Antibody Drug Conjugate Market

Antibody Drug Conjugate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703942 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Antibody Drug Conjugate Market Size

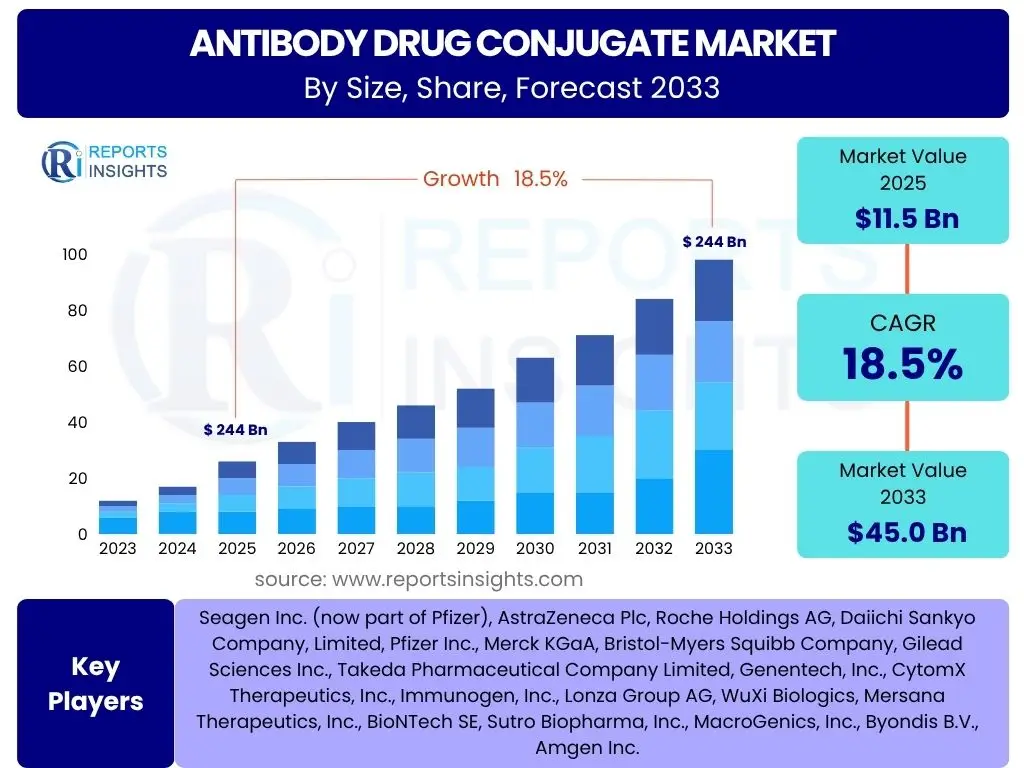

According to Reports Insights Consulting Pvt Ltd, The Antibody Drug Conjugate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 11.5 Billion in 2025 and is projected to reach USD 45.0 Billion by the end of the forecast period in 2033.

Key Antibody Drug Conjugate Market Trends & Insights

The Antibody Drug Conjugate (ADC) market is undergoing significant evolution, driven by advancements in linker technologies and payload diversity. User inquiries frequently center on the emergence of novel ADC constructs that promise enhanced therapeutic windows and reduced off-target toxicities. There is a strong focus on next-generation ADCs employing site-specific conjugation methods, which allow for more homogeneous drug-to-antibody ratios and improved stability in circulation, directly addressing challenges seen with earlier generations.

Furthermore, a notable trend involves the expansion of ADCs beyond oncology into new therapeutic areas, although cancer treatment remains the dominant application. Researchers and industry stakeholders are actively exploring ADCs for autoimmune diseases and infectious diseases, recognizing their precision targeting capabilities. This diversification is coupled with an increasing interest in combination therapies, where ADCs are paired with immunotherapies or conventional chemotherapy agents to achieve synergistic effects and overcome resistance mechanisms, prompting questions about optimal combination strategies and clinical trial outcomes.

The global regulatory landscape and manufacturing capabilities are also key areas of interest. With more ADCs progressing through clinical pipelines, the demand for robust and scalable manufacturing processes for antibodies, linkers, and payloads is escalating. Users often inquire about the supply chain complexities and quality control measures required for these highly potent and intricate biomolecules, highlighting the industry's need for specialized contract development and manufacturing organizations (CDMOs) that can meet stringent regulatory requirements and production demands for diverse ADC components.

- Emergence of next-generation ADCs with enhanced stability and targeted delivery.

- Expansion of ADC applications beyond oncology into autoimmune and infectious diseases.

- Increased adoption of combination therapies integrating ADCs with other treatments.

- Growing emphasis on site-specific conjugation and novel linker-payload technologies.

- Rising demand for specialized manufacturing and supply chain expertise for complex ADC components.

AI Impact Analysis on Antibody Drug Conjugate

Artificial intelligence (AI) is poised to revolutionize various stages of Antibody Drug Conjugate (ADC) development, from target identification to clinical trial optimization. User queries often explore how AI algorithms can accelerate the discovery of novel therapeutic targets suitable for ADC development, particularly in challenging oncology indications. AI's ability to analyze vast genomic, proteomic, and clinical datasets allows for the identification of specific tumor antigens with high selectivity, thereby enhancing the precision and efficacy of future ADCs and minimizing off-target effects.

Moreover, AI plays a crucial role in the rational design and optimization of ADC components, including antibodies, linkers, and payloads. Machine learning models can predict the binding affinity, stability, and pharmacokinetic properties of antibody candidates, as well as the stability and release characteristics of different linker-payload combinations. This computational approach significantly reduces the need for extensive experimental screening, leading to faster lead optimization and more efficient selection of the most promising ADC constructs, thereby saving considerable time and resources in preclinical development.

In the clinical development phase, AI is impacting patient stratification, biomarker discovery, and clinical trial design. Users frequently inquire about how AI can identify patient subgroups most likely to respond to specific ADCs, leading to more personalized treatment approaches and higher success rates in trials. Furthermore, predictive analytics powered by AI can optimize trial protocols, monitor adverse events, and analyze complex clinical data to accelerate drug approval processes and ensure safer, more effective deployment of ADCs in patient populations, addressing critical concerns about development costs and timelines.

- Accelerated identification of novel and highly selective ADC targets.

- Optimization of antibody engineering and linker-payload design for enhanced efficacy and safety.

- Streamlined preclinical development through predictive modeling of ADC properties.

- Improved patient stratification and biomarker discovery for personalized ADC therapies.

- Enhanced clinical trial design and monitoring for faster and more efficient development.

Key Takeaways Antibody Drug Conjugate Market Size & Forecast

The Antibody Drug Conjugate market is positioned for robust growth, reflecting its increasing importance in targeted cancer therapy and expanding therapeutic applications. Key insights suggest that the market's substantial projected CAGR is underpinned by a maturing understanding of ADC mechanisms, leading to the development of more sophisticated constructs with improved therapeutic windows. This growth trajectory is also indicative of the pharmaceutical industry's strategic investments in novel ADC platforms, recognizing their potential to deliver potent cytotoxic agents directly to cancer cells while minimizing systemic toxicity, a long-standing challenge in oncology.

A significant takeaway from the market forecast is the continued dominance of oncology applications, with a strong emphasis on addressing unmet needs in various cancer types where traditional therapies have limitations. However, the forecast also highlights a nascent yet promising expansion into non-oncology indications, signaling a broader recognition of ADCs' versatility. This diversification is expected to contribute to sustained growth beyond the initial forecast period, contingent on successful clinical validation and regulatory approvals in these new therapeutic areas.

Furthermore, the market's trajectory is heavily influenced by the interplay of technological advancements, particularly in linker and payload chemistry, and the strategic partnerships between pharmaceutical companies and biotechnology firms. The ability to overcome manufacturing complexities and address regulatory hurdles for these complex biologics will be paramount. The forecast underscores that success in this dynamic market will be defined by innovation, precision targeting, and the capacity to scale production efficiently to meet global demand, all while ensuring patient safety and treatment efficacy.

- Significant market expansion driven by advanced ADC constructs and targeted therapies.

- Oncology applications remain the primary growth engine, addressing critical unmet needs.

- Emerging potential in non-oncology therapeutic areas offers future diversification and growth.

- Technological innovation in linker-payload design is crucial for therapeutic improvement.

- Strategic collaborations and manufacturing capabilities are vital for market scalability and success.

Antibody Drug Conjugate Market Drivers Analysis

The Antibody Drug Conjugate (ADC) market is significantly propelled by the increasing global prevalence of cancer, which continues to drive demand for more effective and targeted therapeutic options. As cancer incidence rises across various demographics, particularly in aging populations and regions undergoing lifestyle transitions, there is a sustained and urgent need for innovative treatments that offer improved efficacy with reduced systemic side effects compared to conventional chemotherapy. ADCs, with their ability to precisely deliver potent cytotoxic payloads directly to tumor cells, are ideally positioned to meet this growing medical need, fostering robust market expansion and investment in research and development.

Technological advancements in ADC design represent another pivotal driver. Continuous innovation in monoclonal antibody engineering, linker chemistry, and payload potency has led to the development of next-generation ADCs with enhanced stability, optimized drug-to-antibody ratios, and improved therapeutic indices. These advancements address the limitations of earlier ADC generations, such as off-target toxicity and premature drug release, thereby increasing their clinical applicability and safety profile. The ongoing research into novel conjugation methods, cleavable and non-cleavable linkers, and diverse payload mechanisms further expands the therapeutic potential and market adoption of ADCs.

Furthermore, the growing number of regulatory approvals and a robust clinical pipeline for ADCs are significantly contributing to market growth. Successful clinical trials demonstrating superior efficacy and safety profiles for new ADC candidates instill confidence among healthcare providers and patients, accelerating their adoption. Governments and regulatory bodies worldwide are increasingly streamlining approval processes for innovative cancer therapies, recognizing the urgent need for advanced treatment modalities. This supportive regulatory environment, coupled with a healthy pipeline of compounds progressing through various phases of clinical development, ensures a steady influx of new products into the market, sustaining its upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Cancer Prevalence Globally | +4.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in ADC Design | +3.5% | Global | 2025-2033 |

| Growing Number of Regulatory Approvals & Robust Pipeline | +3.0% | North America, Europe, Japan | 2025-2030 |

| Rising Demand for Targeted Therapies | +2.5% | Global | 2025-2033 |

Antibody Drug Conjugate Market Restraints Analysis

Despite the promising outlook, the Antibody Drug Conjugate (ADC) market faces significant restraints, primarily stemming from the high cost associated with their development and manufacturing. ADCs are complex biological entities, requiring intricate processes for antibody production, linker synthesis, payload conjugation, and purification, all contributing to substantial research and development expenditures. These high costs translate into premium pricing for the final drug products, which can limit accessibility and adoption in healthcare systems with budget constraints or in developing regions, thereby slowing market penetration and overall growth.

Another crucial restraint is the inherent complexity of ADC manufacturing and supply chain management. The production of ADCs demands highly specialized facilities, stringent quality control measures, and expertise in handling potent cytotoxic compounds, making the manufacturing process technically challenging and prone to bottlenecks. Ensuring consistent quality, scalability, and regulatory compliance across diverse components (monoclonal antibody, linker, and payload) adds layers of complexity. Any disruption in the supply chain for specific components or issues with manufacturing yields can significantly impact product availability and market supply, posing a considerable challenge for manufacturers.

Furthermore, concerns regarding the potential for off-target toxicity and the development of drug resistance in patients represent significant clinical restraints. While ADCs are designed for targeted delivery, systemic release of the cytotoxic payload or binding to non-tumor cells can lead to adverse effects, impacting patient safety and limiting their broader applicability. Additionally, cancer cells can develop resistance mechanisms to ADCs over time, similar to other targeted therapies, leading to treatment failure. These challenges necessitate ongoing research into improved ADC constructs with enhanced therapeutic windows and the development of effective combination strategies to circumvent resistance, adding to the development burden.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Manufacturing Costs | -2.0% | Global | 2025-2033 |

| Complex Manufacturing & Supply Chain | -1.5% | Global | 2025-2030 |

| Potential for Off-Target Toxicity & Resistance | -1.0% | Global | 2025-2033 |

| Stringent Regulatory Requirements | -0.8% | North America, Europe | 2025-2028 |

Antibody Drug Conjugate Market Opportunities Analysis

The Antibody Drug Conjugate (ADC) market presents significant opportunities driven by the exploration of novel linker and payload technologies. Advances in these critical components are enabling the development of next-generation ADCs with superior stability in circulation, enhanced tumor-specific drug release, and improved therapeutic indices. Researchers are actively pursuing innovative linker designs that prevent premature payload cleavage and novel payloads with diverse mechanisms of action, including topoisomerase inhibitors and DNA-damaging agents, which can overcome existing resistance mechanisms and expand the range of treatable cancers. This continuous innovation fosters a robust pipeline and opens avenues for highly effective therapies.

Another substantial opportunity lies in the expansion of ADCs into non-oncology indications, such as autoimmune diseases and infectious diseases. The highly specific targeting capabilities of antibodies, combined with the potency of a conjugated therapeutic agent, make ADCs an attractive modality for delivering drugs to specific cell types implicated in these conditions. Although early-stage, the successful application of ADCs in these areas could unlock vast untapped markets beyond traditional oncology, diversifying revenue streams and broadening the therapeutic utility of this platform technology. This strategic diversification requires significant investment in preclinical and clinical research to validate safety and efficacy in new disease contexts.

Furthermore, the increasing trend towards combination therapies offers a major growth opportunity for the ADC market. Integrating ADCs with other treatment modalities, such as immune checkpoint inhibitors, chemotherapy, or radiation therapy, has shown synergistic effects in preclinical and clinical studies, leading to enhanced tumor responses and potentially overcoming drug resistance. These combination strategies aim to leverage the distinct advantages of each therapeutic approach, offering more comprehensive and durable treatment options for patients. Successful development and regulatory approval of these combination regimens will significantly expand the market potential and clinical adoption of ADCs, driving innovation in treatment paradigms.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Linker & Payload Technologies | +3.0% | Global | 2025-2033 |

| Expansion into Non-Oncology Indications | +2.5% | Global | 2028-2033 |

| Growing Adoption of Combination Therapies | +2.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Emergence of Biosimilar ADCs & Biobetters | +1.5% | Asia Pacific, Latin America | 2030-2033 |

Antibody Drug Conjugate Market Challenges Impact Analysis

The Antibody Drug Conjugate (ADC) market faces significant challenges, particularly concerning the complexity and cost of clinical development. The intricate nature of ADCs, combining a monoclonal antibody, a linker, and a potent cytotoxic payload, necessitates extensive preclinical validation and highly complex clinical trial designs to assess efficacy, safety, and optimal dosing. High attrition rates in clinical trials for complex biologics, coupled with the extended timelines and substantial financial investment required for each development stage, pose a considerable barrier to market entry and growth. This complexity often leads to higher R&D costs and longer time-to-market compared to conventional small molecule drugs.

Another major challenge lies in overcoming the development of drug resistance and managing potential off-target toxicities. Despite their targeted nature, cancer cells can evolve mechanisms to evade ADC efficacy, such as altered antigen expression, impaired drug internalization, or enhanced efflux pumps, leading to acquired resistance over time. Additionally, even with improved linker stability, some systemic release of the highly potent payload can occur, resulting in dose-limiting toxicities that affect healthy tissues and impact patient quality of life. Addressing these issues requires continuous innovation in ADC design and the exploration of novel combination strategies, adding further layers of research and development complexity.

The manufacturing and regulatory landscape also presents substantial hurdles. The production of ADCs involves highly specialized and controlled processes for each component, followed by precise conjugation, requiring advanced facilities and expertise that are not universally available. This often leads to reliance on specialized contract manufacturing organizations (CMOs), potentially creating supply chain vulnerabilities. Furthermore, navigating diverse and stringent global regulatory requirements for these complex biologics, including demonstrating consistency in drug-to-antibody ratios and payload integrity, adds significant time and cost to the approval process, impacting market launch and commercialization timelines.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Clinical Development Costs & Attrition | -2.0% | Global | 2025-2033 |

| Managing Drug Resistance & Off-Target Toxicity | -1.8% | Global | 2025-2033 |

| Complex Manufacturing & Regulatory Hurdles | -1.5% | North America, Europe, Asia Pacific | 2025-2030 |

| Competition from Alternative Targeted Therapies | -1.2% | Global | 2025-2033 |

Antibody Drug Conjugate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Antibody Drug Conjugate (ADC) market, offering a detailed assessment of its current status, historical trends, and future growth projections. The scope encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. Special attention is given to the impact of emerging technologies such as Artificial Intelligence (AI) on ADC development and commercialization. Furthermore, the report delves into detailed market segmentation by type, technology, application, target antigen, and end-use, alongside a granular regional analysis, to provide a holistic view of the market dynamics from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 45.0 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Seagen Inc. (now part of Pfizer), AstraZeneca Plc, Roche Holdings AG, Daiichi Sankyo Company, Limited, Pfizer Inc., Merck KGaA, Bristol-Myers Squibb Company, Gilead Sciences Inc., Takeda Pharmaceutical Company Limited, Genentech, Inc., CytomX Therapeutics, Inc., Immunogen, Inc., Lonza Group AG, WuXi Biologics, Mersana Therapeutics, Inc., BioNTech SE, Sutro Biopharma, Inc., MacroGenics, Inc., Byondis B.V., Amgen Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Antibody Drug Conjugate (ADC) market is meticulously segmented to provide granular insights into its diverse components and applications, enabling a comprehensive understanding of industry dynamics. This segmentation facilitates detailed analysis of therapeutic areas, technological preferences, and end-user adoption patterns, offering stakeholders a clear view of where growth is concentrated and where opportunities for innovation and market penetration exist. Each segment reflects critical aspects of the ADC ecosystem, from the foundational components to their ultimate clinical deployment.

By dissecting the market along these various axes, the report identifies key trends within specific therapeutic applications, such as the dominance of breast and lung cancers in ADC development, while also highlighting the emergence of new target antigens and the ongoing evolution of linker and payload technologies. This granular analysis is crucial for pharmaceutical companies in strategic planning, R&D investment decisions, and market positioning. Furthermore, understanding the preferences and demands across different end-use sectors, including hospitals and specialized cancer centers, informs commercialization strategies and distribution networks, ensuring that ADCs reach the patient populations most in need efficiently.

- By Type: Monoclonal Antibody, Linker, Cytotoxic Drug/Payload

- By Technology: Cleavable Linker Technology, Non-Cleavable Linker Technology

- By Application: Breast Cancer, Lung Cancer, Leukemia, Lymphoma, Multiple Myeloma, Other Cancers (Gastric, Ovarian, Bladder)

- By Target Antigen: HER2, CD30, CD33, Trop-2, Nectin-4, BCMA, Other Antigens

- By End-Use: Hospitals, Specialty Clinics, Cancer Research Centers, Biopharmaceutical Companies

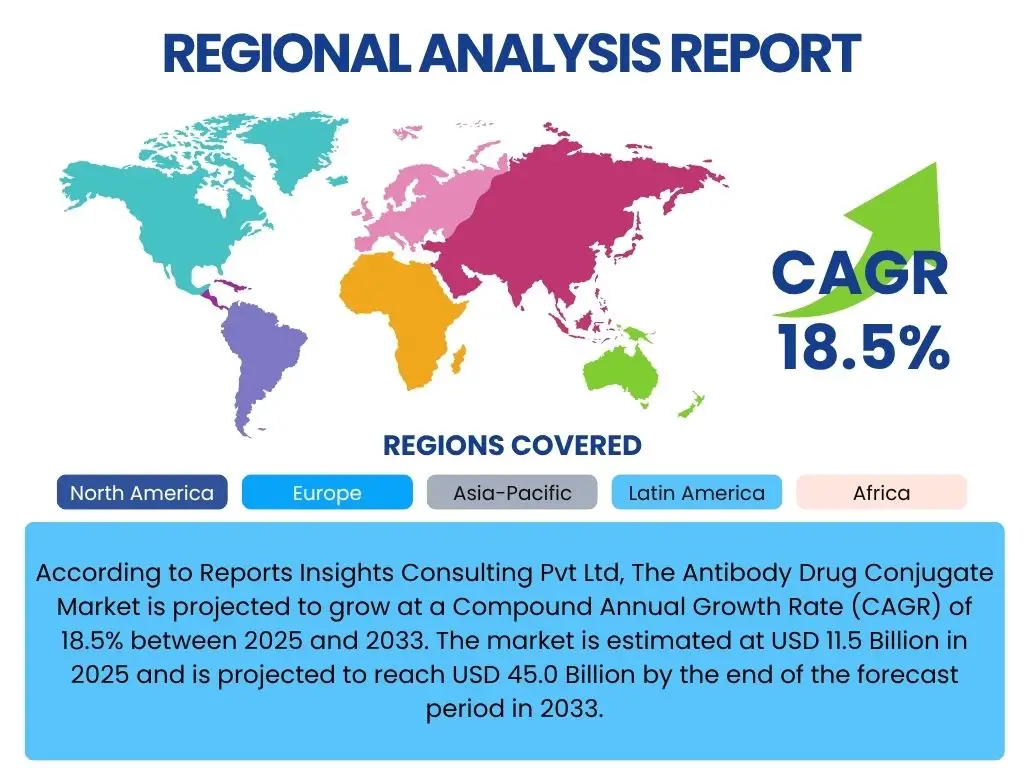

Regional Highlights

North America is anticipated to maintain its dominant position in the Antibody Drug Conjugate (ADC) market, driven by substantial R&D investments, a robust biopharmaceutical infrastructure, and early adoption of advanced therapies. The region benefits from a high prevalence of cancer, favorable reimbursement policies, and the presence of numerous key market players and research institutions. The United States, in particular, leads in clinical trials and new product approvals, consistently pushing the boundaries of ADC innovation and market penetration. This strong ecosystem supports both the development and rapid commercialization of novel ADC therapeutics, making it a critical hub for market growth and technological advancements.

Europe represents another significant market for ADCs, characterized by increasing healthcare expenditure, a rising incidence of cancer, and supportive government initiatives for oncology research. Countries such as Germany, the United Kingdom, France, and Switzerland are at the forefront of ADC adoption and clinical research. The region's focus on precision medicine and personalized oncology further accelerates the demand for targeted therapies like ADCs. Additionally, collaborative efforts between academic institutions and pharmaceutical companies in Europe contribute significantly to the pipeline of promising ADC candidates, reinforcing its strong market position.

Asia Pacific is projected to emerge as the fastest-growing region in the ADC market, primarily due to the large and underserved patient population, improving healthcare infrastructure, and rising awareness about advanced cancer treatments. Countries like China, Japan, and India are witnessing increasing investments in biopharmaceutical R&D and manufacturing capabilities. The growing prevalence of cancer, coupled with rising disposable incomes and expanding access to healthcare facilities, is driving the adoption of innovative therapies. Furthermore, the burgeoning Contract Development and Manufacturing Organization (CDMO) sector in this region offers cost-effective solutions for ADC production, attracting global pharmaceutical companies and fostering rapid market expansion.

- North America: Dominant market share due to extensive R&D, robust infrastructure, high cancer prevalence, and favorable reimbursement.

- Europe: Significant market presence fueled by increasing healthcare spending, oncology research initiatives, and emphasis on precision medicine.

- Asia Pacific: Fastest-growing region driven by large patient pools, improving healthcare access, increasing R&D investments, and burgeoning CDMO sector.

- Latin America & MEA: Emerging markets with growing healthcare needs, increasing awareness, and developing infrastructure, offering long-term growth potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Antibody Drug Conjugate Market.- Seagen Inc. (now part of Pfizer)

- AstraZeneca Plc

- Roche Holdings AG

- Daiichi Sankyo Company, Limited

- Pfizer Inc.

- Merck KGaA

- Bristol-Myers Squibb Company

- Gilead Sciences Inc.

- Takeda Pharmaceutical Company Limited

- Genentech, Inc.

- CytomX Therapeutics, Inc.

- Immunogen, Inc.

- Lonza Group AG

- WuXi Biologics

- Mersana Therapeutics, Inc.

- BioNTech SE

- Sutro Biopharma, Inc.

- MacroGenics, Inc.

- Byondis B.V.

- Amgen Inc.

Frequently Asked Questions

Analyze common user questions about the Antibody Drug Conjugate market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Antibody Drug Conjugates (ADCs) and how do they work?

Antibody Drug Conjugates (ADCs) are a class of highly potent biopharmaceutical drugs designed as targeted therapy for cancer. They combine a monoclonal antibody, a cytotoxic drug (payload), and a chemical linker. The antibody specifically targets antigens found on cancer cells, delivering the highly toxic payload directly to the tumor while minimizing damage to healthy cells, thereby reducing systemic side effects.

What are the primary applications of ADCs in the market?

Currently, the primary applications of ADCs are within oncology, specifically for the treatment of various cancer types including breast cancer, lung cancer, leukemia, lymphoma, and multiple myeloma. Their targeted mechanism makes them highly effective in delivering potent chemotherapy agents directly to malignant cells, addressing specific tumor antigens and improving therapeutic outcomes.

What are the key technological advancements driving the ADC market?

Key technological advancements driving the ADC market include innovations in linker technologies (e.g., cleavable vs. non-cleavable linkers, site-specific conjugation), the development of more potent and diverse cytotoxic payloads, and advancements in antibody engineering to improve specificity and stability. These innovations lead to more stable, effective, and safer ADC constructs, expanding their therapeutic potential.

What are the main challenges facing the ADC market?

The main challenges facing the ADC market include the high cost and complexity of development and manufacturing, potential for off-target toxicity, the development of drug resistance mechanisms in cancer cells, and stringent regulatory requirements for approval. Addressing these challenges necessitates ongoing innovation in design and strategic collaborations for production scalability.

How is Artificial Intelligence (AI) impacting the future of ADC development?

Artificial Intelligence (AI) is significantly impacting ADC development by accelerating target identification, optimizing antibody and linker-payload design, and enhancing clinical trial efficiency. AI algorithms can analyze vast biological datasets to predict optimal drug properties, personalize patient stratification, and streamline R&D processes, potentially reducing development timelines and costs for new ADC therapies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted