Large Volume Parenteral Market

Large Volume Parenteral Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706076 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

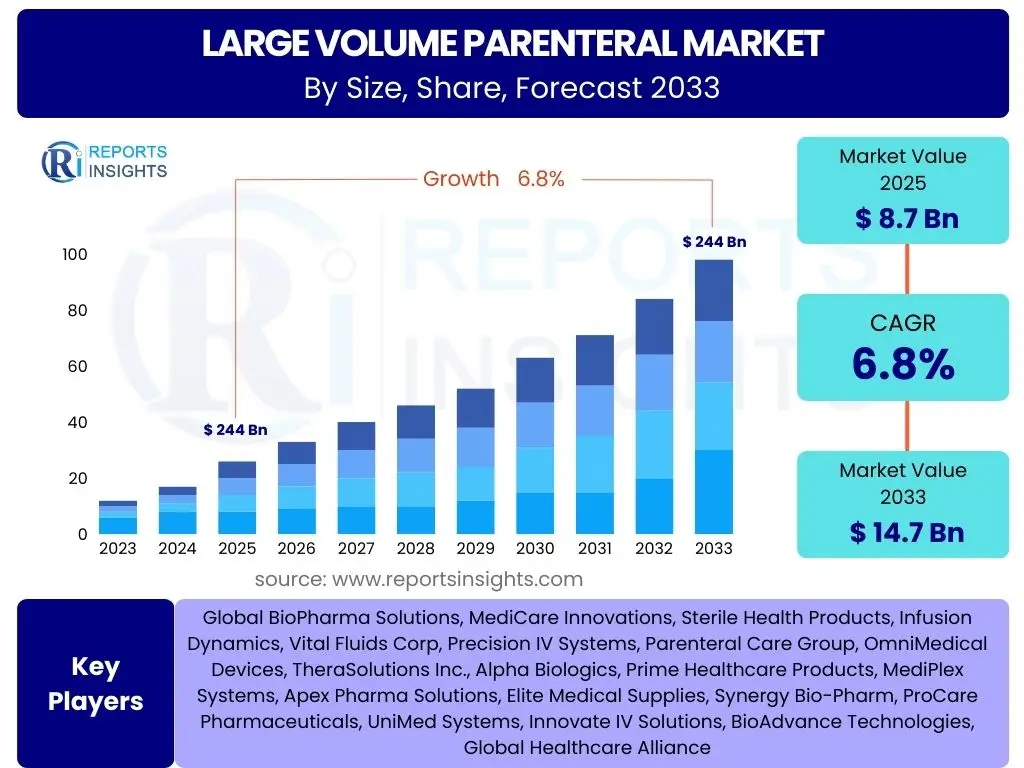

Large Volume Parenteral Market Size

According to Reports Insights Consulting Pvt Ltd, The Large Volume Parenteral Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 8.7 billion in 2025 and is projected to reach USD 14.7 billion by the end of the forecast period in 2033.

Key Large Volume Parenteral Market Trends & Insights

The Large Volume Parenteral (LVP) market is currently undergoing significant transformation, influenced by global demographic shifts and advancements in healthcare delivery. A primary trend observed is the increasing prevalence of chronic diseases such as diabetes, cardiovascular conditions, and various forms of cancer, which necessitate prolonged intravenous fluid administration for hydration, nutrition, and medication delivery. This escalating disease burden, coupled with an expanding aging population more prone to chronic ailments, consistently drives the demand for LVPs across diverse medical settings.

Another crucial insight is the evolving landscape of healthcare delivery, with a noticeable shift towards home healthcare and ambulatory care settings. This transition is spurred by patient preference for comfort and convenience, as well as cost-effectiveness for healthcare systems. Consequently, there is a growing demand for LVPs that are user-friendly, stable for extended periods, and compatible with portable infusion devices, reflecting a need for innovation in product design and packaging suitable for non-hospital environments.

Furthermore, technological advancements in LVP manufacturing and packaging are playing a pivotal role. Innovations in sterilization techniques, the development of safer and more durable packaging materials (such as non-PVC bags), and the integration of smart delivery systems are enhancing product safety, extending shelf life, and improving overall patient outcomes. The market also reflects a heightened focus on stringent regulatory compliance globally, pushing manufacturers to invest in robust quality control and assurance processes to meet evolving safety and efficacy standards.

- Rising prevalence of chronic and acute diseases.

- Increasing shift towards home healthcare and outpatient settings.

- Technological advancements in manufacturing and packaging.

- Growing aging population globally.

- Strict regulatory requirements ensuring product safety and quality.

AI Impact Analysis on Large Volume Parenteral

Artificial Intelligence (AI) is beginning to exert a transformative influence across various facets of the Large Volume Parenteral (LVP) market, particularly in optimizing manufacturing processes and enhancing quality control. AI-powered predictive maintenance systems can analyze data from production lines to anticipate equipment failures, thereby minimizing downtime and ensuring continuous supply. Furthermore, AI-driven visual inspection systems are capable of identifying defects in LVP products and packaging with greater accuracy and speed than traditional methods, significantly improving product quality and reducing the risk of contamination or recalls.

In the realm of supply chain and logistics, AI is proving invaluable for optimizing inventory management, forecasting demand with higher precision, and streamlining distribution networks. By analyzing vast datasets related to historical sales, seasonal variations, and geopolitical events, AI algorithms can help LVP manufacturers ensure adequate stock levels, prevent shortages, and facilitate timely delivery to healthcare facilities worldwide. This efficiency is crucial for critical care products like LVPs, where consistent availability directly impacts patient care.

Looking ahead, AI's potential extends to the development of personalized medicine, which, while not directly altering the LVP composition itself, influences the overall therapeutic landscape where LVPs are utilized. AI can assist in analyzing patient data to recommend optimal LVP formulations and dosages for individual needs, leading to more effective and safer treatments. Moreover, in clinical settings, AI could enhance decision support systems for healthcare professionals, guiding them in the appropriate selection and administration of LVPs based on real-time patient physiological data and treatment protocols.

- Optimization of LVP manufacturing processes through predictive analytics.

- Enhanced quality control and defect detection via AI-powered visual inspection.

- Improved supply chain management, including demand forecasting and inventory optimization.

- Potential for AI-driven clinical decision support for LVP administration.

- Acceleration of research and development in broader therapeutic areas utilizing LVPs.

Key Takeaways Large Volume Parenteral Market Size & Forecast

The Large Volume Parenteral (LVP) market is poised for sustained growth, reflecting its indispensable role in modern healthcare. The market's upward trajectory is primarily driven by the increasing global burden of chronic and acute diseases, which necessitate continuous intravenous administration for hydration, nutrition, and drug delivery. This fundamental demand ensures a resilient market, even amidst economic fluctuations, as LVPs are critical components of patient care across various medical settings, from emergency rooms to home care.

Innovation in product safety, quality, and delivery mechanisms remains a central theme in the LVP market. Manufacturers are increasingly focused on developing advanced packaging materials that enhance product stability and safety, while also exploring user-friendly designs for diverse healthcare environments, particularly outpatient and home care settings. This commitment to product integrity and ease of use is crucial for meeting stringent regulatory standards and fostering patient and healthcare provider confidence.

Furthermore, strategic collaborations, mergers, and acquisitions are significant factors shaping the competitive landscape, allowing companies to expand their geographical footprint, diversify product portfolios, and enhance research and development capabilities. The ongoing expansion of healthcare infrastructure in emerging economies, coupled with rising healthcare expenditure globally, continues to unlock new growth avenues for LVP market players, underscoring the market's long-term potential.

- The LVP market demonstrates robust and consistent growth.

- Product safety, quality, and advanced packaging are paramount.

- Increasing demand from chronic disease management and an aging population.

- Shift towards home and outpatient care drives innovation in delivery.

- Strategic market consolidation and expansion in emerging regions are key.

Large Volume Parenteral Market Drivers Analysis

The Large Volume Parenteral market expansion is significantly propelled by an increasing global disease burden, the aging population requiring intensive care, and advancements in surgical procedures. These demographic and medical trends necessitate a consistent supply of large volume parenteral solutions for hydration, nutrition, and drug delivery. The rising prevalence of chronic conditions like diabetes, cancer, and cardiovascular diseases directly translates into a higher demand for intravenous therapies, which are often sustained treatments utilizing LVPs. Concurrently, the increasing complexity and volume of surgical interventions globally require substantial intraoperative and postoperative fluid management, further boosting LVP consumption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | +0.6% | Global | Long-term |

| Increasing Number of Surgical Procedures | +0.5% | North America, Europe, Asia Pacific | Mid-term |

| Growing Geriatric Population | +0.4% | Developed Nations (e.g., Japan, Germany) | Long-term |

| Advancements in Healthcare Infrastructure | +0.7% | Emerging Economies (e.g., China, India) | Long-term |

| Demand for Home Healthcare & Outpatient Settings | +0.5% | Global | Mid-term |

Large Volume Parenteral Market Restraints Analysis

Despite robust growth, the LVP market faces significant hurdles including stringent regulatory approval processes, high manufacturing costs associated with maintaining sterility, and the inherent risks of product contamination and recalls which can severely impact market reputation and sales. The rigorous regulatory environment, particularly in developed regions, demands extensive clinical trials, quality assurance measures, and post-market surveillance, increasing the time and cost involved in bringing new LVP products to market. Furthermore, the specialized facilities and strict protocols required to ensure sterility during manufacturing contribute significantly to the overall production expenses, impacting profitability and market accessibility for smaller players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Landscape | -0.4% | Global | Ongoing |

| High Manufacturing & Sterilization Costs | -0.3% | Global | Short-term |

| Risk of Product Contamination & Recalls | -0.5% | Global | Recurring |

| Pricing Pressure & Reimbursement Challenges | -0.2% | Developed Markets | Mid-term |

| Supply Chain Disruptions | -0.4% | Global | Short-term |

Large Volume Parenteral Market Opportunities Analysis

Significant growth opportunities exist through the development of novel formulations catering to specific patient needs, expanding into underserved emerging markets, and integrating smart technologies for enhanced product monitoring and delivery. The increasing focus on personalized medicine creates avenues for specialized LVP solutions tailored for unique patient conditions or therapies, moving beyond standard solutions. Furthermore, the burgeoning healthcare sectors in Asia Pacific and Latin America present vast untapped potential, driven by improving economic conditions, increasing healthcare expenditure, and a rising awareness of advanced medical treatments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Formulations | +0.7% | Global | Long-term |

| Expansion into Emerging Markets | +0.8% | Asia Pacific, Latin America | Long-term |

| Integration of Smart Packaging & Delivery Systems | +0.6% | Developed Markets | Mid-term |

| Growing Focus on Personalized Medicine | +0.5% | Global | Long-term |

| Strategic Collaborations & Acquisitions | +0.6% | Global | Mid-term |

Large Volume Parenteral Market Challenges Impact Analysis

The market grapples with challenges such as maintaining product integrity throughout the supply chain, managing intellectual property rights for new formulations, ensuring environmental sustainability in manufacturing, and overcoming potential talent shortages in specialized areas. Ensuring the sterility and chemical stability of LVPs from production to patient bedside, especially across complex global supply chains with varied environmental conditions, poses a continuous challenge. Moreover, as innovations emerge, protecting intellectual property becomes crucial, alongside navigating the complexities of patent expirations and generic competition.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Product Integrity & Shelf Life | -0.4% | Global | Ongoing |

| Managing Complex Global Supply Chains | -0.3% | Global | Ongoing |

| Intellectual Property & Patent Expirations | -0.2% | Global | Mid-term |

| Environmental Compliance & Sustainability | -0.3% | Global | Long-term |

| Shortage of Skilled Workforce | -0.2% | Developed Markets | Mid-term |

Large Volume Parenteral Market - Updated Report Scope

This report provides a comprehensive analysis of the Large Volume Parenteral market, offering detailed insights into market dynamics, segmentation, and regional landscapes. The scope covers historical trends from 2019 to 2023 and provides a robust forecast from 2025 to 2033, enabling stakeholders to understand future growth trajectories and investment opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.7 billion |

| Market Forecast in 2033 | USD 14.7 billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global BioPharma Solutions, MediCare Innovations, Sterile Health Products, Infusion Dynamics, Vital Fluids Corp, Precision IV Systems, Parenteral Care Group, OmniMedical Devices, TheraSolutions Inc., Alpha Biologics, Prime Healthcare Products, MediPlex Systems, Apex Pharma Solutions, Elite Medical Supplies, Synergy Bio-Pharm, ProCare Pharmaceuticals, UniMed Systems, Innovate IV Solutions, BioAdvance Technologies, Global Healthcare Alliance |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Large Volume Parenteral market is comprehensively segmented across various dimensions including product type, application, packaging type, and end-use. This detailed segmentation allows for a granular understanding of specific market niches, demand patterns, and growth opportunities within the broader LVP landscape. Each segment represents distinct requirements and serves different patient populations and healthcare settings, thereby enabling targeted strategic planning for market participants.

The product type segment differentiates between various solutions like saline, dextrose, and specialized nutritional fluids, reflecting diverse medical needs from basic hydration to complex nutritional support. The application segment categorizes consumption based on where LVPs are primarily used, highlighting the growing significance of non-hospital settings. Similarly, packaging type segmentation addresses innovations and preferences in material and design, crucial for safety and ease of use. Lastly, end-use segmentation elucidates the primary medical purpose for which LVPs are administered, providing insights into therapeutic areas driving demand.

- Product Type:

- Saline Solutions

- Dextrose Solutions

- Ringer's Lactate

- Nutrition Solutions (Amino Acids, Lipids, Vitamins)

- Electrolyte Solutions

- Others

- Application:

- Hospitals

- Clinics

- Home Healthcare

- Ambulatory Surgical Centers

- Packaging Type:

- Plastic Bags

- Glass Bottles

- Semi-rigid Containers

- End-Use:

- Therapeutic Use

- Nutritional Support

- Blood Volume Expanders

- Electrolyte & Acid-Base Balance

Regional Highlights

- North America: This region holds a significant share in the Large Volume Parenteral market, driven by its advanced healthcare infrastructure, high prevalence of chronic and lifestyle-related diseases, and widespread adoption of sophisticated medical technologies. Robust healthcare expenditure and favorable reimbursement policies further contribute to market growth, with a strong emphasis on patient safety and quality standards.

- Europe: Europe represents a mature market for Large Volume Parenterals, characterized by a well-established healthcare system and an aging population that consistently drives demand for intravenous solutions for various medical conditions. Stringent regulatory frameworks for pharmaceutical products ensure high-quality standards, while a focus on cost-efficiency and home care solutions influences market trends.

- Asia Pacific (APAC): The Asia Pacific region is anticipated to exhibit the fastest growth rate in the LVP market during the forecast period. This surge is primarily attributed to a large and expanding patient pool, improving healthcare accessibility, increasing disposable incomes, and the rapid development of healthcare infrastructure, particularly in emerging economies like China and India. Government initiatives to enhance public health and rising awareness of advanced medical treatments also fuel market expansion.

- Latin America: The LVP market in Latin America is expected to demonstrate steady growth, propelled by increasing investments in healthcare facilities, rising awareness regarding advanced medical treatments, and a growing incidence of chronic diseases. Economic development and efforts to modernize healthcare systems in several countries are key factors contributing to market expansion in this region.

- Middle East and Africa (MEA): This region is projected to experience gradual growth in the Large Volume Parenteral market. Factors contributing to this growth include improving healthcare expenditure, ongoing development of medical infrastructure, and an increasing prevalence of chronic conditions requiring parenteral therapies. Strategic collaborations and investments in healthcare by regional governments are also supportive of market development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Large Volume Parenteral Market.- Global BioPharma Solutions

- MediCare Innovations

- Sterile Health Products

- Infusion Dynamics

- Vital Fluids Corp

- Precision IV Systems

- Parenteral Care Group

- OmniMedical Devices

- TheraSolutions Inc.

- Alpha Biologics

- Prime Healthcare Products

- MediPlex Systems

- Apex Pharma Solutions

- Elite Medical Supplies

- Synergy Bio-Pharm

- ProCare Pharmaceuticals

- UniMed Systems

- Innovate IV Solutions

- BioAdvance Technologies

- Global Healthcare Alliance

Frequently Asked Questions

Analyze common user questions about the Large Volume Parenteral market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Large Volume Parenterals (LVPs)?

Large Volume Parenterals (LVPs) are sterile, pyrogen-free solutions administered intravenously in volumes of 100 mL or more. They are primarily used for fluid and electrolyte replenishment, caloric and nutritional support, and as carriers for various medications, essential in diverse clinical settings from hospitals to home care.

What factors are driving the growth of the Large Volume Parenteral market?

The key growth drivers for the LVP market include the rising global prevalence of chronic diseases requiring intravenous therapy, the increasing aging population, a growing number of surgical procedures, advancements in healthcare infrastructure, and the expanding demand for home healthcare and outpatient services.

How is technology, particularly AI, impacting the LVP market?

AI is impacting the LVP market by optimizing manufacturing processes through predictive maintenance, enhancing quality control with automated inspection systems, improving supply chain efficiency via demand forecasting, and potentially aiding in clinical decision support for LVP administration and selection.

What are the primary applications of Large Volume Parenterals?

Large Volume Parenterals are primarily applied for therapeutic use (e.g., rehydration, electrolyte balance), nutritional support (e.g., total parenteral nutrition), blood volume expansion, and as vehicles for administering various medications in conditions ranging from acute illnesses to chronic disease management.

What are the key challenges facing the Large Volume Parenteral industry?

The primary challenges include stringent regulatory requirements, high manufacturing and sterilization costs, the persistent risk of product contamination and recalls, complexities in managing global supply chains, and environmental compliance issues. Additionally, pricing pressures and intellectual property concerns pose ongoing hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted