Plaster Cast Market

Plaster Cast Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707351 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

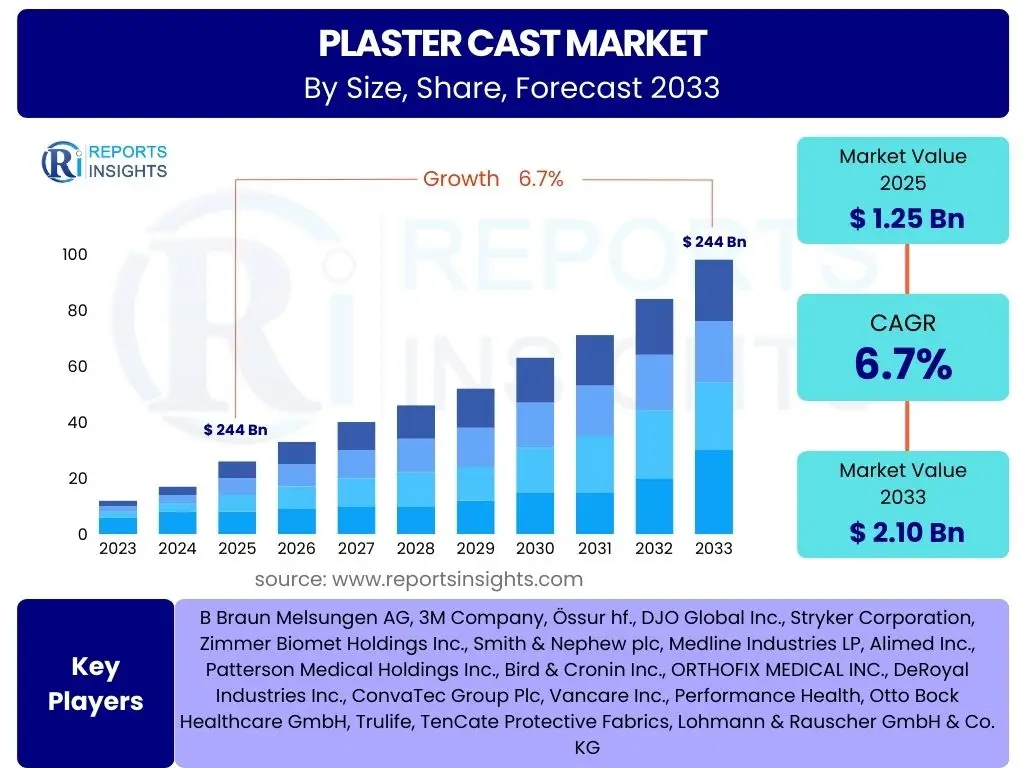

Plaster Cast Market Size

According to Reports Insights Consulting Pvt Ltd, The Plaster Cast Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.10 Billion by the end of the forecast period in 2033.

Key Plaster Cast Market Trends & Insights

The Plaster Cast market is currently undergoing a significant transformation driven by advancements in material science and increasing demand for patient comfort and improved healing outcomes. A notable shift is observed from traditional Plaster of Paris casts towards lightweight, durable, and water-resistant synthetic alternatives, primarily fiberglass. This transition is propelled by synthetic casts' superior properties, including faster setting times, enhanced ventilation, and reduced skin irritation. Furthermore, there is a growing emphasis on customizability and personalized patient care, leading to innovations in casting techniques and materials that can be molded more precisely to individual anatomy, improving therapeutic efficacy and patient compliance. The integration of digital technologies and 3D printing is also beginning to influence the development of next-generation casting solutions, promising even greater precision and patient-specific designs.

- Shift from Plaster of Paris to synthetic fiberglass casts due to enhanced durability and patient comfort.

- Rising adoption of lightweight and water-resistant casting materials improving hygiene and patient lifestyle.

- Increasing demand for customizable and patient-specific casting solutions for optimized fit and support.

- Development of smart casts incorporating sensors for monitoring healing progress and vital signs.

- Growing trend towards environmentally friendly and biodegradable casting materials.

- Integration of advanced imaging and 3D printing for highly precise and personalized cast fabrication.

AI Impact Analysis on Plaster Cast

Artificial Intelligence (AI) is poised to significantly impact the Plaster Cast market, primarily through enhanced diagnostic accuracy, personalized treatment planning, and advanced manufacturing processes. AI algorithms can analyze medical imaging such as X-rays and CT scans with greater precision than traditional methods, aiding in the accurate diagnosis of fractures and other orthopedic injuries, which in turn informs optimal casting strategies. Furthermore, AI can contribute to the design and customization of casts by predicting ideal pressure distribution, material requirements, and fit parameters based on individual patient data, potentially reducing complications like pressure sores or nerve impingement. This capability extends to generative design for 3D printed casts, where AI optimizes the geometry for strength, weight, and ventilation. While ethical considerations regarding data privacy and algorithmic bias remain pertinent, the potential for AI to streamline workflows and improve patient outcomes in orthopedic care is substantial.

- AI-powered diagnostic tools for precise fracture detection and severity assessment.

- Optimization of cast design and fit using AI for enhanced patient comfort and therapeutic effectiveness.

- Predictive analytics for identifying patients at risk of casting complications, enabling proactive interventions.

- Integration of AI in 3D printing processes for automated, customized cast fabrication.

- Development of AI-driven rehabilitation guidance systems for post-cast care and recovery.

Key Takeaways Plaster Cast Market Size & Forecast

The Plaster Cast market is poised for steady growth through 2033, fundamentally driven by an increasing global incidence of orthopedic injuries and the continuous evolution of casting materials and techniques. The forecast highlights a sustained shift towards synthetic materials, emphasizing innovation in patient comfort and functional recovery. This market growth is underpinned by advancements in healthcare infrastructure, particularly in emerging economies, alongside a rising awareness regarding effective fracture management. Stakeholders should recognize the market's trajectory towards more sophisticated, patient-centric solutions, encompassing not just the cast itself but also the diagnostic and rehabilitative ecosystems. The long-term outlook remains positive, with opportunities emerging from material science breakthroughs and the integration of digital health technologies, which promise to redefine traditional orthopedic care.

- Consistent market expansion projected, driven by orthopedic injury prevalence and material innovations.

- Dominance of synthetic casts anticipated due to superior performance and patient benefits.

- Significant growth opportunities in personalized casting solutions and advanced manufacturing.

- Emerging economies presenting robust market potential fueled by healthcare infrastructure development.

- Emphasis on holistic patient care, integrating casting with diagnostics and rehabilitation strategies.

Plaster Cast Market Drivers Analysis

The global Plaster Cast market is propelled by several robust drivers, primarily the escalating incidence of fractures and other orthopedic injuries worldwide. Factors such as a growing aging population, which is more susceptible to fragility fractures, and an increasing participation in sports and recreational activities leading to sports-related injuries, contribute significantly to the demand for effective immobilization solutions. Additionally, the continuous advancements in material science and orthopedic technology have led to the development of more comfortable, durable, and patient-friendly casting materials, encouraging their wider adoption over traditional methods and outdated practices. Improved healthcare infrastructure in developing regions also plays a crucial role by enhancing accessibility to orthopedic treatment and diagnostic services.

Furthermore, heightened awareness about proper fracture management and the critical role of immobilization in effective healing is driving demand across diverse patient demographics. Educational initiatives and better public health outreach programs contribute to patients seeking timely and appropriate medical interventions for musculoskeletal injuries. The transition towards outpatient and ambulatory care settings for minor orthopedic procedures also expands the application scope for plaster casts, making treatment more accessible and reducing hospital stays. These converging factors collectively foster a conducive environment for sustained market growth, emphasizing both the volume of injuries and the quality of available treatment options.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Fractures & Orthopedic Injuries | +1.8% | Global, particularly North America, Europe, APAC | Short to Mid-Term (2025-2030) |

| Rising Geriatric Population & Osteoporosis Prevalence | +1.5% | Global, especially Japan, Western Europe, North America | Mid to Long-Term (2027-2033) |

| Advancements in Casting Materials & Technologies | +1.2% | Developed Economies (US, Germany, UK) | Short to Mid-Term (2025-2029) |

| Growing Participation in Sports & Recreational Activities | +0.9% | North America, Europe, China, India | Short to Mid-Term (2025-2030) |

| Improving Healthcare Infrastructure in Emerging Economies | +0.8% | China, India, Brazil, Southeast Asia | Mid to Long-Term (2028-2033) |

Plaster Cast Market Restraints Analysis

Despite its growth trajectory, the Plaster Cast market faces several notable restraints that could temper its expansion. A primary concern is the potential for complications associated with traditional casting methods, such as skin irritation, itching, pressure sores, and even compartment syndrome if not applied correctly. These issues can lead to patient discomfort and dissatisfaction, sometimes necessitating re-application or alternative treatments. Additionally, the environmental impact of non-biodegradable synthetic casts, particularly fiberglass, is becoming an increasing concern for healthcare providers and environmental regulators, prompting a search for more sustainable alternatives which are not yet widely available or cost-competitive. The relative bulkiness and hygiene challenges associated with casts can also negatively impact patient quality of life and adherence to treatment.

Another significant restraint is the increasing availability and adoption of alternative non-invasive or minimally invasive orthopedic treatments. These include specialized braces, splints, and even advanced surgical techniques that may reduce the necessity for prolonged casting periods. The high cost associated with advanced synthetic casting materials and custom-fabricated casts, especially when compared to traditional Plaster of Paris, can also act as a barrier to adoption, particularly in price-sensitive markets or regions with limited healthcare budgets. Furthermore, the skill-intensive nature of proper cast application and removal, requiring trained professionals, can limit access to optimal treatment in areas with a shortage of skilled healthcare personnel, thereby constraining market reach. These factors collectively pose challenges to the market's unrestricted growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Potential for Skin Complications & Patient Discomfort | -1.0% | Global | Short to Mid-Term (2025-2030) |

| Availability of Alternative Treatment Modalities (Braces, Splints) | -0.8% | North America, Europe | Mid to Long-Term (2027-2033) |

| Environmental Concerns & Waste Management of Non-Biodegradable Materials | -0.7% | Developed Economies (EU, US) | Mid to Long-Term (2028-2033) |

| High Cost of Advanced Synthetic Casts & Customization | -0.6% | Emerging Markets, Public Healthcare Systems | Short to Mid-Term (2025-2030) |

| Need for Skilled Application & Removal by Professionals | -0.5% | Rural & Underdeveloped Regions | Ongoing |

Plaster Cast Market Opportunities Analysis

Significant opportunities exist within the Plaster Cast market, primarily stemming from the increasing focus on patient-centric care and technological innovation. The development of advanced, lightweight, and breathable materials, including those with antimicrobial properties, presents a substantial growth avenue by enhancing patient comfort and reducing complications. Furthermore, the integration of 3D printing technology offers unprecedented customization capabilities, allowing for the creation of truly patient-specific casts that provide optimal fit, support, and ventilation, thereby improving healing outcomes and patient satisfaction. This personalization trend is expected to drive demand for premium casting solutions, opening up new revenue streams for manufacturers and service providers. The burgeoning demand for non-invasive and minimally restrictive orthopedic solutions further pushes innovation, leading to specialized casts that facilitate early mobilization.

Beyond material and technological advancements, geographic expansion into emerging markets offers considerable potential. Countries in Asia Pacific, Latin America, and the Middle East & Africa are witnessing rapid improvements in healthcare infrastructure, an increase in disposable incomes, and a growing patient pool. These regions represent untapped markets where awareness and access to quality orthopedic care are improving, driving the adoption of modern casting solutions. Additionally, the potential for integrating smart features into casts, such as embedded sensors for monitoring temperature, moisture, or even bone healing progress, represents a futuristic opportunity. These 'smart casts' could provide real-time data to healthcare providers, enabling more precise interventions and personalized rehabilitation plans, thereby transforming the standard of orthopedic care and creating premium product categories.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced & Biodegradable Casting Materials | +1.5% | Global, particularly Europe, North America | Mid to Long-Term (2027-2033) |

| Adoption of 3D Printing for Customized Casts | +1.3% | Developed Economies (US, Germany, UK, Japan) | Short to Mid-Term (2025-2030) |

| Expansion into Emerging Markets with Improving Healthcare | +1.1% | China, India, Brazil, Southeast Asia | Mid to Long-Term (2028-2033) |

| Integration of Smart Technology (Sensors) in Casts | +0.9% | North America, Europe, South Korea | Long-Term (2030-2033) |

| Increasing Focus on Patient Comfort & Aesthetic Appeal | +0.7% | Global | Short to Mid-Term (2025-2029) |

Plaster Cast Market Challenges Impact Analysis

The Plaster Cast market faces several significant challenges that could impede its growth and evolution. A major challenge is the persistent issue of patient non-compliance, where individuals may prematurely remove or improperly care for their casts due to discomfort, itching, or hygiene issues, leading to suboptimal healing or re-injury. This challenge necessitates continuous patient education and the development of more comfortable, user-friendly casting solutions. Furthermore, managing the environmental footprint of discarded casts, particularly synthetic ones, presents a growing concern. The disposal of non-biodegradable materials contributes to landfill waste, pushing manufacturers and healthcare systems to seek more sustainable solutions, which often come with higher production costs or regulatory hurdles.

Another critical challenge is intense competition from non-casting alternatives and evolving orthopedic treatment paradigms. As surgical techniques become less invasive and rehabilitation protocols advance, the duration and necessity of traditional casting may diminish for certain injuries. The market also grapples with supply chain complexities, including raw material fluctuations and geopolitical disruptions, which can affect production costs and product availability. Regulatory approvals for new, innovative materials or smart casting technologies can be time-consuming and expensive, delaying market entry. Moreover, the need for specialized training for healthcare professionals to correctly apply and manage advanced casts creates a bottleneck in regions with limited access to such expertise. Addressing these multifaceted challenges will be crucial for sustainable market growth and innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Patient Non-Compliance & Potential Complications | -0.9% | Global | Short to Mid-Term (2025-2030) |

| Competition from Non-Casting Orthopedic Alternatives | -0.8% | North America, Europe | Mid to Long-Term (2027-2033) |

| Environmental Impact & Disposal of Synthetic Materials | -0.7% | Developed Economies | Mid to Long-Term (2028-2033) |

| High Development & Regulatory Costs for New Technologies | -0.6% | Global | Ongoing |

| Supply Chain Volatility & Raw Material Price Fluctuations | -0.5% | Global | Short-Term (2025-2027) |

Plaster Cast Market - Updated Report Scope

This report provides a comprehensive analysis of the global Plaster Cast market, offering insights into its current size, historical performance, and future growth projections. It delves into key market trends, significant drivers, restraining factors, emerging opportunities, and inherent challenges impacting the industry. The scope encompasses detailed segmentation analysis by material, application, end-user, and product type, alongside a thorough regional assessment. The report also profiles leading market players, providing a holistic view for stakeholders seeking strategic insights into this evolving healthcare segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.10 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | B Braun Melsungen AG, 3M Company, Össur hf., DJO Global Inc., Stryker Corporation, Zimmer Biomet Holdings Inc., Smith & Nephew plc, Medline Industries LP, Alimed Inc., Patterson Medical Holdings Inc., Bird & Cronin Inc., ORTHOFIX MEDICAL INC., DeRoyal Industries Inc., ConvaTec Group Plc, Vancare Inc., Performance Health, Otto Bock Healthcare GmbH, Trulife, TenCate Protective Fabrics, Lohmann & Rauscher GmbH & Co. KG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Plaster Cast market is intricately segmented to provide a granular view of its various facets, encompassing the types of materials used, the diverse applications for which casts are employed, the end-user facilities where these are utilized, and the specific product types available. This multi-dimensional segmentation allows for a comprehensive understanding of market dynamics, enabling stakeholders to identify high-growth areas and tailor strategies effectively. The shift from traditional Plaster of Paris to synthetic options highlights an evolving preference driven by performance and patient convenience, while the end-user segments illustrate the broad spectrum of healthcare settings requiring orthopedic immobilization solutions.

- By Material:

- Plaster of Paris

- Fiberglass/Synthetic

- By Application:

- Fracture Management

- Deformity Correction

- Sprains & Strains

- Other Orthopedic Conditions

- By End-user:

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Homecare Settings

- By Product Type:

- Casting Tapes

- Casting Accessories (Padding, Stockinette, Cast Saw Blades)

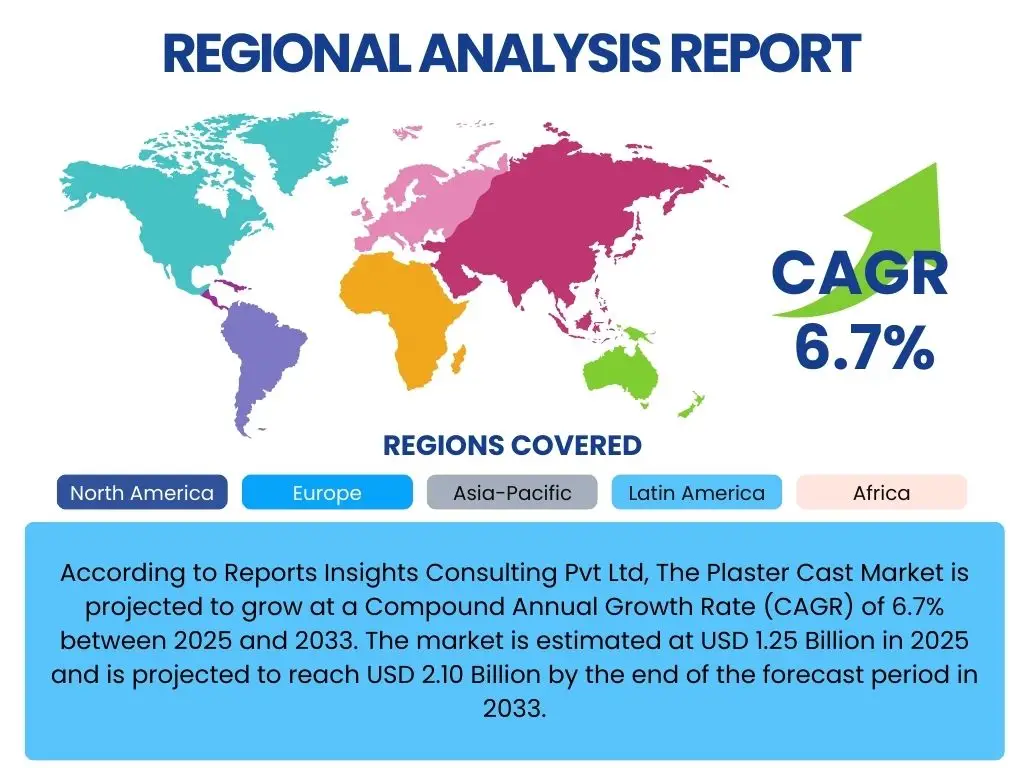

Regional Highlights

- North America: This region holds a significant share of the Plaster Cast market, primarily due to well-established healthcare infrastructure, high awareness regarding advanced orthopedic treatments, and a prevalence of sports-related injuries. High adoption rates of synthetic casts and ongoing research into new materials and technologies contribute to its market dominance.

- Europe: Europe is a prominent market, characterized by technological advancements, favorable reimbursement policies, and an aging population prone to fragility fractures. Countries like Germany and the UK are at the forefront of adopting innovative casting solutions and sustainable materials.

- Asia Pacific (APAC): Expected to witness the highest growth rate during the forecast period, driven by improving healthcare facilities, increasing disposable incomes, and a large patient pool. Rising awareness about modern orthopedic care and increasing government investments in healthcare infrastructure in countries like China and India are key growth catalysts.

- Latin America: This region shows steady growth, propelled by increasing healthcare expenditure, growing medical tourism, and a rising prevalence of road accidents and related injuries. Market expansion is supported by improvements in primary healthcare access.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, primarily due to developing healthcare infrastructure, increasing health awareness, and a rising incidence of orthopedic injuries. Investments in specialized orthopedic centers are expected to fuel future market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plaster Cast Market.- B Braun Melsungen AG

- 3M Company

- Össur hf.

- DJO Global Inc.

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Smith & Nephew plc

- Medline Industries LP

- Alimed Inc.

- Patterson Medical Holdings Inc.

- Bird & Cronin Inc.

- ORTHOFIX MEDICAL INC.

- DeRoyal Industries Inc.

- ConvaTec Group Plc

- Vancare Inc.

- Performance Health

- Otto Bock Healthcare GmbH

- Trulife

- TenCate Protective Fabrics

- Lohmann & Rauscher GmbH & Co. KG

Frequently Asked Questions

What is the projected growth rate for the Plaster Cast Market?

The Plaster Cast Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033.

What are the primary drivers of the Plaster Cast Market?

Key drivers include the increasing incidence of fractures and orthopedic injuries, a growing geriatric population, advancements in casting materials, and rising participation in sports and recreational activities.

How is AI impacting the Plaster Cast industry?

AI is influencing the market through enhanced diagnostic accuracy, optimization of cast design and fit, predictive analytics for complications, and integration into 3D printing processes for customized fabrication.

What are the main types of materials used in plaster casts?

The primary materials used are Plaster of Paris and synthetic materials, with fiberglass being the most common synthetic option due to its lightweight and water-resistant properties.

Which regions are expected to show significant growth in the Plaster Cast Market?

The Asia Pacific (APAC) region is expected to exhibit the highest growth rate, driven by improving healthcare infrastructure and increasing awareness in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted