Passive Optical LAN Market

Passive Optical LAN Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704926 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Passive Optical LAN Market Size

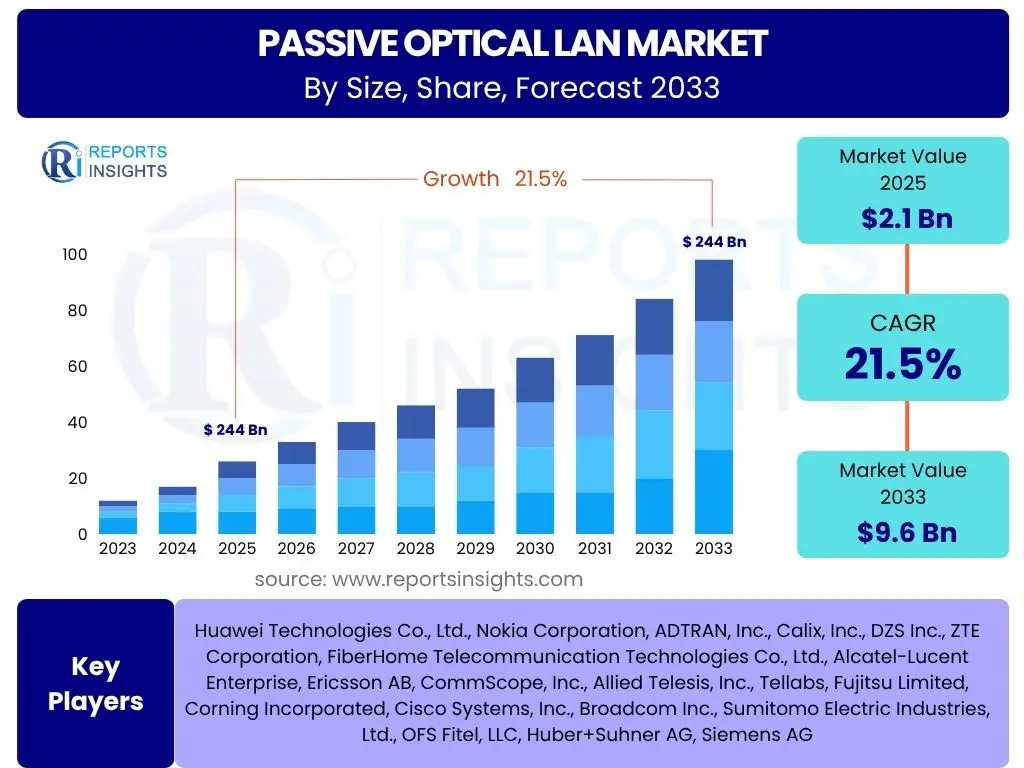

According to Reports Insights Consulting Pvt Ltd, The Passive Optical LAN Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

Key Passive Optical LAN Market Trends & Insights

The Passive Optical LAN (POL) market is experiencing significant transformation driven by the escalating demand for high-bandwidth, energy-efficient, and future-proof network infrastructure. Key inquiries from stakeholders often revolve around the technologies enabling greater speeds, the integration of new applications, and the long-term sustainability of POL solutions. A primary trend involves the adoption of GPON and XG-PON technologies, which provide enhanced bandwidth capabilities necessary for supporting emerging applications like 4K/8K video streaming, virtual reality (VR), and augmented reality (AR) in commercial and residential settings. The market is also witnessing a shift towards consolidated network architectures that leverage POL to reduce operational complexity and capital expenditures.

Furthermore, the increasing focus on sustainable and green IT solutions is propelling the adoption of POL due to its inherently lower power consumption compared to traditional copper-based Ethernet networks. Organizations are actively seeking solutions that align with their environmental, social, and governance (ESG) objectives, making POL an attractive option for new builds and network upgrades. There is a growing interest in how POL can support the proliferation of Internet of Things (IoT) devices and smart building technologies, which require robust and scalable connectivity at the edge. The simplified cabling and longer reach capabilities of POL systems are proving advantageous in these complex environments.

Another prominent trend is the convergence of various network services over a single fiber infrastructure. This includes voice, data, video, and building automation systems, all managed through a centralized optical line terminal (OLT). This integration streamlines network management, reduces infrastructure footprint, and enhances overall operational efficiency. The market is also seeing innovations in POL equipment, with vendors introducing more compact, modular, and software-defined solutions that offer greater flexibility and ease of deployment. These advancements are critical for meeting the diverse requirements of different end-user verticals, from commercial enterprises and data centers to hospitality and healthcare facilities.

- Escalating demand for high-bandwidth applications.

- Increased adoption of GPON and XG-PON technologies.

- Growing emphasis on energy efficiency and sustainability.

- Integration with IoT and smart building ecosystems.

- Convergence of voice, data, and video services over single fiber.

- Advancements in compact and software-defined POL equipment.

- Shift towards centralized network management and simplified cabling.

AI Impact Analysis on Passive Optical LAN

User inquiries regarding the impact of Artificial Intelligence (AI) on Passive Optical LAN primarily focus on how AI can enhance network performance, automate management tasks, and improve overall operational efficiency. There is significant interest in AI's potential to revolutionize network monitoring, fault detection, and predictive maintenance within POL environments. AI algorithms can analyze vast amounts of network data, identify anomalies, and anticipate potential issues before they lead to service disruptions, thereby minimizing downtime and optimizing network reliability. This proactive approach to network management is a key expectation for leveraging AI in POL systems.

The integration of AI also holds promise for optimizing resource allocation and capacity planning in POL networks. AI-driven analytics can provide insights into traffic patterns, user behavior, and resource utilization, enabling network administrators to dynamically adjust bandwidth allocation and ensure optimal performance for critical applications. This capability is particularly valuable in environments with fluctuating demand, such as large enterprises or educational institutions. Furthermore, AI can contribute to enhanced network security by identifying unusual traffic patterns or unauthorized access attempts, adding an intelligent layer of protection to the inherent security benefits of fiber optics.

Looking ahead, AI is expected to drive greater automation in POL deployment and configuration. AI-powered tools can simplify the provisioning of new services, automate firmware updates, and streamline network upgrades, significantly reducing the manual effort required for network operations. This automation not only improves efficiency but also reduces the potential for human error. While the full scope of AI's integration into POL is still evolving, the overarching theme is its potential to transform POL from a robust physical layer into an intelligent, self-optimizing, and highly resilient network infrastructure capable of adapting to future demands with minimal human intervention.

- Enhanced network monitoring and predictive maintenance.

- Automated fault detection and anomaly identification.

- Optimized resource allocation and dynamic bandwidth management.

- Improved network security through intelligent threat detection.

- Simplified deployment and configuration through automation.

- Insights into traffic patterns and user behavior for capacity planning.

Key Takeaways Passive Optical LAN Market Size & Forecast

Analysis of common user questions concerning the Passive Optical LAN (POL) market size and forecast consistently reveals a strong interest in the underlying drivers of growth, the resilience of the market against economic fluctuations, and the long-term viability of POL technology. A key takeaway is the robust and sustained growth trajectory anticipated for the POL market, driven by the insatiable demand for higher bandwidth and reliable connectivity across various sectors. The projected Compound Annual Growth Rate (CAGR) of 21.5% from 2025 to 2033 underscores the market's significant expansion, indicating a profound shift towards fiber-optic infrastructure in enterprise and public networks.

The forecast highlights that the market's expansion from USD 2.1 Billion in 2025 to USD 9.6 Billion by 2033 is not merely incremental but represents a substantial re-evaluation of network architectures in favor of POL's inherent advantages. This growth is fueled by factors such as the lower total cost of ownership (TCO) compared to traditional copper-based LANs, superior energy efficiency, extended reach capabilities, and enhanced security features. End-users are increasingly recognizing these benefits, leading to accelerated adoption in new construction projects and large-scale network modernization initiatives across commercial, residential, and industrial domains.

Furthermore, the market's resilience is attributed to its fundamental role in supporting the digital transformation initiatives of organizations globally, including the widespread adoption of cloud computing, IoT, and smart building technologies. The long-term forecast suggests that POL will continue to be a foundational technology for next-generation networks, providing a scalable and future-proof platform capable of accommodating ever-increasing data demands. The consistent growth trajectory indicates a positive investment climate and a clear market consensus on the strategic importance and sustained relevance of Passive Optical LAN solutions.

- Market exhibits robust and sustained double-digit growth.

- Significant expansion from USD 2.1 Billion (2025) to USD 9.6 Billion (2033).

- Growth driven by high bandwidth demand, TCO benefits, and energy efficiency.

- POL is a key enabler for digital transformation and smart infrastructure.

- Strong adoption in new builds and network modernization projects.

- Positive long-term viability and investment outlook for the technology.

Passive Optical LAN Market Drivers Analysis

The Passive Optical LAN (POL) market is propelled by a confluence of factors underscoring the shift towards high-performance, cost-effective, and sustainable network solutions. A primary driver is the exponentially increasing demand for bandwidth, necessitated by the proliferation of data-intensive applications, cloud computing, 4K/8K video, and IoT devices across all sectors. POL inherently provides superior bandwidth capacity and greater reach compared to traditional copper-based Ethernet, making it an ideal infrastructure for modern digital environments. Additionally, the growing emphasis on energy efficiency and green IT initiatives worldwide strongly favors POL due as it consumes significantly less power and has a longer lifespan, reducing operational expenditure and environmental impact. The simplified infrastructure, requiring less space and fewer active components, also contributes to reduced capital expenditure and easier maintenance, enhancing its appeal.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High Bandwidth | +5.0-6.5% | Global (North America, APAC, Europe) | 2025-2033 |

| Lower Total Cost of Ownership (TCO) | +4.0-5.5% | Global (All Regions) | 2025-2033 |

| Energy Efficiency and Green IT Initiatives | +3.5-4.5% | Europe, North America, Developed APAC | 2025-2033 |

| Longer Reach and Simplified Infrastructure | +2.5-3.5% | Large Campuses, Smart Cities (Global) | 2025-2033 |

| Enhanced Security Features | +1.5-2.0% | Government, Defense, Enterprises (Global) | 2025-2033 |

Passive Optical LAN Market Restraints Analysis

Despite its numerous advantages, the Passive Optical LAN market faces certain restraints that can temper its growth. A significant barrier is the initial capital expenditure (CAPEX) associated with deploying a new fiber optic infrastructure. While POL offers lower TCO in the long run, the upfront cost of fiber installation, specialized optical equipment, and skilled labor can be prohibitive for some organizations, particularly small and medium-sized enterprises (SMEs) with limited budgets. Another restraint is the perceived lack of widespread awareness and standardization compared to ubiquitous Ethernet technologies. Many IT professionals and decision-makers are more familiar with traditional copper-based networking, leading to inertia or hesitation in adopting new optical technologies. Furthermore, integrating POL with existing legacy systems can present technical complexities and compatibility challenges, requiring careful planning and potentially significant investment in migration strategies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -2.0-3.0% | Developing Regions, SMEs (Global) | 2025-2028 |

| Lack of Widespread Awareness/Standardization | -1.5-2.5% | Global (especially smaller markets) | 2025-2027 |

| Compatibility Issues with Legacy Systems | -1.0-2.0% | Mature Markets with Existing Infrastructure | 2025-2029 |

Passive Optical LAN Market Opportunities Analysis

The Passive Optical LAN (POL) market is ripe with opportunities driven by expanding technological landscapes and evolving infrastructure needs. A significant opportunity lies in the burgeoning smart city initiatives and the rapid rollout of 5G networks globally. POL can serve as a robust and efficient backhaul infrastructure for 5G small cells and interconnected smart city components, providing the necessary bandwidth and reliability for next-generation urban environments. The expansion into new vertical markets such as healthcare, hospitality, education, and large-scale residential developments also presents substantial growth avenues, as these sectors increasingly require high-performance, scalable, and energy-efficient network solutions to support specialized applications and a high density of users. Furthermore, government initiatives and funding for digital infrastructure upgrades, particularly in regions striving to enhance broadband connectivity and economic competitiveness, offer considerable impetus for POL adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Smart City Initiatives and 5G Backhaul | +4.0-5.0% | Asia Pacific, North America, Europe | 2026-2033 |

| Expansion into New Vertical Markets (Healthcare, Hospitality) | +3.5-4.5% | Global (Emerging Economies) | 2025-2033 |

| Government Funding for Digital Infrastructure | +2.5-3.5% | North America, Europe, China, India | 2025-2030 |

| Need for Future-Proof Network Architectures | +2.0-3.0% | Global (Enterprises, Data Centers) | 2025-2033 |

Passive Optical LAN Market Challenges Impact Analysis

The Passive Optical LAN market faces several challenges that require strategic navigation for sustained growth. One key challenge is the shortage of skilled professionals capable of designing, deploying, and maintaining fiber optic networks. The specialized nature of optical fiber installation, splicing, and testing requires specific expertise that is not as readily available as traditional copper-based networking skills, potentially slowing down adoption rates. Another significant challenge is the ongoing competition from established and evolving traditional Ethernet solutions, which continue to innovate and offer higher speeds, albeit with different architectural complexities and limitations. Persuading organizations to shift from familiar Ethernet infrastructure to a new POL paradigm often requires compelling demonstrations of long-term benefits and ROI. Furthermore, the risk of technological obsolescence, while lower than copper, still exists with rapid advancements in optical standards (e.g., from GPON to XG-PON to NG-PON2 and beyond), necessitating continuous investment in research and development and ensuring backward compatibility.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Workforce for Fiber Deployment | -1.5-2.5% | Global (especially developing countries) | 2025-2030 |

| Competition from Traditional Ethernet Solutions | -1.0-2.0% | Global (Mature IT Markets) | 2025-2033 |

| High-Risk Aversion for New Technology Adoption | -0.8-1.5% | Conservative Industries (Global) | 2025-2028 |

| Ensuring Interoperability Between Vendors | -0.5-1.0% | Global | 2025-2033 |

Passive Optical LAN Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Passive Optical LAN (POL) market, providing an in-depth analysis of its current landscape, growth drivers, restraints, opportunities, and challenges. The scope encompasses a detailed examination of market size and forecast from 2025 to 2033, broken down by various segments and key regional geographies. It highlights the technological trends shaping the market, including the impact of emerging technologies like AI, and provides a competitive analysis of key players. The report offers actionable insights for stakeholders seeking to understand market potential, strategic imperatives, and future growth trajectories within the POL ecosystem, aiding informed decision-making for investment and market penetration strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Huawei Technologies Co., Ltd., Nokia Corporation, ADTRAN, Inc., Calix, Inc., DZS Inc., ZTE Corporation, FiberHome Telecommunication Technologies Co., Ltd., Alcatel-Lucent Enterprise, Ericsson AB, CommScope, Inc., Allied Telesis, Inc., Tellabs, Fujitsu Limited, Corning Incorporated, Cisco Systems, Inc., Broadcom Inc., Sumitomo Electric Industries, Ltd., OFS Fitel, LLC, Huber+Suhner AG, Siemens AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Passive Optical LAN (POL) market is comprehensively segmented to provide granular insights into its diverse components, applications, and end-user verticals, allowing for a thorough understanding of market dynamics and opportunities. This segmentation helps identify specific growth pockets and demand patterns across different industry sectors and geographical regions. By analyzing each segment independently and in conjunction with others, stakeholders can pinpoint lucrative areas for investment, tailor their product offerings, and devise targeted market entry or expansion strategies.

The component segment, comprising Optical Line Terminals (OLTs), Optical Network Terminals (ONTs), optical splitters, and optical fiber and cables, forms the backbone of POL infrastructure. Understanding the demand and technological advancements within each component is crucial for manufacturers and suppliers. The application segment, including Fiber to the Home (FTTH), Fiber to the Business (FTTB), and Fiber to the Desk (FTTD), illustrates the varied deployment scenarios and the versatility of POL across different user environments, from residential broadband to enterprise connectivity. Each application serves distinct needs, with unique technical and economic considerations driving adoption.

The end-user segment is particularly vital, encompassing commercial enterprises, residential developments, industrial facilities, government and public sectors, healthcare, hospitality, and education. This detailed breakdown highlights how POL addresses the specific networking requirements of diverse industries, from high-security government installations to high-bandwidth academic campuses. The varying data traffic, security needs, and scalability demands of these end-users shape the type and scale of POL solutions deployed. Regional segmentation further refines this analysis, accounting for differences in infrastructure development, regulatory environments, and technological adoption rates across North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

- By Component: Optical Line Terminal (OLT), Optical Network Terminal (ONT), Optical Splitters, Optical Fiber and Cables, Others.

- By Application: Fiber to the Home (FTTH), Fiber to the Business (FTTB), Fiber to the Curb (FTTC), Fiber to the Desk (FTTD), Fiber to the X (FTTx) Backhaul.

- By End-User: Commercial (Enterprises, Data Centers, Offices), Residential, Industrial, Government and Public Sector, Healthcare, Hospitality, Education.

- By Region: North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA).

Regional Highlights

The global Passive Optical LAN (POL) market exhibits varied adoption rates and growth trajectories across different regions, largely influenced by infrastructure maturity, digital transformation initiatives, and government policies. North America stands as a significant market, driven by its early adoption of advanced networking technologies and a strong emphasis on smart building initiatives and data center upgrades. The region sees substantial investment in POL solutions for commercial enterprises, healthcare facilities, and educational institutions, aiming for higher bandwidth and reduced operational costs. The presence of key technology providers and a mature IT ecosystem further fuels market expansion here, with a growing focus on energy efficiency and network security.

Asia Pacific (APAC) emerges as the fastest-growing region in the POL market, propelled by rapid urbanization, extensive infrastructure development, and burgeoning smart city projects, particularly in countries like China, India, Japan, and South Korea. Governments across APAC are heavily investing in digital infrastructure to support economic growth and expand broadband access, creating a robust demand for fiber optic networks. The large-scale deployment of FTTH/B in many APAC countries also provides a strong foundation for POL adoption in the enterprise and residential sectors. This region is witnessing a rapid pace of new construction and network upgrades, making it a pivotal area for POL market expansion.

Europe also demonstrates consistent growth in the POL market, driven by stringent energy efficiency regulations, increasing demand for sustainable IT solutions, and ongoing efforts to upgrade aging network infrastructures. Countries within the European Union are pushing for widespread fiber broadband connectivity, aligning with the benefits offered by POL in terms of TCO and environmental impact. While the market in Latin America and the Middle East and Africa (MEA) is still nascent, it presents significant untapped potential. Digitalization efforts, infrastructure investments, and the rising demand for high-speed internet in these regions are expected to drive future POL adoption, particularly in commercial and public sector applications as these economies mature and prioritize advanced networking capabilities.

- North America: Leading market due to early adoption, smart building trends, and data center modernization.

- Asia Pacific (APAC): Fastest-growing region, driven by rapid urbanization, smart city projects, and government investments in digital infrastructure, particularly in China and India.

- Europe: Consistent growth propelled by energy efficiency mandates, sustainability goals, and network modernization efforts.

- Latin America & MEA: Emerging markets with significant growth potential driven by increasing digitalization and infrastructure development projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Passive Optical LAN Market.- Huawei Technologies Co., Ltd.

- Nokia Corporation

- ADTRAN, Inc.

- Calix, Inc.

- DZS Inc.

- ZTE Corporation

- FiberHome Telecommunication Technologies Co., Ltd.

- Alcatel-Lucent Enterprise

- Ericsson AB

- CommScope, Inc.

- Allied Telesis, Inc.

- Tellabs

- Fujitsu Limited

- Corning Incorporated

- Cisco Systems, Inc.

- Broadcom Inc.

- Sumitomo Electric Industries, Ltd.

- OFS Fitel, LLC

- Huber+Suhner AG

- Siemens AG

Frequently Asked Questions

Analyze common user questions about the Passive Optical LAN market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Passive Optical LAN (POL)?

Passive Optical LAN (POL) is a fiber-optic based local area network (LAN) architecture that utilizes Passive Optical Network (PON) technology to deliver high-speed data, voice, and video services over a single fiber optic cable. Unlike traditional copper-based Ethernet LANs, POL eliminates the need for active electronics between the central optical line terminal (OLT) and the optical network terminals (ONTs) at the user end, relying on passive optical splitters to distribute signals, which enhances energy efficiency and simplifies infrastructure.

What are the primary benefits of deploying POL over traditional Ethernet LANs?

POL offers several key advantages including significantly higher bandwidth capacity (supporting multi-gigabit speeds), reduced infrastructure footprint due to less cabling and fewer active components, and substantial energy savings as passive components require no power. It also provides a longer reach, extending connections up to 20 kilometers, and enhances security because optical fiber does not emit electromagnetic signals and is difficult to tap without detection. These benefits translate to lower total cost of ownership (TCO) and a more future-proof network infrastructure.

Which industries and applications are best suited for Passive Optical LAN?

Passive Optical LAN is highly suitable for various industries and applications requiring high bandwidth, long reach, and energy efficiency. Key sectors include large commercial enterprises, data centers, healthcare facilities, hospitality venues (hotels, resorts), educational campuses, and government buildings. Applications range from general office connectivity and Wi-Fi backhaul to supporting specialized systems like building automation, security cameras, point-of-sale systems, and converged voice, video, and data services over a single network.

How does Passive Optical LAN contribute to sustainability and green IT initiatives?

POL significantly contributes to sustainability by being inherently more energy-efficient than copper-based LANs. It uses passive optical splitters that require no power, leading to lower electricity consumption for cooling and operations. Furthermore, fiber optic cables have a longer lifespan, are made from abundant glass, and their compact size reduces the amount of raw materials needed for cabling, thereby minimizing environmental impact and aligning with corporate green IT and environmental, social, and governance (ESG) objectives.

What are the future prospects for the Passive Optical LAN market?

The future prospects for the Passive Optical LAN market are robust, driven by the increasing global demand for pervasive, high-speed connectivity and the ongoing digital transformation across industries. The market is expected to continue its strong growth trajectory, fueled by advancements in PON technologies like XG-PON and NG-PON2, the proliferation of IoT devices, and the increasing adoption of smart building and smart city initiatives. POL's inherent scalability, energy efficiency, and long-term cost benefits position it as a foundational technology for next-generation wired and wireless networks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted