Industrial Catalyst Market

Industrial Catalyst Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702974 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

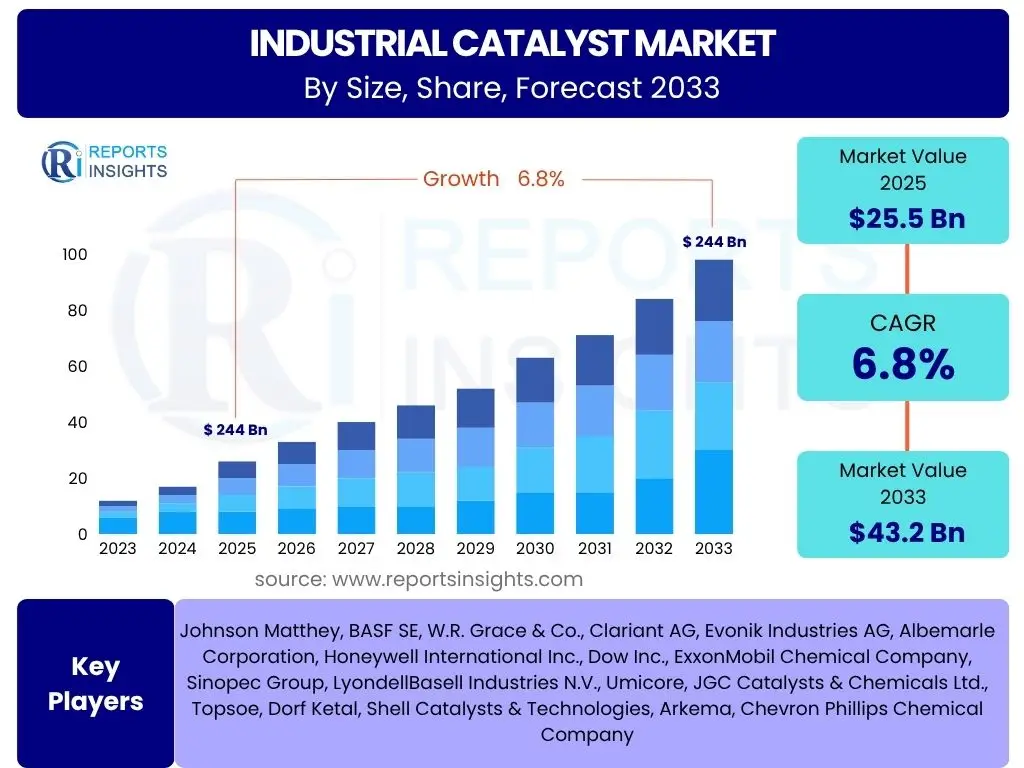

Industrial Catalyst Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Catalyst Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This robust growth trajectory is underpinned by increasing demand from diverse industrial sectors and continuous advancements in catalyst technology. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 43.2 Billion by the end of the forecast period in 2033, driven by a confluence of factors including industrial expansion, environmental regulations, and the pursuit of enhanced operational efficiencies.

The consistent expansion of the chemical and petrochemical industries, particularly in emerging economies, serves as a fundamental driver for the industrial catalyst market. Catalysts are indispensable for optimizing reaction rates, improving selectivity, and reducing energy consumption across a myriad of chemical processes, from polymer production to the synthesis of specialty chemicals. Furthermore, the global shift towards sustainable manufacturing practices and stricter environmental standards is accelerating the adoption of advanced catalysts designed to minimize waste and emissions, thereby contributing significantly to market valuation.

Key Industrial Catalyst Market Trends & Insights

Analysis of common user inquiries regarding trends and insights in the Industrial Catalyst market reveals a strong focus on sustainability, efficiency, and technological integration. Users frequently seek information on how environmental regulations are shaping catalyst development, the role of digitalization and AI in catalyst optimization, and the emergence of novel catalyst materials. There is also significant interest in understanding the impact of resource scarcity and circular economy principles on catalyst innovation and application. The market is increasingly characterized by a push towards green chemistry, smart manufacturing, and customized catalyst solutions tailored to specific industrial needs.

- Emphasis on green and sustainable catalysts: Development of environmentally friendly catalysts that reduce waste, energy consumption, and reliance on hazardous materials.

- Digitalization and AI integration: Leveraging artificial intelligence, machine learning, and advanced analytics for catalyst discovery, design, optimization, and process control.

- Growing demand for specialty catalysts: Increasing adoption of customized and high-performance catalysts for niche applications and complex chemical reactions.

- Circular economy principles: Focus on catalyst regeneration, recycling, and extending catalyst lifespan to minimize resource consumption and waste generation.

- Bio-based catalyst development: Research and commercialization of biocatalysts derived from biological sources for milder reaction conditions and reduced environmental footprint.

- Advanced material innovation: Exploration of novel materials such as nanomaterials, MOFs (Metal-Organic Frameworks), and single-atom catalysts for enhanced activity and selectivity.

AI Impact Analysis on Industrial Catalyst

Common user questions related to the impact of AI on the Industrial Catalyst sector frequently revolve around its potential to accelerate research and development, optimize industrial processes, and enhance the performance and lifespan of catalysts. Users are keenly interested in how AI can reduce the time and cost associated with discovering new catalyst formulations, predict catalyst behavior under varying conditions, and improve operational efficiency in chemical plants. Concerns often include the initial investment required for AI infrastructure, data privacy, and the need for specialized skillsets to implement and manage AI-driven systems within traditional industrial settings. However, the overarching expectation is that AI will be a transformative force, enabling unprecedented levels of innovation and efficiency.

Artificial intelligence is profoundly impacting the industrial catalyst landscape by revolutionizing how catalysts are designed, manufactured, and utilized. AI algorithms can rapidly analyze vast datasets of chemical properties, reaction mechanisms, and experimental results, significantly accelerating the discovery of novel catalyst materials with desired characteristics. This capability reduces the reliance on traditional trial-and-error methods, leading to faster innovation cycles and more efficient catalyst development pipelines. Furthermore, machine learning models can predict the performance and stability of catalysts under various operating conditions, enabling optimized process parameters and extending catalyst lifecycles.

- Accelerated Catalyst Discovery: AI algorithms predict novel catalyst compositions and structures, significantly reducing R&D time.

- Process Optimization: Machine learning models optimize reaction conditions for maximum catalyst efficiency and product yield.

- Predictive Maintenance: AI monitors catalyst performance in real-time, predicting degradation and enabling proactive replacement or regeneration.

- Quality Control: Computer vision and AI enhance quality inspection of catalyst materials during manufacturing.

- Supply Chain Efficiency: AI optimizes logistics and inventory management for catalyst raw materials and finished products.

- Enhanced Safety: AI models can identify potential hazards in catalytic processes, improving operational safety.

Key Takeaways Industrial Catalyst Market Size & Forecast

Analysis of common user questions concerning the key takeaways from the Industrial Catalyst market size and forecast highlights primary interests in growth drivers, emerging technological advancements, and the sustainability imperative. Users want to understand what factors will predominantly influence market expansion, how new technologies like AI and advanced materials will reshape the industry, and the role of environmental regulations in driving demand. There is also a strong desire for clarity on which regional markets are expected to exhibit the most significant growth and why, alongside insights into the competitive landscape and strategic opportunities for market participants. The central insight is that market growth will be primarily fueled by industrial demand, environmental policies, and continuous innovation in catalyst science.

The industrial catalyst market is set for substantial growth, driven by an escalating demand from a diverse array of end-use industries, particularly chemicals and petrochemicals, coupled with increasing environmental scrutiny worldwide. Manufacturers are heavily investing in research and development to create more efficient, selective, and sustainable catalyst solutions. The integration of advanced technologies such as artificial intelligence and nanotechnology is not merely a trend but a fundamental shift towards more intelligent and resource-efficient catalytic processes. This transformative period presents significant opportunities for companies that prioritize innovation, sustainability, and strategic partnerships, allowing them to capture a larger share of the expanding market. The market's future will be largely defined by its ability to balance industrial efficiency with ecological responsibility.

- Significant Market Expansion: The market is poised for robust growth, driven by industrial expansion and environmental regulations.

- Innovation as a Core Driver: Continuous R&D in catalyst materials and processes, including AI integration, is critical for competitive advantage.

- Sustainability Imperative: Green chemistry and eco-friendly catalyst solutions are becoming paramount due to stringent environmental policies.

- Emerging Economies as Growth Hubs: Asia Pacific, particularly China and India, will lead market growth due to rapid industrialization.

- Diversification of Applications: Catalysts are increasingly crucial across varied sectors, from energy to pharmaceuticals.

Industrial Catalyst Market Drivers Analysis

The industrial catalyst market is profoundly influenced by several key drivers, primarily stemming from the global expansion of various industrial sectors and the evolving regulatory landscape. One of the most significant drivers is the burgeoning demand from the chemical and petrochemical industries, which heavily rely on catalysts for efficient and selective production of a vast array of chemicals, polymers, and fuels. As these industries expand globally, particularly in emerging economies, the consumption of catalysts naturally follows suit. Furthermore, the increasing global focus on environmental protection and sustainability mandates the use of more efficient and cleaner catalytic processes, driving innovation and adoption of advanced catalyst technologies.

Another crucial driver is the continuous advancement in catalyst technology itself. Breakthroughs in nanotechnology, material science, and computational chemistry are leading to the development of novel catalysts with enhanced performance, longer lifespans, and greater selectivity, which in turn reduces operational costs and environmental impact for industries. This technological evolution not only meets current industrial demands but also creates new application possibilities. Additionally, the growing energy demand worldwide, particularly for cleaner fuels, fuels the need for catalysts in refining processes that produce low-sulfur fuels and other high-value petroleum products. The synergy of industrial growth, environmental regulations, and technological progress forms the bedrock of the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Chemical and Petrochemical Industry | +1.5-2.0% | Global, particularly APAC (China, India) | 2025-2033 (Long-term) |

| Stringent Environmental Regulations | +1.0-1.5% | North America, Europe, China | 2025-2033 (Continuous) |

| Technological Advancements in Catalyst Production | +0.8-1.2% | Global, R&D Hubs (USA, Germany, Japan) | 2025-2030 (Mid-term) |

| Increasing Demand for Cleaner Fuels | +0.7-1.0% | Global, especially emerging markets | 2025-2033 (Long-term) |

| Rising Investments in R&D for Novel Catalysts | +0.6-0.9% | Developed Economies (USA, Europe, Japan) | 2025-2033 (Long-term) |

Industrial Catalyst Market Restraints Analysis

Despite robust growth prospects, the industrial catalyst market faces several notable restraints that could temper its expansion. One primary concern is the volatility and fluctuating prices of raw materials. Many catalysts rely on noble metals like platinum, palladium, and rhodium, or rare earth elements, whose supply can be limited and prices highly susceptible to geopolitical events, mining disruptions, and economic shifts. Such price instability directly impacts manufacturing costs for catalyst producers and can lead to increased operational expenditures for end-users, potentially hindering adoption rates or prompting a search for more cost-effective alternatives.

Another significant restraint is the high capital expenditure associated with establishing and upgrading catalyst manufacturing facilities, especially for advanced and specialized catalysts. The complex production processes and stringent quality control requirements necessitate substantial investment, which can be a barrier to entry for new players and a financial burden for existing ones seeking to scale up or innovate. Furthermore, the inherent challenge of catalyst deactivation over time necessitates periodic replacement or regeneration, adding to the operational costs for industries. This deactivation also creates a substantial waste management challenge, as spent catalysts often contain hazardous materials, requiring costly and environmentally compliant disposal or recycling processes. These economic and environmental challenges collectively present headwinds for sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8-1.2% | Global | 2025-2033 (Continuous) |

| High Research and Development Costs | -0.5-0.8% | Global, particularly SMEs | 2025-2030 (Mid-term) |

| Stringent Environmental Regulations (Production side) | -0.4-0.7% | Developed Regions (Europe, North America) | 2025-2033 (Continuous) |

| Catalyst Deactivation and Disposal Challenges | -0.3-0.6% | Global, heavy industrial regions | 2025-2033 (Long-term) |

Industrial Catalyst Market Opportunities Analysis

The industrial catalyst market is replete with significant opportunities driven by evolving global demands and technological advancements. A primary area of opportunity lies in the burgeoning focus on sustainable and green chemistry. As industries globally strive to reduce their environmental footprint, there is an escalating demand for catalysts that facilitate eco-friendly processes, such as those that minimize waste, reduce energy consumption, or convert pollutants into valuable products. This trend opens avenues for the development and commercialization of bio-based catalysts, catalysts for CO2 conversion, and those enabling the production of biodegradable polymers, aligning with circular economy principles.

Another substantial opportunity stems from the rapid industrialization and economic growth in emerging economies, particularly across Asia Pacific, Latin America, and parts of Africa. These regions are witnessing a surge in chemical manufacturing, petrochemical refining, and automotive production, creating a vast untapped market for industrial catalysts. Furthermore, the continuous advancements in nanotechnology and materials science offer fertile ground for developing highly efficient and selective catalysts. These novel materials, such as MOFs, zeolites, and single-atom catalysts, promise to revolutionize catalytic processes by enabling reactions at milder conditions, improving yields, and offering longer operational lifespans, thereby creating new market niches and revenue streams for innovative players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable and Green Catalysts | +1.0-1.5% | Global, particularly Europe, North America | 2025-2033 (Long-term) |

| Rising Industrialization in Emerging Economies | +0.9-1.3% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| Advancements in Nanotechnology and Materials Science | +0.8-1.1% | Global, R&D Hubs | 2025-2030 (Mid-term) |

| Growing Focus on Biofuels and Renewable Energy | +0.7-1.0% | North America, Europe, Brazil | 2025-2033 (Long-term) |

Industrial Catalyst Market Challenges Impact Analysis

The industrial catalyst market faces several inherent challenges that demand innovative solutions and strategic adaptation. A significant challenge is the ongoing issue of catalyst deactivation, which occurs due to poisoning, coking, sintering, or leaching, ultimately leading to reduced efficiency and necessitating costly regeneration or replacement. Managing this deactivation while maintaining process continuity and product quality is a complex task for industries. The disposal of spent catalysts also presents a considerable environmental and economic challenge, as many contain heavy metals or hazardous substances that require specialized and expensive treatment to comply with strict environmental regulations, especially in developed economies.

Another prominent challenge is the increasing complexity of synthesizing new, highly specific, and efficient catalysts, particularly those designed for challenging reactions or harsh operating conditions. The research and development process is often protracted and capital-intensive, requiring advanced scientific expertise and state-of-the-art facilities. Scalability from laboratory synthesis to industrial production also poses significant hurdles, as maintaining catalyst performance and consistency at a larger scale can be difficult. Additionally, intense competition within the market, coupled with the need to constantly innovate to offer superior performance at competitive prices, puts considerable pressure on manufacturers to balance R&D investments with market viability. Overcoming these challenges is crucial for sustained growth and profitability in the industrial catalyst sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Catalyst Deactivation and Lifespan Extension | -0.7-1.0% | Global, All end-use industries | 2025-2033 (Continuous) |

| Disposal and Recycling of Spent Catalysts | -0.6-0.9% | Developed Regions (Europe, North America) | 2025-2033 (Continuous) |

| High Cost of Precious Metals in Catalysts | -0.5-0.8% | Global | 2025-2033 (Continuous) |

| Scalability of Novel Catalyst Technologies | -0.4-0.7% | Global, R&D focused regions | 2025-2030 (Mid-term) |

Industrial Catalyst Market - Updated Report Scope

This comprehensive market research report offers a detailed analysis of the industrial catalyst market, providing an in-depth understanding of its size, growth dynamics, key trends, and future projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape. It also includes a detailed segmentation analysis by type, application, and end-use industry, providing granular insights into demand patterns across various sectors. The report further covers a meticulous regional analysis, highlighting growth prospects and market characteristics across major geographical segments, alongside profiles of leading market participants and the impact of technological advancements, including artificial intelligence, on the market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 43.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Johnson Matthey, BASF SE, W.R. Grace & Co., Clariant AG, Evonik Industries AG, Albemarle Corporation, Honeywell International Inc., Dow Inc., ExxonMobil Chemical Company, Sinopec Group, LyondellBasell Industries N.V., Umicore, JGC Catalysts & Chemicals Ltd., Topsoe, Dorf Ketal, Shell Catalysts & Technologies, Arkema, Chevron Phillips Chemical Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial catalyst market is extensively segmented to provide a comprehensive understanding of its diverse applications and material compositions. This segmentation allows for granular analysis of market dynamics, identifying specific growth drivers and challenges within each category. The primary segmentation includes analysis by catalyst type, which broadly categorizes catalysts based on their chemical composition and function, such as metals, zeolites, and chemical compounds. Further breakdown within these types offers insights into the specific sub-segments driving innovation and demand, highlighting the preference for certain materials in particular industrial processes.

Beyond material type, the market is segmented by application and end-use industry. The application segment delineates the primary industrial processes where catalysts are utilized, including chemical synthesis, petroleum refining, and environmental applications. Each application area has unique requirements for catalyst performance and selectivity, influencing R&D efforts and market growth. The end-use industry segment provides a macro-level view of demand from sectors like chemical and petrochemical, automotive, and environmental, offering crucial insights into industry-specific adoption rates and future growth potential. This multi-faceted segmentation helps to pinpoint key market trends and strategic opportunities for stakeholders across the entire value chain.

- By Type:

- Metals (Precious Metals, Base Metals)

- Zeolites

- Chemical Compounds (Acids, Amines, Peroxides, Others)

- Biocatalysts (Enzymes, Microorganisms)

- By Application:

- Chemical Synthesis (Polymerization, Oxidation, Hydrogenation, Alkylation, Others)

- Petroleum Refining (Fluid Catalytic Cracking, Hydroprocessing, Reforming, Isomerization)

- Environmental (Automotive Emission Control, Industrial Emission Control)

- Polymerization

- Adsorbents

- Others (Food Processing, Pharmaceutical Synthesis)

- By End-Use Industry:

- Chemical & Petrochemical

- Automotive

- Polymer & Plastic

- Environmental

- Pharmaceutical

- Food & Beverage

- Others

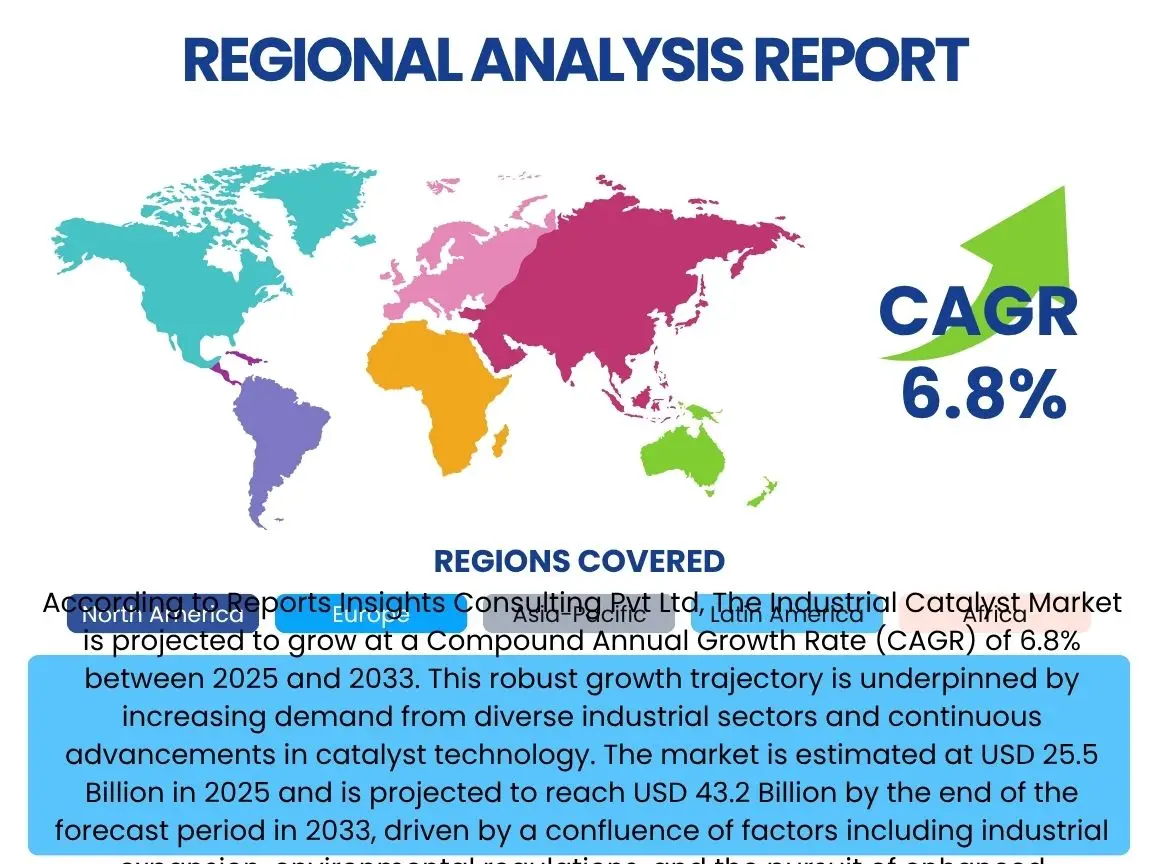

Regional Highlights

The global industrial catalyst market exhibits significant regional disparities in terms of market size, growth rates, and technological adoption, largely driven by differing industrial landscapes, environmental regulations, and economic development levels. Asia Pacific stands out as the fastest-growing and largest market, primarily propelled by rapid industrialization, burgeoning chemical and petrochemical industries, and increasing automotive production in countries like China and India. The region's expanding manufacturing base and growing energy demand necessitate a continuous supply of catalysts for various processes, including petroleum refining and environmental emission control. Government initiatives promoting sustainable industrial practices also contribute to the demand for advanced catalysts in this region.

North America and Europe represent mature markets characterized by stringent environmental regulations and a strong focus on advanced and specialty catalysts. These regions are leaders in catalyst research and development, particularly for applications in sustainable chemistry, emission reduction, and high-performance materials. While growth rates may be lower compared to Asia Pacific, the demand for innovative and efficient catalysts remains high dueiven by the need to optimize existing processes and comply with evolving environmental standards. Latin America and the Middle East & Africa regions are emerging markets, with growth driven by investments in refining capacities, petrochemical expansion, and developing manufacturing sectors. These regions offer significant long-term growth potential as their industrial infrastructure continues to evolve, increasing the demand for catalysts across various applications.

- Asia Pacific (APAC): Dominant market with highest growth due to rapid industrialization, expanding chemical and petrochemical sectors, and increasing automotive production in China and India.

- North America: Mature market characterized by advanced research, stringent environmental regulations, and high demand for specialty and high-performance catalysts.

- Europe: Focus on green chemistry and sustainable manufacturing, driving demand for eco-friendly and energy-efficient catalysts, with significant R&D activities.

- Latin America: Growing market driven by expanding refining capacities, agricultural chemical production, and industrial development, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): Emerging market with significant investments in oil and gas refining, petrochemical production, and industrial diversification, leading to increased catalyst consumption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Catalyst Market.- Johnson Matthey

- BASF SE

- W.R. Grace & Co.

- Clariant AG

- Evonik Industries AG

- Albemarle Corporation

- Honeywell International Inc.

- Dow Inc.

- ExxonMobil Chemical Company

- Sinopec Group

- LyondellBasell Industries N.V.

- Umicore

- JGC Catalysts & Chemicals Ltd.

- Topsoe

- Dorf Ketal

- Shell Catalysts & Technologies

- Arkema

- Chevron Phillips Chemical Company

Frequently Asked Questions

What is the projected growth rate for the Industrial Catalyst market?

The Industrial Catalyst market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 43.2 Billion by the end of the forecast period.

Which factors are primarily driving the growth of the Industrial Catalyst market?

Key growth drivers include the expanding chemical and petrochemical industries, increasingly stringent environmental regulations promoting cleaner production, and continuous technological advancements in catalyst research and development.

How is Artificial Intelligence impacting the Industrial Catalyst sector?

AI is significantly impacting the sector by accelerating catalyst discovery, optimizing industrial processes for enhanced efficiency, enabling predictive maintenance for longer catalyst lifespan, and improving overall quality control.

Which region is expected to lead the Industrial Catalyst market growth?

Asia Pacific is anticipated to be the largest and fastest-growing region in the Industrial Catalyst market due to rapid industrialization and significant expansion in its chemical, petrochemical, and automotive sectors.

What are the main challenges faced by the Industrial Catalyst market?

Major challenges include catalyst deactivation and the need for extended lifespan, the complex and costly disposal and recycling of spent catalysts, and the high research and development expenses associated with creating novel catalyst technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted