Metal Mill Liner Market

Metal Mill Liner Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702095 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

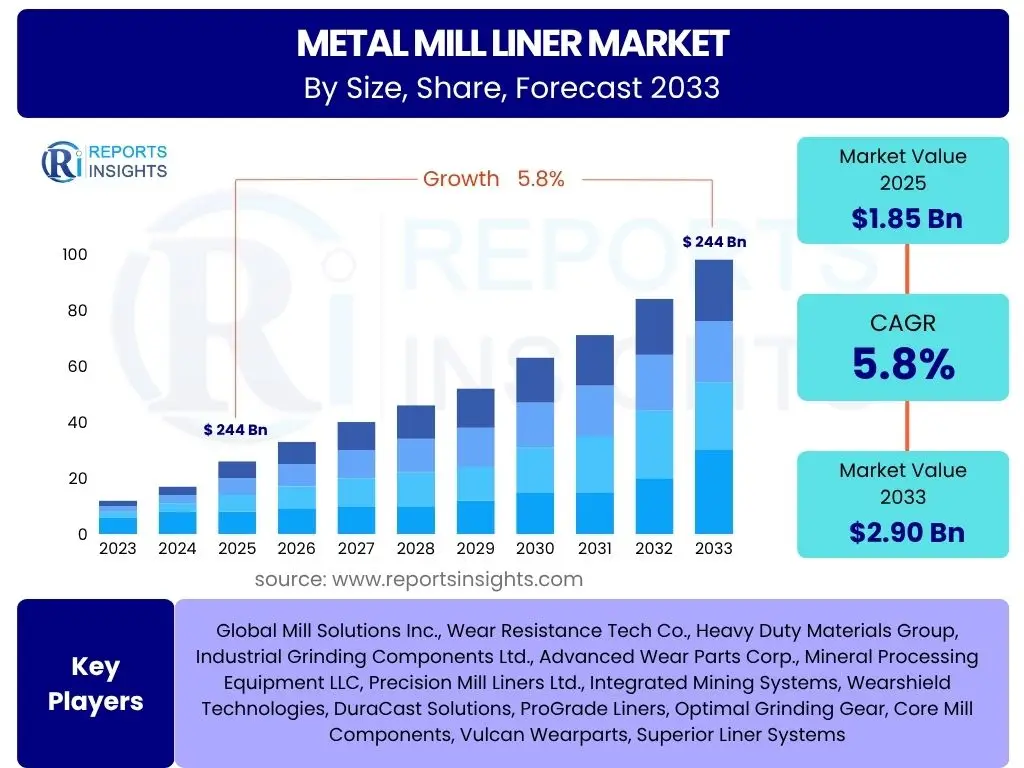

Metal Mill Liner Market Size

According to Reports Insights Consulting Pvt Ltd, The Metal Mill Liner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 2.90 Billion by the end of the forecast period in 2033.

The consistent expansion is primarily driven by robust demand from the global mining industry, which relies heavily on efficient grinding processes for ore extraction. Furthermore, the burgeoning construction sector, particularly in developing economies, contributes significantly to the demand for metal mill liners used in cement and aggregate production.

Key Metal Mill Liner Market Trends & Insights

The Metal Mill Liner market is undergoing significant transformations driven by a confluence of technological advancements, sustainability initiatives, and evolving operational demands from end-use industries. Users frequently inquire about the latest innovations in material science, the adoption of digital technologies for performance monitoring, and the industry's response to environmental regulations. Key insights reveal a clear shift towards high-performance, longer-lasting materials and solutions that enhance operational efficiency and reduce total cost of ownership.

A prominent trend involves the increasing demand for customized liner solutions tailored to specific mill types, ore characteristics, and grinding applications. This customization allows for optimized grinding efficiency, reduced energy consumption, and extended liner lifespan, directly addressing critical pain points for operators. The focus on developing advanced material compositions, such as improved chrome-moly alloys, high-chromium white irons, and composite materials, is paramount in enhancing wear resistance and impact strength, crucial for abrasive grinding environments.

Furthermore, the market is witnessing a growing emphasis on smart liners integrated with sensors for real-time wear monitoring and predictive maintenance. This digitalization facilitates proactive replacement planning, minimizes unscheduled downtime, and contributes to overall operational excellence. The trend towards sustainable practices, including the development of recyclable liner materials and optimizing the lifecycle of liners to reduce waste, is also gaining traction, aligning with broader industry environmental goals.

- Increased adoption of high-performance alloy materials for extended liner lifespan.

- Growing demand for customized liner geometries and material compositions based on specific grinding applications.

- Integration of sensor technologies for real-time wear monitoring and predictive maintenance.

- Emphasis on sustainable and recyclable liner materials to reduce environmental impact.

- Rising focus on total cost of ownership (TCO) rather than just initial purchase price.

- Digitization of mill operations influencing liner selection and management.

AI Impact Analysis on Metal Mill Liner

Common user questions regarding AI's impact on Metal Mill Liner solutions center around its potential to revolutionize predictive maintenance, optimize material design, and enhance overall operational efficiency. There is significant interest in how AI can extend liner life, minimize unexpected failures, and contribute to more sustainable grinding processes. Users are also keen to understand the practical applications of AI in material selection and manufacturing, as well as the challenges associated with implementing such advanced technologies in traditional industrial settings.

Artificial intelligence is set to profoundly influence the Metal Mill Liner market, primarily through advanced analytics and machine learning applications. AI-powered algorithms can process vast amounts of data from mill operations, including vibration, temperature, acoustic emissions, and motor current, to predict liner wear rates with high accuracy. This predictive capability enables operators to schedule liner replacements precisely, thereby minimizing unscheduled downtime, optimizing maintenance schedules, and maximizing the utilization of grinding assets.

Beyond predictive maintenance, AI also holds immense potential in the design and material development phase of mill liners. Machine learning models can analyze material properties, wear patterns, and operational conditions to recommend optimal alloy compositions and liner geometries for specific applications, accelerating research and development cycles. Furthermore, AI can contribute to process optimization within grinding circuits by analyzing grinding performance data and suggesting adjustments to parameters such as feed rate, mill speed, and slurry density to maximize efficiency and further extend liner life. This holistic impact promises significant improvements in productivity and cost-effectiveness across the mineral processing and cement industries.

- Predictive maintenance through AI-driven wear pattern analysis, extending liner lifespan and reducing unplanned downtime.

- Optimized material design and selection using machine learning to simulate performance under various operational stresses.

- Enhanced operational efficiency by AI-guided adjustments to grinding parameters (e.g., feed rate, mill speed) based on real-time data.

- Improved inventory management and supply chain optimization for spare parts through demand forecasting.

- Quality control and defect detection during manufacturing processes leveraging computer vision and AI.

Key Takeaways Metal Mill Liner Market Size & Forecast

Analysis of common user questions regarding the Metal Mill Liner market size and forecast reveals a keen interest in understanding the primary growth catalysts, the longevity of market expansion, and the underlying factors contributing to value generation. Users frequently inquire about the roles of industrial growth, technological innovation, and sustainability efforts in shaping the market's trajectory. The insights underscore a resilient market driven by fundamental industrial needs, projected to exhibit steady growth despite potential economic fluctuations, propelled by advancements in material science and operational efficiency.

The Metal Mill Liner market is poised for consistent growth, primarily fueled by sustained demand from the global mining sector and the expanding infrastructure development initiatives, particularly in emerging economies. The forecast indicates that while traditional applications will remain foundational, significant value creation will stem from the adoption of advanced, high-performance liners that offer superior wear resistance and extended service life. This shift reflects an industry-wide focus on optimizing operational efficiency and reducing total cost of ownership, rather than merely focusing on initial component cost.

Furthermore, technological advancements, including the integration of smart monitoring systems and the development of specialized alloy compositions, are critical enablers of this growth. These innovations allow for more precise maintenance scheduling, reduced downtime, and improved grinding performance, which are highly valued by end-users. The market's resilience is also supported by the ongoing need for replacement parts in existing mill installations, ensuring a continuous revenue stream irrespective of new project developments, cementing its essential role in heavy industrial processes.

- The market is on a steady growth trajectory, driven by core industrial demands from mining, cement, and construction sectors.

- Technological advancements in material science and smart monitoring systems are crucial for future market expansion.

- Emphasis on total cost of ownership and operational efficiency is driving demand for premium, long-lasting liners.

- Emerging economies present significant growth opportunities due to rapid industrialization and infrastructure development.

- Replacement demand for existing mill installations ensures market stability and continuous revenue streams.

- Sustainability initiatives are increasingly influencing material selection and manufacturing processes.

Metal Mill Liner Market Drivers Analysis

The Metal Mill Liner market is propelled by a multitude of factors centered on global industrial growth, technological advancements, and the imperative for operational efficiency. Persistent demand from the mining sector, coupled with robust growth in construction and infrastructure development worldwide, necessitates a consistent supply of durable and high-performance grinding components. Additionally, the continuous drive to minimize downtime and enhance productivity across various industries is fostering the adoption of advanced liner solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Mining Activities & Mineral Processing | +1.5% | APAC, Latin America, Africa, North America | Short to Long Term (2025-2033) |

| Expansion of Construction & Infrastructure Projects | +1.2% | APAC, Middle East, Africa, Eastern Europe | Medium to Long Term (2026-2033) |

| Increasing Focus on Operational Efficiency & Productivity | +0.8% | Global, especially developed economies | Short to Medium Term (2025-2029) |

| Technological Advancements in Liner Materials & Design | +0.7% | Global | Medium to Long Term (2027-2033) |

| Aging Mill Infrastructure Requiring Replacements | +0.5% | North America, Europe, China | Continuous (2025-2033) |

Metal Mill Liner Market Restraints Analysis

Despite significant growth drivers, the Metal Mill Liner market faces several restraints that could impede its expansion. These include the volatility of commodity prices, which directly impacts investment in mining and mineral processing, as well as stringent environmental regulations that can increase operational costs and complexity for end-users. Furthermore, the high capital expenditure associated with new mill installations or extensive upgrades can deter immediate market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Commodity Prices Impacting Mining Investment | -0.9% | Global | Short to Medium Term (2025-2028) |

| High Capital Expenditure for New Mill Installations | -0.6% | Global | Medium Term (2026-2030) |

| Stringent Environmental & Safety Regulations | -0.4% | Europe, North America, Australia | Long Term (2025-2033) |

| Competition from Alternative Grinding Technologies | -0.3% | Global | Medium to Long Term (2027-2033) |

Metal Mill Liner Market Opportunities Analysis

The Metal Mill Liner market is presented with compelling opportunities for growth, particularly stemming from the rapid industrialization and urbanization in emerging economies. These regions are undertaking massive infrastructure projects and expanding their mining operations, creating substantial demand for grinding media. Furthermore, ongoing technological advancements in material science and manufacturing processes offer avenues for developing superior, more efficient, and environmentally friendly liner solutions, opening new market niches and increasing adoption rates.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Economies' Infrastructure Development | +1.0% | APAC, Africa, Latin America | Long Term (2026-2033) |

| Technological Innovations in Advanced Composites & Ceramics | +0.8% | Global | Medium to Long Term (2027-2033) |

| Increased Adoption of Smart Liners & IoT Integration | +0.7% | Developed Economies | Medium Term (2026-2030) |

| Focus on Sustainable Mining Practices & Circular Economy | +0.5% | Europe, North America, Australia | Long Term (2028-2033) |

Metal Mill Liner Market Challenges Impact Analysis

Challenges within the Metal Mill Liner market primarily revolve around intense market competition and pricing pressures, which can erode profit margins for manufacturers. The inherent wear and tear properties of liners necessitate frequent replacement, leading to high operational costs for end-users and continuous demand for cost-effective, yet durable, solutions. Additionally, complexities in the global supply chain, including logistics for heavy components and fluctuations in raw material costs, pose significant hurdles for consistent production and delivery.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Price Pressure | -0.8% | Global | Continuous (2025-2033) |

| Fluctuations in Raw Material Costs | -0.7% | Global | Short to Medium Term (2025-2028) |

| Complex Logistics & Supply Chain Management for Heavy Components | -0.5% | Global | Continuous (2025-2033) |

| Need for Skilled Labor in Installation & Maintenance | -0.3% | Global, particularly remote mining areas | Long Term (2025-2033) |

Metal Mill Liner Market - Updated Report Scope

This report provides a comprehensive analysis of the Metal Mill Liner market, encompassing market size estimations, growth forecasts, key trends, and an in-depth segmentation analysis across various parameters. It offers critical insights into market drivers, restraints, opportunities, and challenges, along with a detailed regional outlook and profiles of key industry players, providing a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.90 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Mill Solutions Inc., Wear Resistance Tech Co., Heavy Duty Materials Group, Industrial Grinding Components Ltd., Advanced Wear Parts Corp., Mineral Processing Equipment LLC, Precision Mill Liners Ltd., Integrated Mining Systems, Wearshield Technologies, DuraCast Solutions, ProGrade Liners, Optimal Grinding Gear, Core Mill Components, Vulcan Wearparts, Superior Liner Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metal Mill Liner market is extensively segmented by material type, mill type, application, and end-use industry, each segment playing a crucial role in defining market dynamics and growth opportunities. This granular segmentation allows for a detailed understanding of specific product demands, technological preferences, and regional consumption patterns. The material segment, for instance, highlights the increasing preference for high-performance alloys and composite materials that offer superior wear resistance and extended lifespan, catering to the rigorous demands of grinding environments.

Further analysis by mill type reveals distinct requirements based on the grinding process, with ball mills and SAG (Semi-Autogenous Grinding) mills dominating the market due to their widespread use in mining and cement applications. Each mill type necessitates unique liner designs and material specifications to optimize grinding efficiency and minimize maintenance. The application segment underscores the pervasive use of mill liners across critical heavy industries, with mining and metallurgy accounting for the largest share, followed by cement production and aggregates, reflecting their fundamental role in industrial processes.

The end-use industry segmentation further refines the market understanding, indicating that the mining industry remains the largest consumer due to the continuous need for ore comminution globally. However, the construction sector, propelled by rapid urbanization and infrastructure development, is rapidly increasing its demand for liners in cement and aggregate production. This multi-faceted segmentation provides a comprehensive framework for assessing market opportunities and challenges across diverse industrial landscapes.

- By Material: Manganese Steel, Chrome Moly Steel, High Chrome Iron, Rubber, Composites, Others.

- By Mill Type: Ball Mills, SAG Mills, AG Mills, Rod Mills, Vertical Roller Mills, Others.

- By Application: Mining & Metallurgy (Gold, Copper, Iron Ore, Other Mineral Processing), Cement Production, Aggregates & Construction, Power Generation (Coal Grinding), Chemical Processing, Other Industrial Applications.

- By End-Use Industry: Mining Industry, Cement Industry, Power Industry, Construction Industry, Chemical Industry, Other Industrial Sectors.

Regional Highlights

Geographically, the Metal Mill Liner market exhibits diverse dynamics shaped by industrial activity, resource availability, and economic development across key regions. Each region presents unique opportunities and challenges for market participants, driven by factors such as infrastructure spending, mining investments, and regulatory landscapes. Understanding these regional nuances is crucial for strategic market penetration and investment decisions. The Asia Pacific region, for instance, is projected to dominate the market, primarily due to its robust industrial growth and extensive mining operations.

Asia Pacific (APAC) stands out as the largest and fastest-growing market, propelled by rapid industrialization, massive infrastructure projects in countries like China and India, and significant mining activities across Australia, Indonesia, and Southeast Asia. The escalating demand for construction materials and minerals in this region fuels the consistent need for mill liners. North America and Europe represent mature markets characterized by a strong emphasis on advanced materials, operational efficiency, and the replacement/upgrade of aging mill infrastructure. These regions also exhibit a growing trend towards sustainable mining practices and the adoption of smart technologies in mill operations.

Latin America is a significant market driven by its rich mineral resources and extensive mining operations, particularly in countries like Chile, Brazil, and Peru, which are major producers of copper, iron ore, and other vital minerals. The Middle East and Africa (MEA) region is experiencing growth due to increasing investments in mining exploration and processing, alongside infrastructure development projects. These regions, while smaller in market size compared to APAC, offer substantial growth potential as their industrial bases continue to expand and modernize, necessitating reliable grinding solutions.

- Asia Pacific (APAC): Dominant and fastest-growing region due to extensive mining, infrastructure development, and industrialization in China, India, and Southeast Asia.

- North America: Mature market focused on technological advancements, operational efficiency, and replacement demand for existing mills in the U.S. and Canada.

- Europe: Stable market with emphasis on high-performance materials, environmental regulations, and advanced manufacturing technologies.

- Latin America: Significant growth driven by rich mineral resources and large-scale mining operations, especially in Chile, Brazil, and Peru.

- Middle East & Africa (MEA): Emerging market with increasing investments in mining and infrastructure, particularly in countries with significant mineral reserves.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metal Mill Liner Market.- Global Mill Solutions Inc.

- Wear Resistance Tech Co.

- Heavy Duty Materials Group

- Industrial Grinding Components Ltd.

- Advanced Wear Parts Corp.

- Mineral Processing Equipment LLC

- Precision Mill Liners Ltd.

- Integrated Mining Systems

- Wearshield Technologies

- DuraCast Solutions

- ProGrade Liners

- Optimal Grinding Gear

- Core Mill Components

- Vulcan Wearparts

- Superior Liner Systems

- Allied Grinding Solutions

- Innovate Castings Global

- Power Mill Systems

- Reliable Industrial Liners

- GrindForce Technologies

Frequently Asked Questions

Analyze common user questions about the Metal Mill Liner market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Metal Mill Liner and what is its primary function?

A metal mill liner is a protective wear component installed inside grinding mills (such as ball mills or SAG mills) to protect the shell from abrasive wear and to lift and agitate the grinding media (balls, rocks, or rods) and material for efficient comminution. Its primary function is to optimize grinding performance and extend the lifespan of the mill shell.

What are the main types of materials used for Metal Mill Liners?

Common materials include high-manganese steel, chrome-moly steel, high-chromium white iron, rubber, and various composites. The choice of material depends on the mill type, the abrasiveness of the material being ground, and the desired balance between wear resistance, impact strength, and cost.

Which industries are the primary consumers of Metal Mill Liners?

The primary consumers are industries involved in mineral processing and comminution, including mining and metallurgy (for grinding ores like gold, copper, iron), cement production, aggregates and construction, power generation (for coal grinding), and certain chemical processing applications.

How do technological advancements impact the Metal Mill Liner market?

Technological advancements are driving innovation in material science, leading to more durable and efficient liners. Furthermore, the integration of smart technologies like sensors for real-time wear monitoring and AI for predictive maintenance is significantly improving operational efficiency, reducing downtime, and extending liner service life.

What are the key factors driving the growth of the Metal Mill Liner market?

Key growth drivers include sustained global demand from the mining sector, rapid expansion of construction and infrastructure projects, the continuous industry focus on enhancing operational efficiency and productivity, and ongoing technological advancements in liner materials and design that offer superior performance and extended lifespan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted