Magnetite Iron Ore Market

Magnetite Iron Ore Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708465 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

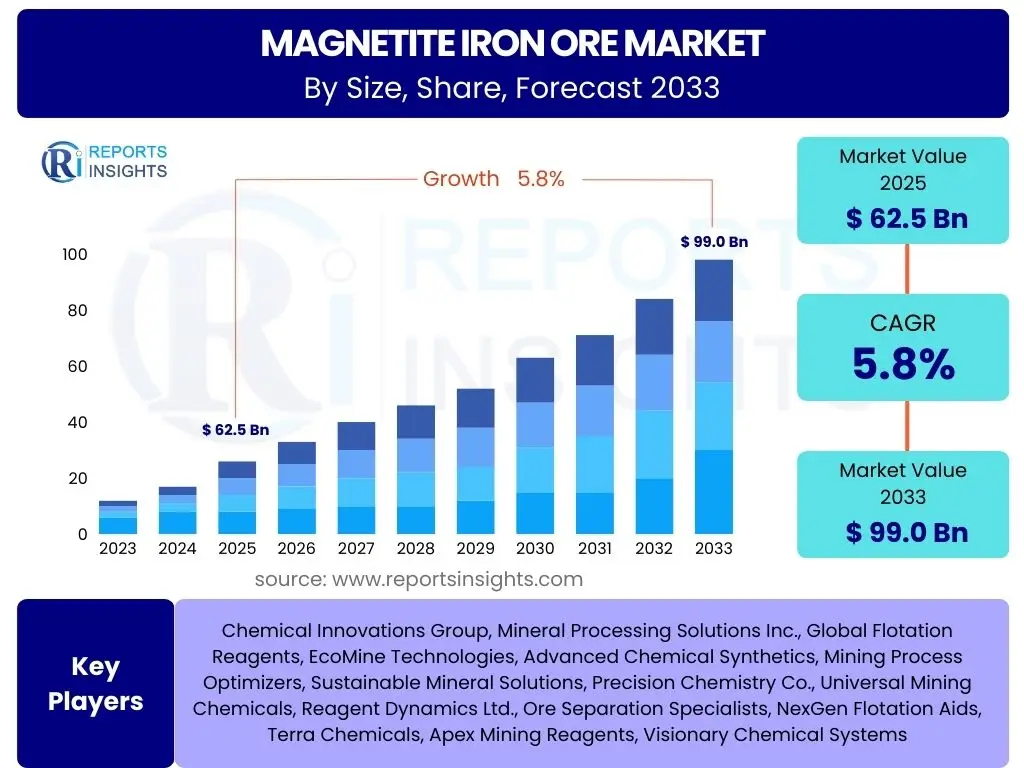

Magnetite Iron Ore Market Size

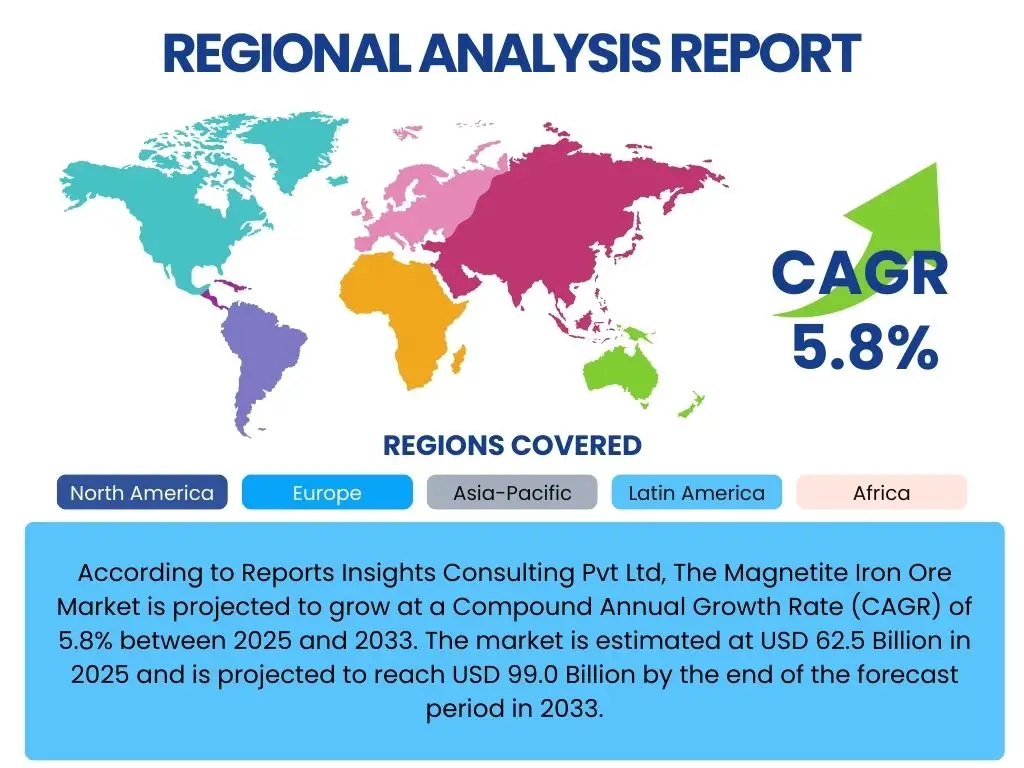

According to Reports Insights Consulting Pvt Ltd, The Magnetite Iron Ore Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 62.5 Billion in 2025 and is projected to reach USD 99.0 Billion by the end of the forecast period in 2033.

Key Magnetite Iron Ore Market Trends & Insights

The Magnetite Iron Ore market is experiencing significant evolution, driven by shifts in global steel production and increasing environmental considerations. Users frequently inquire about the trajectory of demand, the influence of technological advancements in mining and processing, and the role of sustainability initiatives in shaping market dynamics. The prevailing trend indicates a strong preference for high-grade iron ore concentrates, directly impacting the demand for magnetite due to its suitability for beneficiation processes that yield purer products.

Furthermore, the market is observing a geographical rebalancing of supply and demand, with Asia-Pacific nations, particularly China and India, continuing to dominate consumption while new supply regions gain prominence. Investment in advanced crushing, grinding, and magnetic separation technologies is becoming crucial for producers to enhance efficiency and reduce operational costs. The integration of digital technologies and automation in mining operations also represents a critical area of interest, promising improved safety, productivity, and resource utilization across the value chain. These technological adoptions are not merely incremental improvements but represent foundational shifts in how magnetite iron ore is extracted and processed.

- Increasing demand for high-grade iron ore pellets and concentrates for steelmaking.

- Rising adoption of advanced beneficiation techniques, including magnetic separation and flotation.

- Focus on decarbonization in the steel industry driving demand for lower-emission iron sources.

- Geographical shift in supply chain, with new mines and processing capacities emerging.

- Growing integration of automation and digital technologies in mining operations.

- Emphasis on circular economy principles and resource efficiency in mineral processing.

- Volatility in global commodity prices influencing investment decisions and production volumes.

AI Impact Analysis on Magnetite Iron Ore

Users are increasingly interested in how artificial intelligence (AI) and machine learning (ML) are transforming the Magnetite Iron Ore sector. Common questions revolve around AI's ability to optimize mining operations, predict market fluctuations, and enhance environmental compliance. The consensus is that AI offers substantial opportunities for improving efficiency, reducing costs, and boosting productivity throughout the mining lifecycle, from exploration and extraction to processing and logistics. Predictive analytics, powered by AI, can forecast equipment failures, optimize maintenance schedules, and improve ore body modeling, thereby maximizing resource recovery.

The application of AI extends beyond operational efficiencies, impacting strategic decision-making and sustainability efforts. AI-driven systems can analyze vast datasets to identify optimal drilling locations, predict market price trends with greater accuracy, and monitor environmental parameters in real-time, aiding in compliance and impact mitigation. While the adoption of AI is still in its nascent stages for many smaller players, major mining corporations are actively investing in these technologies to gain a competitive edge, streamline their complex operations, and respond more effectively to dynamic market conditions. This strategic integration is expected to become a standard practice, reshaping industry benchmarks for performance and sustainability.

- Enhanced exploration and resource modeling through AI-powered data analysis.

- Optimization of drilling, blasting, and material handling processes using machine learning algorithms.

- Predictive maintenance for mining equipment, reducing downtime and operational costs.

- Improved quality control and process optimization in beneficiation plants.

- Real-time monitoring and analysis of environmental impacts and regulatory compliance.

- Supply chain optimization and logistics management through AI-driven forecasting.

- Market intelligence and price trend prediction for strategic decision-making.

Key Takeaways Magnetite Iron Ore Market Size & Forecast

The Magnetite Iron Ore market is poised for steady growth, reflecting its critical role in global steel production, especially as the industry shifts towards higher-quality inputs and sustainable practices. Users frequently seek concise insights into the market's trajectory, the underlying drivers of this growth, and the key factors that will influence its expansion or contraction. The primary takeaway is the sustained demand for high-grade iron ore, with magnetite being uniquely positioned due to its amenability to beneficiation, which yields premium products essential for modern, efficient steelmaking processes. This inherent advantage ensures its continued relevance and market stability.

Furthermore, the forecast highlights the increasing importance of technological innovation and environmental considerations in shaping market dynamics. The expected growth in market value is not merely a reflection of increasing production volumes but also of the value added through advanced processing and a premium placed on responsibly sourced materials. Market participants must therefore prioritize investments in efficient mining and processing technologies, alongside robust environmental, social, and governance (ESG) frameworks, to capitalize on the anticipated growth and maintain a competitive edge throughout the forecast period. The market's resilience is intrinsically linked to its ability to adapt to evolving global industrial demands and regulatory landscapes.

- Consistent demand for high-grade iron ore driven by global steel production.

- Significant growth anticipated, reaching nearly USD 100 billion by 2033.

- Beneficiation capabilities of magnetite are a key competitive advantage.

- Technological advancements in mining and processing are crucial for market expansion.

- Sustainability and decarbonization initiatives heavily influence market direction.

- Asia-Pacific region remains the dominant consumer, driving significant portion of demand.

- Strategic investments in ESG practices are becoming imperative for market players.

Magnetite Iron Ore Market Drivers Analysis

The Magnetite Iron Ore market is primarily propelled by the persistent global demand for steel, an essential material for infrastructure, manufacturing, and construction. As urbanization and industrialization continue, particularly in developing economies, the need for high-quality steel products remains robust, directly fueling the consumption of iron ore. Magnetite's superior properties, especially its high iron content after beneficiation, make it a preferred feedstock for producing premium steel, which is critical for meeting stringent quality standards in various applications. This foundational demand creates a sustained impetus for market expansion.

Moreover, the increasing focus on environmental sustainability and the decarbonization of the steel industry are significant drivers. Steelmakers are under pressure to reduce their carbon footprint, leading to a greater preference for blast furnace-efficient and direct reduced iron (DRI) grade ores, which often require high-grade concentrates derived from magnetite. Technological advancements in mining and beneficiation techniques also contribute to market growth by enabling more efficient extraction and processing, reducing operational costs, and increasing the supply of high-quality magnetite concentrates. These technological improvements make magnetite more economically viable and environmentally attractive, further solidifying its market position.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Steel Production | +1.5% | Asia Pacific (China, India), North America, Europe | Long-term (2025-2033) |

| Demand for High-Grade Iron Ore Concentrates | +1.2% | Global | Mid to Long-term (2025-2033) |

| Technological Advancements in Beneficiation | +0.8% | Global | Mid-term (2025-2030) |

| Decarbonization Efforts in Steel Industry | +0.7% | Europe, North America, Japan, South Korea | Long-term (2027-2033) |

Magnetite Iron Ore Market Restraints Analysis

Despite its growth prospects, the Magnetite Iron Ore market faces several notable restraints. Price volatility of iron ore in the global commodities market is a significant concern for producers and investors. Fluctuations, often driven by shifts in global demand, geopolitical events, or changes in supply from major producers, can impact profitability and investment decisions. This unpredictability makes long-term planning challenging and can deter new market entrants or expansion projects, thereby limiting the overall growth potential of the market.

Environmental regulations and escalating operational costs also pose substantial challenges. Mining and processing magnetite ore require significant energy and water resources, and stringent environmental compliance, particularly concerning tailings management and emissions, adds to the financial burden. The capital intensity of establishing new mines or upgrading existing facilities, coupled with rising labor costs and energy prices, can constrain production capacity and hinder the adoption of advanced, more sustainable technologies. These factors collectively impact the economic viability of magnetite projects, particularly in regions with high regulatory scrutiny or limited infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Iron Ore Price Volatility | -0.9% | Global | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations | -0.7% | Europe, North America, Australia | Long-term (2025-2033) |

| High Capital Expenditure for Mining & Beneficiation | -0.6% | Global | Long-term (2025-2033) |

| Dependency on Global Economic Health | -0.5% | Global | Short-term (2025-2027) |

Magnetite Iron Ore Market Opportunities Analysis

The Magnetite Iron Ore market presents compelling opportunities, primarily driven by the ongoing shift towards green steel production and the increasing adoption of direct reduced iron (DRI) processes. As the global steel industry seeks to reduce its carbon footprint, high-grade magnetite concentrates become indispensable for producing premium pellets suitable for DRI, a less carbon-intensive steelmaking route. This technological transition opens new avenues for magnetite producers who can meet the stringent quality specifications required for these advanced processes. Investment in facilities capable of producing such high-purity concentrates represents a significant strategic advantage and growth opportunity.

Additionally, the exploration and development of new magnetite deposits in politically stable regions, coupled with advancements in resource extraction and processing technologies, offer substantial market expansion potential. Regions with untapped or underdeveloped magnetite reserves can emerge as new supply hubs, diversifying the global supply chain and reducing reliance on traditional sources. Furthermore, the development of innovative uses for tailings and by-products from magnetite processing, such as in construction materials or other industrial applications, could create new revenue streams and enhance the overall sustainability profile of the industry, contributing to long-term value creation. These opportunities are critical for stakeholders seeking to innovate and expand their market presence.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Green Steel and DRI Production | +1.3% | Europe, North America, Middle East | Long-term (2026-2033) |

| Development of New Magnetite Deposits | +1.0% | Africa, South America, Australia | Mid to Long-term (2028-2033) |

| Innovation in Tailings Management & By-product Utilization | +0.6% | Global | Mid-term (2025-2030) |

| Investment in Advanced Digital Mining Solutions | +0.5% | Global | Short to Mid-term (2025-2029) |

Magnetite Iron Ore Market Challenges Impact Analysis

The Magnetite Iron Ore market faces significant challenges, particularly related to the energy intensity of beneficiation processes and the substantial water requirements. The crushing, grinding, and magnetic separation stages demand considerable power, leading to high operating costs and contributing to carbon emissions, which conflicts with sustainability goals. The scarcity of freshwater in certain mining regions exacerbates this issue, creating operational bottlenecks and increasing environmental compliance risks. Addressing these resource-intensive processes effectively is a critical hurdle for maintaining profitability and social license to operate.

Moreover, the permitting processes for new mining projects are increasingly complex and lengthy, often involving multiple regulatory bodies and extensive environmental impact assessments. This bureaucratic complexity can cause significant delays, escalating project costs and deterring investment, thereby limiting the expansion of supply capacity. Geopolitical instabilities and trade disputes also pose a threat, potentially disrupting supply chains, altering trade flows, and impacting market access for producers. These external factors introduce an element of uncertainty that requires robust risk management strategies from all market participants to mitigate potential adverse impacts on market stability and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy & Water Consumption in Beneficiation | -0.8% | Global | Long-term (2025-2033) |

| Complex & Lengthy Permitting Processes | -0.7% | North America, Europe, Australia | Long-term (2025-2033) |

| Geopolitical Instability & Trade Disruptions | -0.6% | Global | Short-term (2025-2027) |

| Skilled Labor Shortages in Mining Sector | -0.4% | Global | Mid-term (2025-2030) |

Magnetite Iron Ore Market - Updated Report Scope

This comprehensive market report provides a detailed analysis of the global Magnetite Iron Ore market, offering insights into market size, growth drivers, restraints, opportunities, and challenges from 2019 to 2033. It includes an in-depth segmentation analysis by product type, application, and end-use, alongside a thorough regional and competitive landscape assessment to empower strategic business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 62.5 Billion |

| Market Forecast in 2033 | USD 99.0 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Metals & Mining Inc., OreMax Solutions Ltd., IronPeak Resources Corp., MetIron Minerals PLC, Stellar Mining Group, Core Iron Products Ltd., Zenith Ore Holdings, Universal Ironworks, Genesis Mineral Group, Apex Raw Materials, Dynamic Iron Ore Co., Vanguard Mining Solutions, Frontier Iron & Steel, Harmony Minerals Ltd., Prime Ore International, Phoenix Resources Group, Summit Iron Ore, Mega Mining Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Magnetite Iron Ore market is comprehensively segmented to provide granular insights into its various components, reflecting the diverse forms and applications of this crucial raw material. The segmentation helps in understanding specific market dynamics, demand patterns, and technological preferences across different industrial uses. This detailed breakdown enables stakeholders to identify key growth areas and tailor strategies to specific product types or end-use industries, optimizing resource allocation and market penetration efforts.

The primary segments include product types such as crude ore, concentrate, and pellets, each catering to different stages of steelmaking and other industrial applications. Furthermore, the market is segmented by application, prominently featuring steel production via both blast furnace and direct reduced iron (DRI) routes, which signifies the material’s versatility and importance in modern steelmaking processes. Other applications, including heavy media separation and pigments, also play a crucial role. Finally, the market is analyzed by various end-use industries, highlighting the broad impact of magnetite iron ore on global economic activities from construction to automotive manufacturing and energy.

- By Product Type:

- Magnetite Ore (Crude)

- Magnetite Concentrate

- Magnetite Pellets

- By Application:

- Steel Production (Blast Furnace, Direct Reduced Iron)

- Heavy Media Separation

- Pigments

- Others

- By End-Use Industry:

- Construction

- Automotive

- Machinery & Equipment

- Energy

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to massive steel production in China, India, Japan, and South Korea; significant infrastructure development and industrial growth drive high demand.

- Europe: Growing focus on green steel initiatives and decarbonization, increasing demand for high-grade magnetite concentrates suitable for DRI processes; stringent environmental regulations influence sourcing strategies.

- North America: Stable demand driven by construction and automotive industries; increasing investment in advanced mining technologies and sustainable practices to enhance domestic supply.

- Latin America: Holds substantial untapped magnetite reserves, particularly in Brazil and Chile; potential for new project development and increased export volumes, influenced by global commodity prices.

- Middle East and Africa (MEA): Emerging as a key region for DRI-based steel production due to abundant natural gas resources (for DRI) and increasing demand for steel in regional infrastructure projects; potential for new magnetite mining investments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Magnetite Iron Ore Market.- Global Metals & Mining Inc.

- OreMax Solutions Ltd.

- IronPeak Resources Corp.

- MetIron Minerals PLC

- Stellar Mining Group

- Core Iron Products Ltd.

- Zenith Ore Holdings

- Universal Ironworks

- Genesis Mineral Group

- Apex Raw Materials

- Dynamic Iron Ore Co.

- Vanguard Mining Solutions

- Frontier Iron & Steel

- Harmony Minerals Ltd.

- Prime Ore International

- Phoenix Resources Group

- Summit Iron Ore

- Mega Mining Corp.

- Global Resources Alliance

- Integrated Iron Solutions

Frequently Asked Questions

What is magnetite iron ore and why is it important?

Magnetite iron ore is a type of iron ore composed primarily of the mineral magnetite (Fe3O4), known for its strong magnetic properties. It is highly valued in the steel industry because it can be beneficiated (processed) to produce very high-grade concentrates and pellets, which are essential for efficient and sustainable steelmaking processes, including direct reduced iron (DRI).

How is magnetite iron ore different from hematite iron ore?

The primary difference lies in their chemical composition and magnetic properties. Magnetite (Fe3O4) typically has a higher iron content (72.4%) when pure and is strongly magnetic, making it easier to separate impurities through magnetic separation. Hematite (Fe2O3) has a slightly lower theoretical iron content (70%) and is non-magnetic, requiring different beneficiation methods.

What are the key drivers for the growth of the magnetite iron ore market?

Key drivers include the consistent global demand for high-quality steel, increasing adoption of advanced beneficiation technologies, and the steel industry's shift towards decarbonization, which favors high-grade magnetite concentrates for processes like direct reduced iron (DRI).

What role does technology play in magnetite iron ore mining and processing?

Technology plays a crucial role in optimizing every stage, from exploration (using AI for resource modeling) to extraction (automation, IoT) and beneficiation (advanced magnetic separation, grinding). These technologies enhance efficiency, reduce costs, improve safety, and enable the production of higher-grade concentrates, aligning with modern industrial demands.

Which regions are key players in the magnetite iron ore market?

The Asia Pacific region, particularly China and India, dominates consumption due to vast steel production. Other significant regions include North America and Europe, driven by stable industrial demand and green steel initiatives, and emerging regions like Latin America and MEA with substantial reserves and growing processing capacities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted