Paper Pulp Market

Paper Pulp Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701352 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

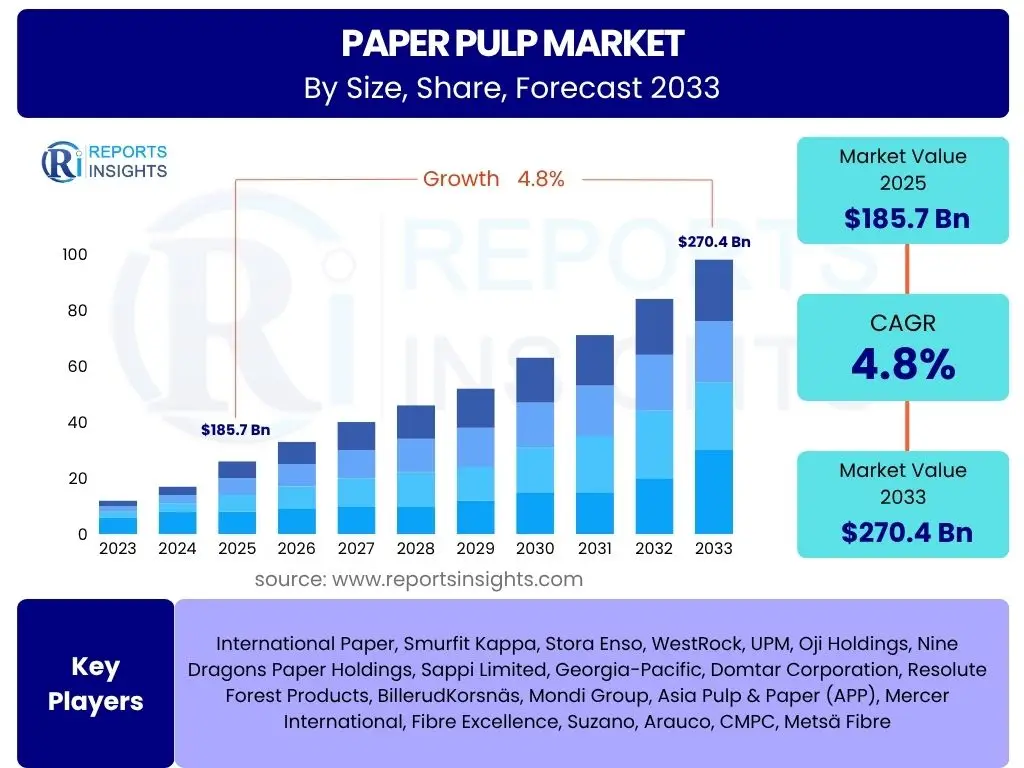

Paper Pulp Market Size

According to Reports Insights Consulting Pvt Ltd, The Paper Pulp Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 185.7 Billion in 2025 and is projected to reach USD 270.4 Billion by the end of the forecast period in 2033.

Key Paper Pulp Market Trends & Insights

The paper pulp market is undergoing significant transformations driven by evolving consumer preferences and regulatory pressures. A prominent trend is the escalating demand for sustainable and eco-friendly packaging solutions, fueled by a global shift away from single-use plastics. This has led to increased innovation in pulp-based packaging materials, including molded fiber products and lightweight paperboards, designed for improved recyclability and biodegradability. Furthermore, the digitalization of the pulp and paper industry is gaining momentum, with companies investing in advanced automation, AI, and IoT to optimize production processes, enhance energy efficiency, and improve supply chain transparency, thereby reducing operational costs and environmental footprints.

Another crucial insight is the growing emphasis on circular economy principles within the paper pulp sector. This involves increasing the utilization of recycled content, developing processes for chemical recycling of paper fibers, and exploring alternative non-wood fiber sources such as agricultural residues. The market is also witnessing a surge in demand for specialty pulps, including those used in textiles (dissolving pulp for rayon/lyocell), non-wovens, and advanced composite materials, indicating a diversification beyond traditional paper products. These trends collectively underscore the industry's commitment to sustainability, efficiency, and diversification in response to global environmental concerns and technological advancements.

The increasing awareness of deforestation and the need for responsible forestry management is also shaping procurement practices, with certifications like FSC (Forest Stewardship Council) becoming increasingly important. This influences supply chain decisions and consumer perception, promoting a more ethical and sustainable industry. The expansion of e-commerce, particularly post-pandemic, has also created an unprecedented demand for robust and sustainable packaging, pushing pulp producers to innovate and scale their production of suitable materials.

- Growing demand for sustainable and biodegradable packaging solutions.

- Increased adoption of automation, AI, and IoT in pulp production for efficiency.

- Strong focus on circular economy principles and higher recycled content utilization.

- Diversification into specialty pulps for textiles and advanced materials.

- Emphasis on responsible forestry and certified raw material sourcing.

AI Impact Analysis on Paper Pulp

The integration of Artificial Intelligence (AI) in the paper pulp industry is poised to revolutionize operational efficiency, resource management, and product quality. Users frequently inquire about how AI can optimize complex manufacturing processes, particularly in areas like pulp quality control, predictive maintenance of machinery, and energy consumption. AI-driven systems can analyze vast datasets from sensors across the production line, identifying anomalies and predicting equipment failures before they occur, thereby minimizing downtime and maintenance costs. Furthermore, AI algorithms can precisely monitor and adjust parameters during the pulping process, such as chemical dosages and temperature, to ensure consistent pulp quality while reducing chemical usage and waste generation.

Beyond process optimization, AI is also anticipated to significantly enhance supply chain management and sustainable forestry practices. Users are keen to understand AI's role in optimizing logistics for raw material procurement and finished product distribution, leading to reduced transportation costs and carbon emissions. In forestry, AI can be applied to satellite imagery and drone data for smarter forest management, including disease detection, growth monitoring, and optimized harvesting schedules, contributing to more sustainable resource utilization. While the initial investment in AI infrastructure can be substantial, the long-term benefits in terms of efficiency gains, cost reductions, and environmental compliance are driving its adoption across the pulp and paper sector.

The potential for AI to foster innovation in new product development, particularly for advanced biomaterials derived from pulp, is another area of interest. AI can accelerate research and development by simulating material properties and optimizing formulations, leading to the creation of novel pulp-based products with enhanced functionalities. This forward-looking application of AI is expected to open new revenue streams and applications for the industry. However, concerns regarding data privacy, cybersecurity, and the need for skilled labor to manage AI systems are also pertinent considerations for industry stakeholders, necessitating robust strategies for implementation and workforce development.

- Optimization of pulp production processes for enhanced quality and efficiency.

- Implementation of predictive maintenance for machinery, reducing downtime.

- Improved energy management and resource utilization through AI-driven insights.

- Advanced supply chain optimization from raw material sourcing to delivery.

- Enhanced sustainable forestry practices and land management.

- Acceleration of new product development for advanced biomaterials.

Key Takeaways Paper Pulp Market Size & Forecast

The Paper Pulp market is set for consistent expansion, primarily driven by the escalating global demand for sustainable packaging and hygiene products. A key takeaway is the robust growth trajectory, reflected in a projected CAGR of 4.8% through 2033, indicating a resilient market despite fluctuating raw material costs and environmental regulations. This growth is intrinsically linked to the increasing consumer preference for environmentally friendly alternatives to plastics, making pulp a critical component in the circular economy initiatives worldwide. The substantial market valuation of USD 185.7 Billion in 2025, forecasted to reach USD 270.4 Billion by 2033, underscores the industry's significant economic impact and future potential.

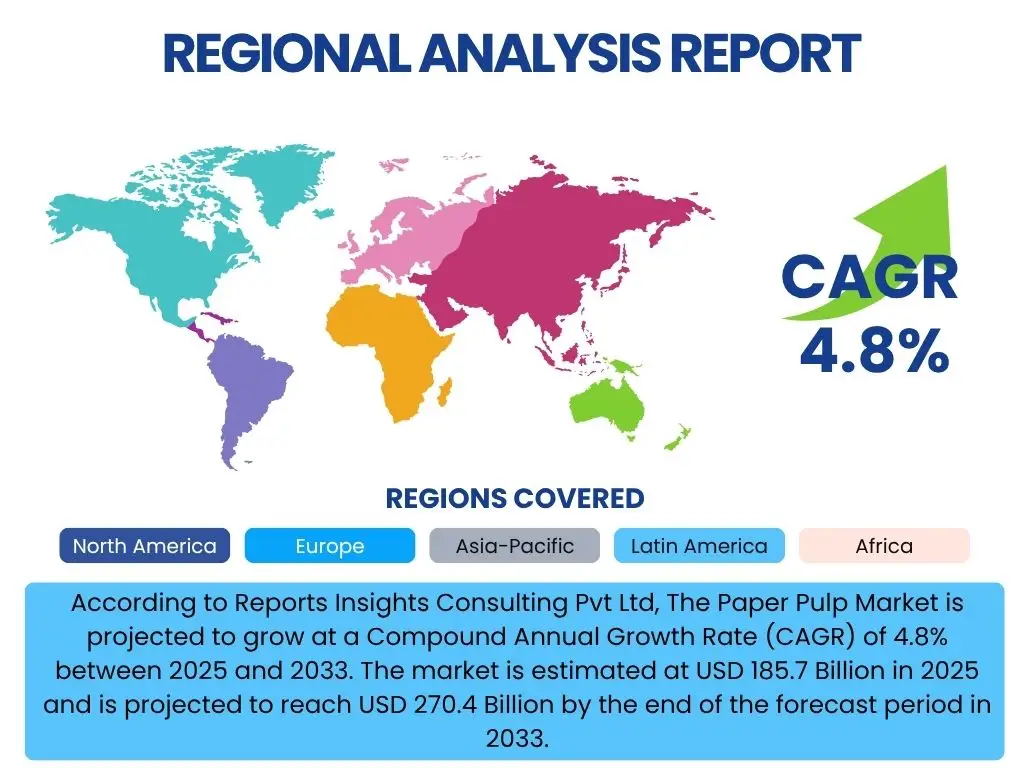

Furthermore, regional dynamics play a crucial role in shaping market growth, with Asia Pacific expected to remain a dominant force due to industrialization, urbanization, and rising disposable incomes fueling demand for paper-based products. Another significant insight is the diversification of pulp applications beyond traditional paper and board, with specialty pulps gaining traction in areas like textiles, non-wovens, and innovative biomaterials. This diversification provides new avenues for revenue generation and mitigates risks associated with reliance on conventional segments. The industry's proactive efforts in adopting advanced technologies, including AI and automation, for operational efficiency and sustainability are also critical drivers of its positive outlook.

The market’s future is heavily influenced by its commitment to sustainability, with companies investing in responsible forestry, reduced energy consumption, and closed-loop systems for water and chemical use. Regulatory frameworks worldwide are increasingly favoring pulp-based products over less sustainable alternatives, providing a tailwind for market expansion. The strategic focus on innovation, resource efficiency, and environmental stewardship will be paramount for stakeholders aiming to capitalize on the growing opportunities within this evolving market landscape. This holistic approach ensures long-term viability and competitiveness in a world increasingly focused on ecological impact.

- Significant market growth projected at a CAGR of 4.8% (2025-2033), reaching USD 270.4 Billion by 2033.

- Primary growth driver is the global shift towards sustainable and eco-friendly packaging.

- Asia Pacific is anticipated to maintain its market dominance due to robust demand and industrial growth.

- Diversification into high-value specialty pulps represents a key growth opportunity.

- Technological advancements, including AI and automation, are crucial for operational efficiency and sustainability.

- Increased emphasis on responsible sourcing and circular economy principles is shaping market strategies.

Paper Pulp Market Drivers Analysis

The paper pulp market is significantly propelled by several key drivers, with the escalating global demand for sustainable packaging solutions at the forefront. As consumers and regulations increasingly push for alternatives to single-use plastics, the versatility, recyclability, and biodegradability of paper pulp make it an ideal choice for packaging across various industries, including e-commerce, food and beverage, and consumer goods. This shift creates a continuous high demand for diverse types of pulp, from kraft for robust corrugated boxes to fine pulps for flexible packaging. Furthermore, the rapid expansion of the e-commerce sector globally directly translates into a higher need for protective and sustainable shipping materials, predominantly paper-based.

Another strong driver is the growing awareness and stringent regulations concerning environmental sustainability. Governments and international bodies are implementing policies that restrict plastic use and encourage the adoption of renewable and recyclable materials. This legislative support, coupled with corporate social responsibility initiatives, drives industries to opt for paper pulp-based products. The demand for hygiene products, such as tissue paper, sanitary napkins, and diapers, also continues to grow steadily, especially in emerging economies, providing a stable and expanding market for bleached chemical pulps. Innovation in specialty pulps, including those for textiles like lyocell and non-wovens, further broadens the application scope and demand for specific pulp types.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable Packaging | +1.5% | Global, particularly Europe & North America | Short to Long Term (2025-2033) |

| Expansion of E-commerce Sector | +1.2% | Asia Pacific, North America, Europe | Short to Medium Term (2025-2029) |

| Increasing Demand for Tissue & Hygiene Products | +0.8% | Asia Pacific, Latin America, Africa | Medium to Long Term (2026-2033) |

| Stringent Environmental Regulations Against Plastics | +0.7% | Europe, North America, parts of Asia | Short to Medium Term (2025-2030) |

| Technological Advancements in Pulp Production | +0.6% | Global, key producing regions | Medium to Long Term (2027-2033) |

Paper Pulp Market Restraints Analysis

Despite robust growth drivers, the paper pulp market faces several significant restraints that could impede its expansion. One primary concern is the volatility of raw material prices, particularly wood fiber. Fluctuations in timber supply due to weather conditions, disease outbreaks, or geopolitical factors directly impact production costs, making it challenging for manufacturers to maintain stable profit margins. This unpredictability in input costs often leads to price instability in the end products, affecting market competitiveness and planning for pulp producers. Additionally, the increasing cost of energy required for the highly energy-intensive pulping processes, especially in regions with fluctuating energy markets, adds further pressure on operational expenses.

Another major restraint is the escalating stringency of environmental regulations. While supporting sustainable practices, these regulations often necessitate significant capital investments in pollution control technologies, water treatment, and air emission reduction systems. Compliance with these evolving standards can increase production costs and complexity, particularly for older mills requiring extensive upgrades. Furthermore, public perception and advocacy against deforestation and unsustainable logging practices can lead to supply chain scrutiny and consumer backlash, impacting market access and brand reputation. The availability of suitable forest land and the social license to operate in certain regions are becoming increasingly restrictive, posing a challenge to capacity expansion.

Competition from alternative materials, particularly advanced plastics, bioplastics, and digital media, also acts as a restraint. While paper pulp is gaining traction due to its sustainability, innovations in synthetic materials that offer superior barrier properties, durability, or cost-effectiveness in specific applications can limit pulp's market penetration. The ongoing digitalization trend reduces the demand for traditional printing and writing paper, forcing a structural shift in the industry and a need for diversification, which comes with its own set of challenges and investments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Wood Fiber) | -0.9% | Global | Short to Medium Term (2025-2030) |

| Stringent Environmental Regulations & Compliance Costs | -0.7% | Europe, North America, specific Asian countries | Medium to Long Term (2026-2033) |

| High Energy Consumption & Costs | -0.6% | Global, especially energy-dependent regions | Short to Medium Term (2025-2029) |

| Competition from Alternative Materials & Digital Media | -0.5% | Global | Medium to Long Term (2027-2033) |

| Forestry Management & Land Availability Issues | -0.4% | Specific logging regions (e.g., Southeast Asia, Latin America) | Long Term (2028-2033) |

Paper Pulp Market Opportunities Analysis

The paper pulp market is ripe with opportunities driven by innovation, sustainability trends, and expanding applications. One significant area of growth lies in the development of advanced biomaterials and biochemicals derived from pulp. Research into cellulose nanofibers (CNF) and cellulose nanocrystals (CNC) is unlocking new applications in composites, filters, electronics, and medical devices, providing high-value revenue streams beyond traditional paper products. This diversification allows pulp producers to tap into emerging industries that seek sustainable, bio-based alternatives to synthetic materials. Investment in biorefineries integrated with pulp mills can further extract valuable co-products from biomass, enhancing profitability and resource efficiency.

Another compelling opportunity emerges from the increasing global push for circular economy models, leading to a greater demand for recycled fiber and the development of advanced recycling technologies. Innovations in de-inking and fiber recovery processes can expand the types of paper waste that can be recycled, reducing reliance on virgin pulp and aligning with sustainability goals. Emerging markets in Asia Pacific, Latin America, and Africa present substantial growth avenues due to rapid urbanization, industrialization, and rising middle-class populations. These regions are experiencing increased demand for packaging, hygiene products, and construction materials, where pulp-based solutions are gaining traction. Localized production and supply chain optimization can cater to these burgeoning markets effectively.

The digitalization of the pulp and paper industry, particularly through the adoption of Industry 4.0 technologies like IoT, AI, and big data analytics, offers immense opportunities for operational optimization. These technologies can improve energy efficiency, predictive maintenance, quality control, and supply chain transparency, leading to significant cost savings and enhanced productivity. Developing pulp grades optimized for these digitalized processes can further solidify market positions. Furthermore, the niche market for specialty pulps, used in applications such as filtration, battery separators, and specialty textiles, continues to expand, offering higher profit margins and less susceptibility to general market fluctuations. Investing in research and development for these high-performance pulps can unlock significant competitive advantages.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Biomaterials & Biorefineries | +1.0% | Global, particularly developed economies | Medium to Long Term (2027-2033) |

| Expansion in Emerging Economies (Packaging, Hygiene) | +0.9% | Asia Pacific, Latin America, Africa | Short to Long Term (2025-2033) |

| Increased Adoption of Recycled Pulp & Advanced Recycling | +0.8% | Global, particularly Europe & North America | Short to Medium Term (2025-2030) |

| Digitalization & Industry 4.0 Integration | +0.7% | Global, particularly leading manufacturers | Medium to Long Term (2026-2033) |

| Growth in Specialty Pulp Applications (Textiles, Filtration) | +0.6% | Global, specific high-tech clusters | Medium to Long Term (2027-2033) |

Paper Pulp Market Challenges Impact Analysis

The paper pulp market faces a unique set of challenges that demand strategic responses from industry players. One significant challenge is the increasing scrutiny over environmental impact and resource management. While the industry is moving towards sustainability, concerns regarding water consumption, effluent discharge, air emissions, and deforestation persist. Meeting increasingly stringent environmental regulations while maintaining cost-effectiveness is a continuous balancing act. Moreover, the need for significant capital investment in modernizing aging mills to integrate eco-friendly technologies and comply with new standards can be a formidable barrier, especially for smaller players. This financial burden can slow down innovation and adoption of best practices.

Another critical challenge involves raw material supply chain complexities and sustainability concerns. Relying heavily on forest resources, the industry must navigate issues such as illegal logging, climate change impacts on forest health, and land-use conflicts. Ensuring a consistent, sustainable, and ethically sourced supply of wood fiber requires robust certification systems and long-term forest management plans, which can be challenging to implement globally. Furthermore, the skilled labor shortage within the pulp and paper industry poses a significant operational challenge. The highly specialized nature of the machinery and processes requires a skilled workforce, but an aging demographic and a lack of new talent entering the sector can lead to operational inefficiencies and difficulties in adopting new technologies.

The fluctuating global economic conditions, including trade disputes, currency volatility, and inflationary pressures, also present ongoing challenges. These factors can disrupt international trade flows of pulp, impact demand from end-use industries, and increase operational costs, thereby affecting profitability. Additionally, managing and processing the vast amounts of waste generated by pulp mills, including sludge and by-products, while simultaneously extracting value from them, remains a significant challenge that requires continuous innovation in waste-to-energy solutions and circular economy approaches. Adapting to the fast pace of technological change and consumer preferences, especially the shift away from traditional printing papers, also requires continuous R&D and market diversification efforts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Compliance & Capital Costs | -0.8% | Global, particularly Europe & North America | Short to Long Term (2025-2033) |

| Raw Material Supply Chain Volatility & Sustainability | -0.7% | Global, specific sourcing regions | Short to Medium Term (2025-2030) |

| Skilled Labor Shortage & Workforce Training Needs | -0.6% | Developed economies, specific manufacturing hubs | Medium to Long Term (2026-2033) |

| Global Economic Volatility & Trade Barriers | -0.5% | Global | Short to Medium Term (2025-2029) |

| Waste Management & By-product Utilization | -0.4% | Global | Medium to Long Term (2027-2033) |

Paper Pulp Market - Updated Report Scope

This comprehensive report on the Paper Pulp Market provides an in-depth analysis of market dynamics, growth drivers, restraints, opportunities, and challenges. It offers a detailed forecast of market size and growth rates from 2025 to 2033, examining key trends shaping the industry and the impact of technological advancements, including AI. The report segments the market by pulp type, end-use application, and source, providing granular insights into each category. It also includes an extensive regional analysis, covering major geographies and their respective market contributions, alongside a competitive landscape assessment featuring profiles of leading market participants and their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185.7 Billion |

| Market Forecast in 2033 | USD 270.4 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | International Paper, Smurfit Kappa, Stora Enso, WestRock, UPM, Oji Holdings, Nine Dragons Paper Holdings, Sappi Limited, Georgia-Pacific, Domtar Corporation, Resolute Forest Products, BillerudKorsnäs, Mondi Group, Asia Pulp & Paper (APP), Mercer International, Fibre Excellence, Suzano, Arauco, CMPC, Metsä Fibre |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The paper pulp market is comprehensively segmented to provide granular insights into its diverse components and applications. These segmentations allow for a detailed analysis of market dynamics within each category, identifying growth pockets and shifting industry preferences. Understanding these segments is crucial for stakeholders to develop targeted strategies, optimize product portfolios, and adapt to evolving market demands. The primary segmentations include categories based on the type of pulp produced, the various end-use applications it serves, and the source of the raw material.

Each segment holds unique characteristics and market drivers. For instance, the demand for chemical pulp is largely driven by packaging and tissue industries due to its strength and brightness, while mechanical pulp finds its niche in newsprint and lower-grade printing papers. Specialty pulps, on the other hand, cater to high-value applications, including textiles and advanced materials, reflecting the industry's diversification efforts. Analyzing these segments provides a holistic view of the market's structure and potential for innovation.

- By Type:

- Chemical Pulp

- Kraft Pulp

- Sulphite Pulp

- Mechanical Pulp

- Groundwood Pulp

- Refiner Mechanical Pulp (RMP)

- Thermomechanical Pulp (TMP)

- Chemi-Thermomechanical Pulp (CTMP)

- Recycled Pulp

- Specialty Pulp

- Dissolving Pulp

- Others (e.g., high-purity pulp)

- Chemical Pulp

- By End-Use:

- Packaging

- Corrugated Boards

- Folding Cartons

- Flexible Packaging

- Printing & Writing Paper

- Tissue Paper

- Specialty Paper

- Textile Industry

- Others (e.g., Building Materials, Non-Wovens, Filters)

- Packaging

- By Source:

- Wood Pulp

- Softwood

- Hardwood

- Non-Wood Pulp

- Agricultural Residues

- Bagasse

- Bamboo

- Others (e.g., Hemp, Cotton Linters)

- Wood Pulp

Regional Highlights

- Asia Pacific (APAC): This region is expected to maintain its dominance in the paper pulp market, driven by rapid industrialization, urbanization, and a burgeoning middle-class population. Countries like China, India, and Indonesia are witnessing significant growth in packaging, tissue, and personal care sectors, fueling high demand for pulp. The region is also a major production hub, leveraging abundant forest resources and expanding recycling infrastructure. Government initiatives promoting sustainable practices and domestic manufacturing further bolster market expansion.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on sustainability, Europe is a leader in adopting recycled pulp and innovative bio-based solutions. The region's mature paper and packaging industries, coupled with a high consumer awareness of eco-friendly products, drive demand for high-quality, sustainably sourced pulp. Nordic countries, in particular, are major pulp producers with advanced forest management practices and integrated biorefineries.

- North America: A significant producer and consumer of paper pulp, North America benefits from vast forest resources and a well-established pulp and paper industry. The increasing demand for e-commerce packaging and tissue products is a key driver. Innovation in specialty pulps and sustainable forestry practices, along with investments in modernizing production facilities, are crucial for market growth in this region.

- Latin America: This region presents considerable growth potential due to its rich forest resources and expanding economies. Countries like Brazil and Chile are major pulp exporters, leveraging efficient plantation forestry. Rising disposable incomes and increasing demand for consumer goods, particularly in packaging and hygiene sectors, contribute to regional market growth. Investments in new pulp mills and sustainable sourcing are key trends.

- Middle East and Africa (MEA): While currently a smaller market, MEA is anticipated to witness steady growth, driven by increasing construction activities, urbanization, and improving living standards. Demand for packaging, tissue, and printing paper is on the rise. Investment in local production capabilities and improved recycling infrastructure will be vital for the region's market development, often relying on imported pulp.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Paper Pulp Market.- International Paper

- Smurfit Kappa

- Stora Enso

- WestRock

- UPM

- Oji Holdings

- Nine Dragons Paper Holdings

- Sappi Limited

- Georgia-Pacific

- Domtar Corporation

- Resolute Forest Products

- BillerudKorsnäs

- Mondi Group

- Asia Pulp & Paper (APP)

- Mercer International

- Fibre Excellence

- Suzano

- Arauco

- CMPC

- Metsä Fibre

Frequently Asked Questions

Analyze common user questions about the Paper Pulp market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current size and growth forecast for the Paper Pulp Market?

The Paper Pulp Market is estimated at USD 185.7 Billion in 2025 and is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% to reach USD 270.4 Billion by 2033. This growth is driven by increasing demand for sustainable packaging and hygiene products.

What are the primary drivers propelling the Paper Pulp Market growth?

Key drivers include the global shift towards sustainable and eco-friendly packaging solutions, the rapid expansion of the e-commerce sector, increasing demand for tissue and hygiene products, and stringent environmental regulations promoting alternatives to plastics.

How is Artificial Intelligence impacting the Paper Pulp industry?

AI is transforming the industry by optimizing production processes, enabling predictive maintenance, enhancing supply chain efficiency, and improving sustainable forestry practices. It helps ensure consistent pulp quality, reduces downtime, and lowers operational costs.

What are the major challenges facing the Paper Pulp Market?

Significant challenges include volatile raw material prices, stringent environmental compliance costs, high energy consumption, a shortage of skilled labor, and global economic volatility. Managing waste and by-products also remains a continuous challenge.

Which regions are key contributors to the Paper Pulp Market?

Asia Pacific is the dominant region due to rapid industrialization and urbanization. Europe and North America are also significant contributors, driven by mature markets, sustainability initiatives, and demand for e-commerce packaging. Latin America offers growth potential with abundant resources.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted