UV Ink Market

UV Ink Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709348 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

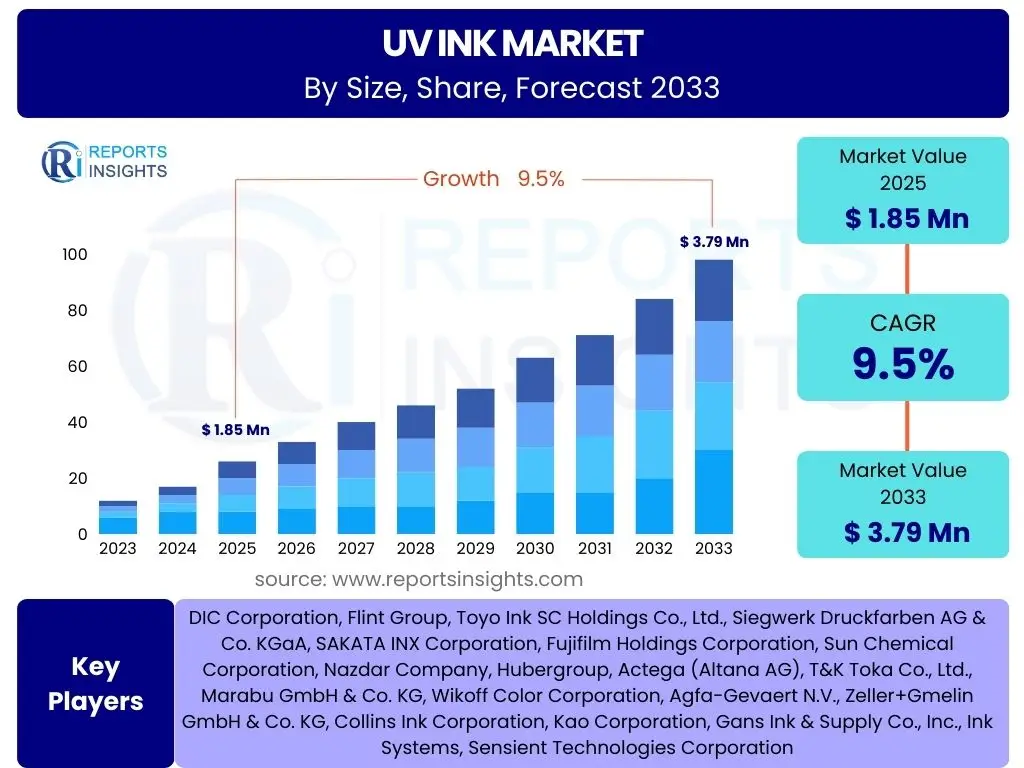

UV Ink Market Size

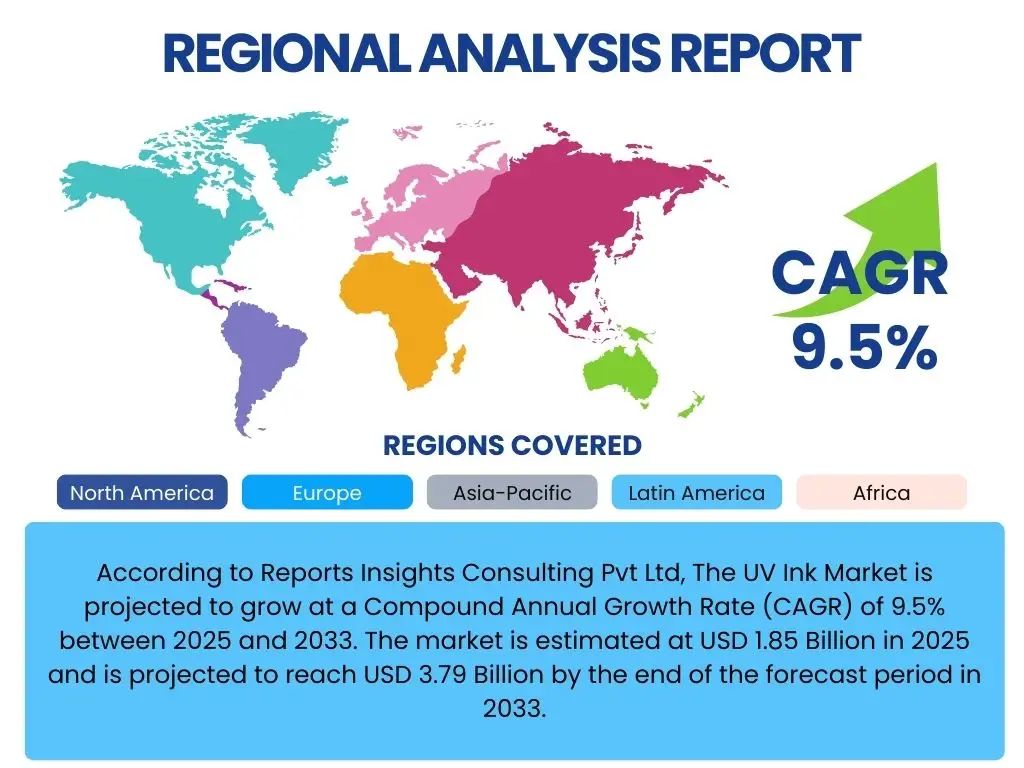

According to Reports Insights Consulting Pvt Ltd, The UV Ink Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.79 Billion by the end of the forecast period in 2033.

Key UV Ink Market Trends & Insights

Users frequently inquire about the evolving landscape of UV ink technology, focusing on innovations, sustainability efforts, and application-specific demands. Key themes revolve around the transition towards more eco-friendly formulations, the proliferation of digital printing technologies, and the expansion into specialized industrial applications. There is also significant interest in the benefits of UV LED curing over traditional UV mercury lamps, driven by energy efficiency and reduced heat generation.

Another area of user curiosity includes the integration of advanced functionalities within UV inks, such as improved adhesion to diverse substrates, enhanced scratch resistance, and the development of intelligent or smart inks. The market's trajectory is strongly influenced by global sustainability initiatives, stringent regulatory frameworks, and the continuous demand for high-quality, durable, and fast-curing printing solutions across various industries, including packaging, automotive, and consumer electronics.

- Shift towards UV LED curing technology due to energy efficiency and reduced environmental impact.

- Growing adoption in digital printing, offering flexibility, faster turnaround, and customization capabilities.

- Increasing demand for sustainable and low-VOC (Volatile Organic Compound) UV ink formulations.

- Expansion of UV ink applications in flexible packaging, labels, and industrial printing.

- Development of specialized UV inks for unique functional properties, such as high scratch resistance, chemical resistance, and outdoor durability.

- Integration of advanced materials for enhanced performance and broader substrate compatibility.

- Focus on automation and process optimization in UV printing workflows.

AI Impact Analysis on UV Ink

Common user questions regarding AI's impact on the UV Ink market center on its potential to revolutionize ink formulation, quality control, and manufacturing processes. Users are keen to understand how artificial intelligence and machine learning can optimize material selection, predict performance characteristics, and streamline production, thereby reducing costs and accelerating innovation cycles. The expectation is that AI will enable more precise and customized ink solutions, addressing specific application requirements with unprecedented accuracy.

Furthermore, there is considerable interest in AI's role in predictive maintenance for printing equipment, optimizing curing parameters, and enhancing supply chain efficiency for raw materials. The application of AI in data analysis can provide valuable insights into market trends, consumer preferences, and operational bottlenecks, allowing manufacturers to adapt quickly and strategically. This intelligent integration promises to elevate product quality, reduce waste, and foster a more responsive and efficient UV ink industry.

- AI-driven optimization of UV ink formulations, leading to faster development cycles and improved performance characteristics.

- Enhanced quality control through AI-powered vision systems for defect detection and color consistency.

- Predictive maintenance for UV printing and curing equipment, minimizing downtime and increasing operational efficiency.

- Supply chain optimization using AI algorithms to forecast demand, manage inventory, and source raw materials more effectively.

- Development of 'smart' UV inks with embedded functionalities, enabled by AI for material science innovation.

- Personalized ink solutions and custom color matching through AI-driven analytical tools.

- Automated process control in manufacturing, ensuring consistent product quality and reducing human error.

Key Takeaways UV Ink Market Size & Forecast

Users frequently seek concise insights into the primary drivers behind the UV Ink market's growth and its future trajectory. A key takeaway is the consistent robust expansion projected throughout the forecast period, primarily fueled by the accelerating adoption of digital printing technologies and the stringent regulatory environment promoting sustainable printing solutions. The market's upward trend is also significantly influenced by the increasing application across diverse end-use industries, including packaging, automotive, and electronics, all demanding high-performance, durable, and fast-curing ink solutions.

Another crucial insight is the strategic importance of technological advancements, particularly in UV LED curing, which offers substantial environmental and operational advantages over traditional methods. This technological evolution not only reduces energy consumption and VOC emissions but also expands the range of printable substrates, opening new revenue streams. The market's growth is therefore a confluence of technological innovation, environmental consciousness, and expanding industrial application, positioning UV inks as a critical component of modern printing and coating industries.

- Substantial market growth projected at a 9.5% CAGR, indicating a strong and expanding industry.

- Digital printing and packaging sectors are primary growth engines for UV ink demand.

- Sustainability regulations and environmental concerns are driving innovation towards eco-friendly UV ink formulations.

- UV LED curing technology is a significant catalyst for market expansion due to its efficiency and versatility.

- Emerging markets, particularly in Asia Pacific, are expected to contribute significantly to market size.

- Increasing adoption of UV inks in industrial and specialty applications underlines market diversification.

- Technological advancements in ink chemistry and curing equipment will continue to shape market dynamics.

UV Ink Market Drivers Analysis

The UV Ink market is significantly propelled by several robust drivers, primarily the burgeoning demand for high-quality, durable, and fast-curing printing solutions across various industries. The rapid expansion of digital printing technologies, offering flexibility, customization, and quicker turnaround times, has created a substantial need for inks that can keep pace with these advanced systems. UV inks, with their instant curing properties and excellent print quality, are ideally suited for this evolution, particularly in packaging, labels, and commercial printing sectors.

Furthermore, escalating environmental concerns and increasingly stringent regulations worldwide are compelling industries to seek more sustainable alternatives to solvent-based inks. UV inks, being nearly 100% solid and free from volatile organic compounds (VOCs), offer a compelling eco-friendly solution, reducing air pollution and workplace hazards. This regulatory push, combined with the operational benefits such as lower energy consumption associated with UV LED curing, positions UV inks as a preferred choice for environmentally conscious manufacturers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Digital Printing Technology | +2.5% | Global, particularly North America, Europe, APAC | Short to Mid-Term (2025-2029) |

| Rising Demand for Sustainable & Eco-friendly Inks | +2.0% | Global, with emphasis on Europe, North America | Mid to Long-Term (2027-2033) |

| Increasing Application in Packaging & Labels | +1.8% | Global, especially APAC and Latin America | Short to Mid-Term (2025-2030) |

| Technological Advancements in UV LED Curing | +1.5% | Global, all developed and emerging economies | Mid to Long-Term (2026-2033) |

| Demand for High-Performance & Durable Prints | +1.2% | Global, particularly industrial applications | Short to Mid-Term (2025-2029) |

UV Ink Market Restraints Analysis

Despite significant growth drivers, the UV Ink market faces several restraints that could impede its full potential. A primary concern is the relatively higher initial investment required for UV printing systems compared to conventional printing technologies. This includes the cost of specialized UV lamps (though LED options are becoming more affordable), and compatible printing presses, which can be a barrier for smaller businesses or those with limited capital, particularly in developing regions.

Another significant restraint involves the fluctuating prices and limited availability of certain raw materials, such as photoinitiators, monomers, and oligomers, which are crucial components in UV ink formulations. These materials are often petrochemical derivatives, making them susceptible to crude oil price volatility and supply chain disruptions. Furthermore, concerns regarding the potential health hazards associated with certain unreacted monomers or specific photoinitiators, although regulated, can sometimes create apprehension among end-users and require continuous innovation for safer formulations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment for UV Printing Equipment | -1.0% | Emerging Economies, SMEs Globally | Short to Mid-Term (2025-2030) |

| Volatility in Raw Material Prices & Supply | -0.8% | Global, all manufacturing regions | Short to Mid-Term (2025-2028) |

| Specific Health & Safety Concerns (e.g., skin irritation) | -0.5% | Europe, North America (due to stringent regulations) | Ongoing |

| Competition from Conventional Ink Technologies | -0.4% | Global, particularly in traditional print segments | Short Term (2025-2027) |

UV Ink Market Opportunities Analysis

The UV Ink market is ripe with opportunities for expansion and innovation, driven by evolving industrial demands and technological advancements. A key opportunity lies in the burgeoning market for 3D printing, where UV-curable resins and inks are fundamental to additive manufacturing processes. As 3D printing continues to expand beyond prototyping into industrial production across sectors like automotive, aerospace, and medical, the demand for specialized UV inks and photopolymers will experience significant growth.

Furthermore, emerging economies, particularly in Asia Pacific and Latin America, present substantial untapped market potential. Rapid industrialization, increasing consumer spending, and the growth of local manufacturing bases in these regions are fueling demand for advanced printing and coating solutions. As these economies prioritize sustainable manufacturing, the low-VOC profile of UV inks makes them an attractive option, opening new avenues for market penetration and regional expansion for manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into 3D Printing and Additive Manufacturing | +1.5% | Global, especially developed markets | Mid to Long-Term (2027-2033) |

| Untapped Potential in Emerging Economies | +1.2% | APAC, Latin America, Middle East & Africa | Mid to Long-Term (2026-2033) |

| Development of Novel Applications (e.g., flexible electronics, medical) | +1.0% | Global, R&D focused regions | Long-Term (2028-2033) |

| Customization and Personalization in Printing | +0.8% | Global, all consumer-driven industries | Short to Mid-Term (2025-2030) |

| Strategic Partnerships & Collaborations for Innovation | +0.7% | Global, among key industry players | Ongoing |

UV Ink Market Challenges Impact Analysis

The UV Ink market faces a unique set of challenges that require continuous adaptation and innovation from industry players. One significant challenge is the intense competition from established conventional ink technologies, which, despite their drawbacks, benefit from lower production costs and widespread existing infrastructure. While UV inks offer superior performance and environmental benefits, convincing a broad base of users to switch from long-standing, cost-effective conventional methods remains an uphill battle, particularly in price-sensitive segments.

Another critical challenge revolves around the increasingly stringent environmental regulations and health and safety standards that govern chemical compositions. Although UV inks are generally considered more eco-friendly, certain components, like specific photoinitiators or monomers, can face regulatory scrutiny due to potential toxicity or migratory properties, especially in food packaging applications. This necessitates continuous research and development to formulate safer, compliant inks without compromising performance, which can be resource-intensive and time-consuming for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental & Health Regulations | -0.9% | Europe, North America, expanding to APAC | Ongoing, Long-Term |

| Complexity in Formulation for Diverse Substrates | -0.7% | Global, specialty printing sectors | Mid-Term (2026-2031) |

| High R&D Investment for New Chemistries | -0.6% | Global, all major manufacturers | Ongoing |

| Disposal & Recycling Challenges of UV Printed Materials | -0.4% | Europe, North America, due to circular economy initiatives | Mid to Long-Term (2028-2033) |

| Need for Specialized Training & Expertise | -0.3% | Global, particularly in new adoption regions | Short to Mid-Term (2025-2029) |

UV Ink Market - Updated Report Scope

This updated report provides an exhaustive analysis of the global UV Ink market, encapsulating comprehensive insights into market size, growth trajectories, and intricate segmentations. It delivers a detailed examination of prevailing market trends, the impact of artificial intelligence, and a thorough assessment of market drivers, restraints, opportunities, and challenges. The report aims to equip stakeholders with critical data for strategic decision-making, offering a forward-looking perspective on market dynamics and competitive landscapes from 2025 to 2033, building upon historical data from 2019 to 2023.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.79 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DIC Corporation, Flint Group, Toyo Ink SC Holdings Co., Ltd., Siegwerk Druckfarben AG & Co. KGaA, SAKATA INX Corporation, Fujifilm Holdings Corporation, Sun Chemical Corporation, Nazdar Company, Hubergroup, Actega (Altana AG), T&K Toka Co., Ltd., Marabu GmbH & Co. KG, Wikoff Color Corporation, Agfa-Gevaert N.V., Zeller+Gmelin GmbH & Co. KG, Collins Ink Corporation, Kao Corporation, Gans Ink & Supply Co., Inc., Ink Systems, Sensient Technologies Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The UV Ink market is meticulously segmented to provide granular insights into its diverse components and applications. This segmentation analysis dissects the market based on various critical parameters, including the chemical composition of the inks, the specific curing technology employed, the end-use applications, and the industry verticals where these inks find utility. This detailed breakdown aids in understanding the specific drivers and trends influencing each sub-segment, offering a clearer picture of market dynamics and growth opportunities within specialized niches.

Understanding these segments is crucial for stakeholders to identify high-growth areas, develop targeted products, and formulate effective market entry strategies. For instance, the distinction between UV LED curable and conventional UV curable inks highlights the ongoing technological transition, while the application segments from packaging to 3D printing reveal the broad utility and innovation potential of UV inks. This comprehensive segmentation provides a foundational framework for analyzing market performance and predicting future trajectories.

- By Composition: Acrylates, Polyesters, Polyurethanes, Epoxies, and Others.

- By Curing Type: UV LED Curable Inks and Conventional UV Curable Inks (Mercury Lamp).

- By Application: Printing (Packaging, Labels, Commercial, Industrial, 3D Printing), Coatings (Wood, Plastic, Metal, Automotive, Optical Fibers), Adhesives, and Others (Medical Devices, Electronics).

- By End-Use Industry: Packaging (Food & Beverage, Pharma & Healthcare, Consumer Goods), Automotive, Electronics, Medical, Textile, Wood & Furniture, and Others.

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by rapid industrialization, expanding manufacturing bases, and increasing demand for packaging and digital printing in countries like China, India, Japan, and South Korea. This region also benefits from a growing middle-class population and increased consumer spending.

- North America: A mature market with significant adoption of advanced printing technologies and a strong focus on sustainable solutions. The presence of key market players and continuous R&D investments contribute to its substantial market share, particularly in industrial and specialty printing.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on eco-friendly printing solutions, driving the demand for low-VOC UV inks. Germany, the UK, France, and Italy are key contributors, with growth fueled by packaging, commercial printing, and automotive sectors.

- Latin America: Exhibiting steady growth, primarily driven by the expansion of the packaging industry and the increasing adoption of digital printing in countries like Brazil and Mexico. Economic development and foreign investments are stimulating market demand.

- Middle East and Africa (MEA): Emerging as a promising market due to infrastructure development, growing industrialization, and increased foreign direct investment. The UAE, Saudi Arabia, and South Africa are key markets, with demand primarily from the packaging and construction sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the UV Ink Market.- DIC Corporation

- Flint Group

- Toyo Ink SC Holdings Co., Ltd.

- Siegwerk Druckfarben AG & Co. KGaA

- SAKATA INX Corporation

- Fujifilm Holdings Corporation

- Sun Chemical Corporation

- Nazdar Company

- Hubergroup

- Actega (Altana AG)

- T&K Toka Co., Ltd.

- Marabu GmbH & Co. KG

- Wikoff Color Corporation

- Agfa-Gevaert N.V.

- Zeller+Gmelin GmbH & Co. KG

- Collins Ink Corporation

- Kao Corporation

- Gans Ink & Supply Co., Inc.

- Ink Systems

- Sensient Technologies Corporation

Frequently Asked Questions

Analyze common user questions about the UV Ink market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are UV inks and how do they differ from traditional inks?

UV inks are a type of ink that cure instantly when exposed to ultraviolet (UV) light, rather than drying through solvent evaporation or absorption. This differs from traditional inks, which often contain volatile organic compounds (VOCs) and require longer drying times, offering UV inks advantages in speed, durability, and environmental safety.

What are the primary applications of UV inks?

UV inks are widely used across various applications including packaging (labels, flexible packaging), commercial printing (brochures, posters), industrial printing (decoratives, automotive parts), and increasingly in 3D printing and specialty coatings. Their versatility and robust properties make them suitable for diverse substrates like plastic, glass, metal, and wood.

Is UV LED curing more sustainable than conventional UV curing?

Yes, UV LED curing is generally considered more sustainable than conventional UV (mercury lamp) curing. LED systems consume significantly less energy, produce negligible ozone, have a longer lifespan, and generate less heat, leading to reduced environmental impact, lower operational costs, and the ability to print on heat-sensitive materials.

What are the main drivers for the growth of the UV Ink market?

Key drivers include the rapid expansion of digital printing technologies, increasing demand for eco-friendly and low-VOC printing solutions, the growing adoption of UV inks in the packaging and labeling sectors, and continuous technological advancements in UV LED curing systems. These factors collectively contribute to the market's robust growth trajectory.

What challenges does the UV Ink market face?

The UV Ink market faces challenges such as the relatively high initial investment cost for UV printing equipment, volatility in raw material prices, and stringent environmental and health regulations concerning certain ink components. Additionally, the need for specialized formulations for diverse substrates and competition from conventional inks present ongoing hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted