Pipeline Thermal Insulation Material Market

Pipeline Thermal Insulation Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701272 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

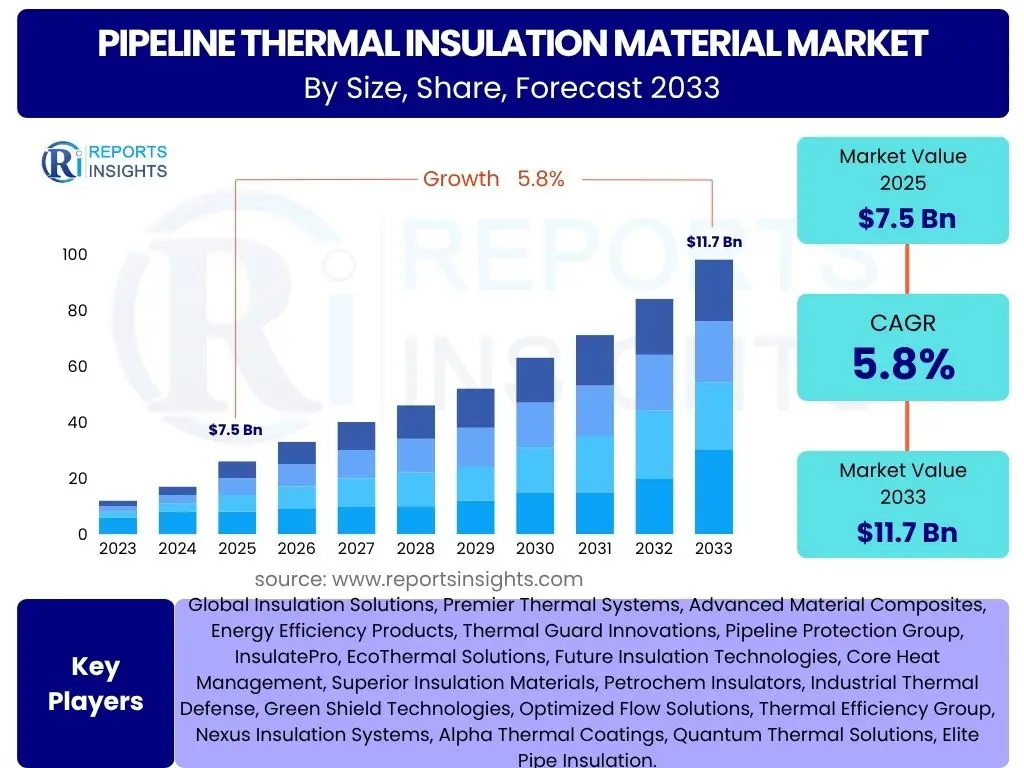

Pipeline Thermal Insulation Material Market Size

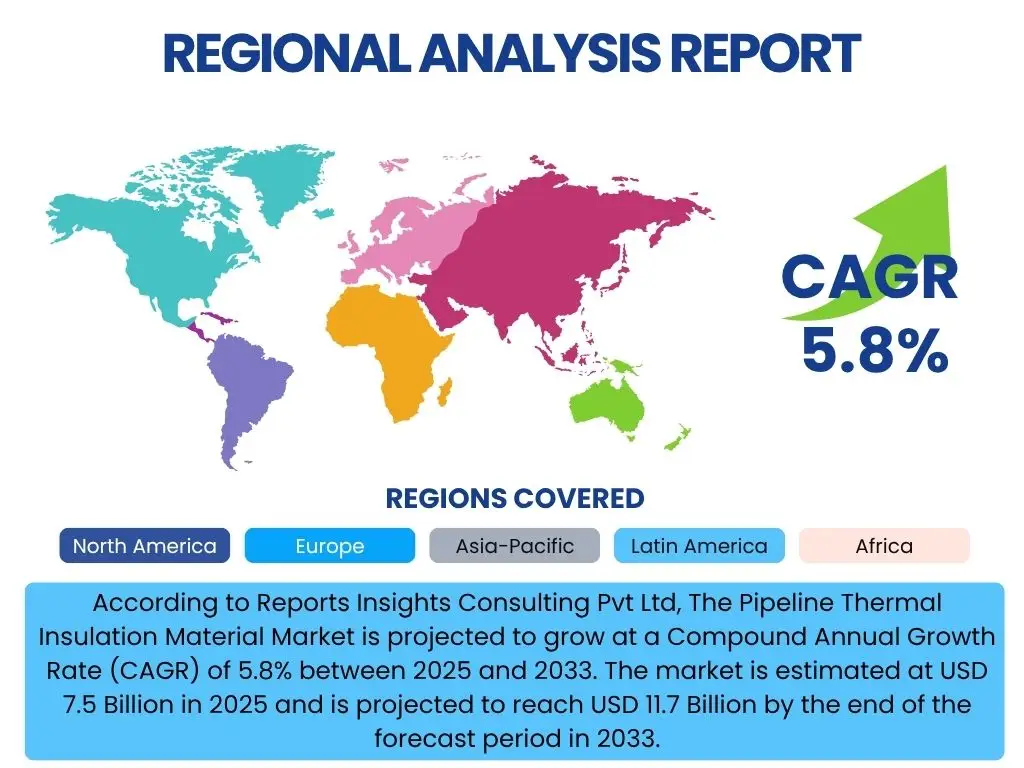

According to Reports Insights Consulting Pvt Ltd, The Pipeline Thermal Insulation Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 7.5 Billion in 2025 and is projected to reach USD 11.7 Billion by the end of the forecast period in 2033.

The robust expansion of the pipeline thermal insulation material market is primarily driven by the escalating global demand for energy efficiency across various industrial sectors. As industries strive to minimize heat loss, optimize energy consumption, and adhere to stringent environmental regulations, the adoption of advanced thermal insulation materials for pipelines has become imperative. This growth is further fueled by significant investments in new infrastructure projects, particularly in oil and gas, chemicals, and power generation, which necessitate reliable and high-performance insulation solutions to ensure operational safety and cost-effectiveness.

The market's trajectory is also influenced by the continuous innovation in material science, leading to the development of more effective, durable, and sustainable insulation products. These advancements address critical industry needs such as enhanced resistance to extreme temperatures, corrosion, and mechanical stress, thereby extending the lifespan of pipelines and reducing maintenance costs. Furthermore, the increasing focus on reducing carbon emissions and achieving net-zero targets globally is propelling the demand for insulation materials that contribute to energy savings and environmental protection, solidifying the market's growth outlook through 2033.

Key Pipeline Thermal Insulation Material Market Trends & Insights

User inquiries regarding trends in the Pipeline Thermal Insulation Material market frequently highlight the shift towards high-performance and sustainable solutions, alongside the integration of smart technologies. There is significant interest in how regulatory pressures for energy efficiency and reduced emissions are shaping material innovation and application techniques. Common questions also explore the impact of digitalization on insulation performance monitoring and the growing importance of life-cycle assessment in material selection, indicating a holistic view of insulation as a critical component of sustainable industrial operations rather than merely a static barrier.

- Advancement in High-Performance Materials: Growing demand for insulation materials with superior thermal resistance, durability, and operational longevity, including aerogels, vacuum insulation panels (VIPs), and advanced elastomeric foams, capable of performing in extreme temperature ranges and harsh environments.

- Emphasis on Sustainability and Eco-Friendly Solutions: Increasing adoption of insulation materials that are recyclable, have lower embodied energy, and are derived from sustainable or bio-based sources, driven by environmental regulations and corporate sustainability initiatives.

- Integration of Smart Insulation Systems: Emergence of insulation solutions incorporating sensors, IoT devices, and data analytics for real-time monitoring of temperature, pressure, and structural integrity, enabling predictive maintenance and optimized energy management.

- Focus on Prefabricated and Modular Insulation Systems: Growing preference for factory-made insulation modules and pre-insulated pipes that offer faster installation, consistent quality, and reduced on-site labor, leading to cost and time efficiencies in project execution.

- Rising Demand for Cryogenic and High-Temperature Insulation: Significant growth in specialized insulation for applications involving liquefied natural gas (LNG), hydrogen transportation, and high-temperature industrial processes, requiring materials with exceptional thermal stability and low thermal conductivity across extreme temperature differentials.

- Strict Regulatory Frameworks for Energy Efficiency: Intensified global regulations and standards promoting energy conservation and emission reduction in industrial and commercial sectors, directly stimulating the adoption of advanced pipeline thermal insulation to meet compliance requirements.

AI Impact Analysis on Pipeline Thermal Insulation Material

User questions related to the impact of AI on Pipeline Thermal Insulation Material primarily revolve around its potential to revolutionize design, monitoring, and maintenance processes. Users are keen to understand how AI algorithms can optimize material selection for specific environmental conditions, predict insulation degradation, and enhance the overall efficiency of pipeline networks. There is also interest in AI's role in improving manufacturing precision for insulation materials and facilitating automated inspection of insulated pipelines, pointing towards an expectation of greater accuracy, reduced human intervention, and proactive asset management.

- Predictive Maintenance and Performance Monitoring: AI-powered analytics can process data from sensors embedded within or around insulation to predict degradation, detect thermal anomalies, and schedule maintenance proactively, minimizing downtime and extending asset life.

- Optimized Material Design and Selection: AI algorithms can analyze vast datasets of material properties, environmental conditions, and performance requirements to recommend optimal insulation material compositions and designs, leading to superior thermal efficiency and cost-effectiveness.

- Automated Quality Control in Manufacturing: AI-driven vision systems and sensors can monitor the production of insulation materials in real-time, identifying defects and ensuring consistent quality, which is crucial for high-performance applications.

- Enhanced Supply Chain and Logistics Management: AI can optimize the procurement, storage, and distribution of insulation materials, predicting demand fluctuations and ensuring timely delivery, thereby reducing logistical costs and project delays.

- Robotics and Automation in Installation: While nascent, AI combined with robotics could potentially automate complex insulation application processes in hazardous or difficult-to-access pipeline sections, improving safety and installation precision.

- Energy Consumption Optimization: AI can model and simulate the thermal performance of insulated pipelines under varying operational conditions, providing insights to further optimize energy consumption and reduce operational expenditure over the pipeline's lifecycle.

Key Takeaways Pipeline Thermal Insulation Material Market Size & Forecast

Common inquiries regarding key takeaways from the Pipeline Thermal Insulation Material market size and forecast consistently focus on identifying the most lucrative growth segments, the geographical areas poised for significant expansion, and the overarching factors driving the market's long-term viability. Users seek concise summaries of market opportunities for new entrants and established players, alongside an understanding of the critical challenges that could impede growth. The general sentiment is a desire for clear, actionable insights that highlight the market's trajectory and strategic implications for investment and development.

- Robust and Consistent Growth: The market is set for steady growth driven by global industrialization, infrastructure development, and an increasing emphasis on energy efficiency and environmental compliance.

- Innovation as a Growth Catalyst: Continuous advancements in material science, including the development of aerogels, vacuum insulation panels, and sustainable materials, are key enablers for market expansion and performance improvement.

- Diverse End-Use Applications: Significant demand spans across critical sectors such as oil & gas, chemicals, power generation, and district heating & cooling, ensuring a broad and resilient market base.

- Asia Pacific Leads Regional Expansion: Rapid industrial growth and extensive infrastructure projects in emerging economies, particularly China and India, position the Asia Pacific region as the dominant and fastest-growing market.

- Strategic Importance of Regulatory Compliance: Stringent environmental regulations and energy efficiency mandates globally are not only driving demand but also shaping product development towards more sustainable and high-performance solutions.

- Increasing Focus on Smart and Integrated Solutions: The market is moving towards intelligent insulation systems that offer real-time monitoring and predictive capabilities, adding significant value beyond basic thermal resistance.

Pipeline Thermal Insulation Material Market Drivers Analysis

The global drive for enhanced energy efficiency and stringent environmental regulations stands as a paramount driver for the Pipeline Thermal Insulation Material market. Industries across the spectrum are increasingly mandated to reduce energy consumption and minimize greenhouse gas emissions, making high-performance thermal insulation a fundamental requirement. This translates into a strong demand for materials that can effectively prevent heat loss or gain in pipelines, thereby optimizing operational costs and ensuring compliance with evolving environmental standards.

Furthermore, the significant global investments in industrial infrastructure, particularly within the oil and gas, chemicals, and power generation sectors, are substantially propelling market growth. As new pipelines are constructed and existing infrastructure undergoes upgrades to improve safety and efficiency, the deployment of advanced thermal insulation materials becomes crucial. This demand is particularly pronounced in emerging economies where rapid industrialization and urbanization projects necessitate extensive pipeline networks, driving both new installations and replacement cycles for insulation materials.

The continuous innovation in material science, leading to the development of superior insulation products, also serves as a vital market driver. The introduction of materials with enhanced thermal performance, durability, and ease of installation, such as aerogels and advanced elastomeric foams, addresses the evolving needs of various applications. These innovations offer solutions for extreme temperature environments and harsh operating conditions, further solidifying the market's expansion as industries seek more effective and long-lasting thermal management solutions for their critical pipeline assets.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Focus on Energy Efficiency and Conservation | +1.5% | Global, particularly Europe & North America | Short to Long-term |

| Growth in Oil & Gas, Chemical, and Power Generation Infrastructure | +1.2% | Asia Pacific, Middle East & Africa, North America | Medium to Long-term |

| Stringent Environmental Regulations and Emission Reduction Targets | +0.8% | Europe, North America, Japan | Short to Medium-term |

| Technological Advancements in Insulation Materials | +0.7% | Global | Medium to Long-term |

Pipeline Thermal Insulation Material Market Restraints Analysis

One significant restraint impacting the Pipeline Thermal Insulation Material market is the volatile pricing of raw materials. The production of many insulation materials, such as polyurethane foam, mineral wool, and fiberglass, relies on petrochemical derivatives, glass fibers, and various binders, whose costs are subject to global supply chain disruptions, geopolitical tensions, and fluctuations in energy prices. This unpredictability in raw material costs can directly affect the manufacturing costs of insulation products, potentially leading to higher end-product prices, which in turn can influence project budgets and deter adoption, especially for large-scale infrastructure projects.

Another key restraint is the high initial installation cost associated with advanced insulation systems. While high-performance materials like aerogels offer superior thermal efficiency and long-term savings, their upfront material and specialized application costs can be considerably higher than traditional insulation types. This elevated initial investment can be a significant barrier for companies, particularly small and medium-sized enterprises (SMEs) or those with limited capital budgets, leading them to opt for less efficient but cheaper alternatives despite the long-term operational disadvantages.

Furthermore, the complexities involved in retrofitting existing pipeline infrastructure with new insulation materials pose a notable challenge. Many older pipelines were designed without considering modern insulation requirements, making it difficult and expensive to remove old, potentially hazardous insulation and replace it with newer, more efficient systems. The logistical challenges, operational disruptions, and the need for specialized equipment and skilled labor during retrofitting projects can add substantial costs and time, thereby restraining the market's growth in mature industrial regions with extensive aging infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | Short to Medium-term |

| High Initial Installation and Material Costs for Advanced Solutions | -0.7% | Global, particularly developing regions | Short to Medium-term |

| Challenges in Retrofitting Existing Infrastructure | -0.5% | North America, Europe | Medium to Long-term |

Pipeline Thermal Insulation Material Market Opportunities Analysis

A significant opportunity within the Pipeline Thermal Insulation Material market lies in the continuous development and commercialization of advanced, high-performance, and sustainable insulation materials. With increasing global emphasis on environmental protection and resource efficiency, there is a burgeoning demand for eco-friendly insulation solutions, such as bio-based materials, recyclable foams, and those with low environmental impact throughout their lifecycle. This drive for sustainability opens avenues for research and development, allowing manufacturers to innovate and introduce next-generation products that not only offer superior thermal performance but also align with circular economy principles, attracting investments and market share.

The expansion of district heating and cooling networks across urban and industrial areas presents another substantial opportunity. As cities worldwide strive to enhance energy efficiency and reduce carbon footprints, district energy systems are gaining traction. These extensive networks of insulated pipelines require vast quantities of high-quality thermal insulation to minimize heat loss during distribution. This trend is particularly strong in Europe and certain parts of Asia, where government initiatives and urban development plans are actively promoting the adoption of centralized heating and cooling solutions, creating a consistent and growing demand for pipeline insulation materials.

Furthermore, the burgeoning liquefied natural gas (LNG) and hydrogen infrastructure projects globally offer a lucrative niche for specialized cryogenic insulation materials. The safe and efficient transportation of LNG and, increasingly, hydrogen requires insulation systems capable of performing under extremely low temperatures, ensuring product integrity and preventing significant boil-off losses. As the world transitions towards cleaner energy sources, the investment in and expansion of these critical infrastructures will intensify, driving a focused demand for highly specialized and technically advanced cryogenic insulation solutions, presenting a premium market segment for innovation and growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable and Eco-Friendly Insulation Materials | +1.0% | Global, particularly Europe | Medium to Long-term |

| Expansion of District Heating & Cooling Networks | +0.9% | Europe, North America, East Asia | Medium to Long-term |

| Growth in LNG and Hydrogen Infrastructure | +0.8% | North America, Asia Pacific, Middle East | Medium to Long-term |

Pipeline Thermal Insulation Material Market Challenges Impact Analysis

One significant challenge confronting the Pipeline Thermal Insulation Material market is navigating the complex and often disparate regulatory landscape across different regions and industries. Adherence to a multitude of safety standards, environmental regulations, and energy efficiency mandates can be particularly challenging for manufacturers and installers operating on a global scale. These varying compliance requirements necessitate product customization, extensive testing, and significant investments in research and development to ensure materials meet specific regional certifications and performance benchmarks, thereby adding to operational costs and potentially slowing market entry or expansion.

Maintaining the long-term performance and integrity of insulation materials in harsh operating environments, such as those exposed to extreme temperatures, chemical corrosion, UV radiation, or mechanical stress, presents another critical challenge. While materials are designed for durability, prolonged exposure to severe conditions can lead to degradation, reduced thermal efficiency, and even structural failure, necessitating costly repairs or premature replacements. Developing and consistently producing insulation solutions that can withstand these demanding conditions throughout their intended lifespan without significant compromise remains a continuous technological and material science challenge for the industry.

Furthermore, the specialized nature of advanced insulation materials often requires skilled labor for proper installation and maintenance, creating a challenge in terms of workforce availability and training. The lack of adequately trained professionals capable of handling and applying complex insulation systems can lead to inefficient installations, compromised performance, and increased project timelines and costs. This skill gap is particularly evident in rapidly developing regions where industrial expansion outpaces the growth of a specialized technical workforce, underscoring the need for greater investment in training and certification programs to support market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Diverse and Evolving Regulatory Standards | -0.6% | Global | Short to Medium-term |

| Maintaining Performance in Harsh and Extreme Operating Environments | -0.5% | Global, particularly industrial zones | Long-term |

| Shortage of Skilled Labor for Installation and Maintenance | -0.4% | Developing Economies, Remote Areas | Short to Medium-term |

Pipeline Thermal Insulation Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Pipeline Thermal Insulation Material market, offering a detailed segmentation by material type, application, and geographical regions. It thoroughly examines market dynamics, including key drivers, restraints, opportunities, and challenges influencing market growth from 2025 to 2033. The report also features an extensive competitive landscape assessment, profiling leading market players and analyzing their strategies to provide a holistic view of the industry's current state and future prospects. It serves as a vital resource for stakeholders seeking strategic insights and data-driven decision-making in this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.5 Billion |

| Market Forecast in 2033 | USD 11.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Insulation Solutions, Premier Thermal Systems, Advanced Material Composites, Energy Efficiency Products, Thermal Guard Innovations, Pipeline Protection Group, InsulatePro, EcoThermal Solutions, Future Insulation Technologies, Core Heat Management, Superior Insulation Materials, Petrochem Insulators, Industrial Thermal Defense, Green Shield Technologies, Optimized Flow Solutions, Thermal Efficiency Group, Nexus Insulation Systems, Alpha Thermal Coatings, Quantum Thermal Solutions, Elite Pipe Insulation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pipeline Thermal Insulation Material market is meticulously segmented to provide a granular view of its diverse components and their respective contributions to overall market dynamics. This segmentation allows for a precise understanding of material preferences, application-specific demands, and regional consumption patterns, aiding stakeholders in identifying high-growth areas and tailoring their strategies accordingly. The primary segmentation dimensions include material type, which details the various compositions used for insulation, and application, which outlines the key industries and sectors utilizing these materials for their pipeline networks.

The material type segment encompasses a wide array of insulation compositions, each offering distinct thermal properties, durability, and cost-effectiveness tailored to specific operational requirements. From traditional options like polyurethane foam and mineral wool to advanced materials such as aerogels and elastomeric foams, this segmentation highlights the technological evolution and material innovations shaping the market. Understanding the demand for each material type is crucial for manufacturers to optimize production and for end-users to select the most appropriate insulation for their particular pipeline systems, considering factors like temperature range, environmental conditions, and installation methods.

The application segment delineates the primary industries that are significant consumers of pipeline thermal insulation materials. This includes critical sectors such as oil & gas, chemicals & petrochemicals, power generation, and the burgeoning district heating & cooling networks. Analyzing demand across these applications provides insights into the key drivers and specific needs of each industry, revealing opportunities for specialized product development and market penetration. The diversity of applications underscores the essential role of thermal insulation in ensuring energy efficiency, operational safety, and process integrity across a broad spectrum of industrial activities globally.

- By Material Type:

- Polyurethane Foam

- Mineral Wool

- Fiberglass

- Calcium Silicate

- Aerogels

- Cellular Glass

- Perlite

- Elastomeric Foam

- Other Advanced Materials

- By Application:

- Oil & Gas

- Chemicals & Petrochemicals

- Power Generation

- District Heating & Cooling

- Food & Beverage Processing

- Water & Wastewater Management

- Other Industrial Applications

Regional Highlights

- Asia Pacific: This region is poised to be the dominant and fastest-growing market for Pipeline Thermal Insulation Material, primarily driven by rapid industrialization, extensive infrastructure development projects, and increasing investments in the oil & gas, chemical, and power generation sectors, particularly in China, India, and Southeast Asian countries. The growing energy demand and emphasis on energy efficiency in these economies are strong catalysts.

- Europe: Characterized by stringent energy efficiency regulations and a strong focus on reducing carbon emissions, Europe represents a mature yet continually growing market. The region's extensive district heating and cooling networks, coupled with ongoing efforts to upgrade aging industrial infrastructure and transition towards sustainable energy systems, ensure a steady demand for high-performance and eco-friendly insulation solutions.

- North America: With a significant installed base of oil & gas pipelines and an increasing focus on industrial energy efficiency, North America is a key market. Investments in modernizing existing infrastructure, the expansion of LNG export capabilities, and a push for sustainable industrial practices contribute to the demand for advanced thermal insulation materials, alongside robust R&D activities for innovative solutions.

- Middle East & Africa (MEA): This region is experiencing substantial growth propelled by massive investments in oil & gas exploration, production, and transportation infrastructure. The need for efficient thermal management in extreme climatic conditions and large-scale industrial projects across the Gulf Cooperation Council (GCC) countries drives demand for durable and high-temperature insulation materials, positioning MEA as a rapidly expanding market.

- Latin America: Growth in Latin America is primarily driven by the expansion of its oil & gas sector, including offshore drilling and pipeline projects. Countries like Brazil, Mexico, and Argentina are investing in energy infrastructure, which in turn fuels the demand for pipeline insulation to ensure operational safety and energy efficiency, albeit with varying paces across the diverse economies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pipeline Thermal Insulation Material Market.- Global Insulation Solutions

- Premier Thermal Systems

- Advanced Material Composites

- Energy Efficiency Products

- Thermal Guard Innovations

- Pipeline Protection Group

- InsulatePro

- EcoThermal Solutions

- Future Insulation Technologies

- Core Heat Management

- Superior Insulation Materials

- Petrochem Insulators

- Industrial Thermal Defense

- Green Shield Technologies

- Optimized Flow Solutions

- Thermal Efficiency Group

- Nexus Insulation Systems

- Alpha Thermal Coatings

- Quantum Thermal Solutions

- Elite Pipe Insulation

Frequently Asked Questions

Analyze common user questions about the Pipeline Thermal Insulation Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is pipeline thermal insulation material and why is it important?

Pipeline thermal insulation material is a specialized substance or system applied to industrial and commercial pipelines to minimize heat transfer between the pipe's contents and its surroundings. Its importance lies in maintaining process temperatures, enhancing energy efficiency by preventing heat loss or gain, ensuring operational safety by protecting personnel from extreme temperatures, and preventing condensation or freezing of pipeline contents, thereby optimizing system performance and reducing operational costs.

What are the primary types of pipeline thermal insulation materials?

The primary types of pipeline thermal insulation materials include traditional options like polyurethane foam, mineral wool, fiberglass, and calcium silicate, as well as advanced materials such as aerogels, cellular glass, perlite, and elastomeric foams. Each material offers distinct thermal conductivity, temperature resistance, and durability characteristics, making them suitable for various applications based on specific operational requirements and environmental conditions.

Which industries are the major consumers of pipeline thermal insulation?

Major consumers of pipeline thermal insulation materials are industries that heavily rely on fluid or gas transportation and require precise temperature control or energy conservation. These include the oil & gas industry (for crude oil, natural gas, and refined products), chemicals & petrochemicals (for various reagents and products), power generation (for steam and hot water lines), and district heating & cooling networks. Other notable consumers include food & beverage processing and water & wastewater management sectors.

How do advancements in material science impact this market?

Advancements in material science significantly impact the market by leading to the development of higher-performance, more durable, and increasingly sustainable insulation materials. Innovations such as aerogels, capable of ultralow thermal conductivity, and bio-based, recyclable foams are enhancing efficiency, reducing environmental footprint, and extending product lifespans. These advancements enable solutions for more extreme temperatures, harsh environments, and offer improved cost-effectiveness over the product's lifecycle, driving market growth and adoption.

What are the key factors driving the growth of the pipeline thermal insulation market?

The key factors driving the growth of the pipeline thermal insulation market include the escalating global demand for energy efficiency and conservation, stringent environmental regulations aimed at reducing carbon emissions, significant investments in new industrial infrastructure (especially in oil & gas, chemicals, and power generation), and the continuous technological advancements in insulation material development. The expansion of district heating and cooling networks and the growth in LNG and hydrogen infrastructure also contribute substantially to market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted