Fighting Game Market

Fighting Game Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702661 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

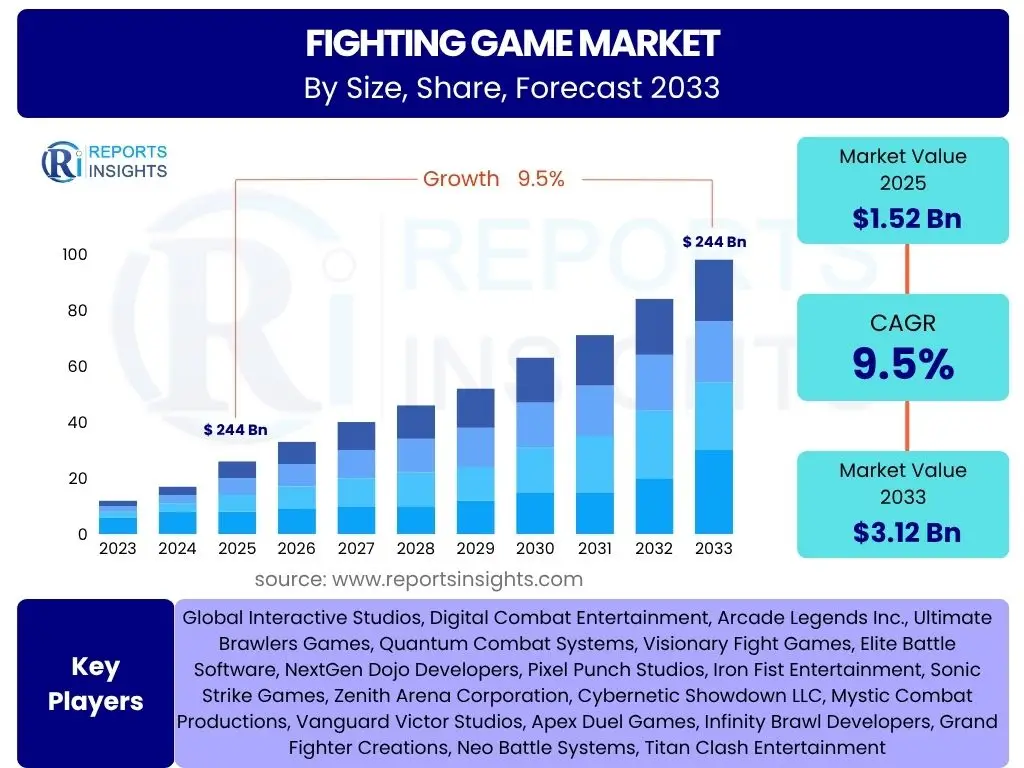

Fighting Game Market Size

According to Reports Insights Consulting Pvt Ltd, The Fighting Game Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 1.52 Billion in 2025 and is projected to reach USD 3.12 Billion by the end of the forecast period in 2033.

Key Fighting Game Market Trends & Insights

User inquiries regarding the Fighting Game market frequently revolve around its evolving landscape, particularly concerning competitive play, technological integration, and content delivery. The sector is witnessing a significant shift towards esports, with major tournaments and professional leagues driving both viewership and player engagement. This trend is amplified by advancements in online infrastructure, facilitating seamless global competition and community interaction, which are critical for the genre's growth.

Another prevalent area of interest concerns the expansion of game accessibility and monetization strategies. Developers are increasingly focusing on features like simplified input systems and comprehensive tutorials to lower the barrier to entry for new players, while retaining the depth that appeals to veterans. Furthermore, the adoption of live-service models, including battle passes, seasonal content, and cosmetic customization, is becoming a standard practice, influencing player spending habits and long-term engagement.

The market is also characterized by a strong emphasis on character diversity, narrative expansion, and cross-platform compatibility. Players are keen on understanding how new characters, storylines, and the ability to compete across different gaming platforms contribute to the genre's appeal and longevity. These elements collectively shape the market's trajectory, moving beyond traditional one-time purchases to a more dynamic, engagement-driven ecosystem.

- Escalating popularity of esports and professional fighting game leagues.

- Increased focus on enhanced online multiplayer infrastructure and netcode.

- Integration of live-service models, battle passes, and seasonal content.

- Growing emphasis on character roster diversity and unique gameplay mechanics.

- Development of simplified control schemes to broaden player accessibility.

- Expansion of cross-platform play capabilities across various devices.

- Rising demand for high-fidelity graphics and immersive visual experiences.

- Strategic intellectual property crossovers driving new player acquisition.

AI Impact Analysis on Fighting Game

Common user questions regarding AI's impact on fighting games primarily focus on its role in gameplay enhancements, development efficiencies, and player experience improvements. There is significant interest in how advanced AI can create more dynamic and challenging single-player experiences, moving beyond predictable bot patterns to simulate human-like opponents. This includes adaptive AI that learns from player behavior and procedural generation of combat scenarios, aiming to extend the longevity and replayability of solo content.

Beyond direct gameplay, users are also curious about AI's application in broader game development and operational aspects. This encompasses AI-driven tools for animation, character balancing, and level design, potentially streamlining the creation process and reducing development cycles. Furthermore, the role of AI in anti-cheat systems, intelligent matchmaking algorithms, and personalized training modes is a key area of discussion, reflecting a desire for fairer, more engaging, and tailored competitive environments.

Concerns also emerge regarding the ethical implications of AI, particularly in competitive settings. Players ponder whether AI could lead to unfair advantages if used in certain capacities, or if over-reliance on AI might stifle human creativity in game design. However, the overarching expectation is that AI will primarily serve to augment the fighting game experience, making it more robust, accessible, and enjoyable for a wider audience, while maintaining the core competitive integrity.

- AI-driven adaptive opponents offering more realistic and challenging single-player experiences.

- Enhanced matchmaking algorithms utilizing AI for balanced competitive play.

- AI-powered anti-cheat systems to maintain fair gameplay environments.

- Procedural content generation for diverse training modes and scenarios.

- Automated testing and bug detection in game development cycles.

- AI for improved animation, character behavior, and environmental reactivity.

- Personalized training systems based on player performance analysis.

- Potential for AI-assisted character balancing and move set optimization.

Key Takeaways Fighting Game Market Size & Forecast

Insights derived from analyzing user questions about the Fighting Game market forecast consistently highlight an optimistic outlook driven by several core factors. A primary takeaway is the genre's robust resilience and sustained growth, largely fueled by its strong foundation in competitive play and a dedicated global fanbase. The forecast indicates that continued investment in esports infrastructure, coupled with innovations in online connectivity, will be crucial in expanding the market's reach and revenue streams.

Another significant point of interest is the increasing diversification of revenue models within the market. Beyond traditional game sales, the growing adoption of live-service elements, battle passes, and cosmetic microtransactions is projected to contribute substantially to overall market size. This shift reflects a consumer preference for ongoing content and personalization, encouraging developers to maintain long-term engagement strategies post-launch.

Furthermore, the market's future growth is intrinsically linked to its ability to attract and retain new players while satisfying its core demographic. This necessitates a balance between preserving the genre's high skill ceiling and introducing features that improve accessibility, such as simplified controls and comprehensive tutorials. Regional growth disparities are also a key takeaway, with emerging markets poised to contribute significantly as gaming infrastructure improves globally, offering new avenues for market expansion.

- Consistent market expansion driven by strong esports ecosystem and community engagement.

- Significant revenue contribution from evolving monetization strategies like live-service models.

- Increasing market value attributed to technological advancements in online play and graphics.

- Growth potential hinges on balancing accessibility for new players with competitive depth.

- North America and Asia Pacific are projected as primary growth regions.

- Mobile fighting games represent an untapped, high-growth opportunity.

- Continued investment in new IPs and crossover collaborations will stimulate demand.

Fighting Game Market Drivers Analysis

The Fighting Game market's expansion is significantly propelled by the burgeoning esports industry, which provides a global platform for competitive play and enhances viewer engagement. Major tournaments, professional leagues, and substantial prize pools attract both players and audiences, transforming fighting games into a spectator sport and driving game sales and in-game purchases. This phenomenon elevates the genre's visibility and cultural relevance, attracting new players eager to participate in or spectate high-stakes competition.

Technological advancements also serve as a crucial driver, particularly in areas like improved netcode, graphics fidelity, and cross-platform compatibility. The development of rollback netcode has vastly improved the online multiplayer experience, reducing latency and making competitive online play more equitable and enjoyable. Similarly, advancements in game engines and hardware allow for more detailed character models, fluid animations, and immersive environments, which attract players seeking cutting-edge visual experiences. The push for cross-play expands the player pool for individual titles, enhancing matchmaking quality and community vibrancy.

Furthermore, the strategic use of intellectual properties (IPs) and character diversity plays a pivotal role. Crossover characters and collaborations with other popular franchises introduce fighting games to new audiences, leveraging existing fanbases. A diverse roster of characters, each with unique fighting styles and backstories, caters to a wide range of player preferences, increasing replayability and fostering deeper engagement. The accessibility improvements, such as simplified control options and comprehensive tutorials, also widen the market by lowering the barrier to entry for newcomers without compromising competitive depth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Esports Popularity | +2.5% | Global, particularly North America, APAC | Short to Medium Term (2025-2029) |

| Technological Advancements (Netcode, Graphics) | +1.8% | Global | Medium Term (2026-2031) |

| Increasing Gaming Penetration & Digital Distribution | +1.5% | Emerging Markets (APAC, Latin America) | Long Term (2027-2033) |

| Character Diversity and IP Crossovers | +1.2% | Global | Short to Medium Term (2025-2029) |

| Accessibility Features & Training Modes | +0.8% | Global | Medium to Long Term (2026-2033) |

Fighting Game Market Restraints Analysis

One significant restraint on the Fighting Game market is the inherent high skill ceiling and perceived difficulty for new players. Many traditional fighting games require extensive practice to master complex command inputs, character matchups, and strategic decision-making. This steep learning curve can deter casual players or newcomers who might quickly become frustrated by the initial barrier to entry, limiting the potential growth of the player base beyond its dedicated core audience. While developers are introducing accessibility features, the genre's fundamental competitive nature often maintains a significant skill gap.

Market saturation and intense competition within the genre also act as a restraint. With multiple established franchises and new titles constantly vying for player attention, it becomes challenging for new IPs to carve out a significant market share. Players often remain loyal to their preferred series, making it difficult for developers to innovate sufficiently to disrupt existing loyalties. This competitive landscape can lead to resource strain for smaller studios and a reliance on established formulas for larger ones, potentially stifling true innovation.

Furthermore, monetization fatigue from live-service models and the high cost of game development pose additional challenges. While microtransactions and battle passes can generate significant revenue, an oversaturation of such models or perceived predatory practices can lead to player backlash and reduced engagement. The substantial investment required for developing high-fidelity fighting games, including character design, animation, online infrastructure, and ongoing content updates, can also be prohibitive, especially for independent developers, limiting the number and diversity of new releases.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Skill Ceiling & Learning Curve | -1.5% | Global | Short to Medium Term (2025-2030) |

| Market Saturation & Intense Competition | -1.0% | Global | Medium Term (2026-2031) |

| Monetization Fatigue & Player Pushback | -0.8% | North America, Europe | Short Term (2025-2028) |

| High Development & Maintenance Costs | -0.7% | Global | Long Term (2027-2033) |

Fighting Game Market Opportunities Analysis

Significant opportunities for growth in the Fighting Game market lie in the expansion into new platforms and monetization strategies. The mobile gaming sector, with its immense global reach and accessibility, represents a largely untapped market for fighting games. Developing titles specifically designed for touch interfaces or simplified controls could attract millions of new players who may not own consoles or high-end PCs. Furthermore, the increasing acceptance of subscription-based gaming services offers a new distribution model, allowing developers to reach a broader audience by reducing the initial cost barrier for players.

The integration of advanced technologies like Virtual Reality (VR) and Augmented Reality (AR) presents novel gameplay experiences and engagement avenues. While still nascent, VR fighting games could offer unparalleled immersion, allowing players to feel more directly connected to the combat. AR applications could blend fighting game elements with real-world environments, creating unique social and interactive experiences. These technologies, as they become more accessible and refined, could revolutionize how players interact with fighting games, opening up entirely new dimensions of play.

Moreover, the opportunity to diversify content beyond core gameplay, such as through comprehensive educational modes, storytelling expansions, and fan-generated content support, is substantial. Detailed tutorials and training environments that break down complex mechanics can significantly aid new players in overcoming the genre's learning curve. Rich lore and character-driven narratives can deepen player investment, fostering stronger communities. Finally, enabling and supporting fan-created content, such as mods or custom characters, can extend game longevity and maintain player interest, fostering a vibrant ecosystem around a title.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Mobile Gaming Expansion & Optimization | +2.0% | APAC, Latin America, MEA | Medium to Long Term (2026-2033) |

| Cross-Platform Play & Unified Ecosystems | +1.5% | Global | Short to Medium Term (2025-2030) |

| VR/AR Integration for Immersive Experiences | +1.0% | North America, Europe | Long Term (2028-2033) |

| Subscription Gaming Service Inclusion | +0.9% | Global | Medium Term (2026-2031) |

| Educational Content & Advanced Training Tools | +0.7% | Global | Short to Medium Term (2025-2029) |

Fighting Game Market Challenges Impact Analysis

One of the persistent challenges facing the Fighting Game market is maintaining a robust and engaged player base over the long term, particularly for individual titles. While initial sales for new releases can be strong, retaining players in a highly competitive and skill-intensive genre is difficult. Players often migrate to newer titles, or revert to established favorites, leading to fragmentation of the player base and reduced online activity for older games. This necessitates continuous content updates, balance patches, and active community management to prevent player attrition.

Combating online toxicity and ensuring a fair play environment are also critical challenges. The competitive nature of fighting games can sometimes foster negative player interactions, including verbal abuse, "rage quitting," or unsportsmanlike conduct. Effective anti-cheat measures, robust reporting systems, and active moderation are essential to maintain a positive and inclusive online environment. Furthermore, addressing issues like "netcode woes" in online matches, where latency can significantly impact gameplay, remains a technical hurdle that can deter players if not adequately managed.

The delicate balance between competitive integrity and accessibility presents another significant challenge. Developers must design games that are deep enough to satisfy seasoned veterans and esports professionals, yet also welcoming enough for newcomers. Overly complex mechanics can alienate new players, while oversimplification can bore experienced ones. Striking this balance requires careful game design and iterative testing. Additionally, the increasing cost of game development and the potential for intellectual property disputes, especially with a growing emphasis on character crossovers and licensed content, can further complicate market dynamics and limit innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Player Retention & Community Management | -1.2% | Global | Short to Medium Term (2025-2030) |

| Combating Online Toxicity & Cheating | -1.0% | Global | Short Term (2025-2028) |

| Balancing Competitive Depth vs. Accessibility | -0.9% | Global | Medium Term (2026-2031) |

| Monetization Model Acceptance & Fatigue | -0.7% | North America, Europe | Short to Medium Term (2025-2029) |

Fighting Game Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Fighting Game market, examining its current size, historical trends from 2019 to 2023, and future growth projections up to 2033. The scope includes a detailed segmentation analysis by platform, genre type, revenue model, and geographic region, offering granular insights into various market dynamics. Furthermore, the report delves into the impact of key market drivers, restraints, opportunities, and challenges, providing a holistic view of the factors influencing market expansion and evolution. It also covers the competitive landscape, profiling leading companies and their strategic initiatives, to offer actionable intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.52 Billion |

| Market Forecast in 2033 | USD 3.12 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 258 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Interactive Studios, Digital Combat Entertainment, Arcade Legends Inc., Ultimate Brawlers Games, Quantum Combat Systems, Visionary Fight Games, Elite Battle Software, NextGen Dojo Developers, Pixel Punch Studios, Iron Fist Entertainment, Sonic Strike Games, Zenith Arena Corporation, Cybernetic Showdown LLC, Mystic Combat Productions, Vanguard Victor Studios, Apex Duel Games, Infinity Brawl Developers, Grand Fighter Creations, Neo Battle Systems, Titan Clash Entertainment |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fighting Game market is meticulously segmented to provide a comprehensive understanding of its diverse components and growth vectors. This segmentation allows for a granular analysis of player preferences, revenue streams, and technological adoption across various sub-categories. By dissecting the market based on platforms, genre types, revenue models, and graphics styles, stakeholders can identify specific niches and tailor their strategies to maximize market penetration and profitability. Each segment exhibits unique growth patterns and competitive dynamics, reflecting the varied landscape of the fighting game community.

The platform segmentation highlights the dominance of console and PC gaming, though mobile is rapidly emerging as a significant growth area, particularly in APAC. Genre type differentiation helps distinguish between traditional 2D and 3D fighting games, and the burgeoning category of arena brawlers, each appealing to distinct player bases with different competitive expectations. Revenue model analysis is critical for understanding consumer spending habits, from traditional premium purchases to the increasingly prevalent free-to-play and microtransaction-driven models. Lastly, graphics style segmentation reflects artistic trends and their appeal to specific aesthetic preferences within the global gaming audience, influencing design and marketing approaches.

- By Platform:

- PC

- Console (PlayStation, Xbox, Nintendo Switch)

- Mobile (iOS, Android)

- By Genre Type:

- 2D Fighting Games (e.g., traditional side-scrolling combat)

- 3D Fighting Games (e.g., character movement in a 3D arena)

- Arena Brawlers (e.g., multi-directional combat in open arenas)

- By Revenue Model:

- Premium/One-Time Purchase

- Free-to-Play (F2P)

- Subscription (e.g., via gaming services)

- In-Game Purchases/Microtransactions (cosmetics, characters, battle passes)

- By Graphics Style:

- Realistic (e.g., highly detailed, lifelike character models)

- Anime/Manga (e.g., cel-shaded, stylized character designs)

- Cartoon/Stylized (e.g., exaggerated, non-realistic aesthetics)

Regional Highlights

- North America: This region maintains a strong market presence, driven by a mature gaming infrastructure, high disposable income, and a deeply entrenched esports culture. The United States and Canada are key contributors, boasting a large player base, significant viewership for fighting game tournaments, and a robust ecosystem of developers and publishers. Innovation in online services and competitive events continues to fuel growth.

- Europe: Characterized by diverse gaming communities and a growing appetite for esports, Europe represents a substantial market for fighting games. Countries such as the UK, Germany, and France are prominent, with increasing internet penetration and a rising number of professional players. The region's market is supported by both established franchises and a burgeoning indie scene, contributing to sustained demand.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to its immense mobile gaming market, increasing internet accessibility, and a vast youth population embracing competitive gaming. Japan, South Korea, and China are significant players, with strong domestic fighting game franchises and a rapidly expanding esports audience. The adoption of free-to-play models and localized content is crucial for market penetration here.

- Latin America: This region shows significant potential for growth, driven by an expanding middle class, increasing smartphone adoption, and a passionate gaming community. Brazil and Mexico are leading the charge, with a growing number of fighting game enthusiasts and rising participation in regional tournaments. Affordable gaming options and localized content are key drivers for market expansion in this area.

- Middle East and Africa (MEA): While currently a smaller market, MEA is experiencing rapid growth due to improving digital infrastructure, rising internet penetration, and increasing investment in gaming and esports. Countries like Saudi Arabia and the UAE are emerging as important hubs, with a youthful demographic eager for new entertainment options. The market is poised for expansion as gaming becomes more accessible and culturally integrated.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fighting Game Market.- Global Interactive Studios

- Digital Combat Entertainment

- Arcade Legends Inc.

- Ultimate Brawlers Games

- Quantum Combat Systems

- Visionary Fight Games

- Elite Battle Software

- NextGen Dojo Developers

- Pixel Punch Studios

- Iron Fist Entertainment

- Sonic Strike Games

- Zenith Arena Corporation

- Cybernetic Showdown LLC

- Mystic Combat Productions

- Vanguard Victor Studios

- Apex Duel Games

- Infinity Brawl Developers

- Grand Fighter Creations

- Neo Battle Systems

- Titan Clash Entertainment

Frequently Asked Questions

What is the projected growth rate for the Fighting Game market?

The Fighting Game market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, driven by esports, technological advancements, and evolving monetization.

How large is the Fighting Game market expected to be by 2033?

The Fighting Game market is estimated at USD 1.52 Billion in 2025 and is projected to reach USD 3.12 Billion by the end of the forecast period in 2033.

What are the primary drivers of growth in the Fighting Game market?

Key drivers include the burgeoning popularity of esports, continuous technological advancements in online play and graphics, increasing global gaming penetration, and the strategic use of character diversity and intellectual property crossovers.

How is AI impacting the Fighting Game market?

AI is significantly impacting fighting games through adaptive AI opponents for enhanced single-player experiences, improved matchmaking, robust anti-cheat systems, and potential for personalized training and development efficiencies.

Which regions are most significant for the Fighting Game market?

North America and Europe currently hold substantial market shares, while Asia Pacific (APAC) is projected to be the fastest-growing region due to its expansive mobile gaming market and increasing digital adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted