Patient Simulator Market

Patient Simulator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678149 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

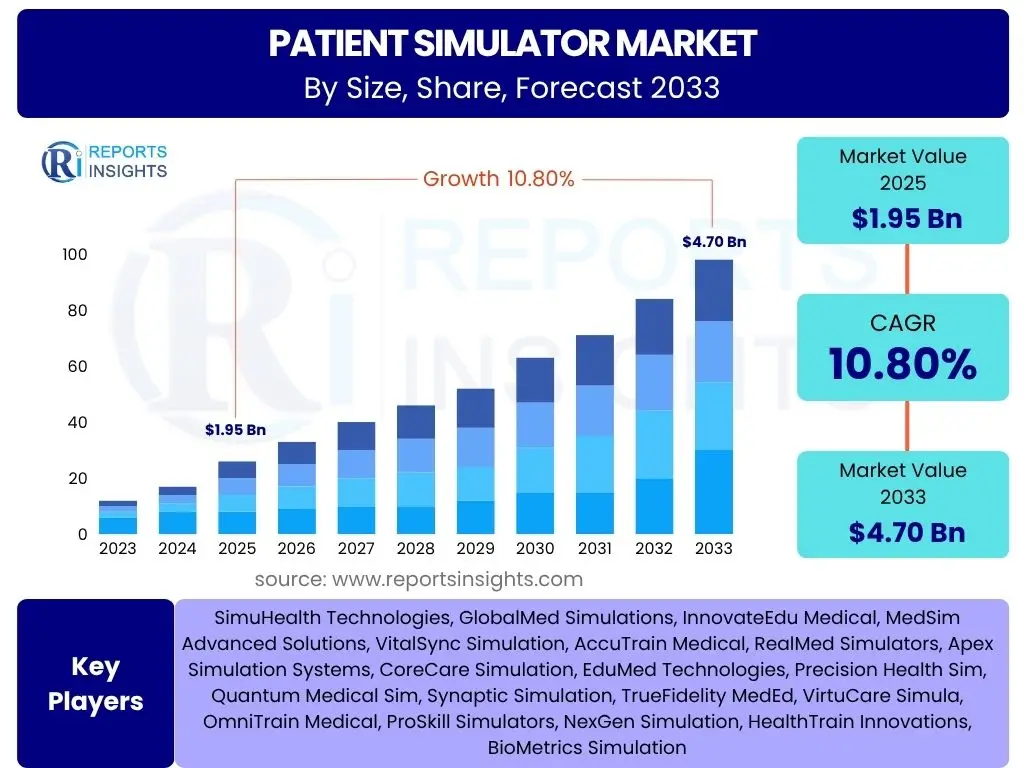

Patient Simulator Market is projected to grow at a Compound annual growth rate (CAGR) of 14.5% between 2025 and 2033, reaching USD 1.52 Billion in 2025 and is projected to grow by USD 4.52 Billion By 2033 the end of the forecast period.

Key Patient Simulator Market Trends & Insights

The patient simulator market is experiencing robust growth driven by the increasing emphasis on advanced medical training and education globally. Key trends include the integration of cutting-edge technologies, the rising adoption of simulation-based curricula in healthcare institutions, and a growing demand for realistic training environments. These factors are collectively shaping the evolution of the market, pushing manufacturers to innovate and provide more sophisticated and versatile simulation solutions.

Further insights reveal a strong focus on enhancing learner engagement and clinical competency through high-fidelity simulators that replicate complex medical scenarios. There is also a notable shift towards remote and blended learning models, which necessitates simulation solutions that can be deployed across various educational settings. The market is also seeing an expansion into new therapeutic areas and specialized training needs, moving beyond traditional emergency and surgical training to include areas like critical care, pharmacology, and interprofessional teamwork.

- Integration of advanced technologies like virtual reality (VR) and augmented reality (AR) for immersive training.

- Increasing adoption of simulation-based education in medical and nursing curricula worldwide.

- Growing demand for high-fidelity patient simulators that offer realistic physiological responses.

- Expansion of simulation training to cover a broader range of medical specialties and procedures.

- Shift towards remote and blended learning models driving demand for adaptable simulation solutions.

- Emphasis on interprofessional teamwork training using multi-patient simulation platforms.

- Development of task-specific trainers and hybrid simulation models for targeted skill acquisition.

AI Impact Analysis on Patient Simulator

Artificial intelligence (AI) is set to profoundly impact the patient simulator market by enhancing the realism, adaptability, and analytical capabilities of simulation platforms. AI can enable simulators to exhibit more dynamic and unpredictable physiological responses, mimicking real patient variability with greater precision. This allows for more challenging and comprehensive training scenarios, moving beyond pre-programmed responses to intelligent, adaptive interactions based on trainee actions and medical data.

The integration of AI also facilitates advanced performance analytics and personalized feedback for learners. AI algorithms can track and analyze trainee performance in real-time, identifying areas of strength and weakness, and providing tailored recommendations for improvement. This leads to more efficient and effective training outcomes, as instructors can leverage AI-driven insights to customize learning paths. Furthermore, AI can aid in the development of automated scenario generation, reducing the manual effort required to design diverse and complex training modules, thereby increasing the scalability and accessibility of high-quality simulation education.

- Enhanced realism and dynamic physiological responses in simulators through AI algorithms.

- Personalized feedback and adaptive learning paths based on trainee performance analysis.

- Automated generation of diverse and complex training scenarios, reducing manual effort.

- Improved diagnostic and decision-making training through intelligent patient responses.

- Integration of AI for predictive analytics on trainee competency and skill gaps.

- Development of AI-powered virtual patients for remote and accessible simulation.

- Optimization of simulation training effectiveness and efficiency through data-driven insights.

Key Takeaways Patient Simulator Market Size & Forecast

- The global Patient Simulator Market is poised for substantial expansion, reflecting growing investments in healthcare education and training infrastructure.

- Projected to achieve a significant Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033, indicating robust market momentum.

- Market valuation is estimated to be USD 1.52 Billion in 2025, serving as a strong base for future growth trajectory.

- By 2033, the market is forecasted to reach a value of USD 4.52 Billion, demonstrating nearly a threefold increase over the forecast period.

- This growth underscores the critical role of patient simulators in enhancing clinical skills, patient safety, and medical education standards.

- The forecast highlights increasing adoption across various healthcare settings, including medical schools, hospitals, and specialized training centers.

- Technological advancements and expanding applications are key drivers contributing to this optimistic market outlook.

Patient Simulator Market Drivers Impact Analysis

The patient simulator market is significantly propelled by several influential factors that underscore the growing necessity for advanced medical training. A primary driver is the increasing global emphasis on patient safety and quality of care, which mandates robust training solutions to mitigate medical errors and enhance clinical outcomes. This push for higher standards in healthcare delivery fuels the demand for realistic simulation platforms that allow practitioners to hone their skills in a safe, controlled environment without risk to actual patients.

Another pivotal driver is the continuous evolution of medical curricula and training methodologies, which are increasingly incorporating simulation-based learning as a core component. Regulatory bodies and accreditation agencies often recommend or mandate the use of simulation for professional development and certification, thereby institutionalizing its adoption. Furthermore, the rising incidence of chronic diseases and complex medical conditions necessitates highly skilled healthcare professionals, which simulation training effectively addresses by providing exposure to diverse clinical scenarios. The rapid pace of technological innovation in areas like virtual reality, haptics, and artificial intelligence also significantly contributes to market growth by enabling the development of more sophisticated, immersive, and effective patient simulators.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing emphasis on patient safety and quality of care | +3.2% | Global, especially North America and Europe | Short to Medium Term |

| Advancements in medical technology and simulation capabilities | +2.8% | Global, with strong adoption in developed regions | Medium to Long Term |

| Growing demand for minimally invasive procedures and complex surgeries | +2.5% | North America, Europe, Asia Pacific | Medium Term |

| Shift towards simulation-based medical education and training | +2.0% | Global, particularly academic institutions | Short to Medium Term |

| Shortage of skilled healthcare professionals and clinical training opportunities | +1.5% | Global, especially developing regions | Medium to Long Term |

| Rising healthcare expenditure and government support for medical training | +1.0% | Emerging economies, certain European countries | Long Term |

| Need for continuous professional development and competency assessment | +0.8% | Global | Ongoing |

Patient Simulator Market Restraints Impact Analysis

Despite the significant growth trajectory, the patient simulator market faces several restraints that could potentially impede its expansion. A primary limiting factor is the high initial cost associated with acquiring and implementing advanced patient simulators. These sophisticated devices, especially high-fidelity models, involve substantial investment, making them less accessible for smaller medical institutions, clinics, or healthcare facilities with limited budgets. This cost barrier can hinder broader adoption, particularly in developing regions where healthcare infrastructure funding may be constrained.

Another significant restraint is the extensive maintenance requirements and the need for specialized personnel to operate and troubleshoot these complex systems. The ongoing operational costs, including software updates, part replacements, and technician salaries, add to the total cost of ownership. Additionally, while simulation offers numerous benefits, the perception that it cannot fully replicate the unpredictable nature of real patient interactions and clinical environments can also be a restraint. Concerns about the lack of standardization in simulation training outcomes and the absence of a universally accepted framework for assessing competency through simulation further contribute to these challenges, potentially slowing down wider integration into core medical curricula.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial cost of advanced patient simulators | -2.5% | Global, more pronounced in developing regions | Short to Medium Term |

| Extensive maintenance and operational costs | -1.8% | Global | Ongoing |

| Lack of standardization in simulation training and assessment | -1.2% | Global, particularly academic and regulatory bodies | Medium Term |

| Limited availability of skilled instructors and technicians | -1.0% | Emerging markets, rural areas | Medium to Long Term |

| Perceived limitations of simulation compared to real clinical experience | -0.7% | Global | Long Term |

Patient Simulator Market Opportunities Impact Analysis

The patient simulator market is ripe with opportunities that can significantly accelerate its growth trajectory. One major opportunity lies in the expanding adoption of simulation in non-traditional healthcare settings, such as military medical training, emergency medical services (EMS), and specialized clinics. As these sectors increasingly recognize the benefits of realistic training for high-stakes situations, the demand for tailored simulation solutions will rise, opening new revenue streams for manufacturers.

Furthermore, the rapid advancements in digital technologies, including virtual reality (VR), augmented reality (AR), and artificial intelligence (AI), present immense opportunities for innovation. Integrating these technologies can lead to the development of more immersive, cost-effective, and highly customizable simulation experiences, broadening the market appeal beyond high-fidelity physical mannequins. There is also a substantial opportunity in developing simulation solutions for emerging economies, where healthcare infrastructure is rapidly developing, and there is a critical need for efficient and scalable training methods. Addressing the high initial cost challenge through subscription-based models, leasing options, or modular systems could unlock a vast, untapped market. Additionally, opportunities exist in developing specialized simulators for niche medical fields, like robotic surgery or personalized medicine, which require highly specific and advanced training protocols.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Virtual Reality (VR) and Augmented Reality (AR) for immersive training | +3.5% | Global, strong potential in developed and tech-savvy regions | Medium to Long Term |

| Expansion into non-traditional healthcare training sectors (e.g., EMS, military, home healthcare) | +2.8% | North America, Europe, Asia Pacific | Medium Term |

| Development of cost-effective and portable simulation solutions for broader accessibility | +2.0% | Emerging economies, smaller clinics | Medium to Long Term |

| Focus on specialized simulators for niche medical procedures and evolving therapies | +1.5% | Global, driven by medical innovation hubs | Long Term |

| Growing adoption of telerehabilitation and remote learning platforms | +1.2% | Global | Short to Medium Term |

Patient Simulator Market Challenges Impact Analysis

The patient simulator market, while promising, navigates several significant challenges that can influence its growth trajectory. A key challenge is the continuous need for technological upgrades and the high research and development costs associated with creating more sophisticated and realistic simulators. As medical procedures and patient conditions become increasingly complex, simulators must evolve rapidly, demanding significant investment in R&D to maintain relevance and efficacy. This rapid technological obsolescence can create a financial burden for both manufacturers and end-users.

Another challenge involves the integration of simulation-based training into existing, often rigid, medical curricula. Overcoming traditional teaching methodologies and securing faculty buy-in can be difficult, requiring substantial effort in curriculum redesign, faculty training, and demonstrating clear educational benefits. Furthermore, ensuring the validity and reliability of simulation as an assessment tool for clinical competency poses a significant hurdle. Developing standardized metrics and robust validation processes for simulation performance is crucial but remains an ongoing challenge. The global disparity in healthcare infrastructure and educational funding also presents a challenge, as it limits the uniform adoption of advanced simulation technology, particularly in resource-constrained regions, where the benefits of such training could be most impactful.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High research and development costs for advanced simulators | -2.0% | Global, impacts manufacturers primarily | Ongoing |

| Integration into established medical curricula and faculty resistance | -1.5% | Global, especially academic institutions | Medium Term |

| Ensuring pedagogical effectiveness and transferability of skills to real clinical settings | -1.0% | Global | Long Term |

| Cybersecurity risks and data privacy concerns with connected simulation systems | -0.8% | Global | Short to Medium Term |

| Rapid technological obsolescence and need for frequent upgrades | -0.7% | Global | Ongoing |

Patient Simulator Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Patient Simulator Market, providing critical insights into its current landscape, growth drivers, restraints, opportunities, and future projections. It covers detailed segmentation analysis, regional dynamics, competitive landscape, and key market trends, equipping stakeholders with actionable intelligence for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Report Name | Patient Simulator Market |

| Market Size in 2025 | USD 1.52 Billion |

| Market Forecast in 2033 | USD 4.52 Billion |

| Growth Rate | CAGR of 2025 to 2033 14.5% |

| Number of Pages | 250 |

| Key Companies Covered | Laerdal Medical, CAE Healthcare, Gaumard Scientific, 3B Scientific, Simulaids |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

:The Patient Simulator Market is meticulously segmented to provide a granular view of its various components, enabling a deeper understanding of market dynamics across different product types and application areas. This segmentation helps in identifying specific growth pockets and market opportunities within distinct categories, offering strategic insights for market participants. The market is primarily bifurcated by product type, encompassing simulators designed for various patient demographics and medical scenarios, and by application, focusing on the primary end-uses of these sophisticated training tools.

Understanding these segments allows for targeted market strategies and product development initiatives. For instance, the demand for adult patient simulators might differ significantly from infant simulators, influenced by disease prevalence, training requirements, and healthcare policies in various regions. Similarly, the specific features and functionalities required for simulators used in academic education may vary from those utilized in professional clinical training, impacting product design and marketing approaches. This detailed breakdown ensures that all facets of the patient simulator market are thoroughly explored, providing a holistic perspective for stakeholders.

Market by Order Type Segmentation:-

- Childbirth Simulator

- Adult Patient Simulator

- Infant Simulator

- Others

Market Application Segmentation:-

- Training

- Education

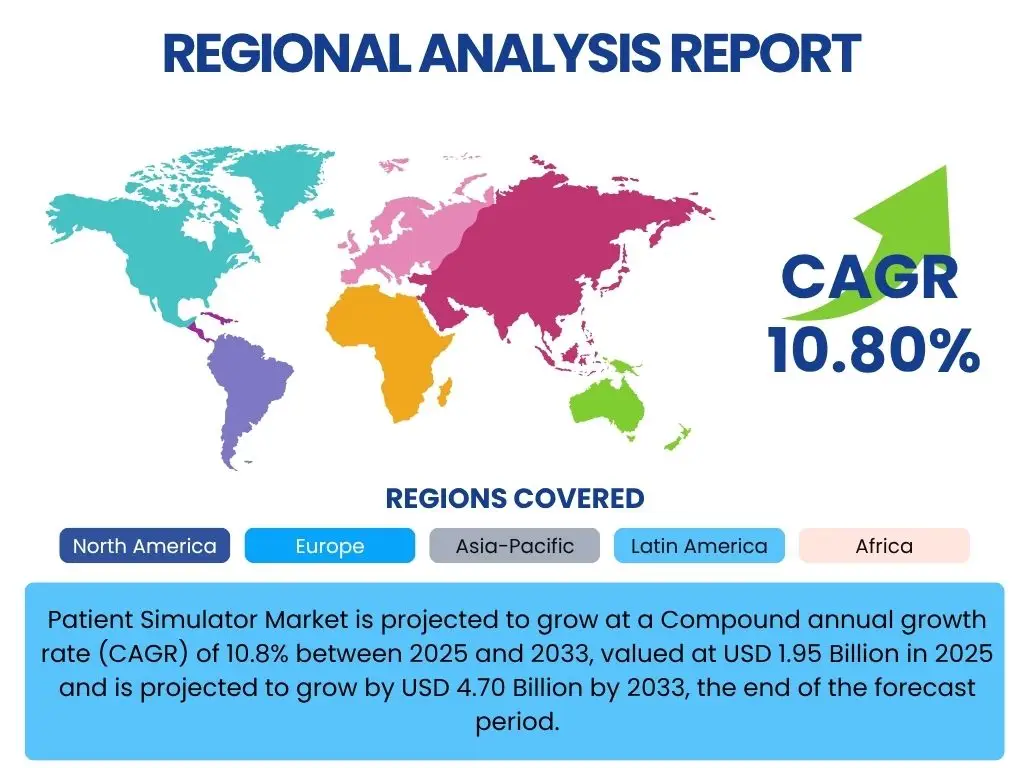

Regional Highlights

The global Patient Simulator Market exhibits significant regional variations, influenced by factors such as healthcare infrastructure development, investment in medical education, technological adoption rates, and regulatory frameworks. Each region presents unique growth opportunities and market dynamics that are crucial for market players to understand for effective geographical expansion and strategic resource allocation.

North America currently leads the Patient Simulator Market, largely driven by the presence of well-established medical and nursing schools, significant healthcare expenditure, and a strong emphasis on patient safety initiatives. The region also benefits from early adoption of advanced medical technologies and favorable government funding for simulation-based training. The United States, in particular, is a dominant force due to its robust healthcare system, extensive research and development activities, and a high concentration of key market players.

Europe stands as another prominent region in the patient simulator market, characterized by advanced healthcare systems and a growing focus on competency-based medical education. Countries like Germany, the United Kingdom, and France are key contributors, driven by strong academic and clinical simulation centers and supportive government policies aimed at enhancing clinical skills. The region's aging population also necessitates advanced training for complex medical conditions, further boosting market demand.

Asia Pacific is projected to be the fastest-growing region during the forecast period, primarily due to improving healthcare infrastructure, increasing awareness about simulation training benefits, and rising healthcare investments, especially in emerging economies like China and India. The large population base, coupled with a growing need for skilled healthcare professionals, is driving the adoption of patient simulators. Government initiatives to upgrade medical education standards and a burgeoning number of private healthcare facilities are also contributing to the region's rapid growth.

Latin America and the Middle East & Africa regions are also experiencing steady growth in the patient simulator market. In Latin America, countries such as Brazil and Mexico are investing in simulation centers to address critical healthcare training gaps and improve patient outcomes. The Middle East, particularly the GCC countries, is witnessing significant growth due to substantial investments in modernizing healthcare facilities and a strong focus on medical tourism, which necessitates high standards of care and highly trained professionals. Africa's growth, though slower, is spurred by international aid and local initiatives aimed at enhancing basic healthcare training and emergency response capabilities.

- North America is the leading region, driven by advanced medical infrastructure, high healthcare spending, and a strong emphasis on patient safety. The United States accounts for a significant share due to widespread adoption in academic and hospital settings.

- Europe holds a substantial market share, with countries like Germany and the UK at the forefront, propelled by well-established medical education systems and increasing integration of simulation in clinical training curricula.

- Asia Pacific is anticipated to be the fastest-growing market, primarily fueled by rising healthcare expenditure, improving medical infrastructure, and a growing demand for skilled healthcare professionals in populous nations such as China and India.

- Latin America demonstrates emerging growth, with countries like Brazil and Mexico investing in simulation centers to address critical healthcare training needs and improve clinical competencies.

- The Middle East and Africa are gradually increasing their adoption of patient simulators, spurred by healthcare modernization initiatives and a focus on enhancing medical education standards, particularly in Gulf Cooperation Council (GCC) countries.

Top Key Players:

The market research report covers the analysis of key stake holders of the Patient Simulator Market. Some of the leading players profiled in the report include -:- Laerdal Medical

- CAE Healthcare

- Gaumard Scientific

- 3B Scientific

- Simulaids

Frequently Asked Questions:

What is a patient simulator and why is it used in healthcare?

A patient simulator is an advanced technological tool designed to replicate human physiological responses and clinical conditions for medical training. It is used in healthcare to provide a safe, controlled, and realistic environment for medical students, nurses, and healthcare professionals to practice clinical skills, emergency procedures, communication techniques, and teamwork without risk to actual patients. This allows for hands-on learning, error practice, and skill mastery, ultimately improving patient safety and quality of care.

What are the main types of patient simulators available in the market?

The patient simulator market offers a diverse range of simulators categorized by patient demographics and complexity. The main types include adult patient simulators, infant simulators, childbirth simulators, and specialized task trainers. Adult patient simulators are comprehensive models replicating adult physiology, while infant and childbirth simulators focus on pediatric and obstetric scenarios, respectively. Task trainers are designed for specific procedures, such as IV insertion or airway management, offering targeted skill development.

How does AI impact the development of patient simulators?

Artificial intelligence significantly enhances patient simulators by enabling more realistic, dynamic, and adaptive learning experiences. AI allows simulators to exhibit unpredictable physiological responses, generate complex scenarios, and provide personalized feedback based on a learner's performance. This results in highly immersive and effective training environments that can analyze skill gaps, customize learning paths, and ultimately improve diagnostic and decision-making capabilities.

What are the key factors driving the growth of the patient simulator market?

The patient simulator market's growth is primarily driven by an increasing global emphasis on patient safety and quality healthcare outcomes, the widespread adoption of simulation-based medical education in curricula, and continuous advancements in medical technology. Additionally, the rising demand for minimally invasive procedures and the need for skilled healthcare professionals globally are significant contributing factors pushing market expansion.

What are the primary challenges faced by the patient simulator market?

Despite its growth, the patient simulator market faces challenges such as the high initial cost of acquiring advanced simulators and the ongoing expenses for maintenance and operation. Other challenges include the lack of standardized assessment methods for simulation training, the need for continuous technological upgrades due to rapid obsolescence, and difficulties in fully integrating simulation into traditional medical education frameworks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted