Plastic Len Market

Plastic Len Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709674 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

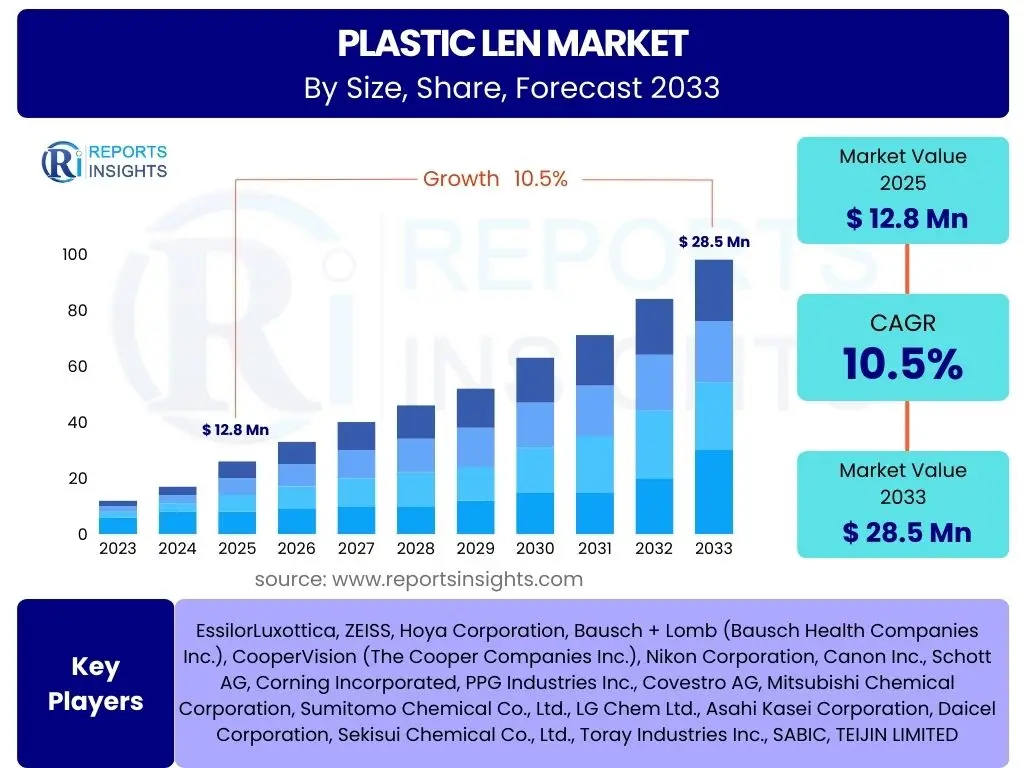

Plastic Len Market Size

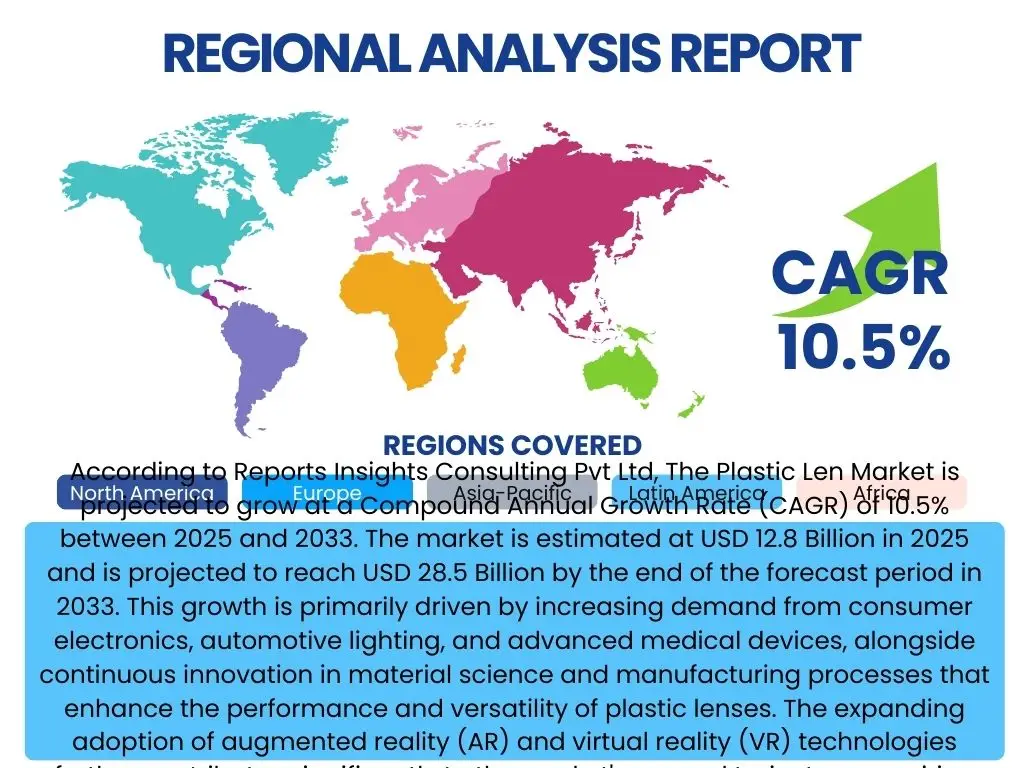

According to Reports Insights Consulting Pvt Ltd, The Plastic Len Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033. This growth is primarily driven by increasing demand from consumer electronics, automotive lighting, and advanced medical devices, alongside continuous innovation in material science and manufacturing processes that enhance the performance and versatility of plastic lenses. The expanding adoption of augmented reality (AR) and virtual reality (VR) technologies further contributes significantly to the market's upward trajectory, requiring lightweight and high-performance optical components.

The robust expansion of the plastic lens market is also fueled by their inherent advantages over traditional glass lenses, including superior impact resistance, reduced weight, and greater flexibility in design and manufacturing. These benefits make plastic lenses ideal for a wide array of applications where durability and customization are paramount. Furthermore, cost-effectiveness in mass production and the ability to integrate complex functionalities make them a preferred choice across various industries. Regional growth is particularly pronounced in Asia Pacific, driven by burgeoning manufacturing hubs and a large consumer base, alongside North America and Europe, which lead in technological advancements and high-value applications.

Key Plastic Len Market Trends & Insights

User inquiries often highlight the dynamic landscape of the plastic lens market, focusing on technological evolution, material innovation, and application diversification. Key themes revolve around the integration of advanced functionalities, the push for sustainable manufacturing, and the customization capabilities that distinguish plastic lenses from their glass counterparts. Users frequently seek information on how these trends translate into new product developments and market opportunities, particularly in emerging high-growth sectors such as advanced driver-assistance systems (ADAS) and wearable technology.

- Integration of advanced coatings for enhanced performance, including anti-reflective, anti-scratch, and hydrophobic properties.

- Development of thinner, lighter, and more durable plastic materials, such as advanced polycarbonates and Trivex.

- Increasing adoption of free-form lens technology, enabling highly customized and precise optical designs.

- Growing demand for plastic lenses in augmented reality (AR), virtual reality (VR), and mixed reality (MR) devices.

- Shift towards sustainable and bio-based plastic materials in response to environmental concerns and regulatory pressures.

- Miniaturization of optical components for compact and portable electronic devices.

- Expansion of plastic lens applications in automotive sectors for lighting, sensors, and interior displays.

AI Impact Analysis on Plastic Len

Common user questions regarding AI's impact on plastic lenses predominantly concern its role in design optimization, manufacturing efficiency, and quality control. Users are keen to understand how artificial intelligence can streamline the complex processes involved in lens production, from initial concept to final product. There is significant interest in AI's potential to reduce material waste, improve precision, and accelerate the development cycle, while also addressing concerns about the automation's implications for labor and the need for specialized skills.

AI is increasingly being leveraged across the entire lifecycle of plastic lens manufacturing, offering substantial improvements in various stages. In the design phase, AI algorithms can simulate optical performance and material behavior, enabling rapid prototyping and optimization of complex lens geometries. During manufacturing, AI-powered systems can monitor production lines, predict potential defects, and adjust parameters in real-time, thereby minimizing errors and maximizing throughput. Furthermore, in quality assurance, machine learning models can perform highly accurate and consistent inspections, identifying microscopic flaws that might be missed by human inspection, ensuring superior product quality and reliability across large production volumes.

- Enhanced Design Optimization: AI algorithms rapidly analyze complex optical properties and material stress, leading to optimized lens geometries for specific applications.

- Predictive Maintenance: AI-driven analytics monitor manufacturing equipment, predicting potential failures and enabling proactive maintenance to reduce downtime.

- Automated Quality Control: Machine vision systems powered by AI perform precise and consistent defect detection, significantly improving product quality and reducing scrap rates.

- Supply Chain Optimization: AI assists in forecasting demand and managing inventory, leading to more efficient raw material procurement and reduced lead times.

- Accelerated Material Discovery: AI helps identify and develop new plastic lens materials with enhanced properties, such as improved refractive index or increased durability.

- Customization at Scale: AI facilitates the design and production of highly customized lenses for individual needs, particularly in medical and eyewear applications.

Key Takeaways Plastic Len Market Size & Forecast

User queries frequently highlight a desire to understand the overarching narrative of the plastic lens market's growth, focusing on the primary drivers, the most promising application areas, and the long-term sustainability. The key takeaways underscore the market's resilience and adaptability, driven by continuous innovation and expanding utility across diverse industries. Users are particularly interested in the factors that will sustain this growth trajectory and the strategic implications for businesses operating within or looking to enter this dynamic sector, emphasizing both technological advancements and market demand shifts.

The plastic lens market is positioned for significant and sustained expansion through 2033, propelled by an confluence of technological innovation and increasing global demand across several key industries. The inherent advantages of plastic lenses, such as their lightweight nature, durability, and design flexibility, continue to make them a preferred choice over traditional glass alternatives, especially in applications requiring impact resistance and complex shapes. This growth is further bolstered by the rapid advancements in smart devices, automotive technologies, and sophisticated medical instruments, all of which increasingly rely on high-performance optical components. The market's future will be characterized by continued material science breakthroughs, advanced manufacturing techniques, and a strong emphasis on customizable and sustainable solutions, ensuring its pivotal role in the optical industry.

- The market is set for robust double-digit CAGR growth, driven by expanding applications in consumer electronics, automotive, and medical sectors.

- Technological advancements in material science and manufacturing processes are critical enablers for market expansion.

- Asia Pacific will remain a dominant and rapidly growing region due to its large manufacturing base and increasing industrialization.

- Focus on lightweight, durable, and customizable plastic lenses will be a key differentiator and growth catalyst.

- Sustainability initiatives, including the development of bio-based plastics and recycling programs, are becoming increasingly important for market competitiveness and consumer acceptance.

Plastic Len Market Drivers Analysis

The plastic lens market is significantly propelled by several key factors that underscore its increasing importance across various industries. A primary driver is the accelerating demand for lightweight, durable, and cost-effective optical components in a wide array of applications. This demand is particularly pronounced in high-growth sectors such as consumer electronics, where miniaturization and performance are paramount, and in the automotive industry, which seeks improved safety and aesthetic integration through advanced lighting and sensor systems. The continuous innovation in plastic materials and manufacturing technologies further enhances the versatility and performance of plastic lenses, allowing them to meet increasingly stringent technical requirements.

Moreover, the growing global population and rising disposable incomes contribute to increased consumption of eyewear, including ophthalmic and contact lenses, where plastic offers superior comfort and impact resistance. The expansion of the healthcare sector also fuels demand for plastic lenses in medical devices, such as endoscopes and diagnostic equipment, benefiting from their sterilizability and design flexibility. Additionally, the emergence of augmented reality (AR) and virtual reality (VR) technologies presents a substantial growth avenue, as these devices heavily rely on sophisticated, lightweight plastic optical systems to deliver immersive user experiences, further cementing the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Consumer Electronics (Smartphones, AR/VR) | +3.2% | Global, particularly Asia Pacific (China, South Korea) & North America | Short to Medium-Term |

| Increasing Use in Automotive Lighting & Sensor Systems | +2.8% | Europe (Germany), North America, Asia Pacific (Japan) | Medium to Long-Term |

| Advancements in Material Science and Manufacturing Technologies | +2.5% | Global, concentrated in developed economies | Short to Long-Term |

| Rising Adoption of Eyewear (Ophthalmic & Contact Lenses) | +1.5% | Global, especially emerging economies | Short to Medium-Term |

| Expanding Applications in Medical Devices & Diagnostics | +1.0% | North America, Europe, parts of Asia Pacific | Medium-Term |

Plastic Len Market Restraints Analysis

Despite its robust growth potential, the plastic lens market faces several restraints that could impede its expansion. One significant challenge is the fluctuating cost of raw materials, such as petroleum-based polymers, which can lead to unpredictable manufacturing expenses and impact profit margins. This volatility makes long-term planning difficult for manufacturers and can translate into higher product costs for consumers, potentially affecting market demand in price-sensitive segments. Additionally, the inherent environmental concerns associated with plastic waste and non-biodegradable materials pose a substantial hurdle, particularly in regions with stringent environmental regulations and a strong consumer preference for sustainable products.

Another restraint stems from the competition with traditional glass lenses, which, despite being heavier and more fragile, still offer superior optical clarity and scratch resistance in certain high-precision applications. While plastic lenses have made significant strides, overcoming this perception and performance gap in specialized fields remains a challenge. Furthermore, the complexity of manufacturing high-precision plastic optics, which often requires advanced molding techniques and specialized equipment, can lead to higher initial investment costs and longer development cycles, particularly for intricate designs. Regulatory pressures concerning material safety and disposal also add to the operational complexities and compliance costs for manufacturers, potentially slowing market adoption in some areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Petroleum-based Polymers) | -1.5% | Global | Short to Medium-Term |

| Environmental Concerns and Regulatory Pressures on Plastic Waste | -1.2% | Europe, North America, specific Asian countries | Medium to Long-Term |

| Competition from Traditional Glass Lenses in High-Precision Applications | -0.8% | Global, niche markets | Medium-Term |

| Complexity and High Initial Investment for Advanced Manufacturing Techniques | -0.7% | Global, especially smaller players | Short to Medium-Term |

| Performance Limitations (e.g., scratch resistance) compared to Glass Lenses | -0.5% | Global, high-end optics | Medium-Term |

Plastic Len Market Opportunities Analysis

The plastic lens market presents numerous compelling opportunities for growth and innovation. The increasing demand for customized and personalized optical solutions, particularly in the eyewear and medical sectors, opens significant avenues for specialized manufacturers. Advances in additive manufacturing, such as 3D printing, are enabling the creation of intricate and complex lens designs previously unattainable with traditional methods, catering to niche applications and individual patient needs. This capability not only enhances product differentiation but also allows for rapid prototyping and reduced time-to-market for new optical devices, fostering innovation.

Furthermore, the growing emphasis on sustainability and the development of bio-based and recyclable plastic materials offer a substantial opportunity for companies to enhance their environmental profile and appeal to eco-conscious consumers and regulators. Investment in research and development for such materials can lead to breakthroughs that address current environmental concerns, providing a competitive edge. The expansion into untapped emerging markets, particularly in Asia Pacific and Latin America, also offers vast potential due to increasing disposable incomes, improving healthcare infrastructure, and rising adoption of consumer electronics. Strategic partnerships and collaborations with technology companies can further accelerate the integration of plastic lenses into next-generation smart devices and immersive technologies, unlocking new revenue streams and market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based and Recyclable Plastic Lens Materials | +2.0% | Global, particularly Europe and North America | Medium to Long-Term |

| Expansion into Emerging Markets (APAC, Latin America) | +1.8% | Asia Pacific (India, Southeast Asia), Latin America | Short to Medium-Term |

| Integration into Advanced AR/VR/MR Devices and Wearables | +1.5% | North America, Asia Pacific (Japan, South Korea) | Medium to Long-Term |

| Customization and Personalization through Advanced Manufacturing (e.g., 3D Printing) | +1.0% | Global, high-value markets | Short to Medium-Term |

| Strategic Partnerships for Cross-Industry Application Development | +0.7% | Global | Medium-Term |

Plastic Len Market Challenges Impact Analysis

The plastic lens market faces several significant challenges that require strategic navigation to sustain growth. One prominent challenge is ensuring consistent product quality and durability, especially for high-precision applications, while maintaining cost-effectiveness. The perception that plastic lenses are less durable or optically inferior to glass lenses in certain specialized contexts continues to influence consumer and industry choices, necessitating continuous innovation in material science and surface treatments to overcome this bias. Furthermore, the rapid pace of technological change in end-use industries, particularly in consumer electronics and automotive, demands constant adaptation and investment in research and development to keep pace with evolving design requirements and performance standards, which can strain resources for manufacturers.

Another critical challenge is managing supply chain complexities and disruptions, especially given the global nature of raw material sourcing and manufacturing. Geopolitical tensions, trade barriers, and natural disasters can significantly impact the availability and cost of essential materials, leading to production delays and increased operational expenses. The plastic lens market also contends with intellectual property protection issues, as innovative designs and manufacturing processes are susceptible to counterfeiting and unauthorized replication, particularly in less regulated markets. Moreover, attracting and retaining skilled labor for advanced manufacturing techniques and precision optics production remains a hurdle, with a shortage of expertise potentially limiting growth and efficiency. Addressing these multifaceted challenges will be crucial for companies aiming to thrive in this dynamic market environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Product Quality and Durability in Mass Production | -1.0% | Global | Short to Medium-Term |

| Supply Chain Disruptions and Raw Material Sourcing Volatility | -0.9% | Global | Short to Medium-Term |

| High Investment in R&D to Keep Pace with Rapid Technological Advancements | -0.8% | Global, particularly developed markets | Medium-Term |

| Intellectual Property Protection and Counterfeiting Concerns | -0.7% | Asia Pacific, emerging markets | Medium to Long-Term |

| Shortage of Skilled Labor for Advanced Manufacturing and Optics Design | -0.6% | North America, Europe, parts of Asia Pacific | Medium to Long-Term |

Plastic Len Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global plastic lens market, offering critical insights into its current size, historical performance, and future growth projections through 2033. The scope encompasses detailed market segmentation by material type, application, and end-use industry, providing a granular understanding of market dynamics across various categories. Furthermore, the report delves into key market drivers, restraints, opportunities, and challenges, along with an impact analysis of artificial intelligence on the industry. It also includes a thorough regional analysis covering major geographies and highlights the competitive landscape by profiling leading market players and their strategic initiatives, enabling stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | EssilorLuxottica, ZEISS, Hoya Corporation, Bausch + Lomb (Bausch Health Companies Inc.), CooperVision (The Cooper Companies Inc.), Nikon Corporation, Canon Inc., Schott AG, Corning Incorporated, PPG Industries Inc., Covestro AG, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., LG Chem Ltd., Asahi Kasei Corporation, Daicel Corporation, Sekisui Chemical Co., Ltd., Toray Industries Inc., SABIC, TEIJIN LIMITED |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plastic lens market is broadly segmented based on material type, application, and manufacturing process, reflecting the diverse range of products and their specialized uses. Each segment plays a crucial role in shaping the overall market landscape, with different material types offering distinct optical and mechanical properties, catering to varied performance requirements. Application segmentation highlights the primary end-use industries driving demand, from consumer-centric eyewear to high-technology automotive and medical devices. Furthermore, analyzing the market by manufacturing process provides insights into production efficiencies, technological advancements, and cost structures inherent in the fabrication of plastic lenses, underlining the market's technological sophistication.

This granular segmentation allows for a comprehensive understanding of market dynamics, growth drivers, and challenges within specific niches. For instance, the rise of polycarbonate lenses is directly linked to demand from impact-resistant eyewear and advanced automotive lighting, while CR-39 remains popular for its optical clarity in traditional ophthalmic applications. The evolution of manufacturing processes, such as advanced injection molding and precision casting, continually pushes the boundaries of design complexity and production efficiency, enabling the development of next-generation optical components for emerging technologies like AR/VR and specialized medical imaging. Understanding these interdependencies is crucial for market participants to identify lucrative opportunities and tailor their strategies effectively across the value chain.

- By Material Type:

- Polycarbonate

- CR-39 (Allyl Diglycol Carbonate)

- Acrylic (PMMA)

- Polyamide (Nylon)

- Trivex

- Polyurethane

- Others (e.g., COC/COP, PMMA-based copolymers)

- By Application:

- Eyewear

- Ophthalmic Lenses

- Contact Lenses

- Safety Eyewear

- Sunglasses

- Automotive

- Headlights & Tail Lights

- Interior Lighting

- Sensor Lenses (ADAS)

- Display Screens

- Consumer Electronics

- Camera Lenses (Smartphones, Digital Cameras)

- Displays (TVs, Monitors)

- AR/VR/MR Headsets

- Projection Systems

- Medical & Healthcare

- Endoscopes

- Diagnostic Tools

- Surgical Lights

- Medical Imaging

- Industrial

- Machine Vision Systems

- Safety Goggles & Shields

- Inspection Systems

- Optics & Imaging

- Cameras (Professional & Consumer)

- Binoculars & Telescopes

- Microscopes

- Others (e.g., Security & Surveillance, Research & Development)

- Eyewear

- By Manufacturing Process:

- Injection Molding

- Cast Molding

- Compression Molding

- Extrusion

- Additive Manufacturing (3D Printing)

Regional Highlights

- North America: This region is characterized by high adoption rates of advanced medical devices and consumer electronics, along with significant investment in research and development for new optical technologies. The presence of key market players and a robust healthcare infrastructure contribute to its stable growth.

- Europe: Europe exhibits strong demand from the automotive industry, particularly for advanced lighting systems and ADAS applications. Strict environmental regulations also drive innovation in sustainable plastic lens materials and manufacturing processes.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for plastic lenses, propelled by vast manufacturing capabilities, increasing disposable incomes, and the booming consumer electronics and automotive sectors in countries like China, India, Japan, and South Korea.

- Latin America: This region is an emerging market with growing demand for eyewear and medical devices, fueled by improving healthcare access and urbanization. Economic growth and increasing industrialization present significant opportunities.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, driven by expanding healthcare infrastructure and rising demand for consumer goods. Investment in urban development and technology adoption will further stimulate the market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic Len Market.- EssilorLuxottica

- ZEISS

- Hoya Corporation

- Bausch + Lomb (Bausch Health Companies Inc.)

- CooperVision (The Cooper Companies Inc.)

- Nikon Corporation

- Canon Inc.

- Schott AG

- Corning Incorporated

- PPG Industries Inc.

- Covestro AG

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co., Ltd.

- LG Chem Ltd.

- Asahi Kasei Corporation

- Daicel Corporation

- Sekisui Chemical Co., Ltd.

- Toray Industries Inc.

- SABIC

- TEIJIN LIMITED

Frequently Asked Questions

What are the primary advantages of plastic lenses over glass lenses?

Plastic lenses offer significant benefits including lighter weight, superior impact resistance (making them safer), greater flexibility in design and tinting, and inherent UV protection. They are also less prone to shattering compared to glass, making them ideal for eyewear and many industrial applications.

Which industries are the largest consumers of plastic lenses?

The largest consumers of plastic lenses include the eyewear industry (ophthalmic, contact, and safety lenses), consumer electronics (camera lenses for smartphones, AR/VR headsets), and the automotive sector (headlights, interior lighting, sensor systems).

What types of plastic materials are commonly used for lenses?

Common plastic materials for lenses include Polycarbonate (known for impact resistance), CR-39 (Allyl Diglycol Carbonate, offering excellent optical clarity), Acrylic (PMMA, lightweight and cost-effective), Polyamide (Nylon), Trivex (high impact resistance and clarity), and Polyurethane.

How is sustainability impacting the plastic lens market?

Sustainability is a growing concern, driving demand for bio-based and recyclable plastic lens materials. Manufacturers are increasingly investing in eco-friendly production processes and developing alternative materials to reduce environmental impact and meet regulatory requirements.

What role does AI play in the future of plastic lens manufacturing?

AI is set to revolutionize plastic lens manufacturing by optimizing design processes, enabling predictive maintenance for equipment, automating quality control through machine vision, and streamlining supply chain management. This leads to increased efficiency, precision, and the development of highly customized optical solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted