PC Game Market

PC Game Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704213 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

PC Game Market Size

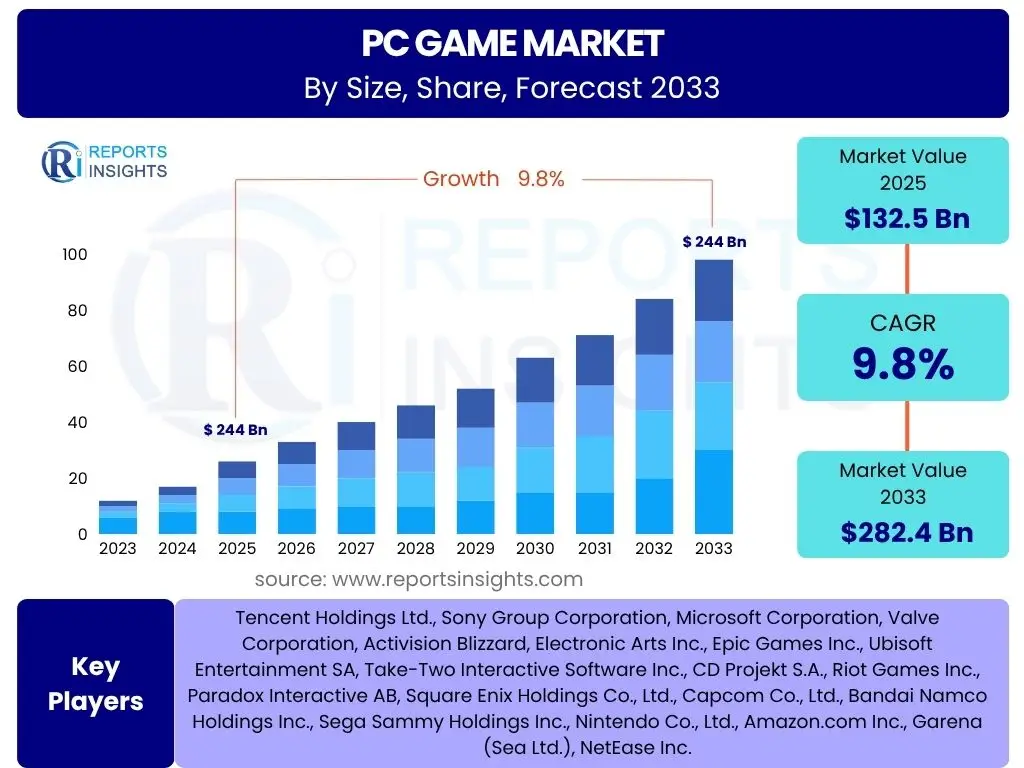

According to Reports Insights Consulting Pvt Ltd, The PC Game Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 132.5 Billion in 2025 and is projected to reach USD 282.4 Billion by the end of the forecast period in 2033.

Key PC Game Market Trends & Insights

The PC Game market is experiencing dynamic shifts, driven by technological advancements and evolving player preferences. Current trends indicate a strong move towards diversified revenue models beyond traditional upfront purchases, with free-to-play titles and subscription services gaining significant traction. User interest in cross-platform interoperability and social gaming features is also on the rise, fostering more connected and communal experiences. Furthermore, the growth of esports continues to elevate PC gaming into a mainstream spectator sport, attracting substantial investment and viewership globally.

Another prominent trend involves the continuous innovation in game development, encompassing enhanced graphics, immersive storytelling, and the integration of emerging technologies like cloud gaming. Players are increasingly seeking high-fidelity experiences and greater accessibility. The indie game development scene is also flourishing, offering unique and experimental titles that cater to niche audiences, complementing the offerings from major studios. These collective trends underscore a vibrant and expanding market, continuously adapting to technological progress and consumer demand.

- Proliferation of Free-to-Play (F2P) and Live Service Games

- Surge in Esports Viewership and Investment

- Advancements in Cloud Gaming Platforms

- Increased Demand for Cross-Platform Play and Social Features

- Growth of Digital Distribution and Subscription Models

- Emergence of Niche Genres and Indie Game Development

- Focus on High-Fidelity Graphics and Immersive Experiences

AI Impact Analysis on PC Game

Artificial Intelligence (AI) is poised to fundamentally transform the PC Game market, impacting every facet from development to player experience. Users frequently inquire about how AI will enhance gameplay, often focusing on more realistic and adaptive Non-Player Characters (NPCs) and intelligent game mechanics that learn from player behavior. There is also considerable interest in AI's role in procedural content generation, which could lead to infinitely varied and dynamic game worlds, reducing development time while increasing replayability. Concerns about AI's potential for misuse, such as advanced anti-cheat systems that might err on false positives or AI-driven monetization strategies, are also prevalent among user inquiries.

Beyond gameplay, AI is expected to revolutionize game development pipelines by automating tedious tasks, optimizing asset creation, and enhancing quality assurance through intelligent testing. This efficiency gain could democratize game development, allowing smaller studios to compete more effectively. From a player perspective, AI-driven personalization, including adaptive difficulty, tailored recommendations, and even dynamic narrative generation, holds significant promise for creating deeply engaging and customized experiences. The integration of AI also raises questions about intellectual property ownership for AI-generated content and the ethical implications of creating increasingly autonomous game systems, highlighting both the immense opportunities and critical challenges ahead.

- Enhanced Non-Player Character (NPC) Intelligence and Realism

- Procedural Content Generation for Dynamic Game Worlds

- Personalized Player Experiences and Adaptive Difficulty

- Sophisticated Anti-Cheat Systems and Security Enhancements

- Automated Game Testing and Quality Assurance

- AI-Powered Narrative Generation and Dynamic Storytelling

- Efficiency Gains in Game Development and Asset Creation

Key Takeaways PC Game Market Size & Forecast

The PC Game market is set for robust expansion through 2033, driven by a confluence of technological innovation and evolving consumer engagement patterns. The substantial projected market size and compound annual growth rate highlight the sector's resilience and capacity for sustained growth. This trajectory is largely fueled by increasing global internet penetration, the pervasive influence of esports, and the continuous release of high-quality, engaging titles across diverse genres. The market's ability to adapt to new revenue models, such as free-to-play with in-game purchases and subscription services, also plays a crucial role in its financial health and accessibility.

Key insights suggest that future growth will be significantly shaped by advancements in cloud gaming, which promises to lower hardware barriers for many potential players, thereby expanding the addressable market. Furthermore, the integration of artificial intelligence will unlock new dimensions of gameplay and development efficiency, while continued investment in interactive social features will deepen player engagement. The forecast indicates that stakeholders should prioritize strategies that leverage these technological shifts and cater to the diverse preferences of a global player base, ensuring continued market leadership and innovation.

- Consistent Strong Growth Trajectory through 2033

- Significant Market Value Increase Driven by Digital Transformation

- Technological Innovation as a Primary Growth Catalyst

- Shift Towards Diverse Revenue Models and Accessibility

- Increasing Importance of Esports and Cloud Gaming for Market Expansion

PC Game Market Drivers Analysis

The PC Game market's growth is propelled by several fundamental drivers that foster increased participation and spending. Global internet penetration and improved broadband infrastructure are enabling more individuals to access and enjoy PC games, particularly in emerging economies. The proliferation of digital distribution platforms has simplified game acquisition, while continuous advancements in gaming hardware and software enhance the immersive quality of games, driving consumer demand for newer titles and upgrades. The increasing popularity of esports, transforming competitive gaming into a major spectator sport, further expands the market by attracting new players and investors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Internet Penetration & Broadband Speed | +2.1% | Asia Pacific, Latin America, MEA | Medium-term to Long-term |

| Growth in Esports Popularity and Professional Leagues | +1.8% | North America, Europe, Asia Pacific (China, South Korea) | Short-term to Medium-term |

| Technological Advancements in Gaming Hardware and Software | +1.5% | Global, particularly developed markets | Continuous, Short-term Cycles |

| Expanding Digital Distribution and Subscription Models | +1.3% | Global | Short-term to Medium-term |

| Rising Disposable Income and Leisure Spending | +1.1% | Emerging Economies (China, India, Brazil) | Medium-term to Long-term |

PC Game Market Restraints Analysis

Despite its robust growth, the PC Game market faces several significant restraints that could temper its expansion. High initial hardware costs for powerful gaming PCs can be a barrier to entry for potential players, especially in price-sensitive markets. The intense competition within the industry, marked by a saturated market with numerous titles and publishers, can make it challenging for new games to gain traction and for smaller developers to thrive. Piracy remains a persistent issue, leading to revenue losses for developers and publishers. Furthermore, increasing concerns around game addiction and mental health, along with potential regulatory scrutiny, could impact market sentiment and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Hardware Costs for Gaming PCs | -0.9% | Emerging Markets, Price-Sensitive Regions | Medium-term |

| Intense Market Competition and Saturation | -0.7% | Global | Continuous |

| Piracy and Intellectual Property Infringement | -0.6% | Global | Continuous |

| Concerns Regarding Gaming Addiction and Mental Health | -0.5% | Global, particularly regulatory bodies | Long-term |

PC Game Market Opportunities Analysis

Significant opportunities exist within the PC Game market for sustained innovation and expansion. The rapid evolution of cloud gaming presents a major opportunity by removing the need for expensive hardware, making high-fidelity gaming accessible to a broader audience. The integration of advanced technologies such as Virtual Reality (VR) and Augmented Reality (AR) offers new immersive experiences, potentially creating entirely new genres and gameplay mechanics. Furthermore, the expansion into untapped emerging markets, particularly in Asia Pacific and Latin America, represents a substantial growth avenue as internet infrastructure improves and disposable incomes rise. Continued diversification of monetization models, including battle passes, NFTs, and premium subscriptions, also offers new revenue streams and engagement strategies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud Gaming Services | +1.6% | Global, particularly regions with strong internet infrastructure | Medium-term to Long-term |

| Integration of VR/AR and Metaverse Elements | +1.4% | Global, focused on early adopters | Long-term |

| Untapped Market Penetration in Emerging Regions | +1.2% | Asia Pacific, Latin America, MEA | Medium-term to Long-term |

| Diversification of Revenue Models (e.g., Battle Passes, NFTs) | +1.0% | Global | Short-term to Medium-term |

PC Game Market Challenges Impact Analysis

The PC Game market faces several critical challenges that require strategic navigation for sustained success. Cyber security threats, including sophisticated hacking, data breaches, and in-game cheating, pose significant risks to player trust and game integrity. The rapid pace of technological obsolescence necessitates continuous investment in research and development to keep up with evolving hardware and software standards, which can be costly for developers. Attracting and retaining top talent in game development, particularly for specialized roles in AI and advanced graphics, is an ongoing hurdle. Furthermore, maintaining the sustainability of free-to-play models, ensuring they remain profitable without alienating players through aggressive monetization, is a continuous balancing act. These challenges demand innovative solutions and adaptive business strategies to mitigate their potential negative impact on market growth and player satisfaction.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cyber Security Threats and In-Game Cheating | -0.8% | Global | Continuous |

| Rapid Technological Obsolescence and Hardware Cycles | -0.7% | Global | Short-term to Medium-term |

| Talent Acquisition and Retention in Game Development | -0.6% | Global, particularly major development hubs | Long-term |

| Sustainability of Free-to-Play Monetization Models | -0.5% | Global | Medium-term |

PC Game Market - Updated Report Scope

This market research report provides a comprehensive analysis of the PC Game market, covering its size, growth trajectory, key trends, and future outlook across various segments and regions. It delves into the impact of technological advancements, particularly Artificial Intelligence, on the industry, alongside an in-depth assessment of market drivers, restraints, opportunities, and challenges. The report offers strategic insights for stakeholders, aiding informed decision-making in a rapidly evolving digital entertainment landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 132.5 Billion |

| Market Forecast in 2033 | USD 282.4 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Tencent Holdings Ltd., Sony Group Corporation, Microsoft Corporation, Valve Corporation, Activision Blizzard, Electronic Arts Inc., Epic Games Inc., Ubisoft Entertainment SA, Take-Two Interactive Software Inc., CD Projekt S.A., Riot Games Inc., Paradox Interactive AB, Square Enix Holdings Co., Ltd., Capcom Co., Ltd., Bandai Namco Holdings Inc., Sega Sammy Holdings Inc., Nintendo Co., Ltd., Amazon.com Inc., Garena (Sea Ltd.), NetEase Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PC Game market is comprehensively segmented to provide a nuanced understanding of its various components and revenue streams. This segmentation allows for detailed analysis of player preferences, monetization strategies, and distribution channels, reflecting the diverse landscape of PC gaming. Each segment highlights different aspects of the market, from the type of games players engage with to how they purchase and access content, providing valuable insights for publishers, developers, and investors alike.

- By Game Type:

- Action-Adventure: Encompasses popular genres like open-world games and cinematic experiences.

- Role-Playing Games (RPGs): Includes single-player epics and massively multiplayer online role-playing games (MMORPGs).

- Strategy: Covers real-time strategy (RTS), turn-based strategy (TBS), and grand strategy titles.

- Simulation: Features life simulations, management simulations, and vehicle simulations.

- Sports: Includes competitive sports titles based on real-world sports.

- Puzzle: Comprises logic, matching, and brain-teaser games.

- Others: Includes niche categories like casual games, indie titles, fighting games, and educational games.

- By Revenue Model:

- Free-to-Play (F2P): Games offered without an upfront cost, relying on in-game purchases for revenue.

- Pay-to-Play (P2P) / Premium: Traditional model where players buy the game upfront.

- Subscription: Players pay recurring fees for access to a library of games or premium content.

- In-Game Purchases / Microtransactions: Additional content, cosmetics, or functional items bought within games.

- By Distribution Channel:

- Digital Download/Online Stores: Dominant channel through platforms like Steam, Epic Games Store, and others.

- Physical Retail: Declining but still present for collector's editions or specific regions.

- By End-User:

- Casual Gamers: Play infrequently or prefer less complex games.

- Core/Hardcore Gamers: Dedicated players who invest significant time and resources into gaming.

- Esports Professionals: Elite players participating in competitive gaming tournaments.

Regional Highlights

- North America: A mature and highly influential market, North America leads in innovation, game development, and esports investment. The region benefits from high disposable incomes, robust internet infrastructure, and a strong preference for AAA titles and competitive gaming. It serves as a significant hub for game publishers and a key market for new technology adoption.

- Europe: Characterized by diverse gaming cultures and strong digital adoption, Europe represents a substantial market. Countries like Germany, the UK, and France are major contributors, with high engagement in both traditional premium games and free-to-play titles. The region also boasts a vibrant indie development scene and a growing esports audience.

- Asia Pacific (APAC): The largest and fastest-growing region in the PC Game market, primarily driven by China, South Korea, and Japan. This region is characterized by the dominance of free-to-play games, particularly MMORPGs and MOBAs, and an unparalleled enthusiasm for esports. Rapid urbanization, increasing disposable incomes, and widespread internet access are key growth catalysts.

- Latin America: An emerging market with significant growth potential, Latin America is witnessing increasing internet penetration and a rising middle class. Brazil and Mexico are leading markets in the region, with a growing appetite for PC games, especially F2P titles. The market is also seeing increased investment in localized content and esports infrastructure.

- Middle East and Africa (MEA): Still in its nascent stages compared to other regions, MEA is experiencing rapid growth, particularly in the Gulf Cooperation Council (GCC) countries and South Africa. Improved internet connectivity, a youthful population, and government initiatives to boost digital entertainment are contributing to market expansion. The region shows increasing interest in esports and mobile-PC crossover experiences.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PC Game Market.- Tencent Holdings Ltd.

- Sony Group Corporation

- Microsoft Corporation

- Valve Corporation

- Activision Blizzard

- Electronic Arts Inc.

- Epic Games Inc.

- Ubisoft Entertainment SA

- Take-Two Interactive Software Inc.

- CD Projekt S.A.

- Riot Games Inc.

- Paradox Interactive AB

- Square Enix Holdings Co., Ltd.

- Capcom Co., Ltd.

- Bandai Namco Holdings Inc.

- Sega Sammy Holdings Inc.

- Nintendo Co., Ltd.

- Amazon.com Inc.

- Garena (Sea Ltd.)

- NetEase Inc.

Frequently Asked Questions

What is the current market size of the PC Game industry?

The PC Game market is estimated at USD 132.5 Billion in 2025.

What is the projected growth rate for the PC Game market?

The PC Game market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033.

How will AI impact the future of PC gaming?

AI is expected to enhance NPC intelligence, enable procedural content generation, personalize player experiences, and automate development processes, leading to more dynamic and efficient game creation.

Which regions are key contributors to the PC Game market?

Asia Pacific, particularly China and South Korea, is the largest and fastest-growing region, followed by mature markets like North America and Europe.

What are the primary revenue models in the PC Game market?

Key revenue models include Free-to-Play (F2P) with in-game purchases, traditional Pay-to-Play (P2P) premium sales, and subscription services.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted