Phenolic Foam Market

Phenolic Foam Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704291 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

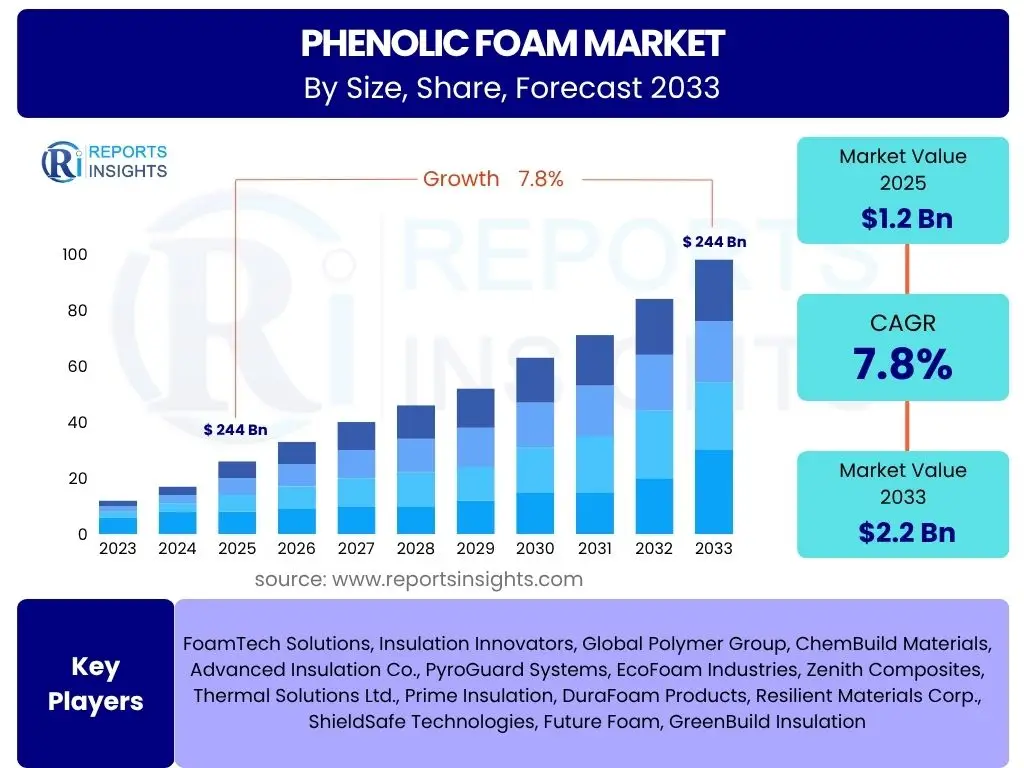

Phenolic Foam Market Size

According to Reports Insights Consulting Pvt Ltd, The Phenolic Foam Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.2 billion in 2025 and is projected to reach USD 2.2 billion by the end of the forecast period in 2033. This growth is primarily attributed to the increasing demand for high-performance insulation materials, particularly in the construction sector, where stringent energy efficiency and fire safety regulations are driving adoption. The inherent properties of phenolic foam, such as superior thermal insulation, excellent fire resistance, and low smoke emission, position it as a preferred choice over conventional insulation options.

The market expansion is further supported by rising awareness regarding energy conservation and sustainable building practices across various regions. Governments and regulatory bodies worldwide are implementing policies that promote the use of advanced insulation materials to reduce carbon footprints and improve building energy performance. This regulatory push, combined with technological advancements in manufacturing processes that enhance product properties and reduce costs, is expected to fuel market growth significantly over the forecast period.

Key Phenolic Foam Market Trends & Insights

Current market analysis reveals a significant pivot towards enhanced sustainability and product innovation within the phenolic foam sector. There is a growing emphasis on developing environmentally friendly manufacturing processes and formulations, including the exploration of bio-based components and reduced volatile organic compound (VOC) emissions. Furthermore, the market is observing a trend towards multi-functional phenolic foam products that offer combined benefits such as superior fire resistance alongside improved structural integrity, catering to more diverse and demanding applications.

Digitalization and automation are increasingly influencing production lines, leading to greater efficiency and consistency in product quality. The integration of advanced analytics in R&D is also accelerating the development of novel phenolic foam variants with tailored properties for specific end-use industries, such as marine and industrial sectors. Customization capabilities are becoming a competitive differentiator, allowing manufacturers to meet niche application requirements more effectively. This strategic focus on innovation and sustainability is reshaping market dynamics and influencing investment priorities.

- Growing demand for sustainable and eco-friendly phenolic foam formulations.

- Increased integration of phenolic foam in prefabricated construction solutions.

- Development of multi-functional phenolic foam offering enhanced thermal and structural properties.

- Rising adoption of automation and digitalization in manufacturing processes to improve efficiency.

- Expansion into niche applications requiring superior fire performance and insulation.

AI Impact Analysis on Phenolic Foam

The integration of Artificial intelligence (AI) is set to significantly revolutionize various aspects of the phenolic foam industry, from raw material sourcing and product development to manufacturing processes and supply chain management. AI-driven analytics can optimize formulations by predicting material interactions and performance characteristics, leading to accelerated R&D cycles and the creation of novel, high-performance foam products with unprecedented properties. This predictive capability reduces the need for extensive physical prototyping, thereby cutting down development costs and time to market.

In manufacturing, AI can enhance operational efficiency through predictive maintenance, quality control, and process optimization. AI algorithms can monitor production lines in real-time, identify anomalies, and autonomously adjust parameters to minimize waste, improve product consistency, and increase throughput. Furthermore, AI-powered supply chain management systems can optimize logistics, inventory, and demand forecasting, leading to more resilient and cost-effective operations. While initial investments in AI infrastructure may be substantial, the long-term benefits in terms of efficiency, innovation, and competitive advantage are poised to be transformative for phenolic foam manufacturers.

- Optimization of phenolic foam formulations and material selection through AI-driven simulations.

- Enhanced quality control and defect detection in manufacturing processes using AI-powered vision systems.

- Predictive maintenance for production machinery, reducing downtime and operational costs.

- Improved supply chain visibility and logistics optimization through AI-driven forecasting and route planning.

- Acceleration of research and development for new phenolic foam applications and properties.

Key Takeaways Phenolic Foam Market Size & Forecast

A comprehensive assessment of the phenolic foam market size and forecast highlights a robust growth trajectory driven by critical global imperatives such as energy efficiency and stringent fire safety regulations. The market's expansion is intrinsically linked to the increasing adoption of advanced insulation materials across diverse industries, particularly within the burgeoning construction sector. The unique combination of superior thermal insulation, exceptional fire resistance, and low smoke emission positions phenolic foam as an indispensable material in modern infrastructure development. This strong market positioning underscores its sustained relevance and demand in the foreseeable future.

Furthermore, the forecast indicates significant opportunities in emerging economies where rapid urbanization and industrialization are fueling construction activities and a growing demand for high-performance building materials. Technological advancements aimed at improving product properties, reducing manufacturing costs, and enhancing sustainability will be crucial for maintaining competitive advantage and unlocking new application areas. Strategic investments in research and development, coupled with an agile response to evolving regulatory landscapes, will enable market players to capitalize on these growth opportunities and solidify their market presence.

- The phenolic foam market is poised for significant growth, driven by global energy efficiency and fire safety mandates.

- Construction and industrial sectors are key drivers of demand for high-performance insulation.

- Technological advancements and product innovation are crucial for market expansion and competitive differentiation.

- Emerging economies present substantial growth opportunities due to rapid infrastructure development.

- Sustainability initiatives and regulatory compliance will increasingly shape product development and market dynamics.

Phenolic Foam Market Drivers Analysis

The phenolic foam market is primarily propelled by the escalating global demand for energy-efficient buildings and industrial insulation solutions. Stringent building codes and regulations, particularly in developed regions, mandate the use of high-performance insulation materials to reduce energy consumption and greenhouse gas emissions. Phenolic foam's excellent thermal insulation properties make it an ideal choice for meeting these rigorous standards, offering superior R-values compared to many traditional insulation materials for a given thickness.

Moreover, the increasing emphasis on fire safety in residential, commercial, and industrial structures is significantly boosting the adoption of phenolic foam. Its inherent fire resistance, low smoke emission, and ability to maintain structural integrity under high temperatures provide a critical safety advantage, making it a preferred material in applications where fire performance is paramount. Rapid urbanization and industrialization in emerging economies are further accelerating construction activities, thereby driving the demand for advanced insulation and fire protection materials like phenolic foam.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Energy-Efficient Buildings | +2.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Stringent Fire Safety Regulations | +1.8% | Global, particularly Europe and North America | 2025-2033 |

| Growing Construction and Infrastructure Development | +1.5% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

| Awareness of Environmental Sustainability | +1.0% | Global | 2026-2033 |

Phenolic Foam Market Restraints Analysis

Despite its advantageous properties, the phenolic foam market faces certain restraints that could impede its growth. One significant challenge is the relatively higher cost of raw materials, such as phenol and formaldehyde, compared to those used in the production of alternative insulation materials like expanded polystyrene (EPS) or mineral wool. This cost disadvantage can limit its adoption in price-sensitive markets, particularly in projects where initial material cost is a primary decision factor over long-term performance benefits.

Additionally, competition from a wide array of alternative insulation materials, each with its own specific advantages and lower price points for certain applications, poses a notable restraint. While phenolic foam excels in fire resistance and thermal performance, the availability of diverse alternatives means that manufacturers must consistently innovate and highlight the unique value proposition of phenolic foam. Regulatory hurdles and environmental concerns related to the production and disposal of certain chemicals used in phenolic foam manufacturing can also present challenges, requiring manufacturers to invest in more sustainable and compliant processes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Raw Material Costs | -1.2% | Global | 2025-2033 |

| Competition from Alternative Insulation Materials | -1.0% | Global | 2025-2033 |

| Environmental Concerns Regarding Production Chemicals | -0.8% | Europe, North America | 2027-2033 |

| Complex Manufacturing Process | -0.5% | Global | 2025-2030 |

Phenolic Foam Market Opportunities Analysis

The phenolic foam market is poised for significant opportunities driven by emerging applications and technological advancements. The increasing focus on passive fire protection in critical infrastructure, such as tunnels, commercial buildings, and industrial facilities, presents a substantial growth avenue for phenolic foam due to its superior fire resistance properties. Developing tailored solutions for these high-value applications can unlock new revenue streams and market segments.

Furthermore, the growing demand for prefabricated and modular construction methods offers a strong opportunity for phenolic foam integration. Its lightweight, rigid, and thermally efficient nature makes it an ideal material for off-site construction, where speed of assembly and energy performance are paramount. Innovation in product formulation, including the development of enhanced water resistance and acoustic properties, can broaden the application scope into areas beyond traditional thermal insulation, such as marine, aerospace, and specialized industrial equipment, thereby expanding the market footprint significantly.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New End-Use Industries (e.g., Marine, Aerospace) | +1.5% | Global | 2027-2033 |

| Development of Advanced Formulations with Enhanced Properties | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Increased Adoption in Prefabricated and Modular Construction | +1.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Growing Demand for Passive Fire Protection in Infrastructure | +0.8% | Global | 2026-2033 |

Phenolic Foam Market Challenges Impact Analysis

The phenolic foam market faces several challenges that require strategic responses from manufacturers. Volatility in raw material prices, particularly for phenol and formaldehyde, can significantly impact production costs and profit margins. This instability necessitates robust supply chain management and hedging strategies to mitigate financial risks and maintain competitive pricing. Additionally, the environmental impact associated with the production process and the end-of-life disposal of phenolic foam can pose regulatory and public perception challenges. Strict environmental regulations, especially in developed countries, require continuous investment in sustainable manufacturing practices and recycling technologies.

Another challenge is the perception and actual risk associated with formaldehyde emissions, even though modern phenolic foam products are designed to meet stringent safety standards. Addressing these concerns through transparent communication, rigorous testing, and the development of formaldehyde-free or low-formaldehyde formulations is crucial for widespread market acceptance. Furthermore, the technical complexity of manufacturing phenolic foam, requiring precise control over chemical reactions and processing conditions, can be a barrier to entry for new players and demands specialized expertise and significant capital investment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | 2025-2033 |

| Stringent Environmental Regulations and Disposal Concerns | -0.7% | Europe, North America | 2026-2033 |

| Public Perception Regarding Chemical Components (e.g., Formaldehyde) | -0.6% | Global | 2025-2033 |

| High Capital Investment for Manufacturing Facilities | -0.4% | Global | 2025-2030 |

Phenolic Foam Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global phenolic foam market, encompassing historical data, current market dynamics, and future projections. The scope of the report includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges. It further offers a thorough segmentation analysis based on product type, application, and end-use industry, providing granular insights into market trends and revenue contributions across various segments. The report aims to equip stakeholders with actionable intelligence to make informed strategic decisions.

Furthermore, the report features a comprehensive regional analysis, highlighting key market trends and growth prospects across North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. It also includes an exhaustive competitive landscape section, profiling key market players, assessing their strategies, product portfolios, and recent developments to provide a holistic view of the competitive environment. The AI impact analysis section offers foresight into how artificial intelligence will shape the future of phenolic foam manufacturing, product development, and supply chain efficiency, providing a forward-looking perspective for industry participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.2 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | FoamTech Solutions, Insulation Innovators, Global Polymer Group, ChemBuild Materials, Advanced Insulation Co., PyroGuard Systems, EcoFoam Industries, Zenith Composites, Thermal Solutions Ltd., Prime Insulation, DuraFoam Products, Resilient Materials Corp., ShieldSafe Technologies, Future Foam, GreenBuild Insulation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The phenolic foam market is extensively segmented to provide a detailed understanding of its dynamics across different product types, applications, and end-use industries. This comprehensive segmentation allows for a granular analysis of market performance, identifying key growth areas and niche opportunities. The segmentation by type typically includes rigid and flexible phenolic foams, each catering to distinct application requirements based on their physical properties and performance characteristics.

Further segmentation by application highlights the primary uses of phenolic foam, such as insulation for building and construction, HVAC systems, and cold storage, as well as its crucial role in fire protection and as a component in structural panels. The end-use industry segmentation provides insights into the major sectors driving demand, including residential and commercial construction, industrial facilities, marine, automotive, and aerospace sectors. Understanding these segments is vital for manufacturers to tailor their product offerings and marketing strategies to specific market needs and capitalize on emerging trends within each category.

- By Type:

- Rigid Phenolic Foam

- Flexible Phenolic Foam

- By Application:

- Insulation

- Building & Construction

- HVAC

- Cold Storage

- Fire Protection

- Structural Panels

- Insulation

- By End-Use Industry:

- Building & Construction

- Residential

- Commercial

- Industrial

- HVAC Systems

- Industrial (Pipe Insulation, Tank Insulation)

- Marine

- Automotive

- Aerospace

- Building & Construction

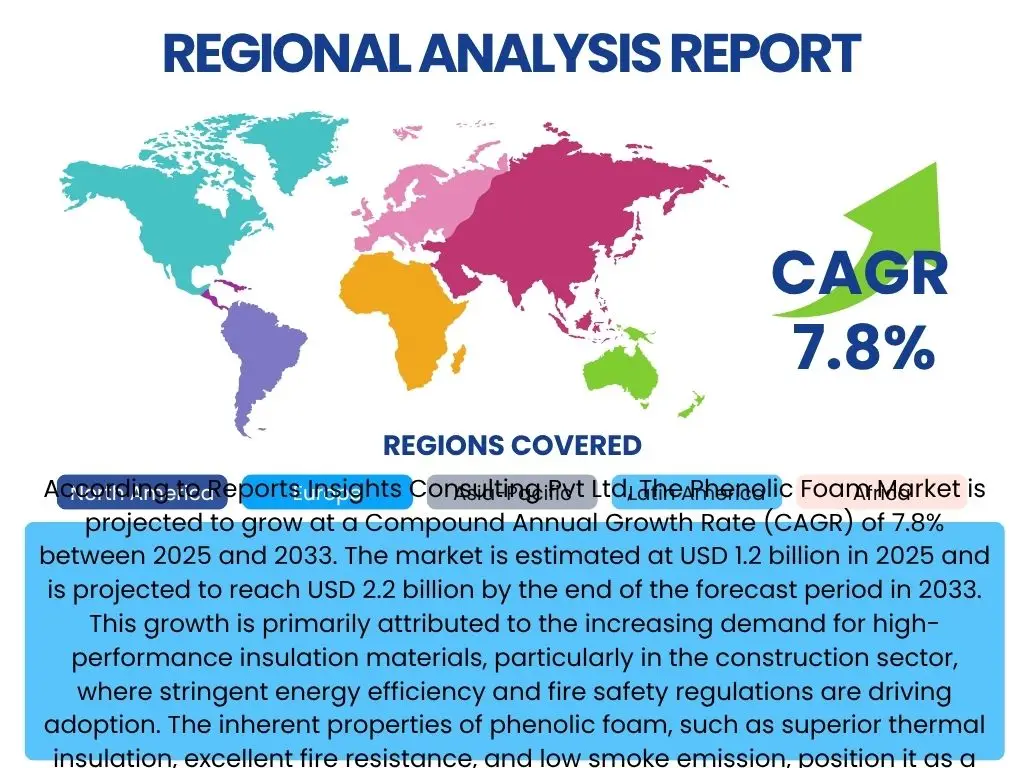

Regional Highlights

The global phenolic foam market exhibits varied growth dynamics across different geographical regions, influenced by economic development, regulatory frameworks, and construction trends. North America and Europe are mature markets, characterized by stringent energy efficiency standards and advanced building codes that drive the demand for high-performance insulation materials. These regions emphasize sustainable construction practices and fire safety, leading to steady adoption of phenolic foam in both new construction and renovation projects. Innovation in product development and strategic collaborations also contribute to market stability and growth in these areas.

Asia Pacific is projected to be the fastest-growing market, primarily due to rapid urbanization, industrialization, and significant infrastructure development in countries like China, India, and Southeast Asian nations. The increasing demand for affordable housing, commercial spaces, and industrial facilities, coupled with a rising awareness of energy conservation, is fueling the adoption of phenolic foam. Latin America and the Middle East & Africa also present promising growth opportunities, driven by expanding construction sectors and growing investments in energy-efficient solutions and robust fire safety measures across various industries.

- North America: Strong demand driven by stringent building codes, energy efficiency mandates, and increasing focus on sustainable construction.

- Europe: Mature market with high adoption rates due to advanced fire safety regulations, strong emphasis on green building, and renovation activities.

- Asia Pacific (APAC): Fastest-growing region due to rapid urbanization, booming construction sector, increasing disposable income, and rising awareness of energy conservation, particularly in China and India.

- Latin America: Emerging market with growth propelled by infrastructure development projects and increasing adoption of modern construction techniques.

- Middle East & Africa (MEA): Growth driven by large-scale commercial and residential projects, investments in industrial infrastructure, and a focus on fire protection in high-rise buildings.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Phenolic Foam Market.- FoamTech Solutions

- Insulation Innovators

- Global Polymer Group

- ChemBuild Materials

- Advanced Insulation Co.

- PyroGuard Systems

- EcoFoam Industries

- Zenith Composites

- Thermal Solutions Ltd.

- Prime Insulation

- DuraFoam Products

- Resilient Materials Corp.

- ShieldSafe Technologies

- Future Foam

- GreenBuild Insulation

- Phoenix Thermal Products

- InsulGuard Technologies

- AeroFoam Composites

- Polymeric Solutions

- Elite Insulation Systems

Frequently Asked Questions

The following section provides concise answers to common inquiries regarding the phenolic foam market, addressing key concerns and offering clarity on its properties, applications, and market dynamics.What is phenolic foam and what are its primary uses?

Phenolic foam is a high-performance insulation material made from phenolic resin, characterized by its closed-cell structure. Its primary uses include thermal insulation in building and construction, HVAC systems, and cold storage, as well as crucial applications in passive fire protection due to its exceptional fire resistance and low smoke emission properties.

Why is phenolic foam considered a superior insulation material?

Phenolic foam is considered superior due to its excellent thermal conductivity (low U-value/high R-value), providing efficient insulation with minimal thickness. Furthermore, its inherent fire resistance, low smoke generation, and high temperature stability make it a safer and more durable choice compared to many conventional insulation materials.

What factors are driving the growth of the phenolic foam market?

Key growth drivers include stringent energy efficiency regulations in the construction sector, increasing demand for fire-safe building materials, rising awareness about sustainable building practices, and rapid infrastructure development, especially in emerging economies. Technological advancements also play a role in enhancing product properties and expanding applications.

What are the main challenges faced by the phenolic foam market?

The main challenges include the relatively higher cost of raw materials compared to some alternative insulation materials, intense competition from various insulation products, and environmental concerns regarding the chemicals used in production and disposal. Volatile raw material prices and public perception issues also present notable hurdles.

How is AI impacting the future of phenolic foam manufacturing?

AI is set to impact phenolic foam manufacturing by optimizing material formulations, improving quality control through predictive analytics, enabling predictive maintenance for machinery, and enhancing supply chain efficiency. This integration is expected to lead to faster R&D, reduced waste, and more consistent product quality.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted