Plasterboard Liner Market

Plasterboard Liner Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702215 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Plasterboard Liner Market Size

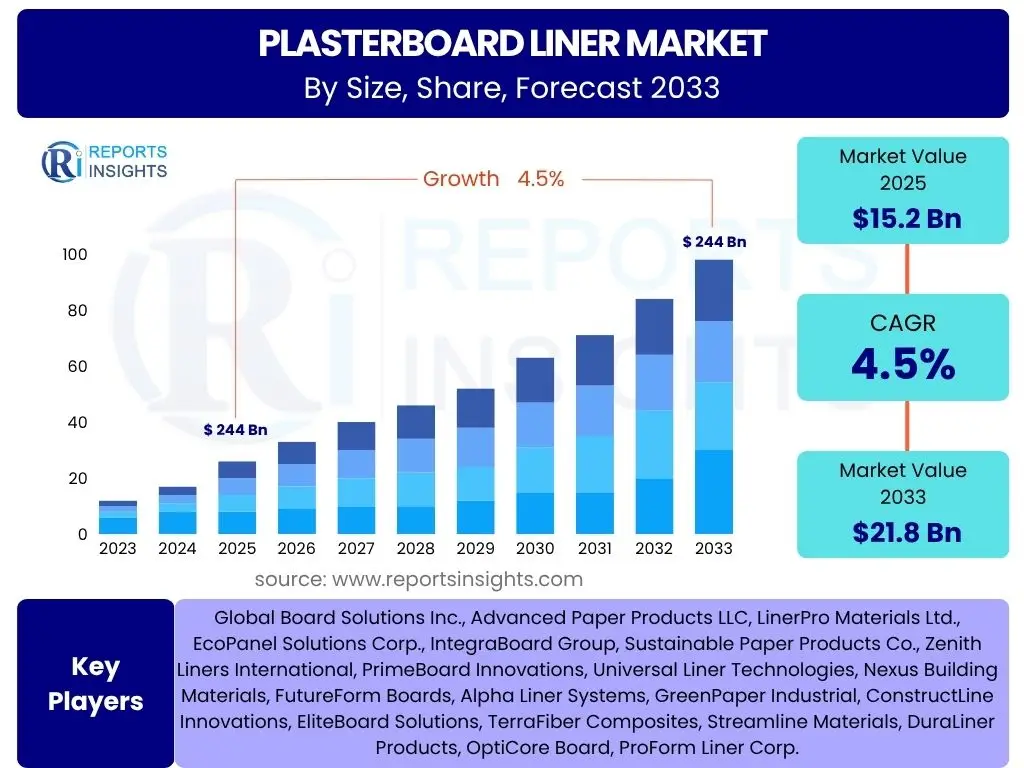

According to Reports Insights Consulting Pvt Ltd, The Plasterboard Liner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 15.2 billion in 2025 and is projected to reach USD 21.8 billion by the end of the forecast period in 2033.

Key Plasterboard Liner Market Trends & Insights

The global plasterboard liner market is significantly influenced by an evolving landscape of construction practices, material innovation, and sustainability imperatives. Common inquiries from stakeholders frequently center on the adoption of eco-friendly materials, the impact of digitalization on manufacturing and supply chains, and the increasing demand for high-performance building components. These questions highlight a market that is not only expanding in volume but also undergoing a qualitative transformation driven by technological advancements and environmental consciousness. The shift towards lightweight, durable, and fire-resistant construction materials, often integrating recycled content, represents a pivotal trend. Furthermore, the push for energy-efficient buildings globally is directly contributing to the demand for advanced plasterboard liner solutions that can contribute to improved insulation and overall building performance.

Another prominent trend is the growing interest in modular and prefabricated construction techniques, which require precise and consistent building materials like plasterboard liners. This method reduces construction time and waste, aligning with both economic and environmental objectives. Alongside this, the integration of smart building technologies is fostering a demand for plasterboard liners that can accommodate complex installations and contribute to healthier indoor environments, such as those with improved acoustic properties or moisture resistance. The globalization of building codes and standards also plays a role, pushing manufacturers to develop products that meet diverse regulatory requirements, ensuring market accessibility and driving product innovation.

- Increased adoption of sustainable and recycled content in liners.

- Rising demand for high-performance properties: moisture, fire, and mold resistance.

- Growth of modular and off-site construction methods.

- Digitization of manufacturing and supply chain processes.

- Emphasis on enhancing indoor air quality and acoustic performance.

- Expansion into emerging economies due to rapid urbanization.

AI Impact Analysis on Plasterboard Liner

The integration of Artificial Intelligence (AI) into the plasterboard liner industry is a topic of increasing discussion among market participants, with common user questions revolving around its potential to revolutionize manufacturing efficiency, optimize supply chain logistics, and enhance product development. Stakeholders are particularly interested in how AI can lead to more precise quality control, reduce waste in production, and provide predictive maintenance for machinery, thereby minimizing downtime and operational costs. The analytical capabilities of AI offer the potential for profound improvements in decision-making, from forecasting market demand with greater accuracy to identifying optimal raw material sourcing strategies. This technological evolution promises to make the production of plasterboard liners more agile and responsive to market fluctuations.

Beyond manufacturing, AI's influence extends to the design and application phases of plasterboard liners. AI-powered design tools can help architects and engineers select the most appropriate liner types for specific building performance requirements, integrating data on acoustics, thermal properties, and fire resistance. Furthermore, in the realm of supply chain management, AI algorithms can optimize inventory levels, route planning, and logistics, ensuring timely delivery of materials to construction sites and reducing transportation carbon footprints. While the full scope of AI's impact is still unfolding, its potential to drive efficiency, innovation, and sustainability within the plasterboard liner market is becoming increasingly evident, positioning it as a key technological enabler for future growth and competitive advantage.

- Optimized manufacturing processes and quality control through AI-driven analytics.

- Enhanced supply chain efficiency and predictive logistics management.

- Accelerated product innovation and material composition refinement.

- Predictive maintenance for production machinery reducing downtime.

- Improved demand forecasting and inventory management.

Key Takeaways Plasterboard Liner Market Size & Forecast

The comprehensive analysis of the Plasterboard Liner market size and forecast reveals a trajectory of steady growth, driven by sustained global construction activities and increasing demand for advanced building materials. Key questions from users often focus on the longevity of this growth, the primary geographical contributors, and the underlying factors sustaining market expansion. The market's projected value reaching USD 21.8 billion by 2033 underscores its resilience and critical role within the broader construction sector. This growth is not merely volumetric but also qualitative, reflecting a market that is adapting to evolving industry standards, environmental concerns, and technological advancements. Understanding these dynamics is crucial for strategic planning and investment decisions across the value chain.

A significant takeaway is the dual influence of traditional construction growth in emerging economies and the refurbishment/renovation wave in developed regions. While urbanization and infrastructure development in Asia Pacific and Latin America fuel demand for new installations, stricter building codes and a focus on energy efficiency in North America and Europe drive the demand for upgraded and higher-performance liners in existing structures. Furthermore, the market's stability is reinforced by the essential nature of plasterboard in modern building practices, making its liner component indispensable. These insights provide a clear picture of a market poised for continued expansion, characterized by a blend of established demand and innovative adaptation to future building requirements.

- Stable growth projected, reaching USD 21.8 billion by 2033.

- Robust demand from both new construction and renovation sectors.

- Asia Pacific and Europe are key growth regions.

- Innovation in sustainable and high-performance liners drives value.

- Market resilience linked to essential role of plasterboard in building.

Plasterboard Liner Market Drivers Analysis

The plasterboard liner market is fundamentally driven by several powerful macroeconomic and industry-specific factors that collectively contribute to its consistent expansion. Global population growth, coupled with increasing urbanization, necessitates continuous development in residential, commercial, and industrial infrastructure, directly translating into higher demand for plasterboard and its essential liner component. Additionally, the rising standards for building safety, efficiency, and sustainability worldwide are compelling construction stakeholders to adopt high-performance building materials, including advanced plasterboard liners that offer enhanced fire resistance, moisture protection, and acoustic insulation. These regulatory and market-driven demands create a sustained need for quality liner products across diverse applications.

Technological advancements in manufacturing processes, leading to more cost-effective and environmentally friendly production of plasterboard liners, also act as a significant driver. Innovations in material science, such as the development of liners with higher recycled content or improved barrier properties, appeal to a broader market segment and support the green building movement. Furthermore, the increasing disposable income in developing economies fuels consumer spending on housing and infrastructure improvements, indirectly boosting the construction sector and, consequently, the plasterboard liner market. The cumulative effect of these drivers creates a positive and dynamic growth environment for the industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Construction Activities | +1.2% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Increasing Demand for Green Buildings | +0.8% | Europe, North America | 2027-2033 |

| Growth in Renovation & Remodeling Projects | +0.7% | North America, Europe | 2025-2030 |

| Advancements in Plasterboard Technology | +0.6% | Global | 2026-2033 |

| Stricter Building Codes & Fire Safety Regulations | +0.5% | Global | 2025-2032 |

Plasterboard Liner Market Restraints Analysis

Despite its robust growth potential, the plasterboard liner market faces several significant restraints that could impede its trajectory. One primary concern is the volatility in the prices of raw materials, particularly paper pulp and recycled paper, which are key components of many liner types. Fluctuations in these commodity prices directly impact manufacturing costs and, consequently, the final product's competitiveness. Such unpredictability can make long-term planning challenging for manufacturers and may lead to price increases for consumers, potentially dampening demand. Additionally, environmental regulations concerning deforestation and sustainable sourcing practices for paper products could restrict the supply of virgin pulp, pushing manufacturers towards more expensive recycled alternatives or limiting overall production capacity.

Another notable restraint is the competition from alternative building materials, such as wood panels, fiber cement boards, and concrete blocks, especially in regions where traditional construction methods remain prevalent or where these alternatives offer a cost advantage. While plasterboard offers unique benefits, the availability and lower cost of substitutes in specific applications or geographical markets can limit its market penetration. Furthermore, economic downturns or recessions can significantly slow down construction activities, leading to a temporary decline in demand for building materials including plasterboard liners. The labor-intensive nature of some aspects of plasterboard installation, particularly in regions with skilled labor shortages, can also present a hurdle to broader adoption, impacting the market's overall growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.9% | Global | 2025-2029 |

| Competition from Alternative Building Materials | -0.7% | Emerging Markets | 2025-2033 |

| Environmental Regulations & Sourcing Constraints | -0.6% | Europe, North America | 2026-2031 |

| Economic Downturns & Reduced Construction Spending | -0.5% | Global, Cyclical | Short-term (1-3 years) |

| Supply Chain Disruptions | -0.4% | Global | 2025-2027 |

Plasterboard Liner Market Opportunities Analysis

The plasterboard liner market is ripe with opportunities that can propel its growth beyond current projections. A significant avenue for expansion lies in the increasing global emphasis on sustainable and green building practices. As governments and private sectors worldwide commit to reducing carbon footprints and enhancing energy efficiency in buildings, the demand for plasterboard liners made from recycled content, or those that contribute to a building's overall sustainability rating, is set to surge. This trend provides manufacturers with an opportunity to innovate and market eco-friendly product lines, differentiating themselves in a competitive landscape and appealing to environmentally conscious consumers and developers. Investing in research and development for biodegradable or compostable liner materials could open entirely new market segments.

Emerging markets, particularly in Asia Pacific, Latin America, and Africa, present vast untapped potential. Rapid urbanization, increasing disposable incomes, and the ongoing development of modern infrastructure in these regions are driving substantial demand for new residential and commercial constructions. Manufacturers can capitalize on these burgeoning markets by establishing local production facilities, adapting products to regional needs and cost structures, and developing robust distribution networks. Furthermore, the continuous evolution of building codes and the demand for specialized performance characteristics, such as enhanced sound insulation, extreme moisture resistance, or superior fire ratings, create opportunities for product diversification and premiumization. Developing liners for niche applications, such as healthcare facilities, data centers, or high-rise buildings, can also unlock significant value and growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-Friendly & Sustainable Liners | +1.0% | Global | 2026-2033 |

| Expansion into Untapped Emerging Markets | +0.9% | Asia Pacific, Africa | 2025-2033 |

| Technological Innovations for Enhanced Performance | +0.8% | Global | 2027-2033 |

| Growth in Modular & Prefabricated Construction | +0.7% | North America, Europe | 2025-2030 |

| Diversification into Niche Applications | +0.6% | Global | 2028-2033 |

Plasterboard Liner Market Challenges Impact Analysis

The plasterboard liner market navigates several persistent challenges that require strategic responses from industry players. One significant challenge is the ongoing pressure to manage raw material costs, which are subject to global commodity market fluctuations and geopolitical events. The availability and stable pricing of essential inputs like paper pulp, gypsum, and chemical additives can be unpredictable, leading to fluctuating production costs and impacting profit margins. This necessitates robust supply chain management, including diversified sourcing strategies and potential vertical integration. Furthermore, increasingly stringent environmental regulations around waste disposal, emissions, and water usage in manufacturing processes present compliance challenges, often requiring significant capital investment in new technologies and processes to meet evolving standards.

Another crucial challenge is the intense competition within the mature segments of the plasterboard market. This competitive landscape drives down prices, making it difficult for manufacturers to maintain healthy profit margins unless they differentiate through innovation, superior quality, or specialized products. Counterfeit products or those that do not meet quality standards also pose a risk, undermining market integrity and consumer trust. Additionally, the construction industry's susceptibility to economic cycles means that demand for plasterboard liners can be highly volatile, influenced by interest rates, housing market bubbles, and overall economic health. Navigating these economic fluctuations requires agile business models and diversified market penetration strategies to mitigate risks and sustain growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Cost Volatility | -0.8% | Global | 2025-2030 |

| Stringent Environmental & Regulatory Compliance | -0.7% | Europe, North America | 2026-2033 |

| Intense Market Competition & Pricing Pressures | -0.6% | Global (Mature Markets) | 2025-2033 |

| Impact of Economic Downturns on Construction | -0.5% | Global, Cyclical | Short-term (1-3 years) |

| Supply Chain Vulnerabilities | -0.4% | Global | 2025-2028 |

Plasterboard Liner Market - Updated Report Scope

This report provides a comprehensive analysis of the global Plasterboard Liner market, offering detailed insights into market size, growth trends, drivers, restraints, opportunities, and challenges across various segments and regions. It aims to equip stakeholders with critical data for strategic decision-making, covering historical performance, current market dynamics, and future projections. The scope encompasses an in-depth review of technological advancements, competitive landscape, and regulatory impacts shaping the industry. Understanding these elements is essential for anticipating market shifts and identifying lucrative investment avenues within the evolving construction materials sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 21.8 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Board Solutions Inc., Advanced Paper Products LLC, LinerPro Materials Ltd., EcoPanel Solutions Corp., IntegraBoard Group, Sustainable Paper Products Co., Zenith Liners International, PrimeBoard Innovations, Universal Liner Technologies, Nexus Building Materials, FutureForm Boards, Alpha Liner Systems, GreenPaper Industrial, ConstructLine Innovations, EliteBoard Solutions, TerraFiber Composites, Streamline Materials, DuraLiner Products, OptiCore Board, ProForm Liner Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plasterboard liner market is segmented to provide granular insights into its diverse components, allowing for a comprehensive understanding of market dynamics and targeted strategic planning. Segmentation by material type offers a view into the prevalent raw materials used, such as recycled paper, virgin pulp, and fiberglass, each presenting distinct properties and environmental implications. The finish segment differentiates between coated and uncoated liners, which affects their performance characteristics like moisture resistance and printability. Understanding these material and finish distinctions is crucial for manufacturers to tailor their production and for consumers to select appropriate products for specific applications, influencing market share and technological advancements across these categories.

Further segmentation by application areas, including walls, ceilings, partitions, and specialty uses, highlights the varied demand patterns across different construction components. The end-use vertical segmentation, comprising residential, commercial, industrial, and institutional sectors, provides an understanding of where the bulk of demand originates and how different construction types impact liner requirements. For instance, commercial buildings might prioritize fire resistance and sound insulation, while residential projects might focus on cost-effectiveness and ease of installation. This detailed segmentation enables market players to identify high-growth niches, allocate resources effectively, and develop products that precisely meet the needs of specific market segments, ultimately driving innovation and market penetration.

- By Material Type:

- Recycled Paper

- Virgin Pulp

- Fiberglass

- Others

- By Finish:

- Coated

- Uncoated

- By Application:

- Walls

- Ceilings

- Partitions

- Specialty Applications (e.g., shafts, curved surfaces)

- By End-Use Vertical:

- Residential

- Commercial

- Industrial

- Institutional

Regional Highlights

- North America: Characterized by a mature construction market with a strong emphasis on renovation, remodeling, and sustainable building practices. Demand for high-performance and specialty liners (e.g., mold-resistant, fire-rated) is prominent, driven by stringent building codes and a focus on indoor air quality. The region also sees significant adoption of modular construction techniques, favoring consistent and quality liner supplies.

- Europe: A leader in green building initiatives and energy efficiency, driving demand for eco-friendly and high-insulation plasterboard liners. Strict environmental regulations and a strong circular economy focus encourage the use of recycled content. Renovation of older buildings and investment in public infrastructure are key growth drivers, particularly in Western and Northern Europe.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, massive infrastructure development, and increasing disposable incomes in countries like China, India, and Southeast Asian nations. While price sensitivity remains, there's a growing shift towards quality and performance, creating opportunities for advanced liner products. Residential and commercial construction booms are the primary catalysts.

- Latin America: Experiencing steady growth in construction due to expanding middle-class populations and investment in affordable housing and infrastructure projects. The market is developing, with a growing awareness of modern construction materials and techniques. Local manufacturing and supply chain development are crucial for market penetration.

- Middle East and Africa (MEA): Marked by significant investments in mega-projects, commercial developments, and hospitality sectors, particularly in the GCC countries. Demand for fire-resistant and high-durability liners is high due to extreme climatic conditions and stringent safety regulations. African markets present long-term growth potential driven by urbanization and industrialization, though economic and political stability can influence growth rates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plasterboard Liner Market.- Global Board Solutions Inc.

- Advanced Paper Products LLC

- LinerPro Materials Ltd.

- EcoPanel Solutions Corp.

- IntegraBoard Group

- Sustainable Paper Products Co.

- Zenith Liners International

- PrimeBoard Innovations

- Universal Liner Technologies

- Nexus Building Materials

- FutureForm Boards

- Alpha Liner Systems

- GreenPaper Industrial

- ConstructLine Innovations

- EliteBoard Solutions

- TerraFiber Composites

- Streamline Materials

- DuraLiner Products

- OptiCore Board

- ProForm Liner Corp.

Frequently Asked Questions

Analyze common user questions about the Plasterboard Liner market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Plasterboard Liner Market?

The Plasterboard Liner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, reaching an estimated value of USD 21.8 billion by the end of the forecast period.

What are the key factors driving the Plasterboard Liner Market?

Key drivers include rapid urbanization, increasing construction activities globally, rising demand for green and sustainable buildings, growth in renovation projects, and advancements in plasterboard technology leading to enhanced performance characteristics.

How is Artificial Intelligence impacting the Plasterboard Liner industry?

AI is impacting the industry by optimizing manufacturing processes for efficiency and quality control, enhancing supply chain logistics, enabling predictive maintenance, and accelerating product innovation and material refinement for future applications.

Which regions are expected to show significant growth in the Plasterboard Liner Market?

Asia Pacific is anticipated to be the fastest-growing region due to extensive urbanization and infrastructure development, while North America and Europe will see continued demand driven by renovation activities and green building initiatives.

What are the main challenges faced by the Plasterboard Liner Market?

Major challenges include the volatility of raw material prices, intense market competition leading to pricing pressures, stringent environmental and regulatory compliance requirements, and the susceptibility of the construction industry to economic downturns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted