Medical Surgical Suture Market

Medical Surgical Suture Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709537 | Last Updated : December 10, 2025 |

Format : ![]()

![]()

![]()

![]()

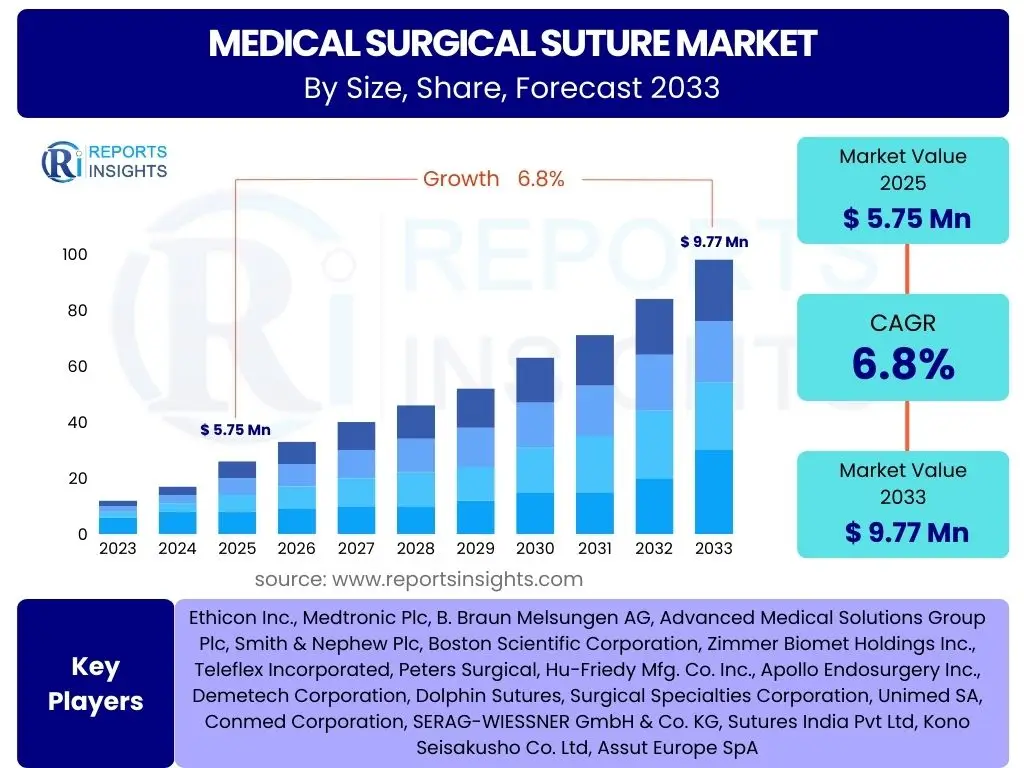

Medical Surgical Suture Market Size

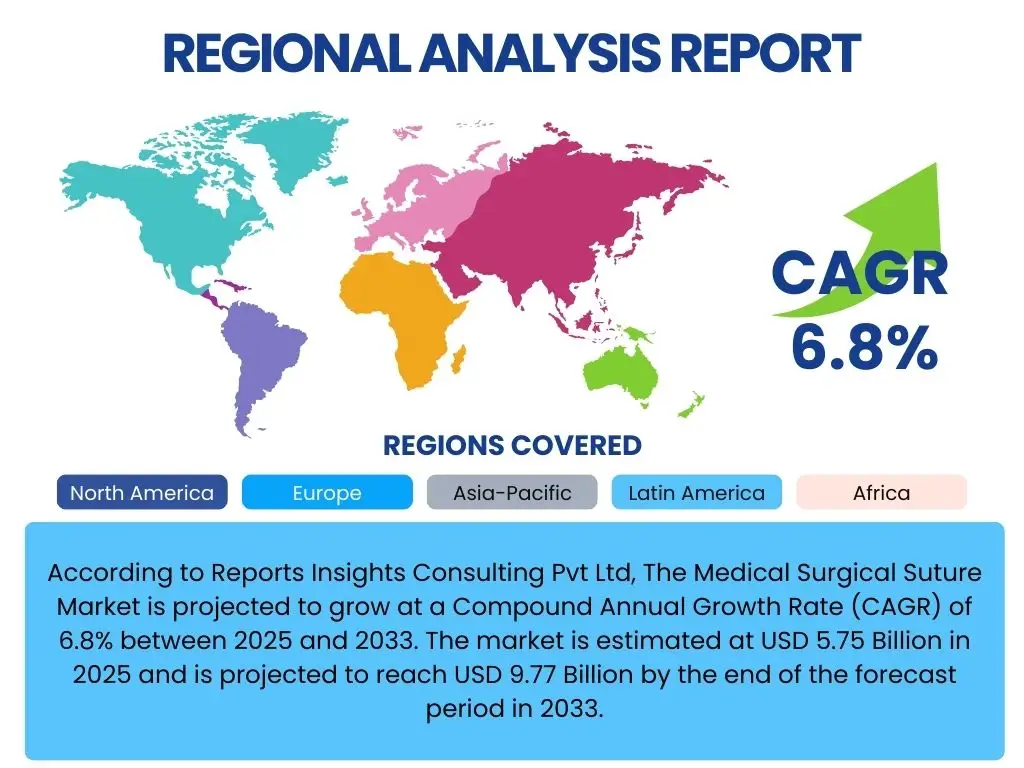

According to Reports Insights Consulting Pvt Ltd, The Medical Surgical Suture Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 5.75 Billion in 2025 and is projected to reach USD 9.77 Billion by the end of the forecast period in 2033.

Key Medical Surgical Suture Market Trends & Insights

The Medical Surgical Suture market is undergoing significant transformation, driven by a confluence of technological advancements, evolving surgical practices, and an increasing focus on patient outcomes. Key trends reveal a strong shift towards advanced materials offering superior performance, enhanced biocompatibility, and reduced risk of complications. Users frequently inquire about novel suture designs that facilitate faster healing and minimize surgical trauma, indicating a high demand for innovative solutions in wound closure.

Another prominent area of interest revolves around the integration of smart technologies and specialized coatings in sutures. The market is witnessing the development of antimicrobial sutures to combat surgical site infections (SSIs) and drug-eluting sutures for localized drug delivery. These advancements are critical as healthcare providers seek to improve post-operative recovery and reduce hospitalization times, addressing common challenges highlighted by surgical professionals and patients alike. The push for minimally invasive procedures further shapes demand, favoring smaller, more versatile, and easier-to-handle sutures.

Furthermore, the market is influenced by the increasing adoption of robotic-assisted surgeries, which necessitate specific types of sutures compatible with robotic instruments. This trend, along with the growing prevalence of chronic diseases requiring surgical intervention and an expanding geriatric population, continues to fuel the demand for diverse and high-quality surgical sutures. The emphasis on biodegradable materials also reflects a broader industry movement towards sustainability and reduced foreign body reactions, a common concern among healthcare practitioners.

- Shift towards advanced biodegradable and bio-absorbable materials.

- Development of antimicrobial and drug-eluting sutures to reduce infection risks.

- Increasing demand for sutures compatible with minimally invasive and robotic surgeries.

- Growing preference for synthetic over natural sutures due to consistent performance.

- Focus on enhanced knot security and tensile strength for improved surgical outcomes.

- Introduction of barbed sutures for knotless wound closure and faster procedures.

AI Impact Analysis on Medical Surgical Suture

Artificial Intelligence (AI) is poised to exert a transformative influence across various facets of the Medical Surgical Suture market, from research and development to manufacturing and even surgical application. User inquiries frequently center on how AI can accelerate the discovery of novel biomaterials for sutures, optimize their design for specific surgical needs, and enhance the precision of manufacturing processes. AI algorithms can analyze vast datasets of material properties and biological interactions, predicting the performance of new suture compositions with greater accuracy and speed than traditional methods, thereby reducing R&D cycles and costs.

In the manufacturing domain, AI-powered systems can significantly improve quality control and production efficiency. Through real-time monitoring and predictive analytics, AI can detect anomalies in suture production, ensuring consistent tensile strength, uniform diameter, and optimal coating application, which are critical for surgical reliability. This precision directly addresses common user concerns regarding suture consistency and reliability. Furthermore, AI can optimize supply chain logistics, predicting demand fluctuations and managing inventory more effectively, thus ensuring timely availability of essential surgical supplies.

Looking ahead, AI's impact could extend to surgical planning and execution, though more indirectly for the suture itself. AI-assisted surgical platforms might recommend optimal suture types or knotting techniques based on patient-specific data and tissue characteristics, potentially minimizing complications. While direct AI involvement in suture placement remains nascent, the technology's role in improving the entire ecosystem surrounding surgical procedures, including the quality and availability of sutures, is becoming increasingly evident. Users are keenly interested in how these technological integrations translate into safer surgeries and improved patient recovery times.

- Accelerated discovery and development of novel suture materials through AI-driven material science.

- Enhanced precision manufacturing and quality control via AI algorithms and predictive analytics.

- Optimized supply chain management and inventory forecasting for suture products.

- Potential for AI-assisted surgical planning to recommend optimal suture types and techniques.

- Data-driven insights for understanding suture performance and improving product design.

- Automation of inspection processes, reducing human error and improving product consistency.

Key Takeaways Medical Surgical Suture Market Size & Forecast

The Medical Surgical Suture market is on a robust growth trajectory, primarily fueled by the global increase in surgical procedures and continuous advancements in suture technology. A significant takeaway for stakeholders is the sustained demand for high-quality, specialized sutures that can address diverse surgical requirements and enhance patient outcomes. The forecast indicates that innovation in material science and manufacturing processes will remain a critical differentiator, pushing the market towards more absorbable, antimicrobial, and minimally invasive-compatible solutions. Users are particularly interested in understanding the core factors contributing to this consistent growth and where future investment opportunities lie.

Furthermore, the market's resilience is underscored by its ability to adapt to evolving healthcare landscapes, including the shift towards outpatient surgeries and the integration of advanced surgical techniques like robotics. Manufacturers focusing on cost-effective, high-performance sutures for emerging economies, alongside premium, specialized products for developed markets, are positioned for substantial growth. The increasing prevalence of chronic diseases and an aging global population will continue to provide a stable foundation for market expansion, ensuring sustained demand for surgical wound closure solutions.

A crucial insight gleaned from market analysis is the intensifying competition among market players, driving continuous product innovation and strategic collaborations. Companies that prioritize research and development, stringent quality control, and effective distribution networks will likely capture a larger market share. The emphasis on reducing surgical site infections and improving patient recovery will continue to shape product development, making features like antimicrobial properties and tailored absorption profiles highly desirable. Understanding these dynamics is essential for market participants to formulate effective strategies and capitalize on the projected market growth.

- The Medical Surgical Suture market is poised for significant growth, reaching nearly USD 10 Billion by 2033.

- Technological innovation in material science and suture design is a primary growth driver.

- Increasing surgical volumes globally, driven by chronic diseases and an aging population, underpins market expansion.

- High demand for specialized sutures, including absorbable, antimicrobial, and barbed varieties.

- Emerging economies present substantial growth opportunities due to improving healthcare infrastructure.

- Focus on reducing surgical site infections and enhancing patient recovery is central to product development.

Medical Surgical Suture Market Drivers Analysis

The Medical Surgical Suture market is significantly propelled by several key drivers that collectively foster its expansion and innovation. A primary driver is the ever-increasing volume of surgical procedures performed globally, stemming from the rising prevalence of chronic conditions such as cardiovascular diseases, orthopedic disorders, and various forms of cancer. As populations grow and healthcare access improves in developing regions, the demand for effective wound closure solutions, including sutures, naturally escalates. This demographic shift, coupled with an aging global population, further contributes to the need for surgical interventions, thereby boosting suture consumption across diverse medical specialties.

Another crucial driver is the continuous technological advancement in suture materials and designs. Innovations have led to the development of sutures with enhanced biocompatibility, improved tensile strength, superior knot security, and reduced tissue drag. The introduction of absorbable sutures that minimize foreign body reactions and eliminate the need for removal, as well as antimicrobial-coated sutures designed to prevent surgical site infections, significantly improves patient outcomes and surgeon preference. These advancements not only meet the evolving demands of modern surgery but also align with the broader healthcare objective of reducing post-operative complications and accelerating patient recovery.

Furthermore, the growing adoption of minimally invasive surgical techniques, including laparoscopic and robotic-assisted surgeries, necessitates specialized sutures that are easy to handle within confined spaces and offer reliable wound approximation. This trend, while challenging in terms of dexterity, drives innovation in suture design and delivery systems, creating new market segments. The increasing investment in healthcare infrastructure, particularly in emerging economies, also facilitates greater accessibility to advanced surgical facilities and, consequently, a higher utilization of medical surgical sutures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Number of Surgical Procedures Globally | +1.8% | Global | Short to Mid-term |

| Technological Advancements in Suture Materials and Design | +1.5% | North America, Europe, Asia Pacific | Mid to Long-term |

| Rising Prevalence of Chronic Diseases and Aging Population | +1.2% | Global, particularly Developed Economies | Long-term |

| Growing Adoption of Minimally Invasive Surgical Techniques | +1.0% | North America, Europe | Mid-term |

| Increasing Focus on Reducing Surgical Site Infections (SSIs) | +0.9% | Global | Ongoing |

Medical Surgical Suture Market Restraints Analysis

Despite robust growth, the Medical Surgical Suture market faces several significant restraints that could impede its expansion. One primary restraint is the increasing availability and adoption of alternative wound closure methods, such as surgical staplers, wound closure strips, tissue adhesives, and sealants. These alternatives often offer advantages like faster closure times, reduced need for knotting, and potentially lower risks of needle-stick injuries, thereby presenting a competitive threat to traditional sutures. While sutures remain indispensable for many complex procedures, the growing preference for these alternatives in certain applications can limit suture market growth.

Another considerable restraint involves the high cost associated with advanced and specialized sutures, particularly those incorporating antimicrobial coatings or unique designs like barbed sutures. Healthcare providers, especially in price-sensitive markets or those operating under strict budget constraints, may opt for more conventional and less expensive suture options. This cost-effectiveness pressure can limit the adoption of premium sutures, impacting manufacturers' profitability and market penetration, particularly in developing regions where healthcare expenditure per capita is lower.

Furthermore, the stringent regulatory approval processes for new medical devices, including surgical sutures, pose a significant challenge. Obtaining approvals from regulatory bodies such as the FDA in the United States or the EMA in Europe requires extensive clinical trials, rigorous testing, and substantial investments, leading to prolonged market entry timelines. This regulatory burden can stifle innovation and delay the introduction of potentially groundbreaking suture technologies. Additionally, the risk of surgical site infections (SSIs), though often mitigated by advanced sutures, still remains a concern and can lead to increased healthcare costs and patient morbidity, indirectly influencing the choice of wound closure products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Availability of Alternative Wound Closure Products | -1.0% | Global | Ongoing |

| High Cost of Advanced and Specialized Sutures | -0.8% | Developing Economies, Budget-Constrained Markets | Short to Mid-term |

| Stringent Regulatory Approval Processes | -0.7% | North America, Europe | Long-term |

| Risk of Surgical Site Infections (SSIs) | -0.6% | Global | Ongoing |

| Lack of Skilled Surgeons in Developing Regions | -0.5% | Asia Pacific, Latin America, MEA | Long-term |

Medical Surgical Suture Market Opportunities Analysis

The Medical Surgical Suture market is rich with opportunities for growth and innovation, driven by unmet clinical needs and evolving healthcare paradigms. A significant opportunity lies in the continuous development of novel suture materials and designs, particularly those offering enhanced therapeutic properties. This includes sutures embedded with growth factors, stem cells, or other bioactive agents that can actively promote tissue regeneration and wound healing, moving beyond mere mechanical wound approximation. Such innovations promise to address complex surgical challenges and open new application areas in regenerative medicine and advanced therapies.

Another promising avenue is the expansion into emerging economies, particularly in Asia Pacific, Latin America, and parts of the Middle East and Africa. These regions are experiencing rapid improvements in healthcare infrastructure, increasing disposable incomes, and a growing patient population with access to surgical care. As these markets mature, the demand for both basic and advanced surgical sutures is expected to surge, offering substantial market penetration and revenue growth opportunities for manufacturers willing to adapt to local market dynamics and pricing sensitivities. Strategic partnerships and localized manufacturing can be key to unlocking these regions' full potential.

Furthermore, the increasing adoption of robotic-assisted and minimally invasive surgical procedures globally presents a lucrative opportunity. These advanced surgical techniques require specialized sutures that are slender, strong, and easy to manipulate through small incisions or robotic instruments. Manufacturers that can develop and supply sutures optimized for these high-precision, low-trauma procedures will gain a significant competitive edge. The growing focus on personalized medicine also creates opportunities for custom-designed sutures tailored to individual patient needs, tissue characteristics, and specific surgical requirements, promising a higher level of surgical precision and improved patient outcomes.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bioactive and Regenerative Sutures | +1.7% | Global | Long-term |

| Expansion into Emerging Economies | +1.5% | Asia Pacific, Latin America, MEA | Mid to Long-term |

| Growing Adoption of Robotic and Minimally Invasive Surgery | +1.3% | North America, Europe, Asia Pacific | Mid-term |

| Increasing Demand for Antimicrobial and Barbed Sutures | +1.1% | Global | Short to Mid-term |

| Partnerships and Collaborations for Product Innovation | +0.9% | Global | Ongoing |

Medical Surgical Suture Market Challenges Impact Analysis

The Medical Surgical Suture market faces several inherent challenges that demand strategic navigation from manufacturers and suppliers. One significant challenge is the intense market competition, characterized by the presence of numerous global and regional players offering a wide range of products. This fierce competition often leads to pricing pressures, forcing companies to balance product innovation with cost-effectiveness. Maintaining profitability while investing heavily in research and development to stay ahead of competitors becomes a delicate act, particularly for smaller market entrants. The constant need to differentiate products in a crowded market segment requires continuous investment in marketing and clinical evidence.

Another critical challenge is ensuring the consistent quality and sterility of suture products, which are directly related to patient safety and surgical outcomes. Any lapse in manufacturing standards or sterilization processes can lead to severe complications, reputational damage, and regulatory penalties. Companies must adhere to rigorous quality control measures and international manufacturing standards, which often involves substantial operational costs and complex supply chain management. The global nature of raw material sourcing further complicates this, as maintaining traceability and quality across diverse supply chains is a perpetual concern.

Moreover, the market is continually challenged by the dynamic regulatory landscape and evolving healthcare policies across different regions. What is approved in one country may require significant modifications or additional trials for approval in another, creating barriers to global market expansion and increasing compliance costs. The imperative to develop sustainable and environmentally friendly manufacturing processes also presents a growing challenge, as healthcare systems increasingly prioritize eco-conscious solutions. Balancing these multiple demands—innovation, quality, cost, regulation, and sustainability—requires robust strategic planning and agile operational execution from all market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressures | -1.0% | Global | Ongoing |

| Stringent Quality Control and Sterility Requirements | -0.8% | Global | Ongoing |

| Complex and Evolving Regulatory Landscape | -0.7% | North America, Europe, Asia Pacific | Long-term |

| Managing Global Supply Chain Disruptions | -0.6% | Global | Short to Mid-term |

| Need for Continuous Research and Development Investment | -0.5% | Global | Long-term |

Medical Surgical Suture Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Medical Surgical Suture market, offering detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. The scope encompasses a thorough examination of key market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape. It also includes an extensive segmentation analysis across various product types, materials, applications, and end-uses, along with a detailed regional outlook. Furthermore, the report assesses the competitive landscape by profiling leading market players and evaluating their strategic initiatives, ensuring a holistic understanding for stakeholders and potential investors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.75 Billion |

| Market Forecast in 2033 | USD 9.77 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ethicon Inc., Medtronic Plc, B. Braun Melsungen AG, Advanced Medical Solutions Group Plc, Smith & Nephew Plc, Boston Scientific Corporation, Zimmer Biomet Holdings Inc., Teleflex Incorporated, Peters Surgical, Hu-Friedy Mfg. Co. Inc., Apollo Endosurgery Inc., Demetech Corporation, Dolphin Sutures, Surgical Specialties Corporation, Unimed SA, Conmed Corporation, SERAG-WIESSNER GmbH & Co. KG, Sutures India Pvt Ltd, Kono Seisakusho Co. Ltd, Assut Europe SpA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Medical Surgical Suture market is meticulously segmented to provide a granular view of its diverse components, allowing for a comprehensive understanding of market dynamics across various dimensions. This segmentation helps identify specific growth areas, competitive landscapes within sub-sectors, and the varying preferences of end-users based on their surgical needs and operational environments. The market is primarily categorized by product type, differentiating between absorbable and non-absorbable sutures, which are further broken down into natural and synthetic materials, reflecting fundamental differences in their biological interaction and application.

Beyond material composition, the market is also segmented by application, covering a wide array of surgical specialties from cardiovascular and orthopedic procedures to general surgery and ophthalmology. This level of detail highlights the specific requirements and demands placed on sutures within each medical field, influencing design, material selection, and technological integration. Furthermore, segmenting by end-use environments, such as hospitals, ambulatory surgical centers, and clinics, provides insights into procurement patterns, volume demands, and infrastructure requirements across different healthcare settings.

Geographical segmentation is also crucial, offering a regional and country-specific analysis of market size, growth rates, and prevailing trends. This multi-faceted segmentation framework enables a detailed assessment of market opportunities and challenges, facilitating strategic decision-making for manufacturers, suppliers, and healthcare providers. Understanding these distinct segments is essential for developing targeted products, optimizing marketing strategies, and capitalizing on niche market demands effectively.

- By Product Type:

- Absorbable Sutures

- Natural Absorbable Sutures (e.g., Catgut)

- Synthetic Absorbable Sutures (e.g., Polydioxanone (PDO), Polyglactin 910 (PGLA), Polyglycolic Acid (PGA), Poliglecaprone 25 (PGCL))

- Non-Absorbable Sutures

- Natural Non-Absorbable Sutures (e.g., Silk, Cotton, Steel)

- Synthetic Non-Absorbable Sutures (e.g., Polypropylene, Nylon, Polyester, PVDF, PTFE)

- Absorbable Sutures

- By Material:

- Natural

- Synthetic

- By Application:

- Cardiovascular Surgery

- General Surgery

- Orthopedic Surgery

- Gynecological Surgery

- Ophthalmic Surgery

- Neurological Surgery

- Plastic Surgery

- Urology

- Others

- By End-Use:

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East and Africa (MEA)

Regional Highlights

- North America: This region holds a dominant share in the Medical Surgical Suture market, driven by its advanced healthcare infrastructure, high per capita healthcare spending, significant number of surgical procedures, and early adoption of innovative medical technologies. The presence of major market players and robust research and development activities also contribute to its leading position.

- Europe: Europe represents a substantial market share, characterized by an aging population, rising prevalence of chronic diseases requiring surgical intervention, and well-established healthcare systems. Countries like Germany, the UK, and France are key contributors, with an increasing focus on minimally invasive surgeries and advanced wound closure techniques.

- Asia Pacific (APAC): Expected to be the fastest-growing regional market, APAC's expansion is fueled by improving healthcare access, increasing medical tourism, rising disposable incomes, and a large patient pool. Countries such as China, India, and Japan are witnessing significant investments in healthcare infrastructure and a growing awareness of advanced surgical practices.

- Latin America: This region is an emerging market with gradual growth, attributed to increasing healthcare expenditure, improving economic conditions, and a growing number of surgical facilities. Brazil and Mexico are leading the regional growth, with rising demand for affordable yet effective surgical solutions.

- Middle East and Africa (MEA): The MEA region is projected to experience steady growth, primarily driven by increasing government initiatives to modernize healthcare facilities, growing health awareness, and a rise in medical tourism in certain countries. The adoption of advanced medical devices, including surgical sutures, is gradually expanding.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Medical Surgical Suture Market.- Ethicon Inc.

- Medtronic Plc

- B. Braun Melsungen AG

- Advanced Medical Solutions Group Plc

- Smith & Nephew Plc

- Boston Scientific Corporation

- Zimmer Biomet Holdings Inc.

- Teleflex Incorporated

- Peters Surgical

- Hu-Friedy Mfg. Co. Inc.

- Apollo Endosurgery Inc.

- Demetech Corporation

- Dolphin Sutures

- Surgical Specialties Corporation

- Unimed SA

- Conmed Corporation

- SERAG-WIESSNER GmbH & Co. KG

- Sutures India Pvt Ltd

- Kono Seisakusho Co. Ltd

- Assut Europe SpA

Frequently Asked Questions

Analyze common user questions about the Medical Surgical Suture market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Medical Surgical Suture Market?

The Medical Surgical Suture Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 9.77 Billion by 2033.

What are the primary drivers of the Medical Surgical Suture Market?

Key drivers include the increasing number of surgical procedures globally, technological advancements in suture materials and designs, the rising prevalence of chronic diseases, and the growing adoption of minimally invasive surgical techniques.

How is AI impacting the Medical Surgical Suture Market?

AI is impacting the market through accelerated material discovery, enhanced precision in manufacturing and quality control, optimized supply chain management, and potential for AI-assisted surgical planning and product design improvements.

Which region holds the largest market share in Medical Surgical Sutures?

North America currently holds the largest market share in the Medical Surgical Suture Market, attributed to its advanced healthcare infrastructure, high surgical volumes, and rapid adoption of innovative medical technologies.

What are the key challenges faced by the market?

Key challenges include intense market competition and associated pricing pressures, stringent quality control and sterility requirements, complex and evolving regulatory landscapes, and the increasing availability of alternative wound closure methods.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted