimizing antiplatelet therapy management.

Concerns and expectations often revolve around AI's role in predictive analytics. Users anticipate AI to forecast patient responses to antiplatelet drugs, identify individuals at higher risk of thrombotic or bleeding events, and personalize treatment regimens based on individual platelet reactivity profiles. This capability would significantly reduce adverse drug reactions and improve patient outcomes. There is also a strong expectation for AI to streamline laboratory workflows by automating data analysis, quality control, and result reporting, thereby increasing efficiency and reducing the burden on healthcare professionals.

Furthermore, the potential for AI to support research and drug development is a significant area of interest. By analyzing large datasets from clinical trials and patient populations, AI can accelerate the discovery of novel antiplatelet agents, identify new therapeutic targets, and refine existing treatment protocols. However, users also express concerns about data privacy, algorithm transparency, and the need for robust validation studies to ensure the reliability and clinical utility of AI-powered platelet aggregation diagnostics. The ethical implications and regulatory frameworks for AI in medical devices are also key considerations.

- Enhanced diagnostic accuracy and pattern recognition in platelet function data.

- Predictive analytics for personalized antiplatelet therapy and risk stratification.

- Automation of data interpretation, quality control, and reporting in laboratories.

- Accelerated drug discovery and development for novel antiplatelet agents.

- Potential for improved patient outcomes through optimized treatment regimens.

- Challenges related to data privacy, algorithm transparency, and regulatory oversight.

Key Takeaways Platelet Aggregation Device Market Size & Forecast

The Platelet Aggregation Device market is on a robust growth trajectory, driven primarily by the escalating global incidence of cardiovascular diseases, an aging population, and the increasing number of surgical procedures requiring precise hemostasis management. The market's expansion is further bolstered by continuous advancements in device technology, offering more accurate, efficient, and user-friendly solutions for assessing platelet function. The forecast indicates a steady upward trend, underscoring the indispensable role these devices play in both clinical diagnostics and research settings.

A crucial insight from the market forecast is the growing emphasis on early and accurate diagnosis of platelet-related disorders, which is vital for effective patient management and prevention of severe health complications. Healthcare providers are increasingly recognizing the value of these devices in guiding personalized antiplatelet therapy, thereby minimizing risks associated with both under- and over-treatment. This drives the demand for innovative and reliable platelet aggregation testing solutions across various healthcare facilities.

Moreover, the market is set to benefit from the rising adoption of point-of-care testing and the expansion of healthcare infrastructure in emerging economies. These factors are creating new avenues for market penetration and wider accessibility of advanced diagnostic tools. Stakeholders should focus on strategic investments in research and development to introduce next-generation devices that address unmet clinical needs and enhance interoperability within integrated healthcare systems, capitalizing on the sustained demand for sophisticated hemostatic assessment tools.

- Significant market growth anticipated due to rising chronic disease prevalence.

- Technological advancements are key drivers for enhanced diagnostic capabilities.

- Increasing adoption of point-of-care testing solutions in diverse settings.

- Personalized medicine and antiplatelet therapy guidance fueling demand.

- Emerging markets offer substantial growth opportunities for market players.

Platelet Aggregation Device Market Drivers Analysis

The Platelet Aggregation Device market is significantly propelled by several critical factors. The escalating global burden of cardiovascular diseases (CVDs), including myocardial infarction and stroke, necessitating routine assessment of platelet function, stands as a primary driver. As CVDs continue to be a leading cause of mortality worldwide, the demand for accurate and timely diagnosis and monitoring of platelet activity for antiplatelet therapy management intensifies, directly contributing to market growth. Additionally, the growing number of surgical procedures, particularly those involving high risks of bleeding or thrombosis, increases the imperative for pre-operative and post-operative platelet function assessment to ensure patient safety and optimize outcomes.

Technological advancements also play a pivotal role in driving market expansion. Innovations in device design, such as the development of automated, miniaturized, and multi-parameter systems, enhance the efficiency, accuracy, and ease of use of platelet aggregation tests. These improvements make the devices more attractive to clinical laboratories and point-of-care settings. Furthermore, the rising adoption of personalized medicine approaches, where antiplatelet therapy is tailored to individual patient responses, heavily relies on precise platelet function testing, thereby boosting the demand for sophisticated aggregation devices capable of providing detailed and reliable data.

The increasing elderly population, which is more susceptible to thrombotic and bleeding disorders, also contributes substantially to market growth. As the global demographic shifts towards an older age structure, the prevalence of conditions requiring platelet function monitoring naturally increases. Moreover, the growing focus on research and development in hematology and hemostasis, leading to new insights into platelet physiology and pathology, further stimulates the need for advanced aggregation devices for both experimental and clinical applications. These collective forces underscore the robust demand for innovative and effective platelet aggregation solutions across the healthcare continuum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Incidence of Cardiovascular Diseases | +1.2% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Number of Surgical Procedures | +0.9% | Global, with emphasis on developed economies | Mid to Long-term (2025-2033) |

| Technological Advancements in Device Capabilities | +1.0% | Global, with R&D hubs in North America, Europe | Short to Long-term (2025-2033) |

| Growing Demand for Personalized Medicine | +0.8% | Developed countries, expanding to emerging markets | Mid to Long-term (2026-2033) |

| Aging Global Population | +0.7% | Global, most pronounced in developed nations | Long-term (2025-2033) |

Platelet Aggregation Device Market Restraints Analysis

Despite significant growth potential, the Platelet Aggregation Device market faces several restraining factors that could impede its expansion. One major restraint is the high cost associated with advanced platelet aggregation devices, especially automated and sophisticated systems. This substantial upfront investment, coupled with ongoing maintenance expenses and the cost of specialized reagents and consumables, can be prohibitive for smaller healthcare facilities, diagnostic laboratories with limited budgets, and even larger institutions in resource-constrained regions. The economic burden often limits the widespread adoption of these crucial diagnostic tools, particularly in emerging markets where healthcare spending is lower.

Another significant challenge stems from the stringent regulatory approval processes required for medical devices. Platelet aggregation devices, being critical diagnostic tools, must undergo rigorous testing and validation to ensure their safety, efficacy, and accuracy. Obtaining regulatory clearances from bodies such as the FDA in the U.S. or CE Mark in Europe can be a lengthy, complex, and costly endeavor. This protracted approval timeline not only delays market entry for new products but also increases the overall development costs for manufacturers, which can then be passed on to end-users, further impacting affordability and accessibility.

Furthermore, the lack of standardization in testing methodologies and result interpretation across different device types and manufacturers presents a considerable restraint. Variations in protocols, reagents, and analytical platforms can lead to discrepancies in platelet function results, making it challenging for clinicians to compare data and make consistent treatment decisions. This lack of harmonization can reduce physician confidence in the reliability of certain tests and create barriers to widespread adoption. Additionally, the availability of alternative, less expensive diagnostic methods, even if less comprehensive, can divert market share, particularly in settings where budget constraints are paramount.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Devices and Consumables | -0.7% | Global, particularly emerging markets | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.5% | Developed countries (North America, Europe) | Mid to Long-term (2025-2030) |

| Lack of Standardization in Testing Methodologies | -0.4% | Global | Long-term (2025-2033) |

| Availability of Alternative, Less Comprehensive Diagnostic Methods | -0.3% | Global, especially cost-sensitive regions | Mid-term (2025-2029) |

| Need for Skilled Professionals for Operation and Interpretation | -0.3% | Global, more pronounced in developing regions | Long-term (2025-2033) |

Platelet Aggregation Device Market Opportunities Analysis

The Platelet Aggregation Device market is ripe with opportunities driven by several evolving trends and unmet needs within healthcare. A significant opportunity lies in the continuous advancement of technology, particularly the development of more compact, user-friendly, and highly automated devices. Miniaturization and integration of AI-powered analytics can transform current devices into smart, portable systems capable of delivering rapid, accurate results in diverse settings, including remote clinics and even home-based care. This innovation can broaden market reach beyond traditional laboratory environments and enhance accessibility for a wider patient population.

The expansion into emerging markets represents another substantial growth opportunity. Countries in Asia Pacific, Latin America, and the Middle East and Africa are witnessing rapid improvements in healthcare infrastructure, increasing disposable incomes, and a rising awareness regarding advanced diagnostic methods. As these regions experience a growing burden of chronic diseases, the demand for sophisticated diagnostic tools, including platelet aggregation devices, is expected to surge. Manufacturers who strategically invest in these regions, offering cost-effective and culturally adapted solutions, stand to gain significant market share.

Furthermore, the increasing focus on personalized medicine and pharmacogenomics creates a unique opportunity for tailored antiplatelet therapy. Platelet aggregation devices can play a pivotal role in identifying individual patient responses to various antiplatelet drugs, allowing clinicians to optimize dosages and select the most effective treatment regimens, thereby improving patient outcomes and reducing adverse events. This personalized approach not only enhances the clinical utility of these devices but also opens avenues for partnerships with pharmaceutical companies engaged in drug development and patient stratification, driving innovation and market adoption in specialized clinical areas.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Portable and Point-of-Care Devices | +1.3% | Global, particularly remote and emergency settings | Mid to Long-term (2026-2033) |

| Expansion into Emerging Economies | +1.1% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Integration with Personalized Medicine & Pharmacogenomics | +1.0% | Developed countries, specialized clinical centers | Mid to Long-term (2027-2033) |

| Strategic Partnerships & Collaborations with Pharma Companies | +0.9% | Global, especially R&D intensive regions | Short to Mid-term (2025-2030) |

| Research & Development for New Clinical Applications | +0.8% | Global, academic and research institutions | Long-term (2025-2033) |

Platelet Aggregation Device Market Challenges Impact Analysis

The Platelet Aggregation Device market faces significant challenges that could hinder its full growth potential. One primary challenge is the reimbursement landscape, particularly in diverse healthcare systems. Obtaining adequate and consistent reimbursement for platelet aggregation tests can be complex and varies significantly by region and payer. Insufficient or inconsistent reimbursement policies can limit the willingness of healthcare providers to adopt new, advanced devices, impacting sales and market penetration. This financial barrier often forces facilities to prioritize less expensive, albeit potentially less accurate, alternatives, especially in budget-constrained environments.

Another substantial challenge is the intense competition among existing market players, coupled with the entry of new innovators. The market features a mix of well-established companies and nimble startups, all vying for market share through product differentiation, pricing strategies, and geographical expansion. This competitive pressure can lead to price erosion, reduced profit margins, and increased marketing expenditures. Furthermore, the need for continuous innovation to stay ahead of competitors necessitates substantial investment in research and development, which smaller companies might find difficult to sustain, potentially leading to market consolidation.

The complexity of interpreting results from various platelet aggregation devices also presents a significant hurdle. Platelet function testing can be influenced by numerous pre-analytical variables, patient specific factors, and medications, leading to variability in results. This complexity requires highly skilled and experienced personnel for both device operation and result interpretation, which can be a limiting factor in regions with a shortage of trained healthcare professionals. Educating clinicians and laboratory staff on the nuances of different technologies and the clinical significance of their outputs remains an ongoing challenge, impacting the consistent and appropriate utilization of these diagnostic tools in routine clinical practice.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Unfavorable Reimbursement Policies | -0.8% | Global, particularly North America, Europe | Long-term (2025-2033) |

| Intense Market Competition and Price Pressures | -0.6% | Global | Long-term (2025-2033) |

| Complexity of Test Interpretation and Standardization | -0.5% | Global | Long-term (2025-2033) |

| Shortage of Skilled Healthcare Professionals | -0.4% | Developing and some developed regions | Long-term (2025-2033) |

| Data Privacy and Cybersecurity Concerns (for connected devices) | -0.3% | Global | Mid to Long-term (2026-2033) |

Platelet Aggregation Device Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Platelet Aggregation Device market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and geographical regions. The study covers historical data from 2019 to 2023, establishes 2024 as the base year, and projects market trends and values through 2033. It examines technological advancements, regulatory landscapes, and competitive dynamics shaping the industry, providing a strategic framework for stakeholders to navigate the evolving market landscape. The report also highlights the impact of AI on diagnostic capabilities and patient care, alongside detailed segmentation to offer granular insights into market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 800 Million |

| Growth Rate | 7.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Diagnostics Inc., MediTech Solutions Corp., Precision BioSystems Ltd., ClotDetect Instruments, Hemostasis Innovations Co., BioQuant Analytics, ThromboScreen Devices, Apex MedTech Group, Advanced Platelet Systems, Dynamic Diagnostics Ltd., Coagulation Technologies, LabPro Instruments, Integrated Medical Devices, HealthFlow Solutions, OmniPath Diagnostics, Synapse Biomedical, Innova Life Sciences, Quantia Labs, Premier Medical Systems, Vitality Diagnostics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Platelet Aggregation Device market is comprehensively segmented to provide a detailed understanding of its diverse components and drivers. This segmentation allows for a granular analysis of market dynamics, identifying key areas of growth, adoption, and competitive intensity. The primary categories for segmentation include product type, application, and end-user. Each segment reflects distinct needs and technological preferences within the healthcare ecosystem, from specialized laboratory equipment to point-of-care solutions, influencing market trends and strategic development.

By dissecting the market along these lines, stakeholders can gain insights into the specific technological preferences of different user groups, the prevalent applications driving demand, and the dominant end-user segments contributing to market growth. This granular approach helps in understanding the varying requirements across clinical diagnosis, research, and drug discovery, enabling manufacturers to tailor their product offerings and marketing strategies more effectively. Such segmentation also aids in forecasting future market shifts and identifying niche opportunities within the broader Platelet Aggregation Device landscape.

- By Product Type:

- Light Transmission Aggregometer (LTA)

- Impedance Aggregometer

- Whole Blood Aggregometer

- Optical Aggregometer

- Electrical Aggregometer

- Consumables (Reagents, Cuvettes, Pipettes)

- By Application:

- Clinical Diagnosis

- Cardiovascular Diseases

- Hematological Disorders

- Bleeding Disorders

- Diabetes Mellitus

- Research Applications

- Drug Discovery & Development

- Clinical Diagnosis

- By End-User:

- Hospitals & Clinics

- Diagnostic Laboratories

- Research & Academic Institutes

- Pharmaceutical & Biotechnology Companies

Regional Highlights

North America currently dominates the Platelet Aggregation Device market, primarily due to advanced healthcare infrastructure, high awareness and adoption of sophisticated diagnostic technologies, and a significant prevalence of cardiovascular diseases. The region benefits from substantial investments in R&D, robust reimbursement policies, and the presence of key market players. The U.S. in particular is a major contributor, driven by a strong focus on personalized medicine and advanced diagnostic capabilities.

Europe also holds a substantial share, propelled by an aging population, rising chronic disease burden, and favorable government initiatives for healthcare expenditure. Countries like Germany, the UK, and France are leading the market with their well-established healthcare systems and increasing adoption of automated diagnostic solutions. The demand for efficient and accurate platelet function testing remains high across the continent.

Asia Pacific is projected to be the fastest-growing region during the forecast period. This growth is attributed to improving healthcare infrastructure, rising disposable incomes, increasing awareness about advanced diagnostics, and the growing prevalence of lifestyle diseases. Countries like China, India, and Japan are investing heavily in healthcare, offering vast untapped potential for market expansion. Latin America, along with the Middle East and Africa, are emerging markets showing gradual growth, driven by increasing healthcare access and improving economic conditions.

- North America: Dominant market share due to advanced healthcare, high disease prevalence, and robust R&D.

- Europe: Strong market position driven by aging population, chronic diseases, and supportive healthcare policies.

- Asia Pacific (APAC): Fastest-growing region, fueled by improving infrastructure, increasing awareness, and high patient volumes.

- Latin America: Emerging market with growing healthcare investment and demand for advanced diagnostics.

- Middle East & Africa (MEA): Gradual growth as healthcare access and infrastructure improve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Platelet Aggregation Device Market.- Global Diagnostics Inc.

- MediTech Solutions Corp.

- Precision BioSystems Ltd.

- ClotDetect Instruments

- Hemostasis Innovations Co.

- BioQuant Analytics

- ThromboScreen Devices

- Apex MedTech Group

- Advanced Platelet Systems

- Dynamic Diagnostics Ltd.

- Coagulation Technologies

- LabPro Instruments

- Integrated Medical Devices

- HealthFlow Solutions

- OmniPath Diagnostics

- Synapse Biomedical

- Innova Life Sciences

- Quantia Labs

- Premier Medical Systems

- Vitality Diagnostics

Frequently Asked Questions

Analyze common user questions about the Platelet Aggregation Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Platelet Aggregation Device?

A Platelet Aggregation Device is a medical instrument used to measure the ability of platelets to clump together (aggregate) in response to various stimuli. This measurement is crucial for diagnosing bleeding disorders, assessing the risk of thrombosis, and monitoring the effectiveness of antiplatelet therapies in patients with cardiovascular diseases or those undergoing surgery.

What are the primary applications of Platelet Aggregation Devices?

The primary applications include clinical diagnosis of cardiovascular diseases, hematological disorders, and bleeding conditions, as well as monitoring antiplatelet therapy. They are also extensively used in research for studying platelet function and in drug discovery and development to evaluate the efficacy of new antiplatelet agents.

What are the key types of Platelet Aggregation Devices available?

Key types include Light Transmission Aggregometers (LTA), Impedance Aggregometers, and Whole Blood Aggregometers. Each type offers different methodologies and advantages, with LTA being traditional, while impedance and whole blood aggregometers provide more physiological assessments of platelet function.

What factors are driving the growth of the Platelet Aggregation Device market?

The market growth is primarily driven by the increasing global incidence of cardiovascular diseases, an aging population, a rising number of surgical procedures, and ongoing technological advancements leading to more accurate and efficient devices. The growing demand for personalized medicine also plays a significant role.

What are the main challenges faced by the Platelet Aggregation Device market?

Key challenges include the high cost of advanced devices and consumables, stringent regulatory approval processes, a lack of standardization in testing methodologies, and the need for highly skilled professionals for operation and interpretation. Unfavorable reimbursement policies in some regions also present a significant hurdle to market penetration.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted