Passive Fire Protection Market

Passive Fire Protection Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705153 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

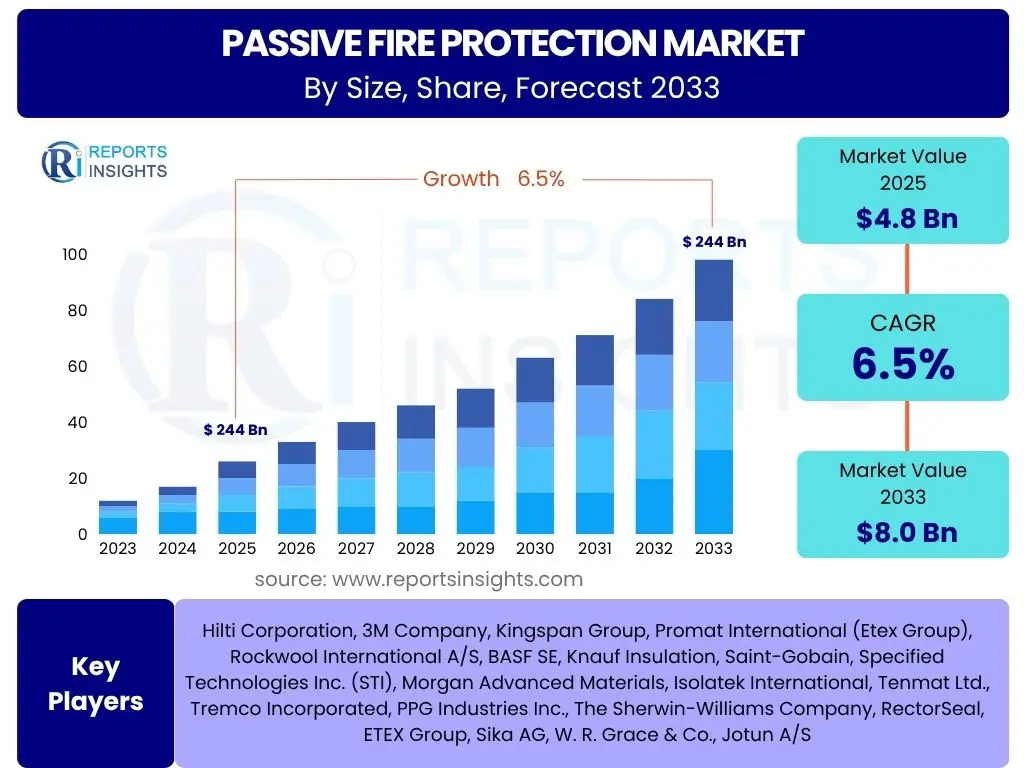

Passive Fire Protection Market Size

According to Reports Insights Consulting Pvt Ltd, The Passive Fire Protection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 8.0 Billion by the end of the forecast period in 2033.

Key Passive Fire Protection Market Trends & Insights

The Passive Fire Protection (PFP) market is currently undergoing significant transformation driven by evolving regulatory landscapes, technological advancements, and a heightened emphasis on building safety. User inquiries frequently highlight a keen interest in how new technologies are integrating with traditional PFP methods and the push for more sustainable and efficient solutions. There is a clear trend towards smart PFP systems, which leverage sensors and IoT for enhanced monitoring and early detection capabilities. Furthermore, the global increase in construction activities, particularly in emerging economies, is fueling demand for comprehensive and compliant fire safety solutions, influencing material innovation and application techniques.

Another prominent trend observed is the growing adoption of intumescent coatings and advanced firestopping materials that offer superior fire resistance and flexibility in application. The market is also seeing a shift towards modular and prefabricated construction methods, which necessitate PFP solutions that can be integrated efficiently during the off-site assembly process. Furthermore, environmental considerations are leading to increased research and development in sustainable and low-VOC (Volatile Organic Compound) passive fire protection products, aligning with green building initiatives and broader environmental safety standards. The push for retrofitting existing structures to meet updated fire safety codes also represents a substantial area of market activity.

- Stringent and evolving building codes and safety regulations globally.

- Integration of smart technologies, IoT, and sensors for enhanced monitoring.

- Increasing adoption of sustainable and environmentally friendly PFP materials.

- Growing demand from the construction industry, especially for high-rise and complex structures.

- Technological advancements in intumescent coatings and firestopping solutions.

- Focus on modular and prefabricated PFP components for efficient installation.

- Rising awareness regarding the importance of fire safety in both residential and commercial buildings.

AI Impact Analysis on Passive Fire Protection

Common user questions regarding AI's impact on Passive Fire Protection often revolve around its potential to enhance safety, improve efficiency, and streamline design and maintenance processes. Users are curious about how artificial intelligence can move PFP beyond static installations into a more dynamic and predictive safety framework. AI's capabilities in data analysis, pattern recognition, and predictive modeling hold significant promise for transforming traditional PFP by offering real-time insights into system integrity and potential vulnerabilities. This allows for more proactive maintenance and more informed design decisions, moving from reactive responses to preventative measures.

AI is poised to revolutionize PFP through predictive analytics for material degradation, optimizing fire safety design through complex simulations, and automating compliance checks. Furthermore, AI-powered systems can analyze vast amounts of data from integrated building management systems to identify anomalous behavior or potential fire hazards, providing early warnings that human systems might miss. While the integration of AI presents opportunities for unprecedented levels of safety and efficiency, concerns include data security, the cost of implementation, and the need for specialized expertise to manage and interpret AI-driven insights. However, the long-term benefits in terms of life safety and asset protection are expected to outweigh these initial challenges, fostering a new era of intelligent passive fire protection.

- Predictive maintenance and fault detection in PFP systems using AI algorithms.

- Optimized design and simulation of fire compartmentation through AI-driven analytics.

- Enhanced monitoring and real-time risk assessment by analyzing sensor data.

- Automation of compliance checks and regulatory adherence for PFP installations.

- Improved material science and product development through AI-guided research.

- More efficient installation planning and resource allocation through predictive modeling.

- Advanced training simulations for fire safety personnel using AI-driven scenarios.

Key Takeaways Passive Fire Protection Market Size & Forecast

Analysis of common user questions regarding the Passive Fire Protection market size and forecast reveals a consistent focus on understanding the primary drivers of growth, the resilience of the market against economic fluctuations, and the long-term sustainability of demand. Users are particularly interested in identifying the sectors and regions that will contribute most significantly to market expansion. The key takeaway is the robust and sustained growth trajectory of the PFP market, primarily propelled by increasingly stringent global fire safety regulations and the rapid expansion of the construction industry, especially in developing economies. The forecast indicates that while traditional PFP solutions remain foundational, significant growth will also stem from the adoption of innovative materials and integrated smart safety systems.

Furthermore, the market's resilience is underscored by its essential role in building safety and infrastructure resilience, making it less susceptible to economic downturns compared to other construction-related sectors. The imperative to protect human lives and assets ensures a continuous demand for effective passive fire protection measures across all building types and industrial applications. The integration of advanced technologies and the emphasis on sustainable solutions are not merely trends but fundamental shifts that will define the market's evolution, presenting substantial opportunities for innovation and market penetration. This dynamic environment suggests a positive outlook, with a continuous need for compliance, upgrading, and expansion of PFP infrastructure globally.

- The market is poised for consistent growth, driven by an escalating global focus on fire safety and stringent building codes.

- Significant opportunities exist in emerging economies due to rapid urbanization and infrastructure development.

- Technological innovation, particularly in smart PFP and sustainable materials, is a critical growth enabler.

- Residential, commercial, and industrial construction sectors are primary demand generators for PFP solutions.

- Retrofitting existing structures to meet updated fire safety standards presents a substantial market segment.

- The market's stability is bolstered by the non-negotiable nature of fire safety, making it less vulnerable to economic volatility.

Passive Fire Protection Market Drivers Analysis

The Passive Fire Protection market is significantly driven by a confluence of factors, primarily strict regulatory frameworks and the expanding global construction sector. Governments and regulatory bodies worldwide are continually updating and enforcing more stringent building codes and fire safety standards in response to increasing urbanization, population density, and high-profile fire incidents. These regulations mandate the incorporation of passive fire protection measures in new constructions and often require upgrades in existing structures, thereby creating a sustained and non-discretionary demand for PFP products and services. The essential nature of these safety measures ensures consistent market expansion, regardless of minor economic fluctuations.

Beyond regulatory impetus, the rapid growth in infrastructure and commercial development, particularly in Asia Pacific and Latin America, serves as a strong market driver. As countries invest heavily in new commercial complexes, residential buildings, industrial facilities, and public infrastructure, the demand for comprehensive fire safety solutions, including passive components, naturally escalates. Additionally, increasing public awareness regarding the importance of fire safety and the potential for devastating losses from fires is influencing building owners and developers to prioritize robust PFP installations, moving beyond mere compliance to proactive safety enhancements. This heightened awareness further contributes to market growth by fostering demand for higher quality and more technologically advanced PFP solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Building Codes and Regulations | +1.8% | Global, particularly Europe, North America, rapidly evolving in APAC | Long-term |

| Growing Construction and Infrastructure Development | +1.5% | Asia Pacific, Middle East & Africa, Latin America | Medium-term to Long-term |

| Increasing Fire Incidences and Public Awareness | +1.2% | Global | Short-term to Medium-term |

| Technological Advancements in PFP Materials | +1.0% | Global, especially developed regions | Medium-term |

| Urbanization and Rise in High-Rise Structures | +0.8% | Global, concentrated in developing economies | Long-term |

Passive Fire Protection Market Restraints Analysis

Despite robust growth drivers, the Passive Fire Protection market faces several significant restraints that could impede its expansion. One of the primary limitations is the high initial installation cost associated with certain advanced PFP systems and materials. While these systems offer long-term benefits in terms of safety and asset protection, the upfront investment can be substantial, particularly for smaller projects or in regions with limited budget allocations for construction. This cost factor can sometimes lead to developers opting for cheaper, less effective solutions or delaying necessary upgrades, thereby slowing market penetration and growth for premium products.

Another notable restraint is the lack of awareness and perceived value in some developing regions. In many areas, fire safety is not always prioritized or understood adequately by stakeholders, leading to a reactive approach rather than a proactive investment in PFP. This results in minimal adoption of passive fire protection measures beyond basic regulatory requirements, if any. Furthermore, the complexity of installing and integrating diverse PFP components, along with a shortage of skilled labor trained in specialized PFP techniques, poses operational challenges. The proper application of firestopping, intumescent coatings, and compartmentation is critical for their effectiveness, and a lack of skilled professionals can lead to faulty installations, reducing overall system reliability and increasing long-term risks. Lastly, volatility in raw material prices can impact manufacturing costs and, subsequently, the final product prices, potentially affecting market affordability and demand.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Installation and Material Costs | -1.3% | Global, more pronounced in developing regions | Medium-term |

| Lack of Awareness and Enforcement in Developing Regions | -1.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Complexity of Installation and Skilled Labor Shortage | -0.9% | Global | Short-term to Medium-term |

| Volatility in Raw Material Prices | -0.7% | Global | Short-term |

| Perceived Lack of Return on Investment | -0.5% | Global | Medium-term |

Passive Fire Protection Market Opportunities Analysis

The Passive Fire Protection market is ripe with opportunities, primarily stemming from the increasing focus on smart building integration and the growing demand for sustainable construction materials. The convergence of PFP systems with building management systems (BMS) and IoT technologies presents a significant avenue for innovation. Smart PFP solutions, which can provide real-time monitoring of fire integrity, alert systems to potential breaches, and even automate responses, are becoming increasingly attractive. This integration enhances overall building safety and operational efficiency, offering a premium segment for manufacturers and service providers. The drive towards smart cities and interconnected infrastructure further amplifies this opportunity, as PFP becomes an integral component of a comprehensive smart safety ecosystem.

Another major opportunity lies in the burgeoning trend of green building and sustainable construction. There is a growing preference for environmentally friendly materials that not only meet fire safety standards but also contribute to energy efficiency and reduce environmental impact. This includes the development and adoption of low-VOC coatings, recycled content insulation, and fire-resistant materials with reduced carbon footprints. Furthermore, the vast market for retrofitting existing, older structures to comply with contemporary fire safety regulations represents a continuous and substantial revenue stream. Many legacy buildings were constructed before current stringent codes were in place, necessitating extensive upgrades to their passive fire protection systems. This area provides consistent demand, especially in developed economies with aging infrastructure, allowing for continuous product and service innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart Building Technologies and IoT | +1.6% | Global, particularly North America, Europe, East Asia | Medium-term to Long-term |

| Growing Demand for Green and Sustainable Building Materials | +1.3% | Global, strong in Europe, North America | Medium-term to Long-term |

| Retrofitting and Renovation of Existing Structures | +1.1% | Developed economies (North America, Europe, Japan) | Long-term |

| Expansion into Emerging Markets and Specialized Applications | +0.9% | Asia Pacific, Latin America, Middle East & Africa, Marine, Oil & Gas | Medium-term |

| Development of Advanced Modular PFP Solutions | +0.7% | Global | Medium-term |

Passive Fire Protection Market Challenges Impact Analysis

The Passive Fire Protection market faces several critical challenges that can impede its growth and widespread adoption. One significant challenge is the complex and often varied nature of regulatory compliance across different regions and countries. While regulations drive demand, their inconsistency and frequent updates can create hurdles for manufacturers and installers trying to operate globally or across diverse jurisdictions. Ensuring products meet multiple standards and obtaining necessary certifications can be time-consuming and costly, potentially limiting market entry for new innovators or increasing operational overheads for established players. This regulatory fragmentation necessitates substantial investment in compliance management and product adaptation.

Another substantial challenge is the proliferation of counterfeit or substandard PFP products in the market. These inferior products often fail to meet performance specifications, leading to severe safety risks and undermining the credibility of legitimate manufacturers. Detecting and preventing the entry of such products into the supply chain is difficult, and their lower prices can distort market competition, putting pressure on compliant manufacturers. Furthermore, the global supply chain for PFP materials can be vulnerable to disruptions, as evidenced by recent events such as pandemic-related factory shutdowns or geopolitical conflicts affecting raw material availability and transportation. Such disruptions can lead to material shortages, increased costs, and project delays, impacting the overall market's stability and growth. Addressing these challenges requires concerted efforts from industry stakeholders, regulators, and enforcement agencies to maintain market integrity and safety standards.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Evolving Regulatory Landscape | -1.2% | Global | Long-term |

| Presence of Counterfeit or Substandard Products | -1.0% | Global, particularly developing markets | Medium-term |

| Supply Chain Disruptions and Raw Material Volatility | -0.8% | Global | Short-term to Medium-term |

| Lack of Standardized Installation Practices | -0.7% | Global | Medium-term |

| Economic Downturns Affecting Construction Activity | -0.6% | Global, varies by region | Short-term |

Passive Fire Protection Market - Updated Report Scope

This comprehensive market research report on the Passive Fire Protection market offers an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report provides a strategic outlook on the industry's growth trajectory, offering detailed insights into market dynamics from historical data to future projections. It also includes an extensive profiling of leading market players, competitive landscape analysis, and a thorough examination of the impact of emerging technologies such as Artificial Intelligence on the sector. The scope is designed to provide stakeholders with actionable intelligence for informed decision-making and strategic planning within the evolving passive fire protection landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.0 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hilti Corporation, 3M Company, Kingspan Group, Promat International (Etex Group), Rockwool International A/S, BASF SE, Knauf Insulation, Saint-Gobain, Specified Technologies Inc. (STI), Morgan Advanced Materials, Isolatek International, Tenmat Ltd., Tremco Incorporated, PPG Industries Inc., The Sherwin-Williams Company, RectorSeal, ETEX Group, Sika AG, W. R. Grace & Co., Jotun A/S |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Passive Fire Protection market is extensively segmented to provide a granular understanding of its diverse components and their respective market dynamics. These segments allow for a detailed analysis of product types, application areas, end-use sectors, and materials, offering insights into market preferences and growth opportunities. Understanding these distinct segments is crucial for stakeholders to tailor their strategies, develop targeted products, and effectively penetrate specific market niches, ensuring comprehensive fire safety solutions are deployed where most needed. Each segmentation category reflects distinct market drivers, technological requirements, and regulatory considerations, contributing to a multifaceted market landscape.

- By Type

- Firestopping Materials (Sealants, Mortars, Collars, Wraps)

- Intumescent Coatings (Water-based, Solvent-based, Epoxy-based)

- Fire-Resistant Boards (Gypsum Boards, Vermiculite Boards, Mineral Wool Boards)

- Fire Doors (Timber, Steel, Glazed)

- Fire-Resistant Glazing (Wired Glass, Ceramic Glass, Borosilicate Glass)

- Fire Dampers (Static, Dynamic)

- Structural Steel Protection (Spray, Board, Coatings)

- By Application

- Commercial Buildings (Offices, Retail, Healthcare, Educational Institutions, Hotels)

- Residential Buildings (Single-Family, Multi-Family, High-Rise)

- Industrial Facilities (Manufacturing Plants, Warehouses, Power Plants)

- Infrastructure & Transportation (Tunnels, Airports, Railways, Roads)

- Oil & Gas (Refineries, Offshore Platforms, Storage Facilities)

- By End-Use

- New Construction

- Retrofit & Renovation

- By Material

- Cementitious Materials

- Gypsum-based Materials

- Mineral Wool

- Fiberglass

- Foams

- Coatings

- Sealants

Regional Highlights

- North America: This region is characterized by stringent building codes and a high awareness of fire safety. Significant investments in infrastructure development, coupled with a focus on smart building technologies, drive the adoption of advanced PFP solutions. The market is mature, with a strong emphasis on continuous innovation and compliance with evolving safety standards.

- Europe: Similar to North America, Europe has well-established and rigorous fire safety regulations. The region is a leader in adopting sustainable and environmentally friendly PFP materials. Renovation and retrofitting projects for older buildings, along with the growth of sustainable construction, are key market drivers. Germany, the UK, and France are significant contributors.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region due to rapid urbanization, massive infrastructure projects, and increasing awareness of fire safety, particularly in China, India, Japan, and Southeast Asian countries. The booming construction sector across residential, commercial, and industrial segments fuels substantial demand for PFP products.

- Latin America: This region presents emerging opportunities, driven by increasing foreign investments in construction and a gradual improvement in regulatory enforcement. While still developing, countries like Brazil and Mexico are showing increased demand for PFP as their building standards evolve and economic growth supports new construction.

- Middle East and Africa (MEA): The MEA market is witnessing significant growth, primarily due to large-scale infrastructure projects, mega-city developments, and stricter fire safety regulations being adopted in the Gulf Cooperation Council (GCC) countries. The demand is concentrated in commercial and residential high-rise constructions, as well as oil and gas facilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Passive Fire Protection Market.- Hilti Corporation

- 3M Company

- Kingspan Group

- Promat International (Etex Group)

- Rockwool International A/S

- BASF SE

- Knauf Insulation

- Saint-Gobain

- Specified Technologies Inc. (STI)

- Morgan Advanced Materials

- Isolatek International

- Tenmat Ltd.

- Tremco Incorporated

- PPG Industries Inc.

- The Sherwin-Williams Company

- RectorSeal

- ETEX Group

- Sika AG

- W. R. Grace & Co.

- Jotun A/S

Frequently Asked Questions

Analyze common user questions about the Passive Fire Protection market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Passive Fire Protection?

Passive Fire Protection (PFP) involves using fire-resistant materials and designs to compartmentalize a building, limiting the spread of fire and smoke. It includes elements like fire-rated walls, doors, floors, and coatings that provide structural integrity and occupant safety during a fire.

Why is Passive Fire Protection important?

PFP is crucial for life safety and property protection by containing fires, slowing their spread, and allowing occupants more time to evacuate safely. It also protects critical assets and structural integrity, minimizing damage and facilitating safer fire-fighting operations.

What are the main types of Passive Fire Protection products?

Key PFP product types include firestopping materials (sealants, collars), intumescent coatings, fire-resistant boards, fire doors, fire-rated glazing, and fire dampers, all designed to create barriers against fire and smoke.

How do regulations impact the Passive Fire Protection market?

Stringent and evolving building codes and fire safety regulations globally are primary drivers for the PFP market. These mandates ensure that new constructions and many renovations incorporate essential fire-resistant measures, thereby stimulating continuous demand and innovation.

What is the future outlook for the Passive Fire Protection market?

The Passive Fire Protection market is expected to demonstrate robust growth, driven by increasing construction activities, stricter global regulations, and technological advancements such as smart PFP systems and sustainable materials. The continuous focus on building safety will ensure sustained demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted