Phosphonate Market

Phosphonate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705494 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

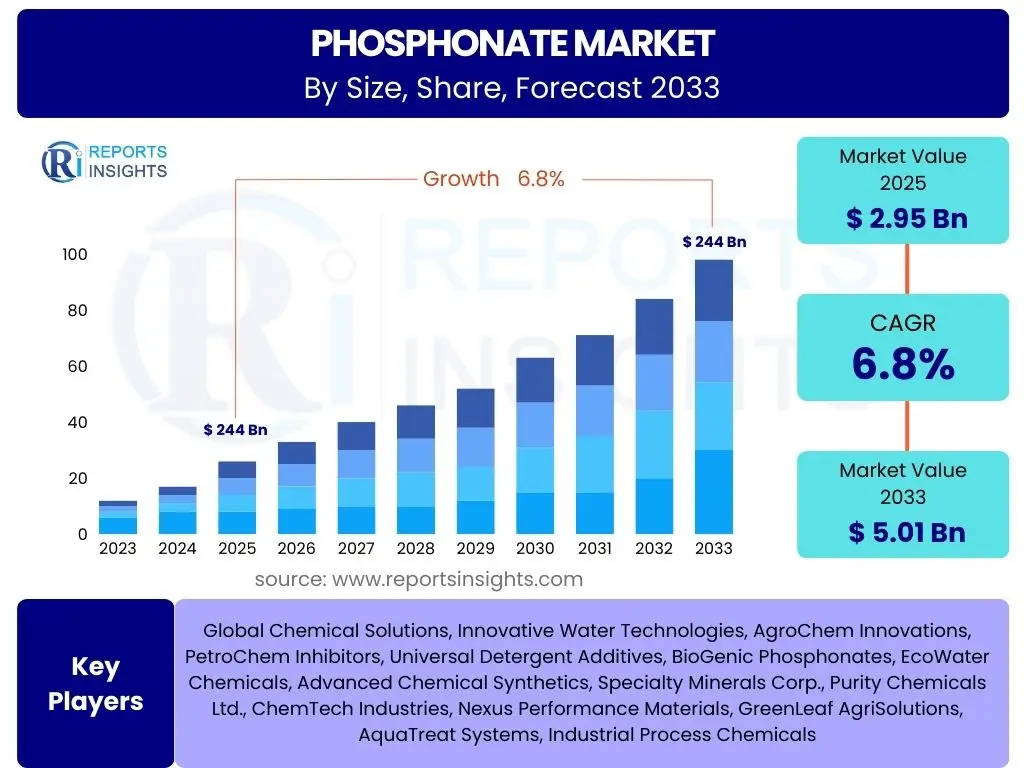

Phosphonate Market Size

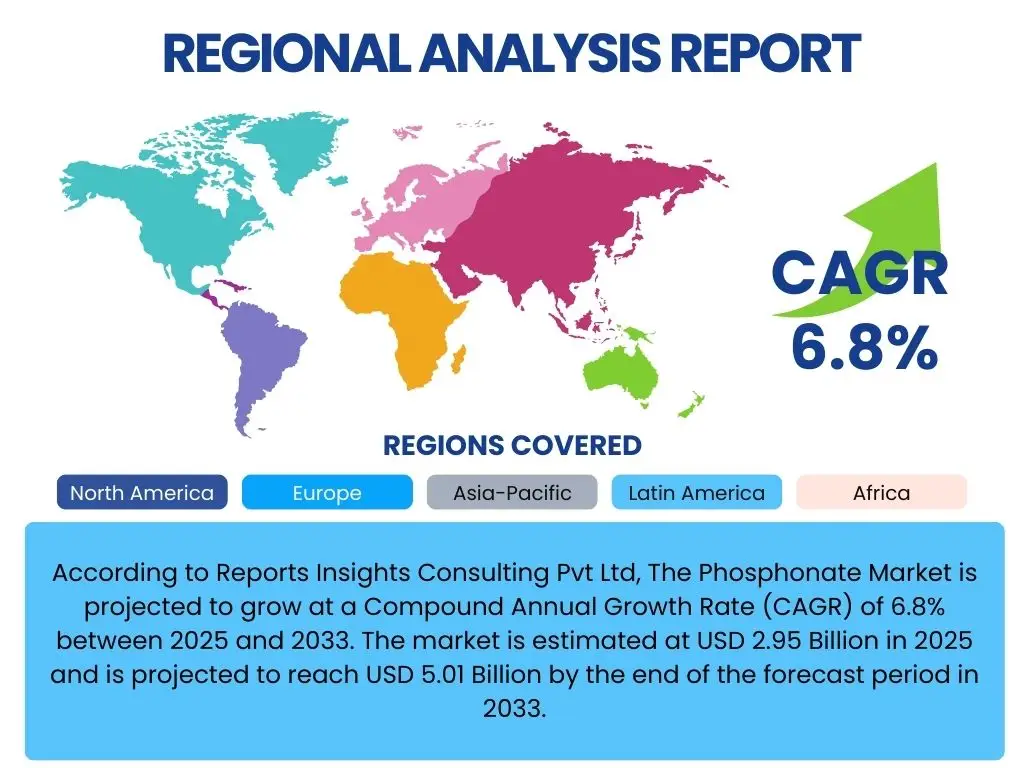

According to Reports Insights Consulting Pvt Ltd, The Phosphonate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.95 Billion in 2025 and is projected to reach USD 5.01 Billion by the end of the forecast period in 2033.

Key Phosphonate Market Trends & Insights

The phosphonate market is experiencing dynamic shifts driven by increasing demand across various industrial applications and growing emphasis on sustainability. Key trends include the expansion of water treatment infrastructure globally, which heavily relies on phosphonates as scale and corrosion inhibitors. Additionally, the agricultural sector's need for effective chelating agents and nutrient stabilizers is fueling demand for specific phosphonate types. Innovation in green chemistry and the development of more environmentally friendly phosphonate derivatives are emerging as critical trends, responding to stricter environmental regulations and consumer preferences for sustainable solutions. Furthermore, the market is seeing a rise in specialized phosphonate applications in areas such as oil and gas, pulp and paper, and detergents, each driven by unique performance requirements and operational efficiencies.

Another significant trend is the regional shift in manufacturing and consumption, with Asia Pacific emerging as a dominant market due to rapid industrialization and urbanization. This region is witnessing substantial investments in water management and industrial processing facilities, leading to increased phosphonate utilization. The market is also characterized by strategic collaborations and partnerships among key players aimed at expanding product portfolios and enhancing distribution networks. Digitalization in supply chain management and process optimization is further streamlining operations, contributing to market efficiency. Overall, the phosphonate market is evolving towards higher performance, greater specificity in applications, and improved environmental profiles to meet the diverse demands of end-use industries.

- Growing demand from the water treatment industry for scale and corrosion inhibition.

- Increasing adoption in agriculture as chelating agents and nutrient stabilizers.

- Focus on developing eco-friendly and biodegradable phosphonate derivatives.

- Expansion of applications in oil and gas, detergents, and pulp and paper sectors.

- Shift in manufacturing and consumption dominance towards Asia Pacific.

- Rise in strategic collaborations and partnerships among market participants.

- Integration of advanced analytics and digitalization in supply chain management.

AI Impact Analysis on Phosphonate

The integration of Artificial intelligence (AI) is poised to significantly impact the phosphonate market by revolutionizing various stages from research and development to manufacturing and supply chain management. AI algorithms can accelerate the discovery of novel phosphonate structures with enhanced properties, such as improved biodegradability or targeted performance in specific applications, by predicting molecular interactions and optimizing synthesis pathways. In manufacturing, AI-powered predictive maintenance can optimize production processes, reduce downtime, and improve efficiency by analyzing real-time operational data, leading to higher yields and reduced operational costs for phosphonate producers. Furthermore, AI can enhance quality control by identifying anomalies in product batches, ensuring consistent quality and adherence to strict industry standards.

Beyond production, AI can optimize complex supply chains by predicting demand fluctuations, managing inventory levels, and optimizing logistics, thereby reducing lead times and transportation costs for phosphonate distribution. AI-driven market analysis tools can provide deeper insights into market trends, competitive landscapes, and customer preferences, enabling manufacturers to make more informed strategic decisions regarding product development and market penetration. While the adoption of AI in the chemical industry, including phosphonates, is still in its nascent stages, its potential for driving innovation, improving efficiency, and fostering sustainable practices is substantial, paving the way for a more data-driven and agile industry landscape.

- Accelerated R&D for novel phosphonate compounds and formulations.

- Optimized manufacturing processes through predictive analytics and automation.

- Enhanced quality control and consistency in phosphonate production.

- Improved supply chain efficiency and logistics through demand forecasting.

- Data-driven market analysis for strategic business development.

- Potential for reduced environmental footprint through process optimization.

Key Takeaways Phosphonate Market Size & Forecast

The phosphonate market is on a robust growth trajectory, primarily driven by the escalating global demand for water treatment solutions and the expanding agricultural sector. The forecast indicates sustained expansion, underpinned by urbanization, industrial growth, and the imperative for effective water resource management. Key takeaways highlight the critical role phosphonates play in preventing scale and corrosion in industrial water systems, a necessity that intensifies with increasing industrial activity. The agricultural sector's growing emphasis on nutrient efficiency and soil health further solidifies the market's positive outlook, with phosphonates serving as vital chelating agents. This consistent demand across diverse end-use industries is a primary factor contributing to the projected market valuation and CAGR.

Moreover, technological advancements in phosphonate synthesis and the development of more environmentally benign products are crucial factors enabling this growth. While regulatory scrutiny remains a challenge, it also pushes innovation towards sustainable solutions, thereby opening new market opportunities. The market's resilience is further supported by its indispensable applications in niche sectors like oil and gas, and detergents, ensuring a broad and diversified demand base. Overall, the market is characterized by a balance of established applications and emerging innovative uses, indicating a healthy and expansive growth phase throughout the forecast period.

- Significant growth primarily driven by water treatment and agriculture.

- Projected steady increase in market size and CAGR through 2033.

- Indispensable role in industrial scale and corrosion inhibition.

- Critical application in enhancing nutrient uptake in agriculture.

- Innovation in sustainable phosphonate chemistries to meet regulatory demands.

- Diversified demand base across multiple industrial and consumer sectors.

Phosphonate Market Drivers Analysis

The global phosphonate market is primarily propelled by the increasing demand for water treatment chemicals across industrial and municipal sectors. As industrialization and urbanization accelerate, particularly in emerging economies, the need for efficient water management to prevent scale, corrosion, and fouling in pipes and equipment becomes paramount. Phosphonates, due to their superior sequestration and dispersing properties, are indispensable in these applications, ensuring the longevity and operational efficiency of water systems. Furthermore, the stringent environmental regulations concerning industrial wastewater discharge are compelling industries to adopt advanced treatment methods, thereby boosting the consumption of phosphonates.

Another significant driver is the expanding agricultural sector, where phosphonates are increasingly used as chelating agents to enhance nutrient availability and uptake in crops. They improve soil health and crop yield by preventing micronutrient deficiencies. The global focus on food security and sustainable agricultural practices further fuels this demand, particularly in regions with nutrient-deficient soils. Beyond these two major applications, the rising demand from sectors such as oil and gas, pulp and paper, and detergents, where phosphonates serve as dispersants, deflocculants, and sequestrants, also contributes substantially to market growth. The versatility and cost-effectiveness of phosphonates in these diverse applications ensure their continued market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrial Water Treatment Demand | +1.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Expansion of Agricultural Sector | +1.2% | Asia Pacific, Latin America, Europe | 2025-2033 |

| Increasing Oil & Gas Exploration and Production | +0.8% | Middle East & Africa, North America | 2026-2030 |

| Rising Demand for Detergents & Cleaning Agents | +0.7% | Global | 2025-2033 |

| Strict Environmental Regulations on Water Discharge | +0.9% | Europe, North America, China | 2025-2033 |

| Innovation in Product Formulations | +0.6% | Global | 2027-2033 |

| Infrastructure Development & Urbanization | +1.0% | Developing Economies (India, Brazil, Indonesia) | 2025-2033 |

Phosphonate Market Restraints Analysis

The phosphonate market faces several restraints that could potentially impede its growth. One primary concern is the increasing environmental scrutiny and regulatory pressures, particularly regarding the biodegradability and long-term environmental impact of certain phosphonate derivatives. Concerns about nutrient loading in water bodies, which can contribute to eutrophication, are leading to calls for more stringent controls on phosphonate usage and discharge. This is compelling manufacturers to invest heavily in research and development for more eco-friendly and readily biodegradable alternatives, which can increase production costs and potentially impact market pricing.

Another significant restraint is the availability and cost volatility of key raw materials used in phosphonate synthesis. Fluctuations in the prices of phosphorus, phosphoric acid, and other chemical precursors can directly impact the manufacturing costs, subsequently affecting the final product prices and profit margins for phosphonate producers. Additionally, the emergence of alternative chemistries for water treatment and other applications, such as biopolymers and other specialty chemicals, poses a competitive threat. While phosphonates offer distinct advantages, the continuous development of competitive substitutes could fragment the market and divert demand. Economic slowdowns or downturns in key end-use industries like manufacturing and construction can also lead to a decrease in demand for phosphonates, as these sectors are significant consumers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -1.0% | Europe, North America, East Asia | 2025-2033 |

| Volatility in Raw Material Prices | -0.7% | Global | 2025-2028 |

| Development of Alternative Chemistries | -0.6% | Global | 2028-2033 |

| Concerns over Eutrophication | -0.5% | Coastal Regions, Europe, North America | 2025-2030 |

| High Research & Development Costs for Green Alternatives | -0.4% | Global | 2025-2033 |

| Supply Chain Disruptions | -0.3% | Global | Short-term (Occasional) |

Phosphonate Market Opportunities Analysis

The phosphonate market presents significant opportunities for growth, primarily driven by the increasing global focus on sustainable water management and agricultural productivity. The escalating water scarcity issues worldwide necessitate advanced water treatment technologies, creating a vast market for phosphonates in industrial, municipal, and even residential applications. Opportunities exist in developing countries where new industrial parks and urban centers require substantial investment in water infrastructure. Moreover, the re-use and recycling of industrial wastewater offer a niche for phosphonates in specialized treatment processes, aligning with circular economy principles.

The burgeoning demand for high-performance and specialty phosphonates, particularly those with enhanced biodegradability and reduced environmental impact, represents a lucrative avenue for innovation. Companies investing in green chemistry and developing novel phosphonate structures that comply with stricter environmental standards will gain a competitive edge. Furthermore, the expansion of precision agriculture and the increasing adoption of efficient farming practices, such as drip irrigation, open up new applications for phosphonates as targeted nutrient delivery agents. Emerging markets in Latin America, Africa, and parts of Asia, characterized by rapid industrial growth and agricultural development, offer untapped potential for market penetration. Strategic collaborations and mergers and acquisitions can also enable market players to expand their geographical reach and product portfolios, capitalizing on these evolving opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Biodegradable Phosphonates | +1.3% | Global, particularly Europe and North America | 2026-2033 |

| Increasing Water Reuse and Recycling Initiatives | +1.0% | Globally, arid regions | 2025-2033 |

| Expansion in Emerging Economies (Water & Agri) | +1.1% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Advancements in Agricultural Technologies | +0.9% | Global | 2027-2033 |

| Niche Applications in Geothermal Energy and Mining | +0.5% | Regions with significant natural resources | 2028-2033 |

| Strategic Partnerships and Collaborations | +0.7% | Global | 2025-2030 |

Phosphonate Market Challenges Impact Analysis

The phosphonate market faces significant challenges, primarily centered around environmental concerns and the evolving regulatory landscape. The persistence of certain phosphonates in the environment and their potential contribution to eutrophication remain a key challenge, leading to stricter regulations and potential restrictions on their use in various applications. This pressure necessitates substantial investment in research and development for more environmentally benign alternatives, which can be costly and time-consuming, affecting market entry for new products and increasing operational expenses for existing manufacturers. Furthermore, ensuring compliance with diverse and often evolving regional and national environmental standards adds complexity to global operations and supply chains.

Another critical challenge is the intense competition within the market, both from established phosphonate producers and from alternative chemistries. This competition can lead to price erosion and reduced profit margins, especially for commodity-grade phosphonates. Maintaining a competitive edge requires continuous innovation, product differentiation, and efficient production processes. Moreover, disruptions in the global supply chain, such as raw material shortages, geopolitical tensions, or transport restrictions, can significantly impact production schedules and delivery, leading to increased costs and potential loss of market share. Educating end-users about the specific benefits and proper handling of various phosphonate types also remains an ongoing challenge, particularly in diverse and less regulated markets, affecting broader adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Regulations & Persistence Concerns | -1.2% | Europe, North America, Developed Asian Markets | 2025-2033 |

| Intense Market Competition & Price Pressure | -0.8% | Global | 2025-2033 |

| Raw Material Supply Chain Volatility | -0.6% | Global | Short to Mid-term |

| Development & Adoption of Substitutes | -0.5% | Global | 2028-2033 |

| High Capital Investment for Sustainable Production | -0.4% | Global | 2025-2030 |

| Public Perception and Awareness | -0.3% | Developed Countries | Long-term |

Phosphonate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Phosphonate market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape from 2019 to 2033. It examines the key drivers, restraints, opportunities, and challenges influencing market growth, alongside an impact analysis of Artificial Intelligence on the industry. The report also includes current market size estimations and future projections, aiming to equip stakeholders with critical information for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 Billion |

| Market Forecast in 2033 | USD 5.01 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chemical Solutions, Innovative Water Technologies, AgroChem Innovations, PetroChem Inhibitors, Universal Detergent Additives, BioGenic Phosphonates, EcoWater Chemicals, Advanced Chemical Synthetics, Specialty Minerals Corp., Purity Chemicals Ltd., ChemTech Industries, Nexus Performance Materials, GreenLeaf AgriSolutions, AquaTreat Systems, Industrial Process Chemicals |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The phosphonate market is comprehensively segmented based on various critical parameters, including type, application, and end-use industry. This granular segmentation provides a detailed understanding of the market's structure and allows for targeted analysis of specific product categories and their respective demand drivers. The diversity of phosphonate types, each possessing unique properties, caters to a wide array of industrial and commercial needs, influencing their adoption across different sectors. Similarly, analyzing the market by application reveals the dominant end-uses that contribute most significantly to market revenue and growth. The end-use industry segmentation further delineates the consumption patterns and market potential within major economic sectors.

- By Type

- HEDP (1-Hydroxyethylidene-1,1-Diphosphonic Acid)

- ATMP (Amino Trimethylene Phosphonic Acid)

- DTPMP (Diethylene Triamine Penta Methylene Phosphonic Acid)

- EDTMP (Ethylene Diamine Tetra Methylene Phosphonic Acid)

- PBTC (2-Phosphonobutane-1,2,4-Tricarboxylic Acid)

- Other Phosphonates (e.g., BHMT, HDTMP, HPPA)

- By Application

- Water Treatment

- Cooling Water Systems

- Boilers

- Desalination

- Reverse Osmosis

- Detergents & Cleaners

- Dishwashing

- Laundry

- Industrial & Institutional Cleaning

- Oil & Gas

- Drilling Fluids

- Enhanced Oil Recovery

- Pipeline Inhibition

- Agriculture

- Fertilizers

- Pesticides

- Foliar Applications

- Pulp & Paper

- Bleaching

- Scale Control

- Textile & Dyes

- Dyeing Auxiliaries

- Scouring

- Other Applications (e.g., Metal Finishing, Pharmaceuticals)

- Water Treatment

- By End-Use Industry

- Industrial

- Commercial

- Residential

- Agricultural

- Institutional

Regional Highlights

- North America: This region maintains a significant share in the phosphonate market, driven by mature industrial sectors and stringent environmental regulations promoting advanced water treatment solutions. The oil and gas industry in the U.S. and Canada, along with robust agricultural practices, contributes substantially to demand. Innovation in sustainable chemistries and high investment in R&D also characterize this market.

- Europe: Europe is a key market, distinguished by its strong emphasis on environmental protection and sustainability. Strict REACH regulations and the push for biodegradable products are shaping the phosphonate market dynamics. Demand is consistent from industrial water treatment, detergent formulations, and a steadily evolving agricultural sector, particularly in countries like Germany, France, and the UK.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, increasing urbanization, and expanding infrastructure development, especially in China and India. The immense demand for water treatment in manufacturing, power generation, and municipal sectors, coupled with the growth of the agricultural industry, drives robust phosphonate consumption. Local manufacturing capabilities are also expanding to cater to regional demand.

- Latin America: This region is experiencing steady growth, largely due to ongoing industrial development, particularly in countries like Brazil and Mexico. The expanding mining, oil and gas, and agricultural sectors contribute significantly to the demand for phosphonates. Investments in improving water infrastructure and industrial processes are also stimulating market expansion.

- Middle East and Africa (MEA): The MEA market is primarily driven by extensive oil and gas activities and increasing investments in desalination plants to address water scarcity. Phosphonates are crucial for corrosion and scale inhibition in these demanding applications. Emerging industrial sectors and a growing focus on water resource management across the region are expected to bolster demand further.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Phosphonate Market.- Lanxess AG

- Italmatch Chemicals S.p.A.

- Solvay S.A.

- AkzoNobel N.V.

- Dow Chemical Company

- Kemira Oyj

- Aqualution Systems Ltd.

- Fosfitalia SpA

- Zschimmer & Schwarz GmbH & Co KG

- Changzhou Natron Chemical Co., Ltd.

- Shandong Taihe Chemicals Co., Ltd.

- Shandong Xintai Water Treatment Co., Ltd.

- Liaocheng City Xinglong Chemical Co., Ltd.

- Suzhou-Chem Co., Ltd.

- Bozhou Jishun Chemical Co., Ltd.

- Jiangsu Zhongsheng Chemical Co., Ltd.

- Hebei Huarun Chemical Co., Ltd.

- Yichang Sanxia Chemical Co., Ltd.

- Transpek Industry Ltd.

- Thermax Limited

Frequently Asked Questions

What are phosphonates primarily used for?

Phosphonates are predominantly used as scale and corrosion inhibitors in water treatment systems, including industrial cooling towers, boilers, and desalination plants. They are also widely applied in detergents, oil and gas, agriculture as chelating agents, and in textiles and pulp & paper industries.

What is the projected growth rate for the Phosphonate market?

The Phosphonate market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing demand across various industrial applications and agricultural sectors globally.

Which region is expected to lead the Phosphonate market growth?

Asia Pacific (APAC) is anticipated to be the fastest-growing region in the Phosphonate market due to rapid industrialization, urbanization, and significant investments in water infrastructure and agricultural development in countries like China and India.

What are the main drivers of the Phosphonate market?

Key drivers include the escalating demand for water treatment solutions in industrial and municipal sectors, the expanding agricultural industry requiring chelating agents, and increasing applications in the oil and gas and detergent sectors. Stringent environmental regulations also push demand for effective water management solutions.

Are there any environmental concerns associated with phosphonates?

Yes, some phosphonates have raised environmental concerns regarding their persistence in water systems and potential contribution to eutrophication. This has led to increased regulatory scrutiny and a growing market demand for more biodegradable and environmentally friendly phosphonate alternatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted