Polyether Polyol for Foam Market

Polyether Polyol for Foam Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702416 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

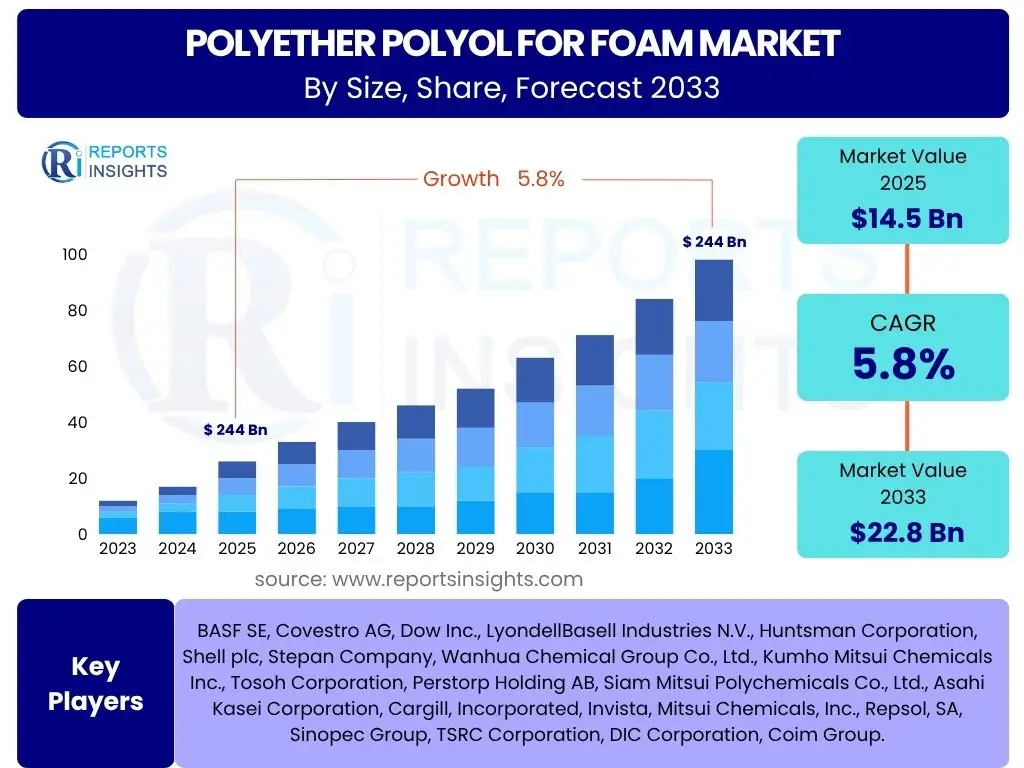

Polyether Polyol for Foam Market Size

According to Reports Insights Consulting Pvt Ltd, The Polyether Polyol for Foam Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 22.8 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by an expanding range of applications across diverse industries, from automotive and construction to furniture and bedding. The increasing demand for lightweight, durable, and versatile foam solutions is a primary factor contributing to this robust market expansion, particularly in emerging economies experiencing rapid urbanization and industrialization.

The market's valuation in 2025 reflects the foundational strength of the polyether polyol segment within the broader polyurethane industry. Its significant utility in both flexible and rigid foam applications provides a stable demand base. Looking towards 2033, the projected increase underscores the sustained innovation within the sector, including the development of advanced formulations that offer enhanced performance characteristics such as improved thermal insulation, sound dampening, and resilience. Furthermore, ongoing investments in manufacturing capacities and supply chain optimization are expected to support this growth, ensuring the availability of polyether polyols to meet escalating global requirements.

Key Polyether Polyol for Foam Market Trends & Insights

User inquiries about polyether polyol for foam market trends frequently revolve around sustainability, performance enhancements, and regional demand shifts. There is a clear interest in how environmental regulations are shaping product development, particularly concerning bio-based and recycled content polyols. Furthermore, users often seek information on technological innovations that are leading to foams with superior mechanical properties, crucial for high-performance applications in automotive and construction. Regional economic growth, especially in Asia Pacific, also emerges as a common theme, highlighting its influence on global market dynamics and supply chain strategies. These collective queries indicate a market keenly focused on future-proofing through innovation and adapting to evolving global demands.

The market is currently experiencing a significant push towards developing more sustainable polyether polyol solutions. This trend is driven by increasing consumer awareness regarding environmental impact, stringent regulatory frameworks encouraging greener manufacturing practices, and corporate commitments to reduce carbon footprints. Companies are investing heavily in research and development to introduce bio-based polyols derived from renewable resources like soy, castor oil, and other plant-based feedstock, aiming to reduce reliance on petrochemical derivatives. Additionally, advancements in chemical recycling technologies for polyurethane waste are gaining traction, presenting an opportunity to recover polyols and reintroduce them into the production cycle, thereby fostering a circular economy model within the industry.

Another prominent trend is the continuous demand for enhanced performance characteristics in foam applications. End-use industries such as automotive and construction are consistently seeking polyether polyols that can produce foams with superior properties like improved flame retardancy, better thermal insulation, enhanced sound absorption, and increased durability. For instance, in the automotive sector, the drive for lightweighting vehicles to improve fuel efficiency and reduce emissions necessitates polyols that can create high-resilience, low-density foams without compromising comfort or structural integrity. Similarly, in construction, the need for energy-efficient buildings is propelling the demand for rigid insulation foams with excellent R-values, driving innovations in polyether polyol formulations specifically for these applications.

- Increasing adoption of bio-based and sustainable polyols.

- Rising demand for high-performance and specialty foam applications.

- Growth in automotive lightweighting initiatives.

- Expansion of construction and infrastructure projects, particularly in Asia Pacific.

- Technological advancements in foam manufacturing processes.

AI Impact Analysis on Polyether Polyol for Foam

Common user questions regarding AI's impact on the polyether polyol for foam market often center on its potential to revolutionize manufacturing efficiency, optimize supply chains, and accelerate research and development. There is particular interest in how AI can lead to smarter factories, more consistent product quality, and quicker development cycles for novel polyol formulations. Concerns sometimes include the initial investment costs, the need for skilled personnel to manage AI systems, and data privacy issues. Overall, users anticipate that AI will bring significant operational advantages and innovation capabilities to the industry, streamlining processes and enhancing competitive edge.

Artificial intelligence is poised to significantly transform the polyether polyol manufacturing landscape by optimizing production processes and enhancing operational efficiencies. AI-powered algorithms can analyze vast datasets from plant operations, including sensor data, process parameters, and quality control metrics, to identify inefficiencies, predict equipment failures, and fine-tune reaction conditions for optimal yield and energy consumption. This predictive analytical capability allows manufacturers to transition from reactive maintenance to proactive strategies, minimizing downtime and maximizing throughput. Furthermore, AI can aid in real-time quality control, automatically adjusting formulations or process settings to ensure consistent product specifications, thereby reducing waste and improving overall product reliability.

Beyond manufacturing, AI holds immense potential in accelerating research and development for new polyether polyol formulations and improving supply chain resilience. Machine learning models can predict the properties of novel molecular structures, significantly reducing the time and resources required for experimental trials. This enables faster development of polyols with desired characteristics, such as enhanced sustainability profiles or improved mechanical properties for specific applications. In supply chain management, AI can forecast demand more accurately, optimize logistics, and identify potential disruptions before they occur, helping companies mitigate risks associated with raw material price volatility or geopolitical events. The integration of AI tools is expected to foster a more agile, responsive, and innovative polyether polyol industry.

- Optimization of manufacturing processes for increased efficiency and reduced waste.

- Enhanced predictive maintenance for production machinery, minimizing downtime.

- Acceleration of research and development for novel polyol formulations.

- Improved supply chain management and demand forecasting.

- Automated quality control and real-time process adjustments.

Key Takeaways Polyether Polyol for Foam Market Size & Forecast

User queries about the key takeaways from the polyether polyol for foam market forecast indicate a primary interest in identifying the most influential growth drivers and understanding the long-term market trajectory. There is a strong emphasis on understanding how sustainable practices and technological advancements will shape future demand and competitive landscapes. Additionally, users often seek concise summaries of market opportunities and potential challenges, aiming to grasp the essential strategic implications for investment and market entry. These questions highlight a collective desire for actionable insights derived from the comprehensive market analysis.

The polyether polyol for foam market is poised for robust expansion, driven predominantly by the escalating demand from key end-use industries such as construction, automotive, and furniture & bedding. The burgeoning global population, coupled with increasing urbanization and industrialization in emerging economies, is creating a sustained need for high-performance insulation, comfortable seating solutions, and protective packaging materials. Manufacturers are continually innovating to meet these diverse application requirements, developing polyols that enable the creation of foams with superior physical properties, including enhanced resilience, thermal efficiency, and lightweight characteristics. This foundational demand, combined with ongoing product development, ensures a positive growth outlook for the sector.

A critical takeaway is the industry's accelerating pivot towards sustainability. The market's future growth is increasingly intertwined with the adoption of bio-based polyols and the implementation of circular economy principles. As regulatory pressures intensify and consumer preferences shift towards environmentally friendly products, companies that invest in renewable feedstock and advanced recycling technologies for polyurethane waste are expected to gain a significant competitive advantage. This strategic shift not only addresses environmental concerns but also offers a pathway to mitigate risks associated with raw material price volatility, positioning the market for more resilient and sustainable growth over the forecast period.

- Robust market growth driven by construction, automotive, and furniture sectors.

- Significant shift towards sustainable and bio-based polyol production.

- Continuous innovation in polyol formulations for enhanced foam performance.

- Emerging economies, particularly in Asia Pacific, represent key growth engines.

- Focus on lightweighting and energy efficiency driving specific foam applications.

Polyether Polyol for Foam Market Drivers Analysis

The polyether polyol for foam market is propelled by several key drivers rooted in global economic development, industrial growth, and evolving consumer demands. These drivers collectively contribute to the increasing consumption of polyether polyols across a spectrum of applications, indicating a positive and sustained growth trajectory. The essential role of foams in enhancing comfort, safety, and efficiency across various sectors underscores the foundational strength of these market drivers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Automotive Industry & Lightweighting Trend | +1.5% | Global, particularly Asia Pacific, Europe, North America | Mid to Long-term (2025-2033) |

| Rising Demand from Construction Sector for Insulation | +1.2% | Global, particularly Asia Pacific, Europe, North America | Mid to Long-term (2025-2033) |

| Increasing Use in Furniture & Bedding Applications | +0.8% | Global, particularly Asia Pacific, North America | Mid to Long-term (2025-2033) |

| Technological Advancements in Foam Properties | +0.7% | Global | Mid to Long-term (2025-2033) |

| Growing Demand for Energy-Efficient Solutions | +0.6% | Global, particularly Europe, North America | Mid to Long-term (2025-2033) |

Polyether Polyol for Foam Market Restraints Analysis

Despite robust growth prospects, the polyether polyol for foam market faces several restraints that could potentially impede its expansion. These challenges often stem from external factors such as raw material supply dynamics, environmental concerns, and competitive pressures from alternative materials. Addressing these restraints effectively will be crucial for market participants to ensure sustainable growth and maintain profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (Propylene Oxide, Ethylene Oxide) | -0.9% | Global | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations and Health Concerns | -0.7% | Europe, North America | Mid to Long-term (2025-2033) |

| Competition from Alternative Insulation Materials | -0.5% | Global | Mid to Long-term (2025-2033) |

| Disposal and Recycling Challenges for Polyurethane Foam Waste | -0.4% | Global | Mid to Long-term (2025-2033) |

Polyether Polyol for Foam Market Opportunities Analysis

The polyether polyol for foam market is characterized by several significant opportunities that hold the potential to unlock new avenues for growth and innovation. These opportunities are often driven by advancements in material science, increasing demand for sustainable solutions, and the expansion into niche application areas. Capitalizing on these emerging trends will be key for market players to diversify their portfolios and capture new market share.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Commercialization of Bio-based Polyols | +1.0% | Global, particularly Europe, North America | Mid to Long-term (2025-2033) |

| Growth of Advanced Recycling Technologies for PU Waste | +0.8% | Global, particularly Europe, North America | Mid to Long-term (2025-2033) |

| Expansion into Emerging Applications (e.g., Medical, Sports) | +0.6% | Global | Mid to Long-term (2025-2033) |

| Increasing Demand for Specialized Foams (e.g., Viscoelastic) | +0.5% | Global | Mid to Long-term (2025-2033) |

Polyether Polyol for Foam Market Challenges Impact Analysis

The polyether polyol for foam market faces distinct challenges that require strategic navigation by industry participants. These challenges can arise from complex regulatory environments, the need for continuous innovation, and the inherent difficulties in managing a global supply chain for chemical products. Effectively addressing these hurdles will be vital for maintaining competitive advantage and ensuring long-term market stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Cost-Effectiveness amidst Raw Material Volatility | -0.8% | Global | Short to Mid-term (2025-2028) |

| Complex Regulatory Landscape and Compliance Requirements | -0.6% | Europe, North America | Mid to Long-term (2025-2033) |

| Need for Significant R&D Investment for Sustainable Solutions | -0.5% | Global | Mid to Long-term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Risks | -0.4% | Global | Short to Mid-term (2025-2028) |

Polyether Polyol for Foam Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the polyether polyol for foam market, encompassing historical data, current market dynamics, and future projections. It delivers crucial insights into market size, growth drivers, restraints, opportunities, and challenges. The report further dissects the market by various segments and offers detailed regional analyses, equipping stakeholders with a holistic understanding of the industry landscape. It is designed to aid strategic decision-making by outlining key trends, competitive intelligence, and future outlooks.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 22.8 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Covestro AG, Dow Inc., LyondellBasell Industries N.V., Huntsman Corporation, Shell plc, Stepan Company, Wanhua Chemical Group Co., Ltd., Kumho Mitsui Chemicals Inc., Tosoh Corporation, Perstorp Holding AB, Siam Mitsui Polychemicals Co., Ltd., Asahi Kasei Corporation, Cargill, Incorporated, Invista, Mitsui Chemicals, Inc., Repsol, SA, Sinopec Group, TSRC Corporation, DIC Corporation, Coim Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The polyether polyol for foam market is meticulously segmented to provide a granular understanding of its diverse applications and product types. This segmentation allows for precise analysis of market dynamics, growth opportunities, and challenges within specific niches. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions, ensuring optimal resource allocation and competitive positioning across the varied demands of the global market.

The market is primarily segmented by type, application, and end-use industry, reflecting the versatile nature of polyether polyols. By type, the market distinguishes between flexible polyols, rigid polyols, and CASE (Coatings, Adhesives, Sealants, Elastomers) polyols, each designed for specific performance requirements. Flexible polyols, for instance, are critical for comfortable seating and bedding, while rigid polyols are essential for insulation and structural components. The application segment further breaks down demand across automotive, construction, furniture & bedding, packaging, and other industrial uses, highlighting the broad utility of these materials. Each sub-segment within these categories addresses unique market needs and technological advancements, contributing to the overall market complexity and growth.

- By Type:

- Flexible Polyols (Conventional Polyols, High Resilience (HR) Polyols, Viscoelastic Polyols)

- Rigid Polyols (Polyurethane (PU) Foam for Insulation, PU Foam for Structural Applications)

- CASE (Coatings, Adhesives, Sealants, Elastomers) Polyols (Polyether Polyols for Coatings, Polyether Polyols for Adhesives, Polyether Polyols for Sealants, Polyether Polyols for Elastomers)

- By Application:

- Furniture & Bedding (Mattresses, Upholstery, Cushions)

- Automotive (Seating, Headliners, Interior Trim, NVH (Noise, Vibration, Harshness))

- Construction (Insulation (Residential, Commercial), Roofing, Spray Foam)

- Packaging (Protective Packaging, Specialty Packaging)

- Industrial

- Others

- By End-Use Industry:

- Construction

- Automotive

- Consumer Goods

- Packaging

- Textile

- Others

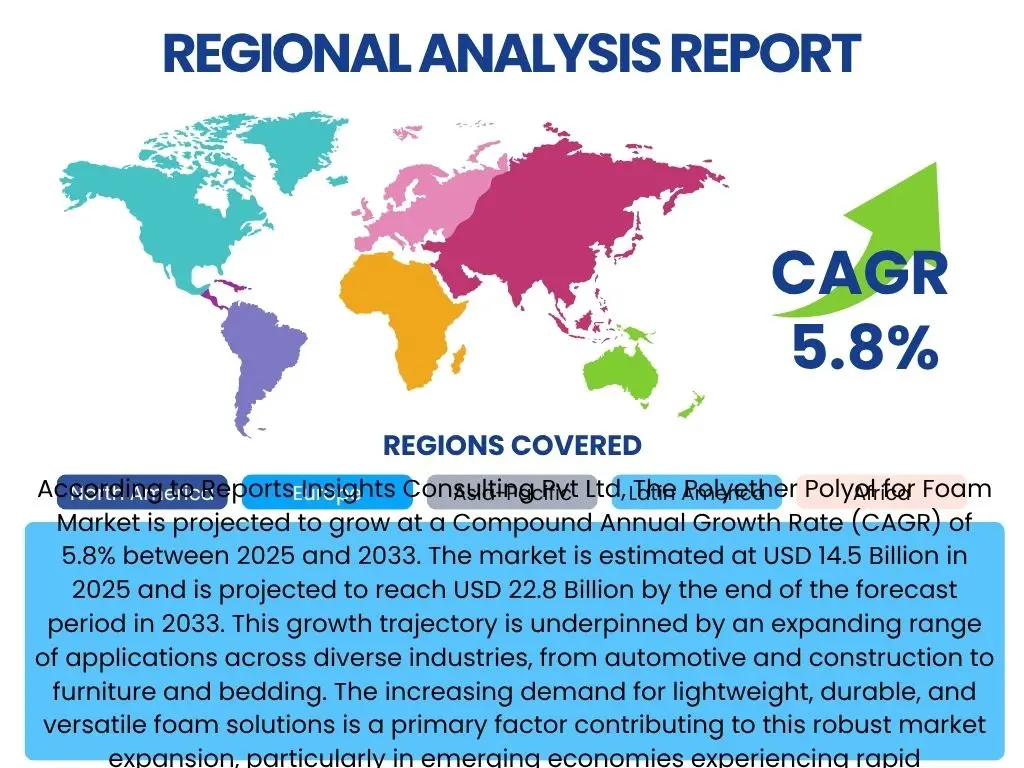

Regional Highlights

The global polyether polyol for foam market exhibits significant regional variations in terms of demand, growth rates, and regulatory environments. These regional dynamics are shaped by factors such as economic development, industrialization levels, infrastructure investment, and consumer preferences. Each region presents a unique set of opportunities and challenges for market participants, necessitating localized strategies for market penetration and expansion. Understanding these geographical nuances is critical for effective global market navigation.

Asia Pacific (APAC) stands out as the dominant and fastest-growing region in the polyether polyol for foam market. This growth is primarily attributed to rapid urbanization, robust industrial expansion, and significant investments in construction and automotive sectors, particularly in economies like China, India, and Southeast Asian countries. The burgeoning middle class and increasing disposable incomes are driving demand for comfortable furniture, efficient insulation, and modern automotive interiors. Furthermore, the presence of a large manufacturing base and growing production capacities for polyether polyols within the region contributes significantly to its leading market share. The region is also becoming a hub for innovation in sustainable polyol solutions, driven by emerging environmental consciousness and government initiatives.

North America represents a mature yet stable market for polyether polyols for foam. The region benefits from a well-established automotive industry, a robust construction sector with a strong emphasis on energy efficiency, and a significant consumer goods market. Demand here is largely driven by replacement and refurbishment activities, coupled with a focus on high-performance and specialized foam applications. Stringent environmental regulations and a strong emphasis on sustainability are pushing manufacturers in the U.S. and Canada towards developing bio-based and low-VOC polyol solutions, fostering innovation in eco-friendly products. The adoption of advanced manufacturing technologies also plays a crucial role in maintaining market value.

Europe is characterized by a high degree of technological sophistication and a strong regulatory environment promoting sustainability. Countries like Germany, France, and the UK are key contributors to the market, driven by stringent energy efficiency standards in buildings and the automotive industry's continuous drive for lightweighting and enhanced safety. European manufacturers are at the forefront of developing innovative polyol solutions, including those with improved flame retardancy and circular economy principles, such as chemical recycling of polyurethane waste. The focus on green building initiatives and circular economy models heavily influences product development and market demand in this region.

Latin America and the Middle East & Africa (MEA) are emerging markets for polyether polyols for foam, offering significant growth potential. In Latin America, increasing industrialization, infrastructure development, and growing automotive production, particularly in Brazil and Mexico, are boosting demand. The MEA region's market growth is driven by significant construction activities, especially in the GCC countries, alongside a developing automotive sector and increasing demand for consumer durables. While these regions currently hold smaller market shares, their rapid economic development and expanding industrial bases are expected to contribute substantially to global demand in the long term, making them attractive for future investments and market expansion strategies for polyol manufacturers.

- Asia Pacific: Dominant market share, highest growth due to rapid industrialization, urbanization, and expanding construction and automotive sectors in China, India, and Southeast Asian countries.

- North America: Mature market driven by a strong automotive industry, focus on energy-efficient construction, and demand for high-performance specialty foams. Emphasis on sustainable and low-VOC products.

- Europe: Advanced market with stringent environmental regulations and a strong emphasis on sustainability and circular economy principles. Leading innovations in high-performance and eco-friendly polyols, particularly in Germany and the UK.

- Latin America: Emerging market with growth fueled by increasing industrialization, infrastructure development, and growing automotive production in countries like Brazil and Mexico.

- Middle East & Africa: Rapidly growing due to significant construction projects and developing industrial sectors, especially in the GCC countries, driving demand for insulation and other foam applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyether Polyol for Foam Market.- BASF SE

- Covestro AG

- Dow Inc.

- LyondellBasell Industries N.V.

- Huntsman Corporation

- Shell plc

- Stepan Company

- Wanhua Chemical Group Co., Ltd.

- Kumho Mitsui Chemicals Inc.

- Tosoh Corporation

- Perstorp Holding AB

- Siam Mitsui Polychemicals Co., Ltd.

- Asahi Kasei Corporation

- Cargill, Incorporated

- Invista

- Mitsui Chemicals, Inc.

- Repsol, SA

- Sinopec Group

- TSRC Corporation

- DIC Corporation

- Coim Group

Frequently Asked Questions

What is polyether polyol for foam used for?

Polyether polyols are primary components in the production of polyurethane foams, which are widely used across various industries for their versatile properties. In the automotive sector, they are used for comfortable seating, headliners, and sound insulation (NVH). The construction industry utilizes them for rigid insulation foams in walls, roofs, and spray applications to enhance energy efficiency. In furniture and bedding, they are crucial for mattresses, cushions, and upholstery due to their resilience and comfort. Additionally, they find applications in protective packaging, industrial equipment, and certain consumer goods.

What is the current market size of polyether polyol for foam?

The global polyether polyol for foam market is estimated at USD 14.5 Billion in 2025. It is projected to demonstrate a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated value of USD 22.8 Billion by the end of the forecast period in 2033. This growth is driven by increasing demand from key end-use industries and ongoing innovations in foam technology.

What are the key drivers for the polyether polyol for foam market?

Key drivers include the robust growth of the automotive industry, particularly the trend towards vehicle lightweighting for fuel efficiency. The escalating demand from the construction sector for effective thermal insulation, driven by energy efficiency regulations and building standards, is another significant driver. Furthermore, the expanding furniture and bedding industry, coupled with technological advancements leading to high-performance and specialized foam properties, also strongly contributes to market growth.

How is sustainability impacting the polyether polyol for foam market?

Sustainability is profoundly impacting the market by driving a shift towards bio-based polyols derived from renewable resources and promoting the development of advanced recycling technologies for polyurethane foam waste. Increasing environmental regulations and consumer demand for eco-friendly products are pushing manufacturers to invest in green chemistry, reduce reliance on petrochemicals, and foster circular economy models within the industry. This focus on sustainability presents both challenges and significant opportunities for innovation and competitive differentiation.

Which regions are leading the polyether polyol for foam market growth?

The Asia Pacific (APAC) region currently holds the largest market share and is projected to exhibit the highest growth rate due to rapid industrialization, extensive urbanization, and substantial investments in the construction and automotive sectors, particularly in countries like China and India. North America and Europe also remain significant markets, driven by established industries and a strong focus on high-performance and sustainable foam solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted