Phosphoric Acid Market

Phosphoric Acid Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709813 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Phosphoric Acid Market Size

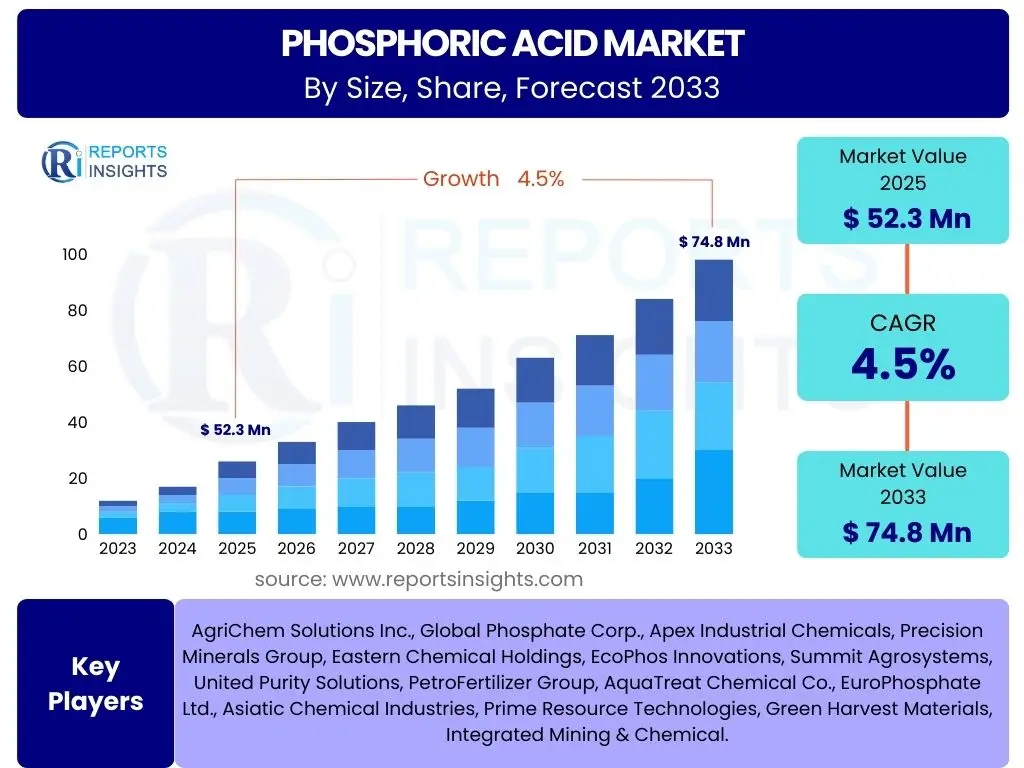

According to Reports Insights Consulting Pvt Ltd, The Phosphoric Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 52.3 Billion in 2025 and is projected to reach USD 74.8 Billion by the end of the forecast period in 2033.

Key Phosphoric Acid Market Trends & Insights

Users frequently inquire about the evolving landscape of the Phosphoric Acid market, seeking clarity on demand drivers, innovative applications, and shifts in production methodologies. The market is witnessing a significant drive towards enhanced sustainability in production processes, alongside a growing emphasis on high-purity grades for specialized applications. Furthermore, the interplay of geopolitical factors with raw material supply chains is a recurring concern, highlighting the market's sensitivity to global economic and political stability.

There is also considerable interest in how technological advancements are shaping the industry, particularly in improving efficiency and reducing environmental impact. The expansion of downstream industries such as food and beverage, and water treatment, continues to create new avenues for market growth. These trends collectively underscore a dynamic market that is both resilient to external pressures and adaptable to emerging consumer and industrial demands.

- Escalating demand for phosphate fertilizers driven by global food security imperatives and agricultural intensification.

- Increasing application in the food and beverage industry as an acidulant, preservative, and flavor enhancer.

- Growing adoption in industrial sectors, including water treatment, metal surface treatment, and detergents.

- Technological advancements aimed at improving production efficiency and reducing the environmental footprint of phosphoric acid manufacturing.

- Shift towards higher purity grades to cater to specialized applications in pharmaceuticals and electronic chemicals.

- Emphasis on sustainable production practices, including recycling and utilization of by-products.

- Impact of fluctuating raw material prices (phosphate rock, sulfur) on production costs and market stability.

- Regional shifts in production capacity and consumption patterns, particularly with rapid industrialization in emerging economies.

AI Impact Analysis on Phosphoric Acid

Users are increasingly curious about the transformative potential of Artificial Intelligence (AI) across industrial sectors, including the Phosphoric Acid market. Key questions revolve around AI's ability to optimize complex chemical processes, enhance operational efficiency, and mitigate environmental risks inherent in phosphoric acid production. There is a strong expectation that AI could revolutionize aspects such as predictive maintenance, quality control, and supply chain management, leading to significant cost reductions and improved product consistency.

However, concerns also exist regarding the initial investment required for AI implementation, data privacy, and the need for specialized skills to manage these advanced systems. Stakeholders are keen to understand how AI can contribute to more sustainable manufacturing by optimizing resource usage and minimizing waste. The consensus points towards AI being a critical enabler for future competitiveness and environmental stewardship within the phosphoric acid industry.

- Optimized Production Processes: AI algorithms can analyze vast datasets from manufacturing plants to optimize reaction conditions, energy consumption, and raw material utilization, leading to higher yields and reduced operational costs.

- Predictive Maintenance: AI-powered systems can monitor equipment health in real-time, predicting potential failures before they occur, thereby minimizing downtime and extending the lifespan of machinery used in phosphoric acid production.

- Enhanced Quality Control: AI vision systems and machine learning models can detect impurities and inconsistencies in phosphoric acid more accurately and rapidly than traditional methods, ensuring adherence to strict purity standards for various applications.

- Supply Chain Optimization: AI can forecast demand, manage inventory, and optimize logistics, leading to more efficient raw material procurement (phosphate rock, sulfur) and finished product distribution, reducing lead times and transportation costs.

- Environmental Monitoring and Compliance: AI tools can continuously monitor emissions and waste output, helping manufacturers stay within regulatory limits and identify areas for environmental impact reduction, such as wastewater treatment optimization.

- Research and Development Acceleration: AI can rapidly simulate molecular interactions and predict material properties, significantly accelerating the development of new phosphoric acid derivatives or more sustainable production methods.

Key Takeaways Phosphoric Acid Market Size & Forecast

User queries regarding the Phosphoric Acid market's future often center on identifying the most critical insights from its growth trajectory and projected market size. A paramount takeaway is the consistent and robust growth driven primarily by the agriculture sector's insatiable demand for fertilizers, fueled by a burgeoning global population and the necessity for increased food production. This foundational demand provides a strong underpinning for the market's stability and expansion.

Furthermore, the diversification of applications into high-value sectors such as food & beverages, water treatment, and specialty chemicals signals significant opportunities for market players to innovate and capture new revenue streams. The market forecast also highlights the growing importance of emerging economies, particularly in Asia Pacific, as key consumption hubs and potential areas for capacity expansion, which will shape future investment decisions and competitive landscapes. Overall, the market demonstrates resilience and adaptability, with strategic shifts towards sustainability and technological integration becoming increasingly vital for long-term success.

- The global phosphoric acid market is poised for steady growth, driven by fundamental demands from the agricultural sector for fertilizer production.

- Diversification into non-fertilizer applications, particularly in the food and beverage and industrial sectors, contributes significantly to market resilience and expansion.

- Asia Pacific is expected to remain the dominant and fastest-growing region, owing to rapid industrialization, increasing agricultural output, and rising population densities.

- Technological advancements in production processes, aiming for higher efficiency and lower environmental impact, are crucial for sustainable market development.

- Volatile raw material prices and stringent environmental regulations represent ongoing challenges that require strategic adaptation and investment in advanced manufacturing techniques.

- The market forecast underscores opportunities for companies investing in research and development for new applications and eco-friendly production methods.

Phosphoric Acid Market Drivers Analysis

The global phosphoric acid market is primarily propelled by the ever-increasing demand from the agriculture sector, which is grappling with the challenge of feeding a rapidly growing world population. Phosphoric acid is a critical component in the production of phosphate fertilizers, essential for enhancing crop yields and ensuring food security. As arable land diminishes and soil nutrient depletion becomes a global concern, the reliance on high-quality fertilizers, and consequently phosphoric acid, intensifies. This fundamental demand underpins a significant portion of the market's sustained growth.

Beyond agriculture, the expansion of the food and beverage industry, particularly in developing economies, serves as another robust driver. Phosphoric acid is widely used as an acidulant, flavor enhancer, and preservative in various food products and soft drinks, contributing to its stable demand. Additionally, the industrial sector's continuous need for phosphoric acid in applications such as water treatment chemicals, detergents, and metal surface treatments further broadens its market base. These diverse applications insulate the market from over-reliance on a single end-use sector, contributing to its overall stability and growth trajectory.

Moreover, global urbanization and industrialization trends lead to increased water treatment requirements and greater consumption of consumer goods containing phosphoric acid derivatives. The push for improved infrastructure and manufacturing capabilities in emerging regions directly translates to higher demand for industrial-grade phosphoric acid. This confluence of agricultural necessity, food industry expansion, and broad industrial applications collectively creates a strong impetus for the phosphoric acid market's consistent upward trend.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Phosphate Fertilizers | +1.8% | Global, particularly APAC & Latin America | Long-term (2025-2033) |

| Growth in Food and Beverage Industry | +1.1% | Global, especially emerging economies | Medium to Long-term (2025-2033) |

| Rising Industrial Applications (e.g., Water Treatment, Detergents) | +0.9% | North America, Europe, APAC | Medium to Long-term (2025-2033) |

| Expanding Chemical Processing Sector | +0.4% | China, India, Southeast Asia | Medium-term (2025-2029) |

| Population Growth & Food Security Concerns | +0.3% | Africa, South Asia | Long-term (2025-2033) |

Phosphoric Acid Market Restraints Analysis

The phosphoric acid market faces significant restraints primarily stemming from the volatility of raw material prices. Phosphate rock and sulfur are key inputs in the production of phosphoric acid, and their prices are subject to global supply-demand dynamics, geopolitical tensions, and extraction costs. Fluctuations in these raw material costs directly impact the profitability of phosphoric acid manufacturers, leading to price instability in the end-product market and making long-term strategic planning challenging for market players. This economic sensitivity can deter new investments and hinder market expansion.

Environmental regulations and concerns over pollution also impose considerable restraints on the market. The production of phosphoric acid, particularly via the wet process, generates large quantities of phosphogypsum, a byproduct that is difficult to manage and can contain radioactive elements. Stricter environmental protection laws concerning industrial waste disposal, air emissions, and water pollution increase operational costs for manufacturers, requiring substantial investments in advanced treatment technologies. Non-compliance can lead to hefty fines and operational shutdowns, thereby limiting production capacity and market growth, especially in regions with stringent environmental policies like Europe and North America.

Furthermore, the high energy consumption inherent in phosphoric acid production processes, particularly for the thermal method, contributes to operational expenses and environmental concerns. Rising energy prices globally can significantly escalate production costs, making the product less competitive. The market also contends with the availability of alternative chemicals for certain applications, such as organic acids in the food industry or other water treatment agents, which can exert competitive pressure and limit phosphoric acid's market penetration in specific niches. These combined factors necessitate continuous innovation and adaptation from market participants to navigate the restraining forces effectively.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Phosphate Rock, Sulfur) | -1.5% | Global, particularly import-dependent regions | Medium to Long-term (2025-2033) |

| Stringent Environmental Regulations and Waste Disposal Issues | -1.2% | Europe, North America, increasingly APAC | Long-term (2025-2033) |

| High Energy Consumption in Production | -0.8% | Global | Medium-term (2025-2029) |

| Supply Chain Disruptions & Geopolitical Instability | -0.6% | Global, especially trade-sensitive regions | Short to Medium-term (2025-2027) |

| Competition from Alternative Chemicals | -0.4% | Developed markets (e.g., Specialty chemicals) | Long-term (2025-2033) |

Phosphoric Acid Market Opportunities Analysis

Significant opportunities exist in the phosphoric acid market, primarily driven by the continuous innovation in developing new applications and higher-value derivatives. As industries evolve, the unique chemical properties of phosphoric acid are being leveraged in emerging sectors such as specialty chemicals for battery production, flame retardants, and advanced materials. Research and development efforts focused on creating these niche, high-purity products can open up substantial new revenue streams, moving beyond traditional fertilizer and food applications. This diversification allows manufacturers to tap into markets with less price sensitivity and higher growth potential.

Another major opportunity lies in the global shift towards sustainable and eco-friendly production methods. With increasing environmental consciousness and stricter regulations, there is a growing demand for "green" phosphoric acid produced with lower energy consumption, reduced waste, and minimal environmental impact. Investing in advanced technologies like solvent extraction or membrane separation for phosphoric acid purification, or developing processes that better utilize phosphogypsum, can provide a competitive edge. Companies that proactively adopt sustainable practices can attract environmentally conscious customers and secure their social license to operate, particularly in regions with strong environmental policies.

Moreover, the industrialization and agricultural growth in emerging economies, particularly in Asia Pacific, Latin America, and Africa, present vast untapped market potential. These regions are experiencing rapid population growth, increasing food demand, and expanding manufacturing sectors, all of which necessitate higher consumption of phosphoric acid. Companies that can strategically establish or expand their presence in these markets, potentially through localized production or strong distribution networks, stand to benefit from significant long-term growth. The ongoing global effort to improve food security and agricultural productivity in these regions will continue to drive demand for phosphate fertilizers, creating a robust and sustained market opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of New High-Value Applications (e.g., Batteries, Electronics) | +1.3% | Global, especially developed economies | Long-term (2027-2033) |

| Focus on Sustainable and Eco-friendly Production Methods | +1.0% | Europe, North America, progressive APAC countries | Medium to Long-term (2025-2033) |

| Growth in Emerging Economies (Agriculture & Industrialization) | +0.9% | APAC, Latin America, Africa | Long-term (2025-2033) |

| Increased Demand for Technical and Food Grade Phosphoric Acid | +0.7% | Global | Medium-term (2025-2030) |

| Recycling and Recovery of Phosphoric Acid from Waste Streams | +0.5% | Europe, Japan, South Korea | Long-term (2029-2033) |

Phosphoric Acid Market Challenges Impact Analysis

The phosphoric acid market faces significant challenges, particularly related to the management of its environmental footprint and waste byproducts. The production process, especially the wet method, generates large quantities of phosphogypsum, a radioactive waste material that requires extensive and costly disposal. Increasing environmental scrutiny and public demand for sustainable industrial practices necessitate substantial investments in waste treatment technologies and research into alternative disposal or utilization methods. Failure to effectively manage this challenge can lead to regulatory penalties, reputational damage, and limits on operational expansion, posing a substantial hurdle for manufacturers globally.

Another persistent challenge is maintaining a stable and cost-effective supply of raw materials, primarily high-grade phosphate rock and sulfur. Phosphate rock reserves are geographically concentrated, leading to supply chain vulnerabilities and geopolitical risks that can disrupt availability and drive up prices. The global nature of the supply chain also exposes the market to macroeconomic fluctuations, trade policies, and logistics issues, making it difficult for manufacturers to ensure consistent and affordable input costs. This uncertainty in raw material sourcing directly impacts production planning, pricing strategies, and ultimately, market competitiveness.

Furthermore, intense market competition and pricing pressures, particularly in mature markets, present an ongoing challenge. With numerous established players and increasing consolidation, maintaining market share often involves aggressive pricing strategies, which can erode profit margins. The capital-intensive nature of phosphoric acid production acts as a barrier to entry, but existing overcapacity in some regions can lead to downward pressure on prices. Additionally, the need for continuous technological upgrades to enhance efficiency and meet evolving environmental standards demands significant capital expenditure, adding to the operational challenges faced by industry participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Impact and Phosphogypsum Waste Management | -1.4% | Global, particularly highly regulated regions | Long-term (2025-2033) |

| Securing Stable and Cost-Effective Raw Material Supply | -1.1% | Global, especially import-reliant nations | Medium to Long-term (2025-2033) |

| Intense Competition and Pricing Pressures | -0.9% | Mature markets (North America, Europe, China) | Medium-term (2025-2030) |

| High Capital Investment for Production Facilities & Upgrades | -0.7% | Global | Long-term (2025-2033) |

| Energy Cost Volatility and Sustainability Pressure | -0.5% | Global | Short to Medium-term (2025-2028) |

Phosphoric Acid Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Phosphoric Acid Market, covering market size estimations, historical data, and future growth projections from 2025 to 2033. It meticulously examines key market drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope includes a detailed segmentation analysis by application, type, grade, and purity, offering granular insights into various market sub-segments. Furthermore, the report delves into regional market dynamics, highlighting key growth areas and competitive landscapes across major geographical regions. It also profiles leading market players, offering a strategic overview of their operations and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 52.3 Billion |

| Market Forecast in 2033 | USD 74.8 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AgriChem Solutions Inc., Global Phosphate Corp., Apex Industrial Chemicals, Precision Minerals Group, Eastern Chemical Holdings, EcoPhos Innovations, Summit Agrosystems, United Purity Solutions, PetroFertilizer Group, AquaTreat Chemical Co., EuroPhosphate Ltd., Asiatic Chemical Industries, Prime Resource Technologies, Green Harvest Materials, Integrated Mining & Chemical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global phosphoric acid market is broadly segmented across several key dimensions, providing a granular view of its diverse applications and production methods. Understanding these segments is crucial for market participants to identify growth areas, tailor product offerings, and devise effective market entry strategies. Each segment addresses distinct industry needs, from large-scale agricultural demands to highly specialized industrial requirements.

The segmentation by application highlights the primary end-use industries driving demand, with fertilizers consistently representing the largest share. However, the expanding use in food & beverages, detergents, and water treatment signifies growing diversification. Segmentation by type differentiates between the two main production methods, each with distinct cost structures, purity levels, and environmental footprints. Further distinctions are made by grade and purity, reflecting the varying quality requirements for different applications, from industrial-grade bulk use to high-purity applications in pharmaceuticals and electronics.

This comprehensive segmentation allows for a detailed analysis of market dynamics within each category, revealing specific growth opportunities and competitive landscapes. It also enables stakeholders to track shifts in consumer and industrial preferences, technological advancements influencing production techniques, and regulatory changes impacting product specifications. Such detailed insights are instrumental for strategic planning and resource allocation in the phosphoric acid market.

- By Application: Fertilizers, Food & Beverages, Detergents, Water Treatment, Metal Treatment, Pharmaceuticals, Others.

- By Type: Wet Process Phosphoric Acid, Thermal Process Phosphoric Acid.

- By Grade: Food Grade, Technical Grade, Industrial Grade.

- By Purity: High Purity, Standard Purity.

Regional Highlights

- Asia Pacific (APAC): Dominates the global phosphoric acid market in terms of consumption and production volume, driven by burgeoning agricultural demands, rapid industrialization, and a vast population base in countries like China, India, and Southeast Asian nations. This region is expected to exhibit the fastest growth over the forecast period due to continued economic development and increasing investments in food production and infrastructure.

- North America: Represents a mature market with significant consumption in agriculture and diversified industrial applications, including food & beverages, and water treatment. The region is characterized by advanced production technologies and stringent environmental regulations, driving innovation towards more sustainable manufacturing processes and high-purity products.

- Europe: A key market with a strong focus on high-purity phosphoric acid for specialty applications, stringent environmental compliance, and continuous innovation in production efficiency. While agricultural demand is substantial, the region also emphasizes circular economy principles and sustainable sourcing, impacting market dynamics and technological adoption.

- Latin America: A significant consumer due to its robust agricultural sector, particularly in countries like Brazil and Argentina, where phosphate fertilizers are crucial for extensive farming operations. The region also holds considerable phosphate rock reserves, influencing its role in the global supply chain, with increasing local production for domestic and export markets.

- Middle East and Africa (MEA): Emerging as a crucial region due to abundant phosphate rock reserves, particularly in North Africa, which acts as a major global supplier. This region is witnessing growing domestic demand from expanding agricultural initiatives and industrial development, presenting opportunities for increased local processing and value addition of phosphoric acid.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Phosphoric Acid Market.- AgriChem Solutions Inc.

- Global Phosphate Corp.

- Apex Industrial Chemicals

- Precision Minerals Group

- Eastern Chemical Holdings

- EcoPhos Innovations

- Summit Agrosystems

- United Purity Solutions

- PetroFertilizer Group

- AquaTreat Chemical Co.

- EuroPhosphate Ltd.

- Asiatic Chemical Industries

- Prime Resource Technologies

- Green Harvest Materials

- Integrated Mining & Chemical

- Specialty Phosphates LLC

- Advanced Mineral Processing

- Global Fertilizers & Chemicals

- InnoPure Systems

- ChemTech Solutions

Frequently Asked Questions

What is phosphoric acid primarily used for?

Phosphoric acid is primarily used in the production of phosphate fertilizers, accounting for the largest share of its global consumption. It is also extensively used in the food and beverage industry as an acidulant and preservative, in detergents, water treatment chemicals, and metal surface treatments.

What are the main types of phosphoric acid available in the market?

The two main types of phosphoric acid available in the market are Wet Process Phosphoric Acid (WPA) and Thermal Process Phosphoric Acid (TPA). WPA is produced by acidulating phosphate rock with sulfuric acid and is primarily used in fertilizers, while TPA, produced by burning elemental phosphorus, offers higher purity for food, pharmaceutical, and specialty applications.

How do environmental regulations impact the phosphoric acid market?

Environmental regulations significantly impact the phosphoric acid market by increasing operational costs due to strict controls on waste disposal, particularly phosphogypsum, and emissions. This drives manufacturers to invest in advanced treatment technologies and more sustainable production methods, influencing market prices and production strategies.

Which region is expected to lead the phosphoric acid market growth?

The Asia Pacific (APAC) region is expected to lead the phosphoric acid market growth. This is primarily due to the region's rapidly growing population, increasing demand for food and agricultural products, extensive industrialization, and expansion of the food and beverage sector, particularly in countries like China and India.

What are the key drivers of the phosphoric acid market?

The key drivers of the phosphoric acid market include the rising global demand for phosphate fertilizers driven by agricultural intensification and food security concerns, the expanding use in the food and beverage industry, and the increasing applications in various industrial sectors such as water treatment, detergents, and metal surface treatment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted