Palladium Catalyst Market

Palladium Catalyst Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701618 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

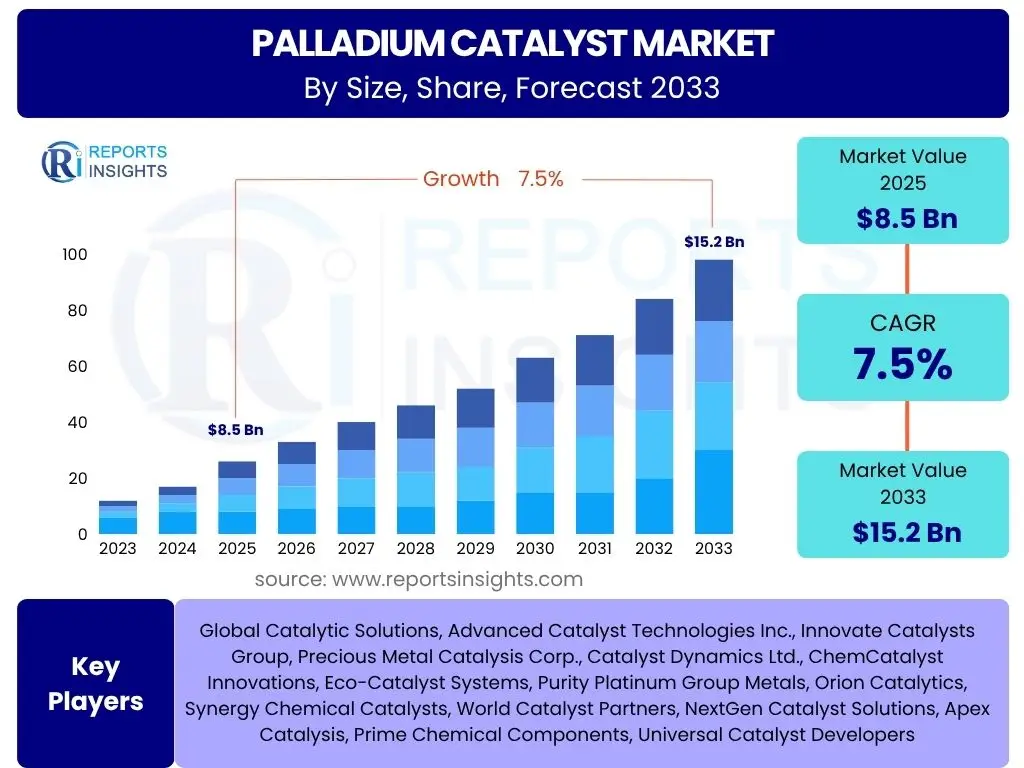

Palladium Catalyst Market Size

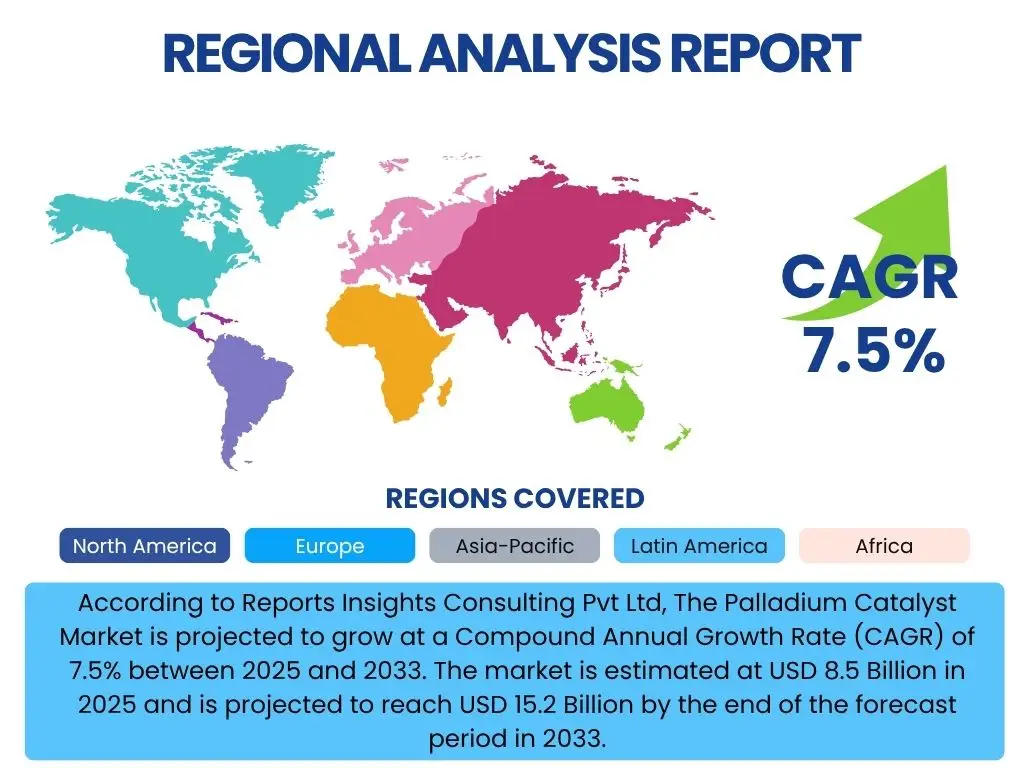

According to Reports Insights Consulting Pvt Ltd, The Palladium Catalyst Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 15.2 Billion by the end of the forecast period in 2033.

Key Palladium Catalyst Market Trends & Insights

Common user inquiries regarding the Palladium Catalyst market frequently center on the driving forces behind its expansion, the emergence of novel applications, and the influence of global regulatory frameworks. Users are keen to understand how stricter environmental regulations are reshaping demand, particularly in the automotive and industrial sectors, and what technological advancements are enabling more efficient and sustainable catalytic processes. There is also significant interest in the volatility of palladium prices and the strategic responses by market participants to ensure supply stability and cost-effectiveness. The increasing focus on green chemistry and sustainable manufacturing processes further highlights a growing trend towards catalysts that offer both performance and environmental benefits.

Furthermore, the market is experiencing a notable trend towards the development of advanced catalyst formulations that offer enhanced activity, selectivity, and stability, often requiring lower palladium loadings. This innovation is driven by the need to reduce reliance on expensive raw materials and improve process economics. The expansion of niche applications, such as in the production of hydrogen fuel cells and specialized pharmaceutical intermediates, is also gaining traction, signaling diversification beyond traditional automotive and petrochemical sectors. Supply chain resilience and circular economy principles, including catalyst recycling and recovery, are becoming critical considerations for stakeholders navigating a dynamic global market.

- Stricter global emission standards driving demand in automotive catalytic converters.

- Increasing adoption in fine chemical and pharmaceutical synthesis due to high selectivity.

- Growing focus on sustainable and green chemistry processes utilizing palladium catalysts.

- Technological advancements in catalyst design leading to improved efficiency and reduced palladium loading.

- Expansion of applications in hydrogen production and fuel cell technologies.

- Volatility in palladium prices influencing research into alternative and more efficient catalyst formulations.

- Emergence of robust catalyst recycling and recovery programs.

AI Impact Analysis on Palladium Catalyst

User questions concerning the impact of Artificial Intelligence (AI) on the Palladium Catalyst market primarily revolve around its potential to accelerate catalyst discovery, optimize manufacturing processes, and predict performance under various operating conditions. Stakeholders are keen to understand if AI can significantly reduce the time and cost associated with research and development, particularly in identifying novel catalyst materials or improving existing formulations. There is also an expectation that AI-driven predictive models could enhance operational efficiency in industrial applications by optimizing reaction parameters and minimizing waste, leading to substantial economic and environmental benefits.

Furthermore, discussions often touch upon the use of machine learning algorithms for high-throughput screening of potential catalyst candidates, virtual prototyping, and real-time process monitoring. The integration of AI tools is anticipated to provide deeper insights into reaction mechanisms and catalyst degradation pathways, enabling more resilient and durable catalyst designs. While there is excitement about the transformative potential, common concerns include the need for extensive datasets, the computational resources required for complex simulations, and the expertise needed to effectively implement and interpret AI solutions within the highly specialized field of catalysis. The balance between leveraging AI for innovation and addressing practical implementation challenges remains a key area of interest.

- Accelerated discovery of new palladium catalyst compositions and formulations through AI-driven material informatics.

- Optimization of catalyst synthesis parameters and manufacturing processes using machine learning algorithms.

- Predictive modeling of catalyst performance, durability, and selectivity under varying reaction conditions.

- Enhanced understanding of reaction mechanisms and active sites via AI-powered computational chemistry.

- Development of digital twins for real-time monitoring and control of catalytic reactors.

- Reduced research and development timelines and costs in catalyst innovation.

- Potential for automated catalyst testing and characterization.

Key Takeaways Palladium Catalyst Market Size & Forecast

Key takeaways from the Palladium Catalyst market size and forecast frequently address the overarching growth trajectory, the dominant application areas, and the strategic importance of this market within the broader chemical and automotive industries. Users are most interested in understanding the primary drivers of the projected growth, such as tightening environmental regulations and the expansion of the chemical and pharmaceutical sectors. The forecast indicates a steady expansion, primarily fueled by sustained demand from catalytic converters in vehicles and significant uptake in various industrial processes, notably hydrogenation and cross-coupling reactions.

Furthermore, a critical insight is the increasing emphasis on innovation to develop more efficient and cost-effective palladium catalyst solutions, partly as a response to price volatility of the raw material. The market’s resilience is also underscored by its diversification into emerging applications like fuel cells and sustainable chemistry. Geographic shifts are anticipated, with significant growth projected in emerging economies due to industrialization and stricter local environmental policies. The ability of manufacturers to navigate supply chain challenges and leverage technological advancements will be crucial for capturing market share and sustaining growth throughout the forecast period.

- Robust market growth driven by escalating environmental regulations and industrial expansion.

- Automotive and chemical processing sectors remain primary demand generators.

- Significant opportunities in pharmaceutical synthesis, green hydrogen production, and fuel cell technologies.

- Innovation in catalyst efficiency and reduction of palladium loading are strategic imperatives.

- Asia Pacific is poised for substantial market expansion due to rapid industrialization.

- Volatility in palladium prices necessitates strategic raw material sourcing and R&D for alternatives.

- The market is undergoing a transformation towards sustainable and resource-efficient catalytic solutions.

Palladium Catalyst Market Drivers Analysis

The Palladium Catalyst market is primarily driven by a confluence of factors including stringent environmental regulations, robust growth in the chemical and pharmaceutical sectors, and the increasing demand for cleaner energy solutions. Global efforts to curb atmospheric pollution have mandated the widespread use of catalytic converters in vehicles, a sector where palladium catalysts are indispensable. Additionally, their unparalleled efficacy in various organic synthesis reactions, critical to the production of fine chemicals and active pharmaceutical ingredients, ensures sustained demand from these industries. The push towards sustainable industrial practices and the burgeoning hydrogen economy further bolster the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Stringency of Emission Regulations (Automotive) | +2.1% | North America, Europe, Asia Pacific (China, India) | Short to Medium Term (2025-2029) |

| Growing Demand from Chemical & Petrochemical Industries (Hydrogenation, Carbonylation) | +1.8% | Asia Pacific, North America, Europe | Medium to Long Term (2027-2033) |

| Expansion of Pharmaceutical Sector (API & Intermediate Synthesis) | +1.5% | North America, Europe, Asia Pacific (India, China) | Medium to Long Term (2026-2033) |

| Technological Advancements in Fuel Cells & Hydrogen Economy | +1.0% | Europe, North America, Japan, South Korea | Long Term (2030-2033) |

Palladium Catalyst Market Restraints Analysis

Despite the strong demand, the Palladium Catalyst market faces significant restraints, primarily stemming from the inherent volatility and high cost of palladium metal. As a precious metal, palladium prices are subject to geopolitical factors, supply chain disruptions, and speculative trading, making it challenging for manufacturers to maintain stable production costs. Furthermore, the limited global supply of palladium and the environmental impact associated with its mining pose long-term sustainability concerns. The emergence of alternative catalyst materials, albeit less efficient for certain applications, also presents a competitive threat, pushing industries to explore less expensive options.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High and Volatile Price of Palladium Metal | -1.5% | Global | Short to Medium Term (2025-2029) |

| Development of Alternative Non-Palladium Catalysts | -0.8% | Global (with focus on R&D hubs in North America, Europe) | Medium to Long Term (2028-2033) |

| Supply Chain Risks and Geopolitical Instability Affecting Palladium Mining | -0.5% | Russia, South Africa, North America, Europe (importing regions) | Short Term (2025-2027) |

Palladium Catalyst Market Opportunities Analysis

Significant opportunities in the Palladium Catalyst market are emerging from the global shift towards sustainable chemistry and the increasing investment in green technologies. The growing demand for catalysts in the production of biofuels, renewable chemicals, and in advanced wastewater treatment processes offers new avenues for market expansion. Furthermore, the development of more efficient and recyclable palladium catalyst systems, aligning with circular economy principles, presents a substantial opportunity for innovation and market differentiation. The burgeoning hydrogen economy, particularly in the context of fuel cells for transportation and stationary power, also opens up a high-growth segment for palladium-based solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Investment in Green Hydrogen Production and Fuel Cells | +1.2% | Europe, North America, East Asia (Japan, South Korea) | Medium to Long Term (2028-2033) |

| Increasing Focus on Sustainable Chemistry and Bio-Based Chemicals | +0.9% | Europe, North America, Asia Pacific | Medium Term (2026-2030) |

| Advancements in Catalyst Recycling and Recovery Technologies | +0.7% | Global (driven by economic and environmental incentives) | Short to Medium Term (2025-2029) |

| Emerging Applications in Environmental Remediation (e.g., Water Treatment) | +0.6% | Asia Pacific, North America, Europe | Long Term (2030-2033) |

Palladium Catalyst Market Challenges Impact Analysis

The Palladium Catalyst market faces several critical challenges that could impede its growth trajectory. The most prominent challenge is the inherent price volatility of palladium, which makes long-term planning and cost management difficult for manufacturers and end-users alike. Additionally, the environmental and ethical concerns associated with the mining of precious metals, including palladium, are prompting increased scrutiny and driving demand for more sustainable sourcing or alternative materials. Intense competition from other precious group metal catalysts and the ongoing research into non-PGM (Platinum Group Metal) catalysts also pose a significant challenge to market dominance. Ensuring consistent quality and performance across diverse applications, while managing intellectual property in a highly specialized field, adds further complexity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Palladium Raw Material Prices | -0.9% | Global | Short to Medium Term (2025-2029) |

| Environmental and Ethical Concerns Regarding Palladium Mining | -0.6% | Global (consumer and regulatory pressure) | Medium Term (2027-2031) |

| Competition from Other PGM and Non-PGM Catalysts | -0.4% | Global (especially in automotive and bulk chemicals) | Medium to Long Term (2028-2033) |

Palladium Catalyst Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Palladium Catalyst market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It examines historical data from 2019 to 2023, establishes 2024 as the base year, and presents forecasts up to 2033, enabling stakeholders to understand future market dynamics and make informed strategic decisions. The report also includes a thorough competitive landscape analysis, profiling leading companies and highlighting their strategic initiatives, product portfolios, and market presence. The scope encompasses detailed segmentation by type, application, and end-use industry, alongside regional breakdowns to provide a holistic view of the market's structure and potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 15.2 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Catalytic Solutions, Advanced Catalyst Technologies Inc., Innovate Catalysts Group, Precious Metal Catalysis Corp., Catalyst Dynamics Ltd., ChemCatalyst Innovations, Eco-Catalyst Systems, Purity Platinum Group Metals, Orion Catalytics, Synergy Chemical Catalysts, World Catalyst Partners, NextGen Catalyst Solutions, Apex Catalysis, Prime Chemical Components, Universal Catalyst Developers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Palladium Catalyst market is meticulously segmented to provide a granular understanding of its diverse applications and market dynamics. This segmentation facilitates a deeper analysis of specific industry demands, technological preferences, and regional consumption patterns, allowing stakeholders to identify niche opportunities and tailor their strategies. The market is primarily categorized by catalyst type, application, and end-use industry, reflecting the varied requirements across the value chain. Understanding these segments is crucial for accurate market sizing, forecasting, and strategic planning.

- By Type: This segment differentiates palladium catalysts based on their structural composition and how palladium is supported. Supported catalysts, where palladium is dispersed on a high-surface-area material like alumina or carbon, dominate due to their efficiency and stability in various industrial processes. Unsupported catalysts, such as palladium black or sponge, are used in specialized applications where high purity and surface area are critical.

- By Application: This is a critical segment illustrating the primary uses of palladium catalysts. Automotive catalytic converters represent the largest application, driven by global emission regulations. Chemical processing, encompassing a wide array of reactions like hydrogenation and cross-coupling, is another major consumer due to palladium's unparalleled catalytic activity. The pharmaceutical industry heavily relies on palladium for the synthesis of complex active pharmaceutical ingredients (APIs) and intermediates. Emerging applications in fuel cells and environmental remediation further diversify the market.

- By End-Use Industry: This segment categorizes the market by the industries that utilize palladium catalysts. The Automotive industry remains the largest end-user, followed closely by the Chemical & Petrochemical sector. The Pharmaceutical industry shows consistent demand for high-value applications. The Oil & Gas and Energy sectors are growing areas, particularly with the push for cleaner fuels and alternative energy sources.

Regional Highlights

- North America: This region holds a significant share in the Palladium Catalyst market, driven by stringent environmental regulations, a mature automotive industry, and robust research and development activities in chemical and pharmaceutical sectors. The presence of key market players and a focus on advanced catalyst technologies contribute to its sustained growth. The region is also witnessing increased adoption in emerging applications like fuel cells.

- Europe: Europe is a prominent market for palladium catalysts, characterized by strict emission standards, a strong chemical manufacturing base, and substantial investments in green technologies and sustainable chemistry. Countries like Germany, the UK, and France are leading in pharmaceutical research and advanced materials development, ensuring steady demand. The region's commitment to the hydrogen economy is also a key growth driver.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the Palladium Catalyst market. This growth is primarily attributed to rapid industrialization, burgeoning automotive production, and expanding chemical and pharmaceutical industries in countries like China, India, and Japan. Increasing environmental concerns and the adoption of stricter emission norms in developing economies are fueling demand for catalytic converters and industrial catalysts. Government initiatives promoting cleaner manufacturing processes further bolster market expansion.

- Latin America: This region is experiencing moderate growth, driven by increasing automotive sales and the expansion of its chemical and petrochemical sectors, particularly in Brazil and Mexico. While environmental regulations are becoming more stringent, the market's development is often influenced by economic stability and investment in industrial infrastructure.

- Middle East and Africa (MEA): The MEA market for palladium catalysts is nascent but growing, primarily influenced by investments in petrochemical refining and the automotive sector in countries like Saudi Arabia, UAE, and South Africa. Growing environmental awareness and the implementation of cleaner fuel standards are expected to drive future demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Palladium Catalyst Market.- Global Catalytic Solutions

- Advanced Catalyst Technologies Inc.

- Innovate Catalysts Group

- Precious Metal Catalysis Corp.

- Catalyst Dynamics Ltd.

- ChemCatalyst Innovations

- Eco-Catalyst Systems

- Purity Platinum Group Metals

- Orion Catalytics

- Synergy Chemical Catalysts

- World Catalyst Partners

- NextGen Catalyst Solutions

- Apex Catalysis

- Prime Chemical Components

- Universal Catalyst Developers

Frequently Asked Questions

Analyze common user questions about the Palladium Catalyst market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary applications of palladium catalysts?

Palladium catalysts are predominantly used in automotive catalytic converters for emission control, and extensively in chemical processes such as hydrogenation, carbonylation, and cross-coupling reactions (e.g., Heck, Suzuki) in the pharmaceutical and fine chemical industries. They are also integral to petroleum refining, fuel cells, and environmental remediation.

What factors influence the price of palladium catalysts?

The price of palladium catalysts is primarily influenced by the global market price of palladium metal, which is subject to supply-demand dynamics, geopolitical events affecting mining regions (e.g., Russia, South Africa), and speculative trading. Manufacturing costs, catalyst efficiency, and purity also play a role.

How do environmental regulations impact the palladium catalyst market?

Stricter global environmental regulations, particularly emission standards for vehicles and industrial processes, significantly drive the demand for palladium catalysts. These regulations necessitate the use of efficient catalytic converters and cleaner chemical processes, directly bolstering market growth.

What are the key emerging trends in palladium catalyst technology?

Emerging trends include the development of highly efficient catalysts requiring lower palladium loading, increased focus on sustainable and green chemistry applications, advancements in catalyst recycling and recovery technologies, and growing integration into hydrogen fuel cell and renewable chemical production processes.

Which regions are leading the growth in the palladium catalyst market?

The Asia Pacific region, particularly China and India, is expected to exhibit the highest growth due to rapid industrialization, increasing automotive production, and evolving environmental regulations. North America and Europe also maintain significant market shares due to established industries and strong R&D.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted